Barite Market Report Scope & Overview:

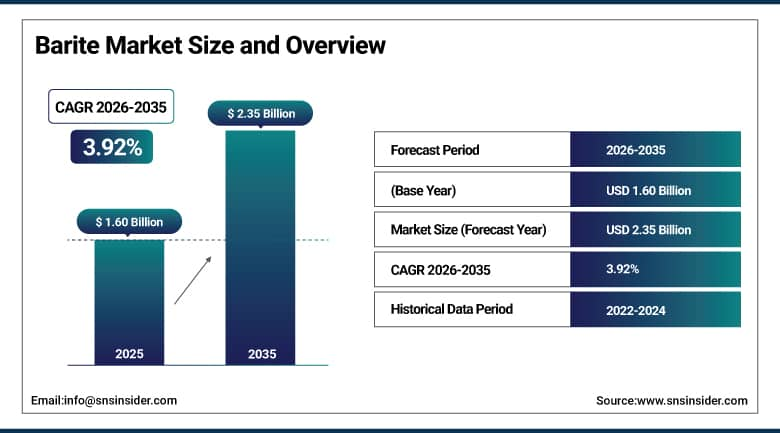

The Barite Market was valued at USD 1.60 billion in 2025 and is expected to reach USD 2.35 billion by 2035, growing at a CAGR of 3.92% from 2026–2035.

The barite market is witnessing steady growth in the global market owing to the increasing demand from oil and gas drilling activities. Rising exploration and production investments are supporting the consumption of barite across major regions. Growing utilization in paints, polymers, and chemical manufacturing is contributing to market expansion. Increasing demand for radiation shielding materials in healthcare and industrial applications is driving market growth. Advancements in construction materials and infrastructure development projects are fueling the demand for barite.

As per the report Mineral Commodity Summaries 2025 released by the U.S. Geological Survey, more than 90% of the barite used in the United States is used as a weighing material in drilling fluids of oil and natural gas wells, the total consumption of barite, both domestic and foreign imports, amounting to 2.3 million metric tons in 2024. As stated by the United Nations Statistics Division, the UN Comtrade database collects statistical data on trade among approximately 200 countries of the world, representing over 99% of world trade, in which barite falls under industrial minerals.

Market Size and Forecast:

-

Market Size 2026E: USD 1.66 billion

-

Market Size 2035: USD 2.35 billion

-

CAGR (2026 - 2035): 3.92%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Barite Market - Request Free Sample Report

Barite Market Trends:

-

Expanding offshore drilling activities increased API-grade barite demand, prompting capacity additions and supply-chain diversification initiatives globally.

-

Beneficiation technology adoption improved recovery rates by over 10%, enhancing resource utilization and reducing processing waste.

-

Stricter mining and environmental regulations accelerated investments in water recycling systems and lower-emission mineral processing operations.

-

Rising demand from paints, polymers, and specialty chemicals increased consumption of high-purity barite grades across industries.

-

Domestic critical mineral strategies introduced during 2024–2026 encouraged exploration spending and reduced dependence on imported barite supplies.

-

Digital mine management and automated ore-sorting technologies improved operational efficiency, supporting consistent quality and lower production costs.

U.S. Barite Market Size Outlook:

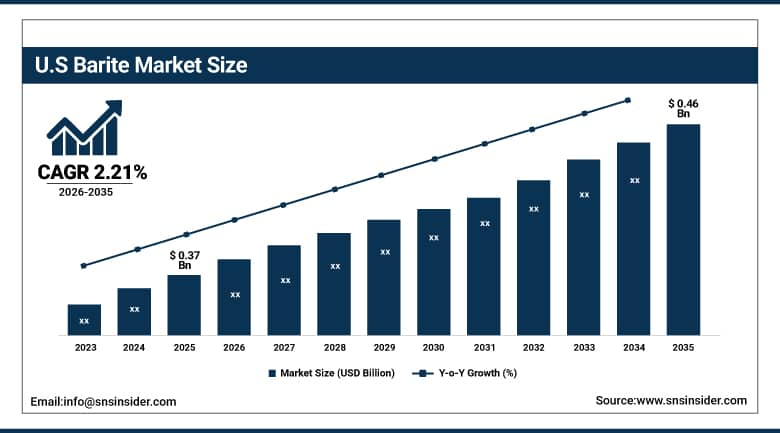

The U.S. Barite Market was valued at USD 0.37 Billion in 2025 and is expected to reach around USD 0.46 Billion by 2035, growing at a CAGR of 2.21% from 2026–2035.

The U.S. barite market is witnessing steady growth because of increasing oil and gas drilling activities. Barite consumption across drilling mud, chemical manufacturing, and construction applications has been responsible for strong market expansion. Increasing investments in domestic energy production and exploration projects have led to rising demand for barite. Growing utilization in radiation shielding materials, paints, and polymer applications is further supporting market growth. Continuous focus on energy security and industrial development activities is strengthening market demand.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025, three companies operated four barite mining sites in Nevada during 2024. More than 90% of U.S. barite consumption was used in oil and natural gas drilling fluids. The U.S. remained heavily import-dependent, with net import reliance exceeding 75% of apparent consumption, while imports supplied roughly 2.5 million metric tons in 2023.

Barite Market Segment Analysis:

-

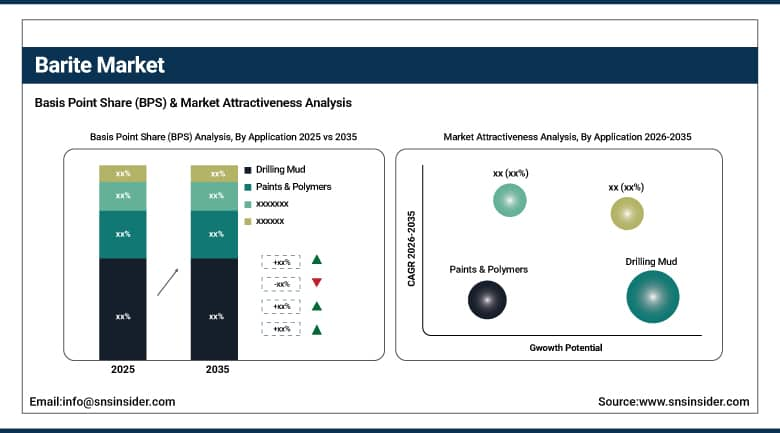

By Application, drilling mud dominated the barite market with 70.00% share in 2025; while paints & polymers are the fastest growing segment with CAGR of 7.40% during 2026 to 2035.

-

By Radiation Shielding, nuclear power plant shielding dominated the barite market with 39.88% share in 2025; while medical radiation shielding is the fastest growing segment with CAGR of 4.57% during 2026 to 2035.

-

By Construction Materials, cement & concrete additives dominated the barite market with 45.18% share in 2025; while high-density construction blocks are the fastest growing segment with CAGR of 6.23% during 2026 to 2035.

By Application, drilling mud dominated the barite market, while paints & polymers are the fastest growing segment.

Drilling Mud segment emerged as the dominated player in the Barite Market, holding the largest share of revenue in 2025. This was due to the extensive usage of barite as a weighting agent in drilling mud. The increase in oil and gas exploration operations in both offshore and onshore reservoirs led to a higher global demand. The growth in the number of investment projects in energy generation has improved drilling activities. Demand from established and emerging hydrocarbon regions has reinforced the position of the segment.

The Paints & Polymers segment is expected to register the fastest CAGR between 2026 and 2035. This growth will be triggered by the growing demand for performance fillers in coating applications. The increasing use of barite enhances the attributes of performance fillers such as chemical resistance, durability, and improved surface finishes. Growth in construction activities, the automotive industry, and industrial manufacturing has boosted the demand for products.

By Radiation Shielding, nuclear power plant shielding dominated the barite market, while medical radiation shielding is the fastest growing segment.

The Nuclear Power Plant Shielding segment held the dominated share of the global barite market on the basis of revenue generation in the year 2025. The large share was owing to the wide usage of barite materials of high density for providing shielding against radiations. Increasing investments in nuclear energy systems augmented the requirement for effective shielding systems, leading to growing material consumption throughout their lifetime and strict safety regulations. Further development of various modernization works and maintenance activities within nuclear power plants fueled segmental growth.

Medical Radiation Shielding is projected to register the fastest CAGR between 2026 and 2035. The growth is attributed to increasing installations of medical devices like radiation imaging and therapies. The rising investments within the healthcare industry have boosted demand for effective medical radiation shielding products. Growing consumer concerns about safety of patients and medical professionals are fuelling the segmental growth. Growing technology up-gradation in healthcare sector and increasing cases of cancer are expected to fuel demand.

By Construction Materials, cement & concrete additives dominated the barite market, while high-density construction blocks are the fastest growing segment.

Cement & Concrete Additives segment held the dominated revenue share in the barite market during 2025. The growing demand for reinforced materials in high-density concrete for infrastructure development was seen as responsible for the market dominance of this segment. Increasing demand for durable and sturdy construction material fueled its adoption. Additionally, higher investments in constructing roadways and buildings contributed to this growth. Consistency and effectiveness in the performance of this segment cemented its leadership position in the market.

High-Density Construction Blocks segment will witness fastest CAGR from 2026-2035. Growth in this segment is propelled by increasing need for materials that provide resistance to radiation and noise insulation purposes. Healthcare institutions, scientific research centers, and special industries are driving the market uptake of products in this segment. The focus on safety and the adoption of high-performance building materials is creating opportunities. Innovation in construction technologies and investments in developing infrastructures are expected to support its rapid growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

68.75% |

|

Europe |

Germany |

24.78% |

|

Asia Pacific |

China |

43.15% |

|

Middle East & Africa |

UAE |

18.64% |

|

Latin America |

Brazil |

47.21% |

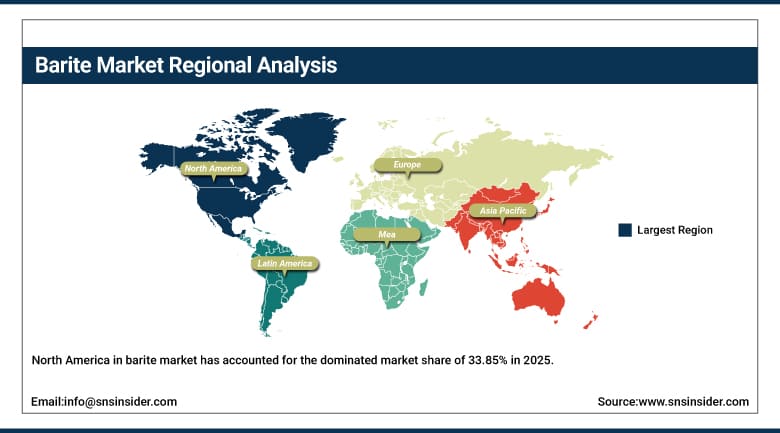

North America Barite Market Insights.

North America in barite market has accounted for the dominated market share of 33.85% in 2025 due to extensive oil and gas drilling activities. The region benefits from established energy infrastructure, high exploration spending, and consistent demand for drilling mud applications. Increasing investments in domestic energy production and offshore exploration projects are driving steady growth across the United States and Canada. Expanding industrial applications and growing utilization in construction materials are further supporting market expansion.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025, the United States produced approximately 340,000 metric tons of barite in 2024, while apparent consumption reached about 2.1 million metric tons. More than 90% of barite consumption in North America is associated with drilling fluids used in oil and gas exploration. The report also notes that the United States relied heavily on imports to meet demand, reflecting sustained drilling activity and continued utilization of barite as a critical weighting material in energy-sector operations.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Barite Market Insights.

The Europe barite market makes an important mark in the year 2025 owing to growing industrial manufacturing and infrastructure modernization activities. Countries like Germany, France, United Kingdom, Italy, and Spain are leading contributors to regional demand. High focus on specialty chemicals, paints, coatings, and radiation shielding applications is supporting consistent market expansion. Increasing investments in industrial production and sustainable construction programs are strengthening adoption across multiple end-use sectors.

According to the European Commission’s Raw Materials Information System, baryte has been classified as a Critical Raw Material for the European Union since 2017 and remains on the 2023 EU Critical Raw Materials list due to its economic importance and supply-risk profile. The 2023 EU criticality assessment identified 34 critical raw materials, up from 30 in 2020 and 27 in 2017, reflecting growing concerns over supply security and import dependence for minerals essential to European industrial and energy value chains.

Asia Pacific Barite Market Insights.

Asia Pacific is well positioned to experience the fastest CAGR of 5.57% in the barite market during the forecast period due to rapid industrialization and energy sector expansion. China, India, Japan, South Korea, and Australia are key contributors. Rising demand from oil and gas exploration, chemical manufacturing, and construction industries is boosting adoption. Expanding manufacturing capacity and infrastructure development are further strengthening market growth across the region.

According to the U.S. Geological Survey Mineral Commodity Summaries 2026, Asia Pacific remains the center of global barite supply, with India producing about 3.0 million metric tons and China about 2.2 million metric tons in 2025. The report also estimates barite reserves of approximately 51 million tons in India and 120 million tons in China. Barite demand is closely linked to oil and gas drilling, where it serves as a critical weighting agent in drilling fluids and has no large-scale substitute for this application.

Middle East & Africa and Latin America Barite Market Insights.

The Middle East & Africa region along with Latin America will exhibit consistent growth in the barite market up till 2025 due to expanding energy exploration and infrastructure investments. Saudi Arabia, UAE, South Africa, Brazil, and Mexico will join the list as countries with an emerging market for barite. Given that the growing oil and gas demand, industrial sector expansion, and construction activities will increase the consumption of barite across these regions.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025 and the OPEC Annual Statistical Bulletin 2025, Morocco remains one of the world’s key barite-producing countries, while barite demand across the Middle East, Africa, and Latin America is closely linked to oil and gas drilling activity. In 2024, crude oil production reached 23.04 million barrels per day in the Middle East, 6.10 million barrels per day in Africa, and 7.01 million barrels per day in Latin America, supporting sustained consumption of drilling-grade barite used in well construction and exploration activities.

Market Dynamics:

Growth Drivers: Expanding oil and gas exploration activities across major producing regions continue increasing demand for barite in drilling operations globally

Growing oil and gas exploration activities are contributing to increased demand for barite across the world due to drilling activities. Barite is commonly used as a weighting material in the composition of drilling fluids. Growing investments in exploration programs both offshore and onshore are contributing to increased consumption. Increasing energy demands in both developed and developing countries are resulting in increased production of barite. The need for highly specialized drilling fluid due to increased depths of drilling activities and complex recovery procedures is leading to growth in consumption levels. Energy security measures are boosting investments in exploration and production activities.

As per the IEA Oil 2025 and the U.S. Geological Survey Mineral Commodity Summaries 2025, there was a global oil demand in excess of 103 million barrels per day in 2024, thereby ensuring that there were continuous upstream exploration and drilling operations.

As per the USGS, more than 75 percent of global barite production is used for its application as a weighting material in drilling fluids for oil and gas wells. With increased drilling activity in various oil-producing zones, there remains an unrelenting need for drilling grade barite around the world.

Restraints: Environmental regulations and mining permit restrictions are reducing expansion opportunities for barite extraction projects globally

Strict environmental policies have started to affect the operations in mining as well as the processing of barite. It is becoming harder for governments to approve applications for permits due to strict guidelines and policies in terms of land use and extraction of resources. The process of getting permits might become more difficult because of monitoring requirements. Community pressure with respect to the environmental impacts of the project might lead to delays. Mining restrictions might affect supplies as well as capacity.

Opportunities: Rising infrastructure development and advanced construction projects are expanding applications for high density barite materials

Global investments in infrastructural developments are proving favorable for the potential use of barite in the construction sector. Use of barite in the production of cement, concrete, and other construction materials has been increasing lately. Increased trends in urbanization have led to increased demand for strong construction solutions across the world. There has been an increasing need for high density aggregate usage in various infrastructure projects. Various developments in the transport, energy, and public infrastructure sectors have been contributing towards adoption. Use of advanced materials due to increased need for better performance is also a factor.

According to the United Nations Environment Programme and the United Nations Department of Economic and Social Affairs (UN DESA), the global building floor area is projected to increase by approximately 230 billion square meters by 2060, equivalent to adding the floor area of an entire city the size of Paris every week.

Recent Developments:

-

2026: Halliburton Company entered a multi-year agreement with Pampa Energía to deploy digital orchestration, reservoir modeling, logistics optimization, and energy-efficiency management technologies across unconventional shale operations in Argentina’s Vaca Muerta basin.

-

2025: Baker Hughes Company partnered with Repsol to deploy new Leucipa digital capabilities, including a generative AI-powered virtual assistant delivering real-time production insights and predictive analytics for field operations.

-

2025: Halliburton Company introduced the next-generation Summit Knowledge digital ecosystem, featuring SK Well Pages that enhance electric submersible pump monitoring through advanced data science and real-time production analytics.

-

2024: Halliburton Company generated more than $2.6 billion in free cash flow during 2024 while continuing investments in drilling technology, artificial lift solutions, and digital portfolio expansion.

Barite Market Key Players are:

-

China Zhongrun Barium Industry Co., Ltd.

-

Excalibar Minerals LLC

-

CIMBAR Performance Minerals

-

Andhra Pradesh Mineral Development Corporation

-

Halliburton Company

-

Schlumberger Limited

-

The Andhra Sugars Limited

-

Ashapura Group

-

Milwhite Inc.

-

Newpark Resources, Inc.

-

P&S Barite Mining Co., Ltd.

-

Baker Hughes Company

-

Sojitz Corporation

-

Desku Group Inc.

-

Ado Mining Company Ltd.

-

Guizhou Tianhong Mining Co., Ltd.

-

Red Star Barium Sulfate Industrial Co., Ltd.

-

Seaforth Mineral & Ore Co., Inc.

-

International Earth Products LLC

-

Anglo Pacific Minerals Ltd.

Barite Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.60 Billion |

| Market Size by 2035 | USD 2.35 Billion |

| CAGR | CAGR of 3.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Drilling Mud, Chemical Manufacturing, Paints & Polymers, Pharmaceuticals) • By Radiation Shielding (Medical Radiation Shielding, Nuclear Power Plant Shielding, Industrial Radiography Shielding) • By Construction Materials (Cement & Concrete Additives, Heavy Aggregates, High-Density Construction Blocks) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | China Zhongrun Barium Industry Co., Ltd., Excalibar Minerals LLC, CIMBAR Performance Minerals, Andhra Pradesh Mineral Development Corporation, Halliburton Company, Schlumberger Limited, The Andhra Sugars Limited, Ashapura Group, Milwhite Inc., Newpark Resources, Inc., P&S Barite Mining Co., Ltd., Baker Hughes Company, Sojitz Corporation, Desku Group Inc., Ado Mining Company Ltd., Guizhou Tianhong Mining Co., Ltd., Red Star Barium Sulfate Industrial Co., Ltd., Seaforth Mineral & Ore Co., Inc., International Earth Products LLC, Anglo Pacific Minerals Ltd. |

Frequently Asked Questions

The barite market is expected to grow at a CAGR of 3.92% from 2026 to 2035.

The barite market was valued at USD 1.60 billion in 2025.

Expanding oil and gas exploration activities and increasing demand for drilling fluids are driving global barite consumption.

Drilling Mud dominated the market in 2025 with a 70.00% share due to its extensive use in oil and gas drilling operations.

North America dominated the barite market in 2025 due to extensive oil and gas drilling activities and strong energy infrastructure investments.

Get in Touch