Transcatheter Aortic Valve Replacement Market Report Scope & Overview:

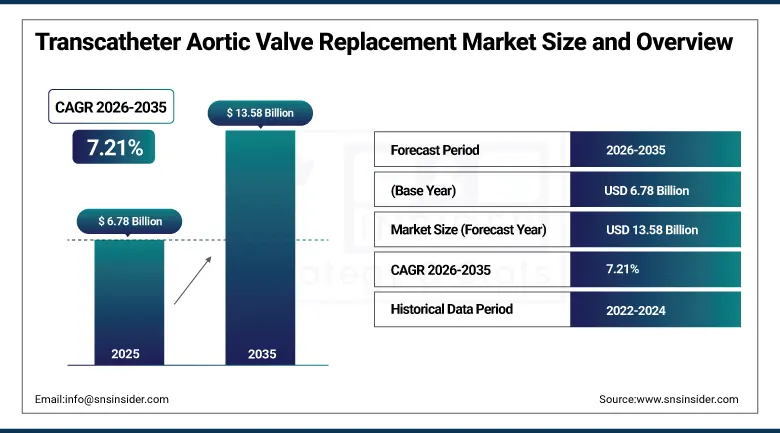

The Transcatheter Aortic Valve Replacement Market was valued at USD 6.78 billion in 2025 and is expected to reach USD 13.58 billion by 2035, growing at a CAGR of 7.21% from 2026–2035.

The transcatheter aortic valve replacement market is witnessing strong growth in the global market owing to increasing prevalence of aortic stenosis and structural heart diseases. Rising preference for minimally invasive cardiac procedures is driving adoption across hospitals and specialized cardiac centers. Expanding geriatric population and higher surgical risk patients are increasing TAVR utilization. Technological advancements in balloon-expandable and self-expanding valves are improving procedural outcomes. Growing healthcare infrastructure and expanding catheter-based treatment access are further accelerating market growth.

According to the U.S. Centers for Medicare & Medicaid Services & Transcatheter Valve Therapy Registry and American College of Cardiology 2025 clinical outcomes reporting, transcatheter aortic valve replacement volumes have continued to rise annually across the United States, with procedural expansion driven by inclusion of low-risk patients. As per peer-reviewed JAMA Cardiology 2025 registry analysis of 410,720 TAVR cases, redo-TAVR accounted for 2,374 procedures, representing a growing proportion of total interventions, while over 87% of patients with untreated severe aortic stenosis underwent valve replacement within 4 years of diagnosis in major clinical cohorts.

Market Size and Forecast

-

Market Size 2026E: USD 7.26 billion

-

Market Size 2035: USD 13.58 billion

-

CAGR (2026 - 2035): 7.21%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Transcatheter Aortic Valve Replacement Market - Request Free Sample Report

Transcatheter Aortic Valve Replacement Market Trends

-

Innovations in both balloon-expandable and self-expanding valves are leading to improved procedural success and improved survival among patients.

-

With advanced imaging tools and precision in delivery methods, there have been reductions in complication rates in transcatheter aortic valve replacement surgeries.

-

Use of transfemoral procedures is being increasingly preferred to enable less invasive and more accessible approaches for aortic valve replacement.

-

Increased use of minimally invasive cardiac surgeries is leading to shorter stay in hospitals along with faster healing processes.

-

Increasing popularity of ambulatory surgical facilities is aiding the use of minimally invasive approaches for valve replacements and other cardiovascular procedures.

-

Rising medical awareness and acceptance of catheter-based interventions by doctors and clinicians has led to increased need for minimally invasive options.

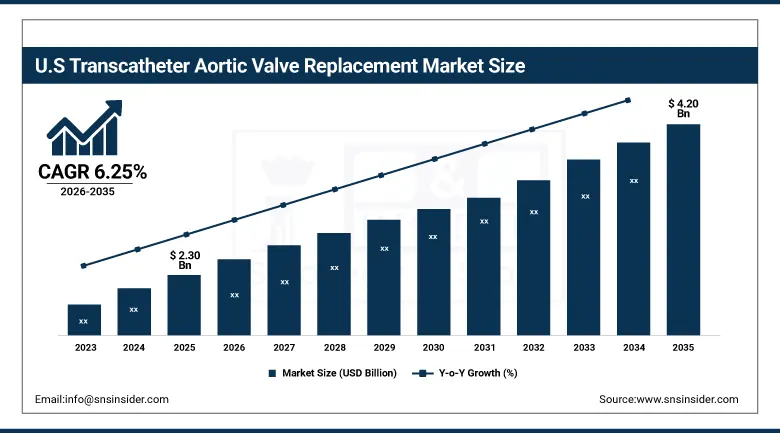

U.S. Transcatheter Aortic Valve Replacement Market Size Outlook.

The U.S. Transcatheter Aortic Valve Replacement Market was valued at USD 2.30 billion in 2025 and is expected to reach around USD 4.20 billion by 2035, growing at a CAGR of 6.25% from 2026–2035.

The U.S. transcatheter aortic valve replacement market is growing consistently owing to high prevalence of aortic stenosis. Rising adoption of minimally invasive cardiac procedures is driving strong demand across hospitals and cardiac catheterization labs. The presence of advanced healthcare infrastructure and skilled cardiac surgeons has supported market expansion. Increased healthcare spending and rapid adoption of innovative valve technologies have generated higher procedural volumes. Development of self-expanding valves, transfemoral access, and advanced imaging systems is further driving market growth.

As per CMS-supported clinical trial, more than 90% of patients undergoing aortic valve replacement in modern the U.S. trials are aged above 70 years, reflecting high geriatric adoption. Additionally, clinical outcome registries such as the STS/ACC TVT Registry continuously track procedural safety and post-operative outcomes across all the U.S. approved TAVR systems.

Transcatheter Aortic Valve Replacement Market Segment Analysis

-

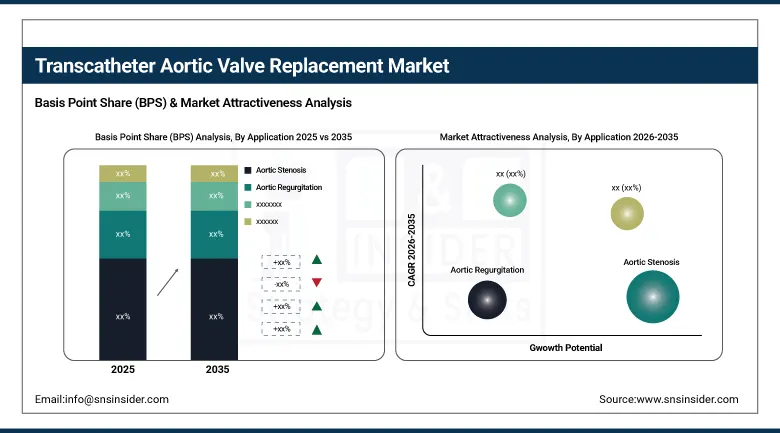

By Application, aortic stenosis dominated the market with 82.40% share in 2025; while aortic regurgitation is the fastest growing segment with CAGR of 14.21% during 2026 to 2035.

-

By Procedure Type, transfemoral dominated the market with 88.58% share in 2025; while transapical are the fastest growing segment with CAGR of 13.88% during 2026 to 2035.

-

By End User, hospitals dominated the market with 76.50% share in 2025; while ambulatory surgical centers are the fastest growing segment with CAGR of 15.40% during 2026 to 2035.

-

By Valve Type, balloon-expandable dominated the market with 54.60% share in 2025; while self-expanding is the fastest growing segment with CAGR of 9.84% during 2026 to 2035.

By Application, aortic stenosis dominated the transcatheter aortic valve replacement market, while aortic regurgitation is the fastest growing segment.

The Aortic Stenosis segment held the dominated revenue share in the transcatheter aortic valve replacement market in 2025. This can be attributed to the widespread prevalence rate of the disease worldwide amongst the elderly population, combined with clinical necessity. Improved screening practices, increasing rates of diagnoses, and established treatment guidelines also said the market growth of this segment. High success rate of procedures and robust reimbursement environment also drive its market dominance.

Aortic Regurgitation segment is projected to register the fastest CAGR in the forecast period from 2026-2035 due to the growing use of the transcatheter procedure to treat complex conditions of valve defects. Awareness about the disease, improvements in imaging technology, and rising incidence rates are facilitating earlier diagnosis and increasing patient eligibility. Improvements in valve design have enabled more procedural success, and increased numbers of risky surgery patients are also driving market growth.

By Procedure Type, transfemoral dominated the transcatheter aortic valve replacement market, while transapical is the fastest growing segment.

Transfemoral segment was the leading product segment of the transcatheter aortic valve replacement market in 2025 by virtue of having the dominated revenue share. The key factor behind the predominance of this segment is that it is minimally invasive in nature and offers higher rates of procedural success. It enables quick recovery and short hospital stay when compared with other procedures. Physician preference along with wide clinical adoption in hospitals is another reason behind the leadership of this segment. Technological advances in catheter delivery and imaging are boosting the use of the procedure among high-risk cardiac patients.

The Transapical segment is predicted to have the fastest CAGR from 2026–2035 because of the applicability of this technique in patients who are not fit for transfemoral approach. It involves a direct approach to the heart, helping in treating difficult anatomy cases. Its use among high risk and elderly patients is rising and driving growth in demand. Developments in surgical techniques and increasing compatibility with devices are boosting its use.

By End User, hospitals dominated the transcatheter aortic valve replacement market, while ambulatory surgical centers are the fastest growing segment.

Hospitals emerged as the dominated segment of the transcatheter aortic valve replacement market in 2025, with the highest share of revenues. The segment is characterized by availability of advanced catheterization labs and experienced cardiac surgeons. Hospitals undertake complex and high-risk TAVR procedures that require intensive care services. In addition, higher influx of patients along with existing reimbursement mechanisms makes hospitals preferred for undergoing TAVR procedures. Incorporation of advanced technology such as imaging systems and surgical equipment helps in increasing success rate of procedure.

Ambulatory Surgical Centers segment will witness rapid growth during the forecast period owing to growing preference for minimally invasive out-patient cardiac procedures. Low cost involved in hospitalization and shorter recovery time is encouraging more and more people opting for ASCs. Transfemoral TAVR procedures can be performed in an ASC with advanced technology making sure that patients can be discharged within the same day. Growing number of cardiac ambulatory centers and supportive reimbursement scenario further propel the growth of the segment.

By Valve Type, balloon-expandable dominated the transcatheter aortic valve replacement market, while self-expanding is the fastest growing segment.

The Balloon-Expandable segment captured dominated revenue share in the transcatheter aortic valve replacement market in 2025 because of high procedural accuracy along with excellent clinical outcomes during the treatment of aortic stenosis. The high precision in placing these valves, combined with low paravalvular leakage rates, has helped establish their prominence in the market. In addition, extensive experience among physicians and easy availability of reimbursements for these devices have led to their dominance in the market.

The Self-Expanding segment will witness fast-paced growth from 2026 to 2035 owing to the rising popularity of flexible and minimally-invasive valves. These valves ensure greater flexibility in treating cases with complex anatomies and help reduce procedural complications. Their adoption in older, high-risk patients has driven their adoption. Technological advancements, along with the ease of repositioning, continue to improve their efficiency and effectiveness. Growth in transfemoral procedures and approval of products will fuel the growth of this segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

86.40% |

|

Europe |

Germany |

29.10% |

|

Asia Pacific |

China |

43.60% |

|

Middle East & Africa |

UAE |

19.30% |

|

Latin America |

Brazil |

48.20% |

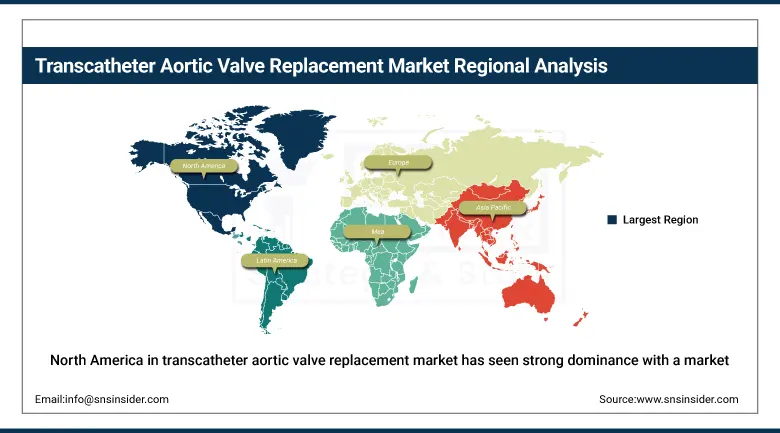

North America Transcatheter Aortic Valve Replacement Market Insights.

North America in transcatheter aortic valve replacement market has seen strong dominance with a market share of about 39.20% in 2025 due to advanced cardiac care infrastructure and high procedure adoption rates. The region benefits from strong demand in minimally invasive valve replacement procedures and structural heart interventions. Increasing prevalence of aortic stenosis and aging population is driving expansion across the United States and Canada. Rising adoption of transfemoral procedures and self-expanding valves is further supporting market leadership. Strong clinical research activity is strengthening innovation in TAVR technologies.

According to the Centers for Medicare & Medicaid Services & National Coverage Determination and STS/ACC TVT Registry evidence 2025, transcatheter aortic valve replacement in North America is still governed by Coverage with Evidence Development and thus requires involvement in approved clinical registries to facilitate outcome assessment.

As per CDC-linked cardiovascular surveillance datasets and peer-reviewed registry analyses, over 80% of TAVR procedures in the U.S. are performed in patients aged 70 years or older, with procedural stroke rates reported below 5% and in-hospital mortality consistently under 3% across large registries. Additionally, transfemoral access accounts for more than 75% of implantation approaches, indicating strong procedural standardization in 2025.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Transcatheter Aortic Valve Replacement Market Insights.

Europe transcatheter aortic valve replacement market is characterized by strong growth in 2025 owing to favorable reimbursement policies and expanding structural heart programs. The major countries contributing towards demand include Germany, France, United Kingdom, and Italy. Rising prevalence of degenerative aortic stenosis is fueling procedure volumes across cardiac centers. Increasing adoption of minimally invasive valve implantation and growing geriatric population is propelling market usage. Expansion of heart valve clinics and hybrid operating rooms is further improving clinical access.

According to the European Society of Cardiology and EuroPCR registry analyses in European cardiovascular intervention reports, transcatheter aortic valve replacement procedures in Europe have shown continuous expansion, with over 96% of procedures performed via transfemoral access in patients aged ≥85 years and 98% in women in advanced age groups.

Asia Pacific Transcatheter Aortic Valve Replacement Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the transcatheter aortic valve replacement market during the forecast period with a market share of about 8.71% in 2025. Rapid expansion of cardiac care infrastructure and increasing prevalence of cardiovascular diseases are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Growing hospital networks and rising awareness of minimally invasive treatments are significantly boosting adoption. Increasing affordability of advanced valve systems is further accelerating market growth. Large scale investments in interventional cardiology and training programs support strong regional outlook.

According to the International Trade Administration and Asia Pacific cardiovascular registry in peer-reviewed clinical reports, transcatheter aortic valve replacement procedures in Asia Pacific are expanding with registry coverage exceeding 1,000–2,500 recorded cases across multicentre.

As per the American Heart Association epidemiological estimates cited in 2025 clinical literature, aortic stenosis prevalence affects approximately 3%–4% of individuals over 75 years, a rapidly growing demographic group in Japan, China, and South Korea. Clinical adoption studies further indicate that minimally invasive valve replacement usage has increased from 11% to 23% in recent surgical practice trends, reflecting measurable procedural uptake across advanced cardiac centers in the region.

Middle East & Africa and Latin America Transcatheter Aortic Valve Replacement Market Insights.

The Middle East & Africa along with Latin American countries are experiencing steady growth on account of increasing healthcare infrastructure development and rising cardiac disease burden. Some of the countries that are fast becoming prominent centers of demand include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Investments in advanced cardiac catheterization labs and specialized heart centers have been facilitating market growth. Growing requirement for minimally invasive valve replacement procedures is driving clinical adoption. Expansion of private healthcare systems is further supporting access to advanced therapies.

As per recent clinical registry updates published in 2025, over 98,000 TAVR procedures were performed annually in the U.S., while surgical aortic valve replacement volumes declined by 36% over the same period. These indicators reflect accelerating adoption trends that influence MEA and Latin America diffusion patterns through procedural training and guideline convergence.

Market Dynamics

Growth Drivers: Technological advancements in valve design and minimally invasive catheter-based delivery systems improving outcomes

Innovations in the areas of balloon expandable valves and self-expanding valves have resulted in better procedural success rates and outcomes for patients. Improved guidance imaging and delivery precision have reduced any complications that can arise during the procedure. The development of transfemoral access methods has rendered the process minimally invasive and more convenient. Advanced biomaterial integration into the process has increased the longevity of the valve as well as improved its biocompatibility. More clinical trials and regulatory approvals have made these products available.

According to the U.S. Food and Drug Administration device approvals and the American College of Cardiology 2025 clinical trial, transcatheter aortic valve replacement has expanded across all surgical risk categories, with randomized evidence showing a 15.5% composite rate of death or disabling stroke at five years in low-risk cohorts versus 16.4% with surgery.

According to ACC and JACC 2025, self-expandable and balloon-expandable next generation valves show stable hemodynamics and similar follow up completion rate of more than 91%, while FDA-approved valves are adopting sealing skirts, reduced delivery sheaths, and better commissural alignment systems.

Restraints: Strict regulatory approvals and procedural complexity increasing barriers to widespread clinical adoption

The complexity involved in securing the required regulatory approval for transcatheter heart valves is another reason why the introduction of such technology takes longer than anticipated into the market place. In addition, the complex processes involved in carrying out clinical trials and validation take even longer before the product can be introduced into the market. The complexity of the entire process requires that operators be trained in special ways. Risks such as stroke and blood vessel injuries require strict patient selection processes. Some places do not have skilled operators.

Opportunities: Expanding minimally invasive treatment adoption and outpatient cardiac care creating strong growth potential

Greater inclination towards minimal invasive treatments is presenting substantial growth prospects in terms of transcatheter aortic valve replacements. Preference for shorter hospitalization periods and rapid recovery times has encouraged the adoption of outpatient-based cardiology treatments. The opening up of ambulatory surgery centers will enable better access to sophisticated valve treatments. Greater funding on structural heart disease treatment programs has increased the number of cases being performed across the globe. Next generation self-expanding valves have also contributed to improved accuracy in treatments.

As per the centers for Medicare & Medicaid services & national coverage determination and the STS/ACC TVT registry 2025, TAVR is covered by coverage with evidence development in Medicare-approved clinicals, showing regulatory growth in minimally invasive cardiac treatment. As per the American College of Cardiology 2025 study results, TAVR has an incidence rate of 26.8%, whereas there is a 45.3% incidence rate with clinical surveillance among asymptomatic severe aortic stenosis patients.

Recent Developments

-

2026: Medtronic gained FDA approval for Mosaic Neo bioprosthetic mitral valve and initiated U.S. commercial rollout with early robotic implantation use.

-

2025: Edwards Lifesciences received FDA approval for Sapien M3 transcatheter mitral valve replacement system, expanding structural heart therapy portfolio significantly.

-

2025: Medtronic launched Evolut FX+ transcatheter aortic valve in India after regulatory approval, enhancing coronary access and procedural flexibility.

-

2024: Boston Scientific Corporation TAVR-related structural heart investments focused on R&D expansion and next-generation valve technologies advancement.

Transcatheter Aortic Valve Replacement Market Key Players are:

-

Edwards Lifesciences

-

Medtronic

-

Abbott Laboratories

-

Boston Scientific Corporation

-

JenaValve Technology

-

JC Medical Inc.

-

Venus Medtech (Hangzhou) Inc.

-

MicroPort Scientific Corporation

-

Lepu Medical Technology

-

Meril Life Sciences Pvt. Ltd.

-

Peijia Medical Limited

-

Braile Biomédica

-

Colibri Heart Valve LLC

-

Artivion Inc.

-

LivaNova PLC

-

Shandong Weigao Group Medical Polymer Co., Ltd.

-

Blue Sail Medical Co., Ltd.

-

Medinol Ltd.

-

Terumo Corporation

-

Hangzhou NuMED Medical Co., Ltd

Transcatheter Aortic Valve Replacement Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.78 Billion |

| Market Size by 2035 | USD 13.58 Billion |

| CAGR | CAGR of 7.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Aortic Stenosis, Aortic Regurgitation, Congenital Heart Defects, Heart Failure) • By Procedure Type (Transfemoral, Transapical, Subclavian, Direct Aortic) • By End User (Hospitals, Ambulatory Surgical Centers, Cardiology Clinics) • By Valve Type (Balloon-Expandable, Self-Expanding, Surgical Aortic Valve Replacement) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Edwards Lifesciences, Medtronic, Abbott Laboratories, Boston Scientific Corporation, JenaValve Technology, JC Medical Inc., Venus Medtech (Hangzhou) Inc., MicroPort Scientific Corporation, Lepu Medical Technology, Meril Life Sciences Pvt. Ltd., Peijia Medical Limited, Braile Biomédica, Colibri Heart Valve LLC, Artivion Inc., LivaNova PLC, Shandong Weigao Group Medical Polymer Co., Ltd., Blue Sail Medical Co., Ltd., Medinol Ltd., Terumo Corporation, Hangzhou NuMED Medical Co., Ltd. |

Frequently Asked Questions

The transcatheter aortic valve replacement market was valued at USD 6.78 billion in 2025.

The major growth factors include the rising prevalence of aortic stenosis and structural heart diseases, increasing preference for minimally invasive cardiac procedures, expanding geriatric population, growing number of high-risk surgical patients, and continuous advancements in balloon-expandable and self-expanding valve technologies improving procedural outcomes.

Get in Touch