Drone Sensor Market Report Scope & Overview:

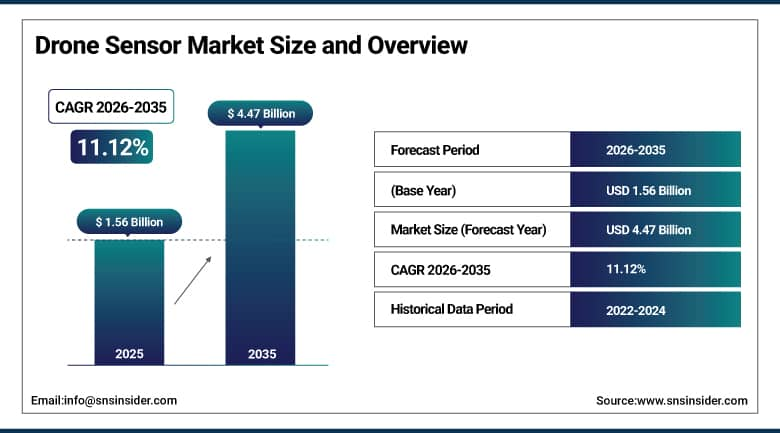

The Drone Sensor Market was valued at USD 1.56 Billion in 2025 and is expected to reach USD 4.47 Billion by 2035, growing at a CAGR of 11.12% from 2026–2035.

The global drone sensor market is growing at a sustained and commercially significant pace. Drone sensors are the perceptual and navigational intelligence systems that transform unmanned aerial vehicles from remotely piloted aircraft into autonomous platforms capable of sophisticated environmental awareness, precision navigation, data collection, and obstacle detection. The market is driven by increased spending on smart infrastructure, precision farming, and border surveillance directly contributing to its expansion, and growing fleet operability with AI-driven autonomy revolutionizing drone processes. As sensor costs decline and performance improves, smaller enterprises are entering the market, while military applications continue creating premium procurement from defense agencies globally.

In 2024, Teledyne FLIR launched the Hadron 640R dual-sensor payload combining thermal and color visible imaging in a miniaturized module optimized for drone integration, enabling simultaneous thermal and visible inspection in a single lightweight unit that reduces drone payload complexity and extends flight endurance. The product addresses the commercial demand for multi-sensor drone payloads whose combined imaging capability creates inspection quality that separate sensor alternatives cannot achieve at equivalent payload weight.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.73 Billion

-

Market Size by 2035: USD 4.47 Billion

-

CAGR: 11.12% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Drone Sensor Market - Request Free Sample Report

Drone Sensor Market Trends:

-

AI-powered sensor fusion technologies are enhancing autonomous drone navigation by combining data from GPS, LiDAR, cameras, and inertial measurement units for improved situational awareness

-

Miniaturization and declining costs of LiDAR sensors are accelerating adoption in applications such as precision agriculture, surveying, construction mapping, and infrastructure inspection

-

Progress in beyond visual line of sight (BVLOS) regulations is expanding demand for advanced drone sensor systems that support long-range autonomous operations

-

Increasing use of hyperspectral imaging sensors is enabling advanced crop monitoring, environmental analysis, and precision agriculture applications

-

Growing investments in counter-drone and anti-UAS systems are creating new opportunities for sensor technologies used in drone detection, identification, tracking, and security applications

U.S. Drone Sensor Market Outlook:

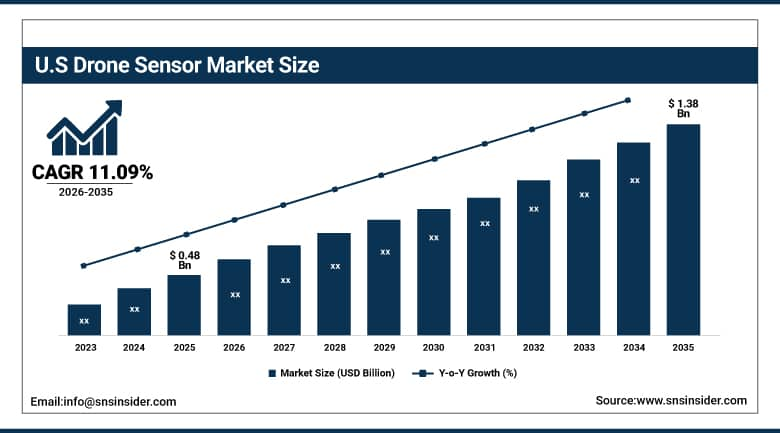

The U.S. Drone Sensor Market was valued at approximately USD 0.48 Billion in 2025 and is expected to reach approximately USD 1.38 Billion by 2035, growing at a CAGR of approximately 11.09%.

The U.S. is the most commercially significant drone sensor market within North America’s dominant revenue position. Teledyne FLIR, L3Harris Technologies, DJI’s enterprise sensor division, Velodyne Lidar (Ouster), and Trimble’s geospatial division collectively serve the domestic commercial, government, and military drone sensor markets. The FAA’s progressive BVLOS operation regulatory framework, the DoD’s extensive drone sensor procurement, and the commercial precision agriculture sector’s drone adoption create the most commercially diverse national drone sensor application deployment globally.

Skydio launched its Skydio X10 enterprise drone with enhanced multi-sensor suite in 2024, integrating 50MP color camera, thermal imaging, and obstacle avoidance sensors in a single platform optimized for infrastructure inspection, public safety, and defense reconnaissance. The platform’s domestic U.S. manufacture provides NDAA compliance that federal procurement and defense applications require, creating market access that Chinese-manufactured drone alternatives cannot satisfy in government and critical infrastructure applications.

Drone Sensor Market Segment Analysis:

-

By Sensor Type, the Image Sensors segment dominated the Drone Sensor Market with 30.6% share in 2025, while the Inertial Measurement Units (IMU) segment is projected to register the highest CAGR.

-

By Function, the Navigation segment dominated the Drone Sensor Market with 37.7% share in 2025, while the Data Acquisition segment is estimated to register the highest CAGR.

-

By Application, the Defense & Security segment dominated the Drone Sensor Market with approximately 38% share in 2025, while the Agriculture segment is the fastest growing.

-

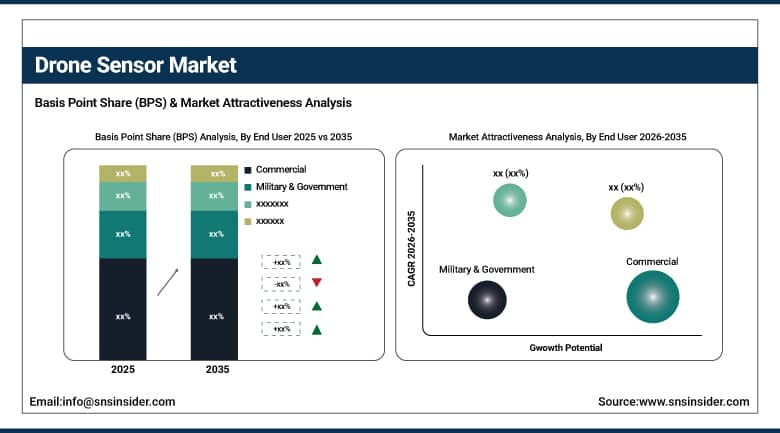

By End User, the Commercial segment dominated the Drone Sensor Market with approximately 42% share in 2025, while the Military & Government segment is the fastest growing.

By End User, Commercial dominate, Military & Government grow fastest

The Commercial segment dominated the Drone Sensor Market, accounting for approximately 42.0% of the global market share in 2025, driven by the increasing adoption of drones across agriculture, infrastructure inspection, construction, mining, logistics, energy, and environmental monitoring. Commercial operators are integrating advanced sensors such as LiDAR, thermal imaging, multispectral, and high-resolution optical sensors to improve operational efficiency, data accuracy, and automation. The growing use of AI-enabled drone analytics and expanding regulatory support for commercial drone operations continue to strengthen demand. The commercial segment was valued at approximately USD 0.78 billion in 2025 and is projected to reach around USD 2.05 billion by 2033, registering strong growth throughout the forecast period.

The Military & Government segment is projected to be the fastest-growing during the forecast period, supported by rising defense modernization programs, increasing investments in intelligence, surveillance, reconnaissance (ISR), border security, disaster response, and public safety applications. Governments worldwide are deploying drones equipped with advanced electro-optical, infrared, radar, and hyperspectral sensors to enhance situational awareness and mission effectiveness. Growing geopolitical tensions, defense spending, and technological advancements in autonomous UAV systems are expected to accelerate the expansion of this segment over the coming years.

By Sensor Type, image sensors dominate, IMUs grow fastest

Image sensors retained the dominant sensor type position with 30.6% of the drone sensor market in 2025. Image sensor’s commercial primacy reflects the universal requirement for visual situational awareness in every drone application from consumer photography through industrial inspection to military surveillance. High-resolution RGB cameras, multispectral imaging sensors, and thermal cameras collectively define the image sensor category whose application breadth creates the most commercially diverse drone sensor procurement. Aerial photography’s consumer and commercial demand, precision agriculture’s crop health mapping, infrastructure inspection’s visual documentation, and military’s reconnaissance imagery collectively create consistent procurement that sustains image sensors’ dominant market position. The progressive improvement in sensor resolution, dynamic range, and low-light performance creates upgrade procurement whose commercial momentum sustains the category’s leadership.

Inertial measurement units are the fastest-growing sensor type because autonomous flight capability’s progressive advancement requires above-standard IMU precision whose sensor fusion with GPS and visual odometry creates the localization accuracy that BVLOS operations and autonomous inspection missions require. Each new drone platform generation that improves autonomy capability creates premium IMU specification whose navigational accuracy requirement creates commercial differentiation from commodity IMU alternatives. The military’s GPS-denied environment navigation requirement creates above-average precision IMU procurement whose mission-critical performance specification sustains premium commercial relationships.

By Application, defense dominates, agriculture grows fastest

Defense and security retained the dominant application position with approximately 38% of the drone sensor market in 2025. The military and government sector’s sensor performance specification, whose mission-critical surveillance, reconnaissance, and intelligence requirements create above-commodity sensor procurement, defines the most commercially significant drone sensor application category by per-unit value. Each military drone programme’s sensor suite investment, encompassing electro-optical/infrared cameras, hyperspectral imagers, synthetic aperture radar, and signals intelligence sensors, creates per-drone sensor procurement whose premium specification reflects the operational requirements whose performance directly impacts mission success. Government border surveillance, critical infrastructure protection, and counter-UAS programmes collectively create defense and security’s dominant commercial position.

Agriculture is the fastest-growing application because precision farming’s systematic drone adoption for crop health monitoring, irrigation management, yield estimation, and pest detection is creating structured demand growth that compounds with the global agricultural sector’s technology investment. Each agricultural drone deployment creates sensor procurement for the multispectral camera, thermal imager, and NDVI index calculator whose combined crop intelligence creates agronomic value that sustains producer investment. Government precision agriculture subsidy programmes in India, China, and the EU create institutional adoption motivation that accelerates commercial sector growth.

By Function, navigation dominates, data acquisition grows fastest

Navigation retained the dominant function position with 37.7% of the drone sensor market in 2025. GPS receivers, inertial measurement units, barometric altimeters, and magnetometers collectively create the navigation sensor suite whose position determination, attitude estimation, and flight path planning capability is the foundational requirement for every drone operation. Each drone platform’s navigation sensor procurement creates commercial relationships whose volume reflects the drone fleet’s size and mission requirement. The navigation function’s safety-critical character creates specification standards that sustain premium procurement above commodity alternatives whose navigational accuracy or reliability cannot meet regulatory and operational requirements.

Data acquisition is the fastest-growing function because the commercial drone’s economic value creation is fundamentally dependent on the quality and diversity of data it captures from its operational environment. Each new data acquisition application—precision agriculture’s multispectral vegetation mapping, infrastructure inspection’s 3D point cloud, gas pipeline’s leak detection—creates sensor procurement whose functional value sustains above-average commercial growth. The data analytics platform’s ability to transform raw sensor data into operational intelligence creates downstream value whose measurement sustains sensor investment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Drone Sensor Market Insights

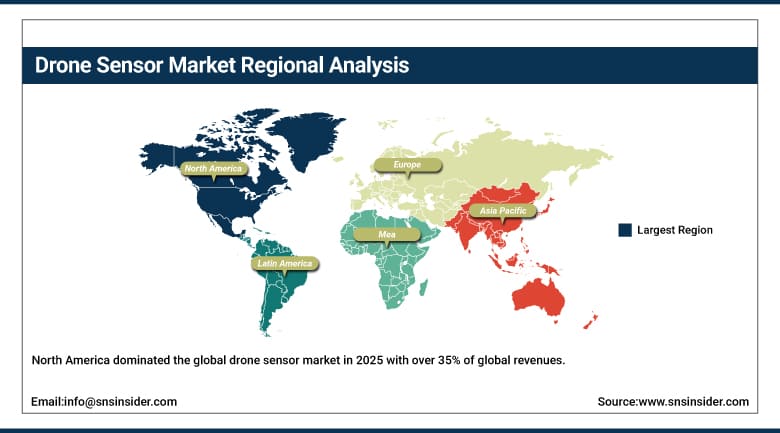

North America dominated the global drone sensor market in 2025 with over 35% of global revenues. The United States accounts for approximately 87.4% of North American revenues through Teledyne FLIR, L3Harris, Skydio, and the defense sector’s premium drone sensor procurement. The DoD’s extensive drone programme and the FAA’s progressive commercial BVLOS framework create the most commercially sophisticated national drone sensor market globally.

Canada contributes approximately 12.6% of North American revenues through its agriculture drone adoption, the natural resources sector’s inspection drone deployment, and the defense procurement programme’s sensor investment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Drone Sensor Market Insights

Europe is a technically sophisticated drone sensor market where EASA’s drone regulatory framework, Airbus Defense’s and MBDA’s military drone programme, and the precision agriculture sector create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its industrial drone inspection adoption, the Bundeswehr’s drone sensor procurement, and the precision agriculture sector’s multispectral imaging adoption.

France, the United Kingdom, and the Netherlands are significant secondary markets where military procurement, commercial inspection, and agricultural drone adoption create consistent drone sensor demand.

Asia Pacific Drone Sensor Market Insights

Asia Pacific is the fastest-growing regional drone sensor market, driven by China’s extraordinary commercial and military drone industry, India’s rapidly growing agriculture drone programme, Japan’s industrial inspection drone adoption, and South Korea’s logistics drone investment. China accounts for approximately 44.8% of Asia Pacific revenues through DJI’s commercial drone ecosystem, the government’s precision agriculture drone subsidy, and the military’s drone sensor procurement.

India’s government drone PLI scheme, Japan’s advanced industrial inspection drone programme, and South Korea’s delivery drone infrastructure creates significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional status.

MEA & Latin America Drone Sensor Market Insights

UAE leads MEA revenues at approximately 38.4% through its extraordinary military drone procurement, the smart city surveillance infrastructure, and the government’s drone logistics investment. Brazil leads Latin American revenues at approximately 44.2% through its agriculture drone adoption for the extraordinary soybean and sugarcane production monitoring and the growing infrastructure inspection sector.

Market Dynamics:

Growth Drivers: Defense surveillance investment and precision agriculture drone adoption creating dual demand vectors

Increased spending on smart infrastructure, precision farming, and border surveillance is SNS Insider’s confirmed primary driver of drone sensor market expansion. The defense sector’s surveillance drone programme creates the most commercially concentrated premium drone sensor procurement whose mission-critical performance specification sustains above-commodity commercial relationships. Each new military drone programme creates sensor procurement whose aggregate across NATO, Asia Pacific, and Middle Eastern defense investment creates commercial scale. Border surveillance investment’s drone sensor demand compounds with each new geopolitical security programme.

Precision agriculture’s drone adoption creates structured commercial demand whose multispectral camera, thermal imager, and NDVI sensor procurement creates consistent agricultural sector revenue. Each government precision agriculture programme that subsidizes drone adoption creates sensor demand whose commercial scale compounds with adoption programme coverage expansion. The agricultural drone’s ROI measurement in fertilizer savings, yield improvement, and labor cost reduction creates financial justification that sustains investment.

Restraints: Regulatory airspace restrictions and battery life limiting operational range

Drone airspace regulation’s BVLOS operation restriction, altitude limitation, and no-fly zone enforcement create operational constraints that limit commercial drone sensor application deployment to approved corridors and visual observation ranges. Each regulatory restriction that prevents commercial drone operators from accessing economically valuable operational areas creates market limitation whose resolution requires regulatory approval process investment.

Battery energy density’s limitation of commercial drone flight endurance to 20-45 minutes creates operational range constraints that limit sensor data collection coverage per mission. Each flight endurance limitation that restricts drone survey coverage per sortie creates operational cost that moderates the economic viability of drone sensor data collection relative to alternative survey methods.

Opportunities: BVLOS commercial operations regulatory approval and autonomous inspection drone proliferation

BVLOS regulatory approval’s progressive implementation creates the most commercially transformative drone sensor market development opportunity whose infrastructure inspection, precision agriculture, and logistics delivery applications create new commercial revenue at scales that visual line of sight operations cannot achieve. Each BVLOS operation regulatory approval creates a new commercial application category whose drone sensor procurement compounds with the operational programme’s scale.

Autonomous inspection drone proliferation for power line, pipeline, wind turbine, and solar farm inspection creates structured enterprise procurement whose inspection frequency and coverage requirement creates consistent drone sensor demand. Each industrial operator whose inspection drone programme replaces rope access and helicopter inspection creates sensor procurement whose ROI measurement sustains programme expansion.

Recent Developments:

-

2024: Teledyne FLIR launched the Hadron 640R dual-sensor payload in 2024 combining thermal and color visible imaging in a miniaturized module for drone integration, enabling simultaneous thermal and visible inspection in a single lightweight unit for commercial and defense applications.

-

2024: Skydio launched its Skydio X10 enterprise drone in 2024 with integrated multi-sensor suite including 50MP color camera, thermal imaging, and obstacle avoidance sensors, with NDAA-compliant domestic U.S. manufacture for federal procurement and defense applications.

-

2024: Velodyne Lidar (Ouster) launched new ultra-compact drone LiDAR sensors in 2024 targeting the commercial inspection and precision agriculture markets with reduced weight and power consumption that extends drone flight endurance without compromising 3D point cloud resolution.

Drone Sensor Market Key Players:

-

Teledyne FLIR LLC

-

L3Harris Technologies Inc.

-

Bosch Sensortec GmbH

-

TE Connectivity Ltd.

-

InvenSense Inc.

-

STMicroelectronics N.V.

-

Trimble Inc.

-

Velodyne Lidar Inc.

-

Skydio Inc.

-

Parrot SA

-

senseFly SA

-

Microstrain

-

Analog Devices Inc.

-

Honeywell Aerospace

-

Silicon Sensing Systems

-

Sparton Corporation

-

UTC Aerospace Systems

-

Xsens

-

AMS AG

-

Seakeeper Inc.

Drone Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.56 Billion |

| Market Size by 2035 | USD 4.47 Billion |

| CAGR | CAGR of 11.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Sensor Type (Image Sensors/Cameras, Inertial Measurement Units/IMU, LIDAR, Proximity Sensors, GPS/GNSS Sensors, Gas & Chemical Sensors, Others) • by Function (Navigation, Data Acquisition, Detection & Avoidance, Propulsion Monitoring) • by Application (Defense & Military, Commercial/Agriculture, Infrastructure Inspection, Logistics & Delivery, Search & Rescue, Others) • by End User (Military & Government, Commercial, Consumer) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Teledyne FLIR LLC, L3Harris Technologies Inc., Bosch Sensortec GmbH, TE Connectivity Ltd., InvenSense Inc., STMicroelectronics N.V., Trimble Inc., Velodyne Lidar Inc., Skydio Inc., Parrot SA, senseFly SA, Microstrain, Analog Devices Inc., Honeywell Aerospace, Silicon Sensing Systems, Sparton Corporation, UTC Aerospace Systems, Xsens, AMS AG, Seakeeper Inc. |

Frequently Asked Questions

The Drone Sensor Market is expected to grow at a CAGR of 11.12% from 2026 to 2035.

The Drone Sensor Market was valued at USD 1.56 Billion in 2025.

Increased spending on smart infrastructure, precision farming, and border surveillance directly contributing to market expansion, and growing fleet operability with AI-driven autonomy revolutionizing drone processes as sensor costs decline and performance improves.

Image Sensors dominated the Drone Sensor Market with 30.6% share in 2025 as confirmed by SNS Insider, while Inertial Measurement Units are projected to register the highest CAGR.

Navigation dominated the Drone Sensor Market with 37.7% share in 2025 as confirmed by SNS Insider, while Data Acquisition is estimated to register the highest CAGR.

Get in Touch