Pipeline Integrity Management Market Report Scope & Overview:

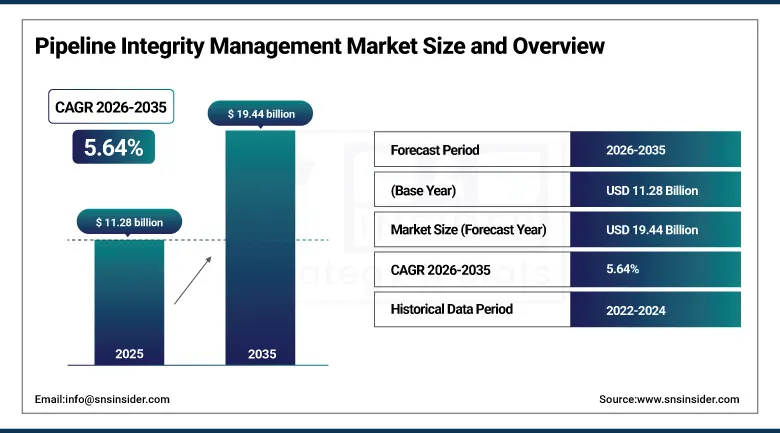

The Pipeline Integrity Management Market was valued at USD 11.28 billion in 2025 and is expected to reach USD 19.44 billion by 2035, growing at a CAGR of 5.64% during the forecast period.

The market for pipeline integrity management is witnessing strong growth owing to rising energy consumption worldwide, old oil and gas pipeline networks, and increased emphasis on ensuring safety and environment protection. The growing need for strict compliance and regulations to avoid pipeline breakages, leaks, and environmental pollution is another factor boosting the growth of pipeline integrity management solutions in the oil and gas industries. The latest technological innovations such as intelligent pigging, AI-based predictive analytics, leak detection systems, GIS-based asset integrity software, and real-time monitoring systems are revolutionizing the inspection process.

To back up this development, PHMSA enacted 13 final rules, April 2026, which would update pipeline safety regulations in 49 CFR Parts 191, 192, and 195 through integrity assessment approaches, corrosion control, and inspection standards.

Market Size and Forecast

-

Market Size in 2025: USD 11.28 Billion

-

Market Size by 2035: USD 19.44 Billion

-

CAGR: 5.64% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Pipeline Integrity Management Market - Request Free Sample Report

Pipeline Integrity Management Market Trends

-

The growing application of artificial intelligence based predictive analytics solutions for early identification of corrosions, cracks, and leakages in pipelines.

-

The quick adoption of intelligent pigging (ILI) solutions for accurate inspection and detection of defects within pipelines.

-

A clear inclination towards the use of digital twins that help in simulating the behavior of pipelines for better maintenance.

-

The growing adoption of GIS-based asset integrity software for centralized management of pipeline networks.

-

Strict regulatory environment created by organizations such as PHMSA and EU energy regulators.

-

The growing investment in methane emission detection and reduction technologies due to the global push towards decarbonization.

-

The adoption of cloud-based integrity management platforms to monitor pipeline networks remotely and perform centralized analytics.

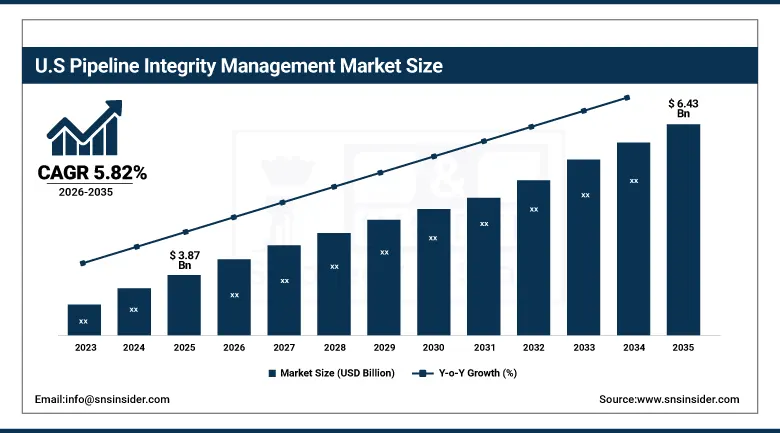

U.S. Pipeline Integrity Management Market was valued at USD 3.87 billion in 2025 and is expected to reach USD 6.43 billion by 2035, growing at a CAGR of 5.82% from 2026-2035.

The U.S. Pipeline Integrity Management Market is the largest in the world, characterized by the extensive oil & gas pipeline network, stringent government safety regulations, and presence of major players like Baker Hughes, Emerson Electric, ROSEN Group, and DNV, among others. The regulatory oversight of Pipeline and Hazardous Materials Safety Administration remains a key determinant for increased focus on integrity management, resulting in wide-spread use of inspection, monitoring, and risk assessment tools.

In addition, major infrastructure buildouts across Texas and the Gulf Coast such as the Permian Highway Pipeline, Matterhorn Express Pipeline, and Gulf Coast Express system are significantly increasing natural gas transport capacity from the Permian Basin to LNG export terminals and industrial hubs. These pipelines are part of a broader midstream expansion cycle aimed at reducing regional price volatility and improving supply reliability across high-demand zones.

Pipeline Integrity Management Market Segment Analysis

-

By Service Type, Inspection Services dominated the Pipeline Integrity Management Market with 39.46% share in 2025; Repair & Refurbishment Services fastest growing (CAGR).

-

By Technology, Intelligent Pigging (ILI) dominated the Pipeline Integrity Management Market with 34.78% share in 2025; AI-Based Predictive Analytics fastest growing (CAGR).

-

By Pipeline Type, Natural Gas Pipelines dominated the Pipeline Integrity Management Market with 46.25% share in 2025; it is also has fastest growing (CAGR).

-

By Location, Onshore Pipelines dominated the Pipeline Integrity Management Market with 62.31% share in 2025; Subsea Pipelines fastest growing (CAGR).

By Service Type, Inspection Services segment dominates the Pipeline Integrity Management Market, Repair & Refurbishment Services segment expected to grow fastest

The Inspection Services segment led the Pipeline Integrity Management Market in terms of market share in 2025, contributing nearly 39.46% of the overall revenue share. The Inspection Services segment consists of In-Line Inspection (ILI) Surveys, Ultrasonic Testing, Magnetic Flux Leakage (MFL) Inspection, Corrosion Monitoring, and integrity assessment to check the status of pipelines and identify defects like cracks, corrosion, and metal loss.

The Repair & Refurbishment Services segment is anticipated to have the highest CAGR from 2026 to 2035. Pipeline failures, leakage issues, and the necessity to enhance the lifespan of the aging infrastructure drive the demand for innovative repair services like composite repair, weld overlay, pipeline replacement, and rehabilitation services.

By Technology, Intelligent Pigging (ILI) segment dominates the Pipeline Integrity Management Market, AI-Based Predictive Analytics segment expected to grow fastest

In 2025, the Intelligent Pigging (ILI) segment dominated the Pipeline Integrity Management Market, generating about 34.78% of overall market revenue. The intelligent pigging segment consists of cleaning pigs, gauging pigs, MFL probes, ultrasonic testing equipment, and geometry measuring equipment. This equipment is utilized for conducting internal inspection and identifying defects in pipelines.

The AI-Based Predictive Analytics segment will witness the fastest CAGR from 2026 to 2035 owing to quick digitalization in the oil & gas industry. AI-based predictive analytics can help operators analyze inspection data, predict corrosion growth, identify probability of leaks, and schedule maintenance work.

By Pipeline Type, Natural Gas Pipelines segment dominates the Pipeline Integrity Management Market, also expected to grow fastest

The Natural Gas Pipelines segment occupied the leading share of the Pipeline Integrity Management Market in 2025 and accounted for around 46.25% of the overall market revenue. The reason behind such a dominance lies in the fast growth of natural gas network construction around the world, higher interest in alternative fuel options, and massive investments into pipelines.

Between 2026 and 2035, the Natural Gas Pipelines segment is also projected to post the highest CAGR. The current trend of moving to low-carbon energy sources, increase in the volume of liquefied natural gas trade, and the role of gas as a transition fuel will contribute to this result.

By Location, Onshore Pipelines segment dominates the Pipeline Integrity Management Market, Subsea Pipelines segment expected to grow fastest

The Onshore Pipelines segment was the leading segment of the Pipeline Integrity Management Market in 2025, with its market share being about 62.31%. The major reason for the leading position of this segment is the widespread use of onshore oil and gas pipelines for crude oil, natural gas, and refined products transportation throughout the world.

During 2026-2035, the fastest CAGR will be demonstrated by the Subsea Pipelines segment due to growing offshore exploration and deepwater production. Growing investments in offshore oil & gas projects in regions such as the Gulf of Mexico, the North Sea, and pre-salt basins in Brazil will stimulate the demand for sophisticated integrity management systems for subsea pipelines.

Pipeline Integrity Management Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

81.31% |

|

Europe |

Germany |

32.48% |

|

Asia Pacific |

China |

41.77% |

|

Middle East & Africa |

UAE |

13.64% |

|

Latin America |

Brazil |

60.24% |

North America Pipeline Integrity Management Market Insights:

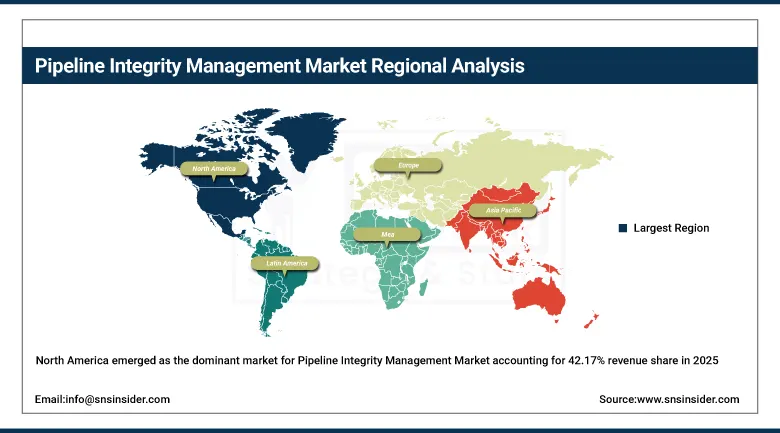

North America emerged as the dominant market for Pipeline Integrity Management Market accounting for 42.17% revenue share in 2025 owing to its well-established midstream oil and gas infrastructures, robust regulatory compliance, and extensive adoption of advanced inspection technologies. North America has a vast network of pipelines, which leads to the increased necessity for regular integrity testing, corrosion monitoring, and preventative maintenance of pipelines. Besides, well-established energy distribution networks and high awareness regarding operational risks associated with pipelines further bolster demand for integrity management solutions in the region.

Furthermore, there is significant momentum in the adoption of integrated digital ecosystem solutions incorporating SCADA systems, IoT sensors, satellite monitoring, and artificial intelligence-based platforms to form an intelligent pipeline layer solution. Such systems help in the early detection of pipeline problems such as micro-leaks, ground movements, and internal corrosion growth, helping reduce unexpected downtime and risk of environmental exposure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Pipeline Integrity Management Market Insights:

Asia Pacific is projected to experience the highest CAGR of 6.74% over the forecast period of 2026-2035 owing to rapid developments in energy infrastructure, increase in oil & gas cross-border transportation networks, and growing investments in pipeline safety & modernization. Nations like China, India, Japan, South Korea, and Australia are some of the main contributing economies, with China expected to contribute significantly to regional demand on account of its massive development plans for natural gas pipeline network, west-east natural gas transmission system, and energy corridor development.

Further, in support of these growth prospects, China National Energy Administration (NEA) and National Development and Reform Commission (NDRC) are actively pursuing efforts in pipeline safety modernization in China.

Furthermore, the Japanese energy and industrial safety regulators are still insisting on maintaining high levels of integrity management in pipelines especially those transporting LNG to the importing terminals and domestic gas distribution networks.

Europe Pipeline Integrity Management Market Insights:

Europe is one of the major regions that dominates the global Pipeline Integrity Management Market, thanks to advanced energy infrastructure, rigorous environmental and safety standards, and a focus on asset reliability through cross-country oil and gas transmission pipelines. Important markets in Europe include Germany, United Kingdom, France, Italy, and Netherlands, which are known for having matured pipeline systems and need to be monitored because of their old age, large population density zones, and tough environmental compliance laws.

Middle East & Africa and Latin America Pipeline Integrity Management Market Insights:

Middle East & Africa (MEA) region as well as the Latin America regions have shown significant growth in the Pipeline Integrity Management Market because of increased investments in the upstream and midstream operations, increased activities of pipeline construction, and the growing importance of avoiding losses from operations and environmental issues. Latin America’s growth is mainly powered by Brazil, Mexico, and Argentina, with offshore operations as well as pipelines linked to refineries being developed. As the emphasis shifts towards minimizing production downtime and minimizing environmental risks, more effort is being made towards investing in intelligent inspection equipment and predictive maintenance technology.

Pipeline Integrity Management Market Growth Drivers:

Rising demand for pipeline safety, environmental protection, and prevention of leakage-related incidents driving global adoption of pipeline integrity management solutions:

The major growth factor of Pipeline Integrity Management Market is the rising importance being attached worldwide to safe and environmentally friendly transportation of oil and gas through pipelines. The increasing importance to avoid failure, minimize the risk of spillage, and maintain uninterrupted supply of energy resources through pipelines has compelled the operators to invest more into integrity management systems. With aging and complex nature of pipeline system, there is a need to constantly monitor the pipeline for any defects and maintain it properly.

Pipeline Integrity Management Market Restraints:

High capital investment and maintenance costs of advanced integrity management technologies restraining widespread adoption across smaller pipeline operators and emerging markets:

A major restraint for the Pipeline Integrity Management Market is that it requires substantial capital and operating expenditures to adopt the latest inspection and monitoring solutions. Intelligent pigs, AI-based predictive analytics, real-time leak detection systems, and digital twin technologies involve substantial initial investments as well as special integration within pipeline infrastructures. Besides, it also necessitates a number of other resources like skilled manpower, data management systems, and software updates. The high cost of implementation is a deterrent for many small and medium-sized pipeline operators.

Pipeline Integrity Management Market Opportunities:

Expanding adoption of advanced digital technologies such as AI-based analytics, digital twin systems, and IoT-enabled monitoring creating significant growth opportunities in pipeline integrity management:

There are several favorable factors that are contributing to the growth of the pipeline integrity management market. The rapid digital transformation that is taking place within the oil and gas industry is opening up a variety of opportunities for pipeline integrity management solutions. The use of technologies such as artificial intelligence-enabled predictive maintenance, real-time sensors, and digital twins makes it possible for organizations to adopt predictive integrity management practices.

Recent Developments:

-

2026: Baker Hughes added to its pipeline integrity and inspection capabilities through the advanced use of AI-enabled asset performance management services and sensing technology on its Cordant™ digital platform. The company also made advances in the use of real-time monitoring technologies for midstream operators in North America and the Middle East, with applications in predictive integrity assessment and emissions monitoring.

-

2025: ROSEN Group further developed its global pipeline inspection services through the advancement of next generation intelligent pigging technology with advanced high-resolution crack detection and corrosion mapping. The company also advanced its digital ROSEN Integrity Platform, allowing operators to leverage inspection data into risk-based integrity assessment models.

-

2025: DNV improved its pipeline integrity advisory and certification offerings through the expansion of pipeline risk models based on digital twin technology, allowing for the simulation of corrosion progression, changes in pressure, and potential pipeline failures. The organization was also involved in developing certification systems for hydrogen-ready pipelines, as part of the energy transition infrastructure development process.

-

2025: SGS extended its offering of pipeline inspection and integrity management services by leveraging more remote inspection tools and artificial intelligence-powered defect detection software. The organization also became more active in offshore pipeline monitoring projects in Europe and Africa, while improving its non-destructive testing (NDT) services for vital energy infrastructure facilities.

Pipeline Integrity Management Market Key Players

-

ROSEN Group

-

DNV

-

SGS

-

Bureau Veritas

-

Emerson Electric

-

T.D. Williamson

-

NDT Global

-

Applus+

-

Schneider Electric

-

TechnipFMC

-

Schlumberger (SLB)

-

Aker Solutions

-

Oceaneering International

-

MISTRAS Group

-

TÜV Rheinland

-

Fluor Corporation

-

Wood PLC

-

Penspen Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.28 Billion |

| Market Size by 2035 | USD 19.44 Billion |

| CAGR | CAGR of 5.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Inspection Services, Cleaning Services, Repair & Refurbishment Services, Risk Assessment Services, Others), • By Technology (Intelligent Pigging (ILI), Leak Detection Systems, GIS & Asset Integrity Software, AI-Based Predictive Analytics, Others), • By Pipeline Type (Natural Gas Pipelines, Crude Oil Pipelines, Refined Product Pipelines, Chemical Pipelines, Others), • By Location (Onshore Pipelines, Offshore Pipelines, Subsea Pipelines, Cross-Country Transmission Pipelines, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Baker Hughes, ROSEN Group, DNV, SGS, Bureau Veritas, Emerson Electric, T.D. Williamson, NDT Global, Applus+, Intertek Group, Schneider Electric, TechnipFMC, Schlumberger (SLB), Aker Solutions, Oceaneering International, MISTRAS Group, TÜV Rheinland, Fluor Corporation, Wood PLC, Penspen Ltd. |

Frequently Asked Questions

The Pipeline Integrity Management Market is expected to grow at a CAGR of 5.64% from 2026 to 2035.

The Pipeline Integrity Management Market was valued at USD 11.28 billion in 2025.

Increasing global energy demand, aging oil & gas pipeline infrastructure, and rising emphasis on operational safety and environmental protection are the primary growth drivers of the Pipeline Integrity Management Market.

The Intelligent Pigging (ILI) segment dominated the Pipeline Integrity Management Market in 2025.

North America dominated the Pipeline Integrity Management Market in 2025.

Get in Touch