Chronic Venous Occlusions Market Report Scope & Overview:

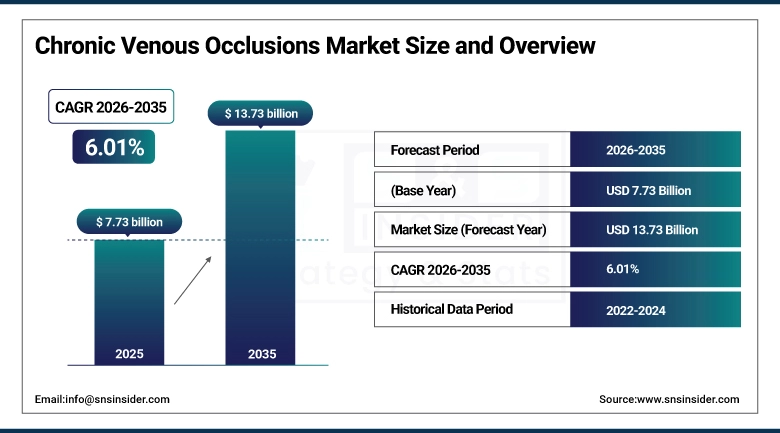

The Chronic Venous Occlusions Market size is valued at USD 7.73 Billion in 2025 and is projected to reach USD 13.73 Billion by 2035, growing at a CAGR of 6.01% during the forecast period 2026–2035.

The analysis report for the Chronic Venous Occlusions (CVO) Market offers a comprehensive overview of the therapeutic innovations and clinical applications. With a high prevalence rate of venous disorders, a rise in minimally invasive procedures, an increase in advanced imaging techniques, and a rise in healthcare infrastructure, the market is witnessing robust growth between 2026 and 2035.

Minimally invasive procedures recorded over 320 million treatments in 2025, driven by rising patient preference for safer, quicker recovery options and strong clinical adoption.

Market Size and Forecast:

-

Market Size in 2025: USD 7.73 Billion

-

Market Size by 2035: USD 13.73 Billion

-

CAGR: 6.01% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Chronic Venous Occlusions Market - Request Free Sample Report

Chronic Venous Occlusions Market Trends:

-

Increase in the adoption of minimally invasive image-guided procedures as a treatment of choice.

-

The need for better diagnostic imaging methods is becoming more important.

-

Increase in patient-centric therapies that reduce recovery times and enhance quality of life.

-

Patient-focused treatments are also gaining traction, leading to quicker recoveries and a better overall quality of life.

-

The vascular device sector is buzzing with activity, particularly when it comes to stents, catheters, and compression devices.

-

Digital health tools and artificial intelligence (AI) are becoming more common in vascular diagnostics.

-

Increase in awareness campaigns and screening programs to detect venous disorders early.

U.S. Chronic Venous Occlusions Market Insights:

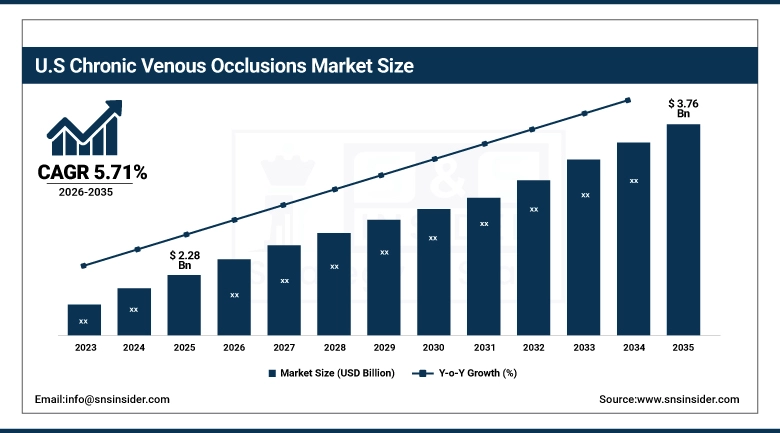

The U.S. Chronic Venous Occlusions Market is projected to grow from USD 2.28 Billion in 2025 to USD 3.76 Billion in 2035, at a CAGR of 5.71%. An increase in the prevalence of venous disorders, a rise in demand for minimally invasive vascular procedures, high acceptance of advanced imaging technologies, and a rise in healthcare infrastructure are boosting market growth for the U.S. Chronic Venous Occlusions Market from 2026 to 2035.

Chronic Venous Occlusions Market Growth Drivers:

-

Rising prevalence of venous disorders and increased demand for minimally invasive vascular procedures are driving adoption of advanced therapies.

The rise in the incidence rate of chronic venous occlusions and the growing patient population are also key drivers for market growth. Hospitals, clinics, and ambulatory surgical centers are increasingly using sophisticated treatment modalities to treat patients with chronic venous occlusions. Advanced biologics, targeted medicines, and sophisticated medical devices are being increasingly used to treat patients with chronic venous occlusions, thereby reducing recovery periods.

More than 60% of hospitals, clinics, and ambulatory surgical centers adopted sophisticated Chronic Venous Occlusion treatments in 2025 to treat patients with venous disorders.

Chronic Venous Occlusions Market Restraints:

-

High treatment costs and limited affordability in developing regions are restraining widespread adoption of advanced therapies.

The high cost associated with minimally invasive treatments, biologics, and high-end imaging is still a roadblock for patients as well as the healthcare industry, especially in low-income markets. For hospitals, specialty centers, as well as outpatient facilities, it is a challenge to achieve the right balance between cost efficiency and access to the latest medical technologies. Other factors affecting the market growth are regulatory challenges, reimbursement issues, as well as insurance coverage.

Fewer than half of the healthcare providers in resource-constrained markets used advanced treatments for Chronic Venous Occlusion in 2025.

Chronic Venous Occlusions Market Opportunities:

-

Expanding healthcare infrastructure and rising investments in advanced vascular care are creating strong opportunities for market growth.

In addition, emerging markets are increasingly employing minimally invasive technologies, advanced imaging techniques, and innovative vascular technologies to ensure improved patient outcomes. There is a rise in investments in digital health technologies, artificial intelligence, and precision therapies in hospitals, specialty clinics, and ambulatory surgery centers. There is a development of new oral, injectable, and intravenous formulations, sustained release biologics, and therapies, creating new avenues for innovation in therapy.

Over 65% of healthcare providers in developed regions are likely to adopt advanced Chronic Venous Occlusion therapies by 2030.

Chronic Venous Occlusions Market Segmentation Analysis:

-

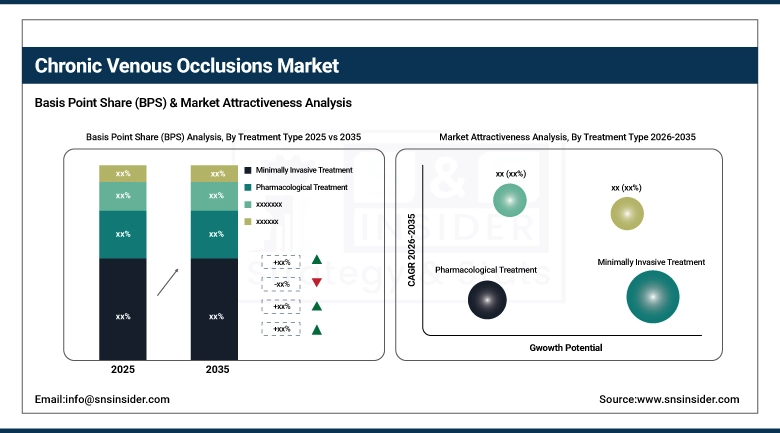

By Treatment Type, Minimally Invasive Treatment held the largest market share of 36.54% in 2025, while they are also expected to grow at the fastest CAGR of 6.68% during 2026–2035.

-

By Diagnosis Type, Duplex Ultrasound dominated with 38.82% market share in 2025, whereas MRI (Magnetic Resonance Imaging) are projected to record the fastest CAGR of 5.65% through 2026–2035.

-

By Product Type, Devices accounted for the highest market share of 40.68% in 2025, while they are expected to grow at the fastest CAGR of 5.89% during the forecast period.

-

By End User, Hospitals held the largest share of 44.38% in 2025, while Ambulatory Surgical Centers (ASCs) are expected to grow at the fastest CAGR of 5.81% during the forecast period.

By Treatment Type, Minimally Invasive Treatment Dominate and expected to grow at the fastest CAGR

In 2025, Minimally Invasive Treatment dominated the market by treatment type, holding the largest share. Its prominence is driven by benefits such as reduced patient recovery time, lower risk of complications, and improved procedural precision. Growing patient preference for less invasive procedures, advancements in surgical technologies, and increased awareness of minimally invasive options are fueling demand. As a result, this segment is also expected to register the fastest growth during the forecast period from 2026 to 2035.

By Diagnosis Type, Duplex Ultrasound Dominate While MRI (Magnetic Resonance Imaging) Grow Rapidly:

Duplex Ultrasound was the most dominated market in 2025, based on its reliability, accessibility, and usage in all medical institutions to correctly diagnose retinal vein occlusion. Its non-invasive nature and cost-effectiveness have made it the preferred diagnostic technique among medical practitioners.

MRI or Magnetic Resonance Imaging is the fastest growing diagnostic technique due to its superior image quality, enabling the visualization of structures in the retina. The ability to detect subtle vascular changes, provide non‑invasive insights, and support early diagnosis makes MRI highly valuable.

By Product Type, Devices Dominate While Also Grow Rapidly:

Devices held the dominated market share in 2025. This is because they are critical in the diagnosis and treatment of retinal vein occlusion. Advanced imaging systems, surgical devices, and therapeutic equipment are used extensively by healthcare providers to ensure precision and safety in patient treatment.

Devices are also growing at a fastest rate. This is because of the rapid advancements in imaging devices, surgical devices, and AI-enabled devices. increasing integration of portable and wearable technologies is expanding accessibility, allowing real‑time monitoring and enhancing patient engagement in retinal care.

By End User, Hospitals Dominate While Ambulatory Surgical Centers Grow Rapidly:

Hospitals had the highest share in the market in 2025, owing to the infrastructure that they provide, the diagnostic tools that they employ, and the ability that they have in handling complicated cases of retinal vein occlusions. They are the primary healthcare institutions that provide specialized ophthalmic services, which include access to professionals and the latest technology.

Ambulatory Surgical Centers are the fastest-growing end-users of retinal vein occlusion treatment, owing to the increasing need for cost-effective healthcare services that provide quick turnaround and lower overall treatment costs. rising patient preference for convenient, accessible care closer to home is accelerating the expansion of ASCs across both urban and suburban regions.

Regional Analysis:

North America Chronic Venous Occlusions Market Insights:

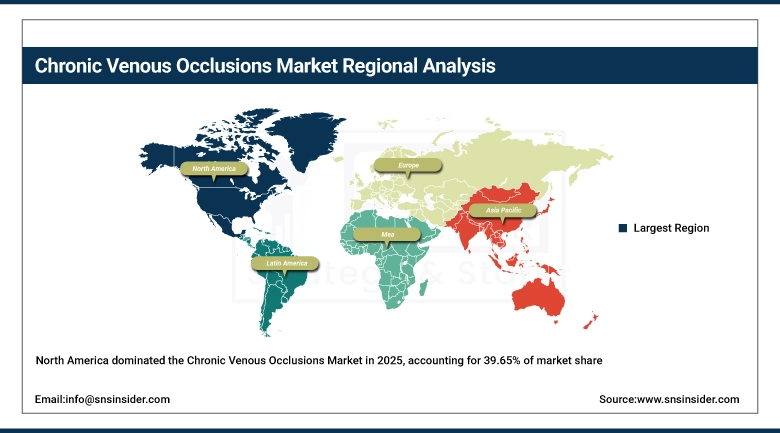

North America has been a market leader in the global market in terms of market share, which was 39.65% in 2025. This is due to a strong healthcare infrastructure, high rates of organ transplants, and widespread use of advanced immunosuppressive agents. There is a high demand for immunosuppressive agents in hospitals and clinics in North America. These hospitals and clinics are equipped to deal with organ transplant rejections and autoimmune conditions, where immunosuppressive agents are used. There is a high prevalence rate of inflammatory conditions, and this has further fueled the market in North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Market Insights:

The US is a global leader in this market, fueled by a high rate of organ transplants, well-developed healthcare infrastructure, and high adoption rates of calcineurin inhibitors, biologics, and monoclonal antibodies. Increasing prevalence of autoimmune and inflammatory conditions, a rise in specialty clinics, and favorable reimbursement will support this position. Ongoing innovation in oral, injectable, and intravenous formulations will drive growth and maintain this leadership.

Asia‑Pacific Chronic Venous Occlusions Market Insights:

Asia Pacific is a fastest growing market with a CAGR of 7.98%, mainly fueled by a rise in healthcare infrastructure, transplant procedures, and autoimmune conditions. China, India, and Japan are investing significantly in biologics, targeted therapies, and diagnostic tools. In addition, a rise in patient demand, government initiatives, and a high rate of adoption of minimally invasive procedures are driving growth in this region. A strong pipeline of clinical research and a rise in healthcare expenditure are making this region a growth driver for the upcoming decade.

China Market Insights:

The Chinese market is the fastest-growing market in the Asia Pacific region, driven by the expansion of healthcare infrastructure, the number of transplant procedures, and the incidence of autoimmune conditions. Robust government support for biologics, targeted therapies, and diagnostic tools is fueling the market’s growth. Increasing patient demand, rapid urbanization, and rising healthcare expenditures make China a major contributor to the overall growth of the CVO market globally.

Europe Chronic Venous Occlusions Market Insights:

The region holds a considerable share in the world market, mainly due to the high incidence rates of aging populations, as well as the incidence rates of autoimmune diseases. In addition, the region has shown high adoption rates of biologics in specialty clinics. Countries such as Germany, France, and the U.K. have shown high adoption rates in the use of advanced therapy, owing to the high standards of their healthcare infrastructure as well as government initiatives in the same.

Germany Market Insights:

Germany is considered a major market in the European region with a well-established healthcare system and a relatively higher awareness of healthcare among patients and clinical adoption of advanced therapies. In addition, the prevalence of autoimmune diseases is rising in the country, and the government is making efforts to provide access to biologics. Clinical trials and approvals are also driving the market in the country.

Latin America Chronic Venous Occlusions Market Insights:

Latin America has witnessed a growth trajectory in the region, fueled by the increasing awareness of venous diseases and the adoption of advanced treatment modalities in countries like Brazil and Mexico, despite the challenges related to infrastructure and affordability. The increasing number of specialty clinics and the government’s initiatives to enhance the accessibility of biologics and targeted therapies are helping the region to move forward in a gradual manner.

Middle East & Africa Chronic Venous Occlusions Market Insights:

The Middle East & Africa region is a developing market; investments in healthcare and transplant procedures are driving growth in this region. Autoimmune conditions are also prevalent in this region. Although advanced therapy is still concentrated in urban areas and private facilities, government initiatives are slowly enhancing access to healthcare infrastructure. Although this region is a challenge in terms of affordability and availability of expert professionals, it is a promising region in terms of growth in biologics and targeted therapies.

Competitive Landscape:

Roche/Genentech is a leader in the ophthalmology market, admired for their leadership in anti-VEGF treatments such as Lucentis, which has revolutionized the treatment of retinal vein occlusion. Roche's product line excels in the areas of innovation, safety, and long-term efficacy, backed by robust clinical trials as well as real-world evidence. Roche is also investing heavily in the development of biological manufacturing as well as next-generation ocular treatments, including sustained release and gene therapy, providing a robust market position in the face of competition.

-

In 2025, Roche advanced its Port Delivery System (PDS) program into late-stage trials for retinal vein occlusion, aiming to reduce injection frequency and improve patient quality of life.

Novartis AG is a multinational pharmaceutical company that has a strong presence in retinal disease management, especially through its anti-VEGF therapy, Beovu. It is working towards making treatments more durable and accessible to patients by reducing treatment burden. It is a strong competitor in RVO management. It has a strong R&D pipeline and a strong distribution network across the globe. It is making efforts to increase access to advanced treatments for patients. It is also working towards digital health platforms that can be helpful for ophthalmologists.

-

In 2025, Novartis expanded Beovu’s clinical program to include broader retinal vein occlusion indications, while initiating trials for combination therapies to improve long‑term outcomes.

Regeneron is a biotech company based in the USA and is best known for its anti-VEGF drug Eylea, which is the most widely used anti-VEGF drug for retinal vein occlusion. Regeneron’s strength is in the consistency of the drug’s efficacy and safety in treating diverse populations with the support of physicians globally. Regeneron is continuously innovating in the market with long-acting formulations and next-generation biologics that can minimize the frequency of administration. Regeneron's collaboration with Bayer has solidified its standing in the industry.

-

In 2025, Regeneron launched its high‑dose Eylea program for retinal vein occlusion, targeting fewer injections per year and improved patient adherence.

Chronic Venous Occlusions Market Key Players:

-

Roche / Genentech

-

Novartis AG

-

Regeneron Pharmaceuticals

-

Bayer AG

-

AbbVie (Allergan)

-

Pfizer Inc.

-

Johnson & Johnson Vision

-

Bausch Health Companies

-

Amgen Inc.

-

Santen Pharmaceutical

-

Alcon Inc.

-

Teva Pharmaceutical Industries

-

Samsung Bioepis

-

Biogen Inc.

-

Iveric Bio (Astellas)

-

Kodiak Sciences

-

Adverum Biotechnologies

-

Graybug Vision

-

Ocugen Inc.

-

Outlook Therapeutics

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.73 Billion |

| Market Size by 2035 | USD 13.73 Billion |

| CAGR | CAGR of 6.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Minimally Invasive Treatment, Pharmacological Treatment, Surgical Treatment, Compression Therapy, Others), • By Diagnosis Type (Duplex Ultrasound, Venography, CT (Computed Tomography), MRI (Magnetic Resonance Imaging), Others), • By Product Type (Devices, Medication, Therapeutic Equipment, Others), • By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Diagnostic Laboratories, Home Care Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Roche / Genentech, Novartis AG, Regeneron Pharmaceuticals, Bayer AG, AbbVie (Allergan), Pfizer Inc., Johnson & Johnson Vision, Bausch Health Companies, Amgen Inc., Santen Pharmaceutical, Alcon Inc., Teva Pharmaceutical Industries, Samsung Bioepis, Biogen Inc., Iveric Bio (Astellas), Kodiak Sciences, Adverum Biotechnologies, Graybug Vision, Ocugen Inc., Outlook Therapeutics. |

Frequently Asked Questions

North America and Europe hold the largest shares of 39.65%, while Asia‑Pacific is recording the fastest growth rate 7.98% CAGR due to expanding healthcare infrastructure and increasing patient demand.

Opportunities lie in the growing adoption of sustained‑release formulations, gene therapy approaches, and AI‑enabled diagnostic platforms that improve treatment efficiency.

Key growth drivers include rising prevalence of retinal disorders, higher adoption rates of anti‑VEGF therapies, and expanding access to advanced imaging technologies.

The notable share of 36.54% of the broader Minimally Invasive Treatment market, with its proportion expected to rise as patient prevalence increases.

The market is projected to grow at a steady CAGR of 6.01%, driven by increasing adoption of advanced therapies and diagnostic technologies.

Get in Touch