Smart TV Market Report Scope & Overview:

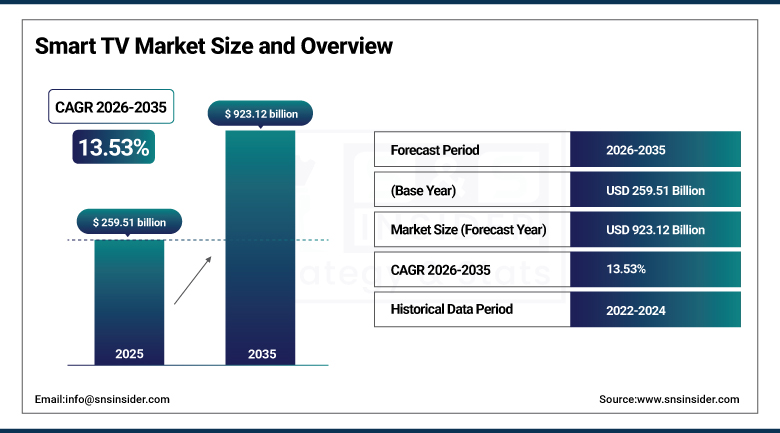

The Smart TV Market was valued at USD 259.51 Billion in 2025 and is expected to reach USD 923.12 Billion by 2035, growing at a CAGR of 13.53% from 2026–2035.

The global smart TV market is growing at an exceptional and transformative pace. Smart TVs are television sets that integrate internet connectivity and an operating system, allowing users to access streaming services, apps, web browsing, voice assistant integration, and smart home device control directly on the display without additional hardware. The market is rapidly evolving driven by product performance improvements including 4K and 8K resolution, higher refresh rates, and innovative technology progression including AI-based content recommendations, voice control integration, and gaming mode enhancement. Rising OTT streaming platform adoption and growing consumer preference for connected home entertainment ecosystems collectively sustain the market’s above-average growth trajectory.

In 2024, Samsung launched its Neo QLED 8K QN900D television with AI-powered upscaling that uses a neural quantum processor to enhance lower-resolution content to near-8K quality in real time, combined with an anti-reflection matte display and built-in Tizen OS with SmartThings smart home integration. The product demonstrates the commercial direction of premium smart TV development toward AI-enhanced picture processing whose intelligent upscaling creates display quality improvement from existing streaming content that sustains consumer willingness to invest in premium 8K specification beyond the currently limited native 8K content availability.

Market Size and Forecast

-

Market Size in 2026E: USD 294.73 Billion

-

Market Size by 2035: USD 932.12 Billion

-

CAGR: 13.53% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Smart TV Market - Request Free Sample Report

Smart TV Market Trends

-

AI-powered smart TV systems with content recommendation engines, voice assistants, and intelligent picture optimization are enhancing user experience and driving preference for connected displays over traditional televisions.

-

Advanced display technologies such as Mini-LED and QD-OLED are improving brightness control, contrast accuracy, and color performance, enabling premium viewing quality beyond conventional LED-LCD panels.

-

Gaming-focused smart TV features including HDMI 2.1, 4K@120Hz refresh rate, and variable refresh rate (VRR) are accelerating adoption among console and cloud gaming users seeking low-latency performance.

-

Smart home integration with ecosystems such as Alexa, Google Home, and Apple HomeKit is positioning smart TVs as central control hubs for connected home devices and automation.

-

Declining panel costs and manufacturing scale efficiencies are driving rapid adoption of large-screen (75-inch+) smart TVs, expanding home theater experiences at more accessible price points.

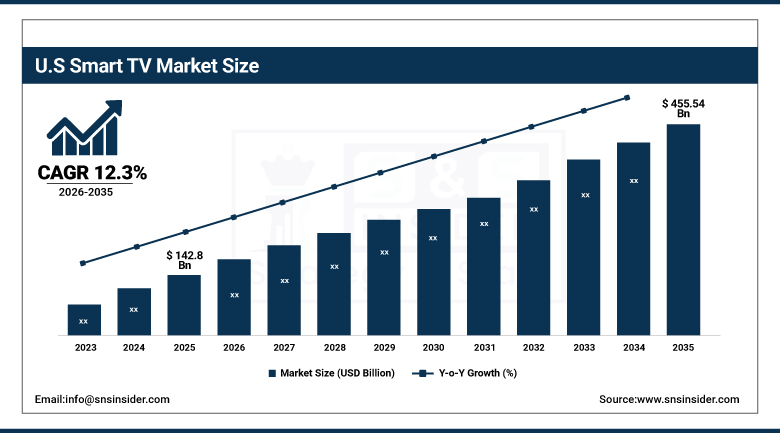

The U.S. Smart TV Market Outlook

The U.S. smart TV market was valued at approximately USD 142.8 Billion in 2025 and is expected to reach approximately USD 455.54 Billion by 2035, growing at a CAGR of approximately 12.3 %.

The U.S. Smart TV Market is the most commercially sophisticated national smart TV market within North America. Samsung, LG, Sony, TCL, Hisense, and Roku TV’s U.S. commercial operations collectively define the domestic smart TV landscape. The U.S.’s extraordinary OTT streaming ecosystem, encompassing Netflix, Disney+, Amazon Prime Video, HBO Max, Peacock, and Apple TV+, creates the world’s most content-rich streaming environment whose smart TV access motivation sustains above-average premium specification investment. The U.S. consumer’s above-average disposable income creates premium 65-inch and above OLED, QLED, and Neo QLED specification accessibility that sustains per-unit commercial value growth.

LG Electronics launched its 2024 OLED evo G4 series with the world’s first integrated OLED panel with a built-in heatsink, enabling 42% brighter peak luminance than prior OLED generations, combined with the AI-powered Alpha 11 processor whose intelligent picture and sound optimization creates adaptive display calibration for different content types and viewing environments. The OLED evo G4’s self-luminous pixel technology eliminates the backlight halo effect and local dimming approximation that LED LCD alternatives create, sustaining OLED’s premium display quality positioning at above-commodity pricing.

Smart TV Market Segment Analysis

-

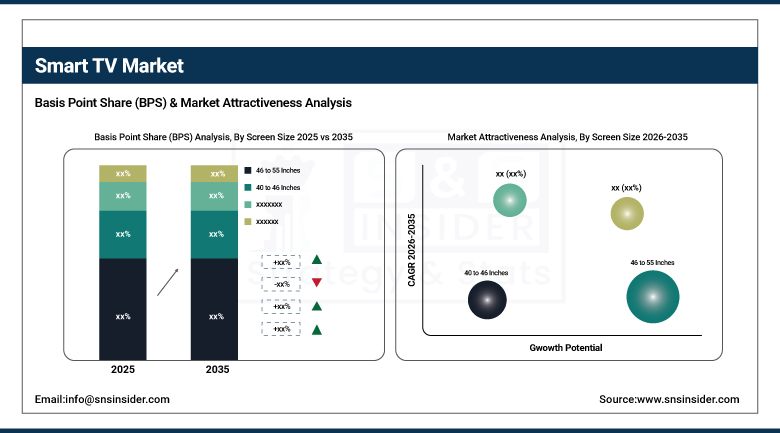

By Screen Size, the 46 to 55-inch segment dominated the Market with 34.6% share in 2025, while the above 65-inch segment is expected to witness the fastest CAGR from 2026 to 2035.

-

By Resolution, the 4K ultra-HD (UHD) segment dominated the market with approximately 48% share in 2025, while the 8K UHD segment is the fastest growing.

-

By Operating System, the android TV/Google TV segment dominated the market with approximately 43% share in 2025, while the Roku OS segment is the fastest growing.

-

By Distribution Channel, the online/e-commerce segment dominated the market with the highest share in 2025, while the offline/retail stores segment serves the premium in-store demonstration experience for consumers.

By Screen Size, 46–55-inch dominates, above 65-inch grows fastest

The 46 to 55-inch segment retained the dominant screen size position with 34.6% of the smart TV market in 2025. This screen size range’s commercial primacy reflects its position as the mass-market sweet spot whose balance of immersive viewing area, comfortable viewing distance in standard living rooms, 4K content appreciation at typical seating distances, and value-for-money premium feature accessibility creates the highest-volume smart TV specification category. Each mainstream consumer whose living room dimensions, seating distance, and budget create 46-55-inch specification creates procurement whose aggregate across the global consumer electronics market creates commercial scale.

Above 65-inch is the fastest-growing segment because the extraordinary panel price reduction driven by LCD manufacturing scale economics is creating large-screen specification accessibility for budget segments that previously required premium price tolerance. Each percentage point reduction in 65-inch and above panel pricing creates new addressable consumer demographic whose size aspiration was previously price-constrained. The home theatre trend’s growing consumer adoption, whose desire for cinematic viewing experience at home creates 75-inch and above specification motivation, sustains large-screen segment’s fastest-growing commercial momentum.

By Resolution, 4K UHD dominates, 8K grows fastest

4K Ultra HD retained the dominant resolution position with approximately 48% of the smart TV market in 2025. 4K’s commercial primacy reflects its position as the mainstream premium resolution standard whose streaming platform library depth, Netflix’s, Disney+’s, and Amazon Prime Video’s extensive 4K content catalogues, creates daily consumption motivation that justifies the 4K specification premium over Full HD alternatives. Each gaming console’s native 4K output, each streaming service’s 4K tier’s visual quality improvement, and each 4K Blu-ray’s physical media quality demonstration collectively create consumer motivation that sustains 4K’s dominant specification share.

8K UHD is the fastest-growing resolution because AI upscaling technology’s progressive improvement is creating 8K-quality viewing experience from 4K and even lower-resolution source content whose artificial intelligence processing converts existing content to near-native 8K quality. Samsung’s Neural Quantum Processor 8K, LG’s Alpha 11 AI Processor, and Sony’s Cognitive Processor XR collectively demonstrate the AI picture enhancement ecosystem whose upscaling capability sustains 8K specification investment ahead of native 8K content availability. Each premium consumer who adopts 8K as a future-proof resolution investment creates above-average per-unit commercial value.

By OS, Android TV dominates, Roku grows fastest

Android TV and Google TV retained the dominant OS position with approximately 43% of the smart TV market in 2025. Android TV’s commercial primacy reflects its universal availability across the broadest range of smart TV brands whose Play Store access creates the largest streaming app ecosystem of any smart TV operating system. The Google Assistant’s voice control, Chromecast content mirroring’s ecosystem integration, and the familiar Android UX’s consumer comfort collectively sustain Android TV’s dominant OS market position. Each new smart TV brand that adopts Android TV/Google TV creates OS adoption that compounds with global brand distribution.

Roku is the fastest-growing OS because its simplified, clutter-free interface designed specifically for streaming content accessibility creates user experience advantages over Android TV’s and Fire TV’s app-heavy navigation for the mainstream consumer whose primary use case is streaming content rather than smart home management or app installation. The Roku Channel’s free ad-supported streaming content creates platform value whose AVOD model sustains consumer engagement without subscription requirement. Strategic partnerships with Hisense, TCL, and multiple OEM manufacturers create hardware distribution whose breadth expands Roku’s ecosystem.

By Distribution, online dominates, retail serves premium demonstration

Online distribution retained the dominant channel position in the smart TV market in 2025. E-commerce’s commercial primacy reflects the consumer’s progressive purchase comfort for large consumer electronics through online channels whose price comparison, review research, and home delivery convenience create specification and purchase decision efficiency that physical retail cannot match at equivalent purchase outcome confidence. Amazon, Best Buy’s online channel, Walmart.com, and brand direct-to-consumer websites collectively create online smart TV procurement infrastructure whose aggregate across the global consumer electronics e-commerce creates commercial scale.

Offline retail remains commercially significant for premium smart TV specification because the consumer’s high-value OLED, QLED, and 8K purchase decision creates physical demonstration motivation whose in-store display quality assessment creates purchase confidence that online specification research cannot replicate with equivalent sensory validation. Each premium consumer whose display quality investment requires physical assessment before commitment creates retail store visit whose premium specification conversion sustains above-average offline revenue concentration at the market’s premium segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

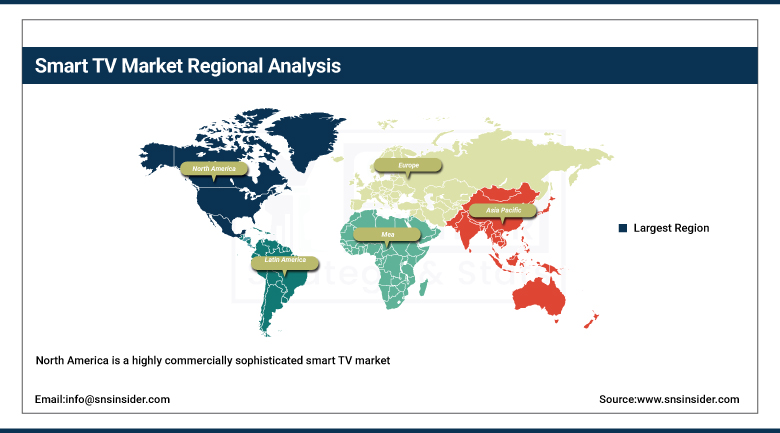

North America Smart TV Market Insights

North America is a highly commercially sophisticated smart TV market where Samsung, LG, Sony, TCL, and Hisense’s commercial operations, the extraordinary OTT streaming ecosystem, and the consumer’s above-average disposable income create premium specification adoption. The United States accounts for approximately 87.4% of North American revenues through its above-average per-unit commercial value, the premium OLED and QLED market’s specification motivation, and the gaming ecosystem’s high-refresh-rate 4K smart TV procurement.

Canada contributes approximately 12.6% of North American revenues through its consumer electronics adoption, the growing streaming market’s content consumption, and the premium specification market’s OLED and QLED adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Smart TV Market Insights

Europe is a technically sophisticated smart TV market where premium display specification, European content regulation’s local streaming platform creation, and the consumer’s above-average feature discernment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its premium consumer electronics market, the Bundesliga sports streaming’s smart TV consumption motivation, and the home entertainment sector’s advanced display specification.

France, the United Kingdom, and Italy are significant secondary markets where OTT platform adoption, sports rights streaming, and the consumer electronics replacement cycle create consistent smart TV procurement.

Asia Pacific Smart TV Market Insights

Asia Pacific dominated the global smart TV market in 2025 as both the largest and fastest-growing regional market with the highest revenue share and above-average CAGR. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary consumer electronics market scale, the domestic smart TV manufacturer’s competitive innovation, and the rising middle class’s premium display adoption. China’s Skyworth, TCL, Haier, and Hisense collectively represent the domestic brand ecosystem whose scale creates commercial concentration.

South Korea’s Samsung and LG’s global premium smart TV leadership, Japan’s advanced consumer electronics adoption, and India’s rapidly growing consumer electronics market create significant secondary markets whose combined procurement sustains Asia Pacific’s dominant regional commercial position.

MEA & Latin America Smart TV Market Insights

The MEA and Latin America Smart TV markets are witnessing strong growth driven by rising digital entertainment consumption and expanding streaming ecosystems. In the MEA region, Saudi Arabia dominates with approximately 31.2% share, supported by premium consumer electronics adoption, rapid expansion of the entertainment sector, and high demand from gaming communities for advanced display technologies.

In Latin America, Brazil leads with around 44.2% share, fueled by a large consumer base, increasing penetration of streaming platforms, and strong sports-driven viewership, particularly football content. Both regions are benefiting from improving internet infrastructure and growing preference for large-screen smart TVs.

Market Dynamics

Growth Drivers: OTT streaming platform proliferation and 4K/8K content ecosystem creating premium smart TV investment motivation

OTT streaming platform proliferation is the smart TV market’s most commercially certain primary growth driver. Netflix’s 270+ million subscribers, Disney+’s 150+ million, Amazon Prime Video’s 200+ million, and the extraordinary global streaming content investment collectively create daily smart TV consumption motivation whose content library depth sustains consumer willingness to invest in premium smart TV specification. Each new streaming platform launch that creates exclusive content creates smart TV access motivation whose value proposition sustains hardware investment. The cord-cutting trend’s progressive replacement of cable television with OTT streaming creates structural smart TV demand that compounds with each new streaming subscription.

High-speed internet penetration’s global expansion, driven by 5G mobile broadband, fiber optic broadband infrastructure, and government digital connectivity investment, is creating smart TV functionality access for previously network-constrained demographics. Each household that gains reliable high-speed internet access creates smart TV streaming functionality activation whose value realization sustains hardware upgrade motivation.

Restraints: Market saturation in developed economies and short replacement cycle creating upgrade motivation challenge

Smart TV market maturity in developed market consumer segments creates household penetration saturation where replacement demand replaces net new unit sales. Each household that already owns a functional smart TV creates replacement-only procurement whose 7–10-year typical replacement cycle moderates annual unit sales below the addressable household universe. The functional adequacy of 4K smart TVs purchased 3-5 years ago creates specification inertia that moderates upgrade motivation below the available premium display technology’s potential adoption.

Panel price deflationary pressure creating per-unit revenue decline moderates market value growth below unit volume growth. Each annual price reduction that creates larger screen accessibility for budget segments reduces per-unit commercial value whose aggregate moderates revenue growth relative to unit shipment growth.

Opportunities: 8K content ecosystem and AI-powered smart TV personal entertainment assistant

8K content ecosystem development through terrestrial 8K broadcasting in Japan, 8K YouTube content, and AI upscaling’s content enhancement creates progressive 8K specification motivation whose combined native and AI-enhanced content creates consumer adoption momentum. Each 8K content source addition creates 8K smart TV specification motivation whose commercial value compounds with premium consumer adoption.

AI-powered smart TV personal entertainment assistant capability, whose content preference learning, viewing habit adaptation, and proactive recommendation intelligence creates value beyond simple streaming aggregation, creates premium platform differentiation whose subscription service revenue sustains manufacturer investment in AI capability development.

Recent Developments:

-

2026: LG Electronics introduced next-generation OLED evo smart TVs featuring improved tandem OLED brightness architecture, enhanced webOS AI recommendation engine, and expanded 4K 120Hz gaming capabilities.

-

2025: TCL expanded its QM7K and QM8K Mini-LED smart TV lineup with up to 144Hz refresh rate, 4K resolution, and Google TV integration, strengthening high-brightness QD-Mini LED performance.

-

2025: Samsung advanced its Neo QLED smart TV series by integrating AI-powered picture processing with up to 4K 165Hz gaming support and enhanced anti-glare technology, improving HDR performance.

Smart TV Market key players are:

-

Samsung Electronics Co., Ltd. (Tizen OS)

-

LG Electronics Inc. (webOS)

-

Sony Corporation (BRAVIA Google TV)

-

TCL Electronics Holdings Ltd. (Google TV)

-

Hisense Group Co., Ltd.

-

Philips (TP Vision)

-

Panasonic Corporation

-

Skyworth Digital Holdings Co., Ltd.

-

Xiaomi Corporation (MIUI TV)

-

Haier Group Corporation

-

Vizio Inc. (WatchFree+)

-

Roku Inc. (Roku OS TVs)

-

Amazon.com Inc. (Fire TV)

-

Realme

-

Toshiba Corporation

-

Sharp Corporation (Aquos TV)

-

Grundig (Arçelik)

-

Vestel Electronics Sanayi ve Ticaret A.Ş.

-

Changhong Electric Co., Ltd.

-

OnePlus

Smart TV Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 259.51 Billion |

| Market Size by 2035 | USD 923.12 Billion |

| CAGR | CAGR of 13.53% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Screen Size (Below 32 Inches, 32 to 40 Inches, 40 to 46 Inches, 46 to 55 Inches, Above 65 Inches) • By Resolution (HD/720p, Full HD/1080p, 4K Ultra HD/UHD, 8K UHD) • By Operating System (Android TV/Google TV, Tizen OS/Samsung, webOS/LG, Roku, Fire TV OS/Amazon, Others) • By Distribution Channel (Online/E-Commerce, Offline/Retail Stores) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Electronics Co., Ltd. (Tizen OS), LG Electronics Inc. (webOS), Sony Corporation (BRAVIA Google TV), TCL Electronics Holdings Ltd. (Google TV), Hisense Group Co., Ltd., Philips (TP Vision), Panasonic Corporation, Skyworth Digital Holdings Co., Ltd., Xiaomi Corporation (MIUI TV), Haier Group Corporation, Vizio Inc. (WatchFree+), Roku Inc. (Roku OS TVs), Amazon.com Inc. (Fire TV), Realme, Toshiba Corporation, Sharp Corporation (Aquos TV), Grundig (Arçelik), Vestel Electronics Sanayi ve Ticaret A.Ş., Changhong Electric Co., Ltd., OnePlus |

Frequently Asked Questions

The Smart TV Market is expected to grow at a CAGR of 13.53% from 2026 to 2035.

The Smart TV Market was valued at USD 259.51 Billion in 2025.

Rapidly evolving product performance through 4K and 8K resolution, higher refresh rates, and HDR technology, combined with innovative AI-based content recommendations.

The 46 to 55-inch segment dominated the Smart TV Market with 34.6% share in 2025.

Asia Pacific dominated the Smart TV Market in 2025 with the highest revenue share and is also the fastest-growing region.

Get in Touch