Vacuum Blood Collection Tube Market Report Scope & Overview:

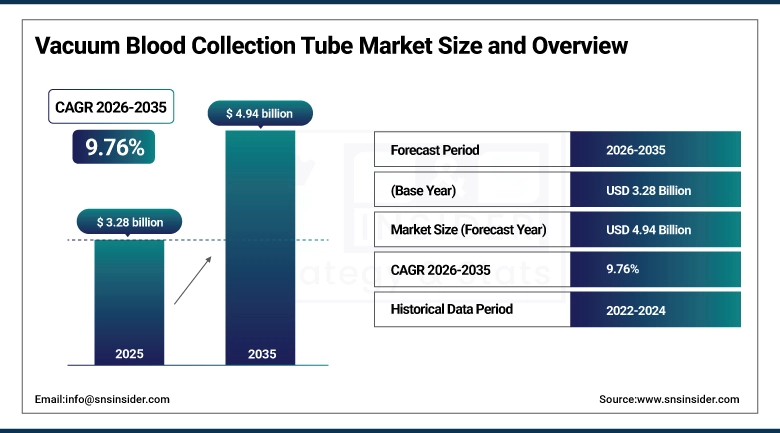

The Vacuum Blood Collection Tube Market size was estimated at USD 3.28 Billion in 2025 and is expected to reach USD 4.94 Billion by 2035 and grow at a CAGR of 4.18% over the forecast period of 2026-2035.

The vacuum blood collection tube market is growing due to increasing demand for accurate and efficient blood collection methods in clinical laboratories and hospitals. Rising prevalence of chronic diseases, expanding healthcare infrastructure, and the need for standardized, contamination-free sample collection are driving adoption. Additionally, advancements in tube materials, safety features, and automation compatibility are encouraging healthcare providers to prefer vacuum blood collection systems, supporting steady market growth across diagnostic and research applications in the U.S.

85% of U.S. clinical and research facilities prioritized vacuum blood collection systems driven by chronic disease burdens, infrastructure expansion, and innovations in safety and automation solidifying their role as the gold standard for accurate, efficient diagnostics.

Market Size and Forecast:

-

Market Size in 2025: USD 3.28 Billion

-

Market Size by 2035: USD 4.94 Billion

-

CAGR: 4.18% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vacuum Blood Collection Tube Market - Request Free Sample Report

Vacuum Blood Collection Tube Market Trends:

-

Rising demand for standardized blood collection to improve diagnostic accuracy and laboratory workflow efficiency

-

Increasing adoption of safety-engineered tubes to reduce needlestick injuries and enhance healthcare worker protection

-

Growth in chronic disease testing driving higher routine blood sample collection volumes globally

-

Expansion of automated laboratory systems boosting demand for compatible vacuum blood collection tubes

-

Rising use of plastic PET tubes over glass for improved safety, durability, and transportation efficiency

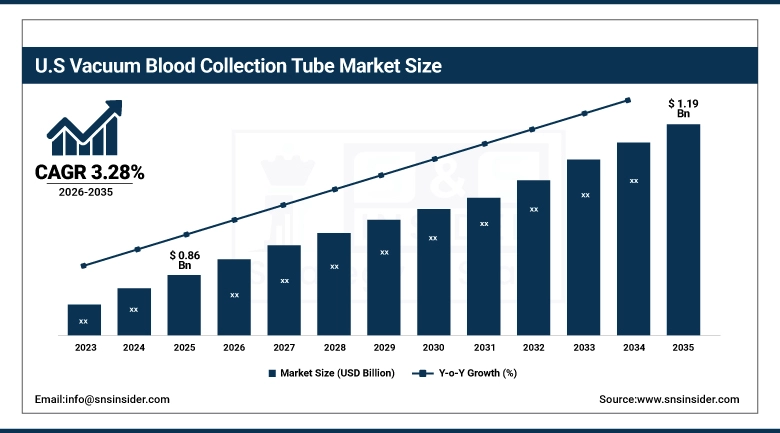

U.S. Vacuum Blood Collection Tube Market is valued at USD 0.86 Billion in 2025 and is expected to reach USD 1.19 Billion by 2035, growing at a CAGR of 3.28% from 2026-2035.

The U.S. vacuum blood collection tube market is growing due to rising demand for efficient, safe, and accurate blood sampling in hospitals and laboratories. Increasing prevalence of chronic diseases, growing diagnostic testing, and adoption of advanced tube technologies are driving steady market expansion across healthcare and research applications.

Vacuum Blood Collection Tube Market Growth Drivers:

-

Rising demand for accurate diagnostic testing and increasing prevalence of chronic and infectious diseases are driving adoption of vacuum blood collection tubes globally

The growing burden of chronic diseases such as diabetes, cardiovascular disorders, and cancer, along with rising incidences of infectious diseases, has significantly increased diagnostic testing volumes worldwide. Accurate and contamination-free blood sample collection is critical for reliable diagnosis and treatment monitoring. Vacuum blood collection tubes ensure standardized sample volume, reduced contamination risk, and improved laboratory efficiency. Hospitals, diagnostic laboratories, and blood banks increasingly prefer these tubes to support high-throughput testing. The expanding role of preventive healthcare and routine health screenings further accelerates demand, making vacuum blood collection tubes essential components of modern diagnostic workflows globally.

83% of clinical labs worldwide increased their use of vacuum blood collection tubes spurred by rising demand for accurate diagnostics and the growing burden of chronic and infectious diseases.

-

Growing healthcare infrastructure development and higher laboratory testing volumes are boosting demand for safe, standardized, and contamination-free blood collection solutions

Investments in healthcare infrastructure, including hospitals, diagnostic centers, and clinical laboratories, are rising across both developed and emerging economies. Increased access to healthcare services has led to higher patient testing volumes, creating demand for efficient and standardized blood collection products. Vacuum blood collection tubes offer safety, ease of use, and compatibility with automated laboratory systems, making them widely adopted. Governments and private healthcare providers emphasize quality diagnostics and patient safety, further supporting adoption. As laboratory automation expands and testing frequency rises, demand for reliable blood collection solutions continues to strengthen market growth.

80% of healthcare systems reported increased demand for safe, standardized, and contamination-free blood collection solutions driven by expanding diagnostic infrastructure and rising laboratory testing volumes globally.

Vacuum Blood Collection Tube Market Restraints:

-

Fluctuating raw material prices and supply chain disruptions increase manufacturing costs, impacting profit margins and pricing stability for vacuum blood collection tube manufacturers

Vacuum blood collection tubes rely on raw materials such as plastics, rubber stoppers, additives, and specialized coatings. Fluctuations in raw material prices, driven by global supply-demand imbalances and geopolitical factors, increase production costs. Supply chain disruptions, including transportation delays and shortages, further challenge manufacturers. These factors reduce pricing flexibility and compress profit margins, particularly for small and mid-sized producers. Manufacturers may face difficulties maintaining competitive pricing while ensuring quality standards. As a result, cost volatility can hinder long-term planning, slow capacity expansion, and limit market growth.

72% of vacuum blood collection tube manufacturers faced margin pressure due to volatile raw material costs and supply chain disruptions leading to pricing instability and delayed product availability in key markets.

-

Risk of needlestick injuries and improper handling in low-resource settings limits adoption and requires continuous training and compliance with strict safety protocols

Despite safety advancements, risks associated with needlestick injuries and improper handling remain significant, especially in low-resource healthcare settings. Limited access to safety-engineered devices, inadequate training, and non-compliance with protocols increase occupational hazards for healthcare workers. These challenges can discourage adoption of vacuum blood collection systems or lead to misuse. Healthcare facilities must invest in continuous staff training, awareness programs, and compliance measures, increasing operational costs. Regulatory scrutiny related to occupational safety further adds complexity. These factors collectively act as barriers to widespread adoption, particularly in underdeveloped healthcare environments.

68% of healthcare facilities in low-resource settings reported constrained adoption of vacuum blood collection systems due to needlestick injury risks and inconsistent handling practices highlighting the critical need for ongoing safety training and protocol enforcement.

Vacuum Blood Collection Tube Market Opportunities:

-

Technological advancements in tube coatings, additives, and safety-engineered designs create opportunities for product innovation and improved diagnostic accuracy

Ongoing innovation in vacuum blood collection tubes, including advanced tube coatings, improved additives, and safety-engineered designs, is enhancing sample integrity and user safety. Innovations such as gel separators, clot activators, and anticoagulant optimization improve diagnostic accuracy and reduce pre-analytical errors. Safety features like retractable needles and protective shields lower injury risks for healthcare workers. Manufacturers investing in research and development can differentiate products, meet evolving regulatory requirements, and address specific clinical needs. These technological advancements create strong opportunities for premium product offerings and long-term market expansion.

76% of vacuum blood collection tube manufacturers introduced advanced coatings, optimized additives, and safety-engineered designs enhancing sample integrity, user safety, and diagnostic accuracy across clinical settings.

-

Expanding diagnostic laboratories and rising healthcare access in emerging economies present significant growth opportunities for vacuum blood collection tube manufacturers

Emerging economies are witnessing rapid expansion of diagnostic laboratories driven by improving healthcare access, urbanization, and government-led health initiatives. Increased awareness of early disease detection and preventive healthcare is boosting testing demand. Public and private investments in laboratory infrastructure create strong demand for reliable blood collection consumables. Vacuum blood collection tubes are preferred for their efficiency, safety, and compatibility with automated analyzers. Manufacturers expanding distribution networks and forming local partnerships in emerging regions can tap into large patient populations, enhance market penetration, and achieve sustained growth over the forecast period.

74% of vacuum blood collection tube manufacturers expanded into emerging economies capitalizing on the rapid growth of diagnostic labs and improved healthcare access to meet surging demand for standardized, reliable sample collection solutions.

Vacuum Blood Collection Tube Market Segmentation Analysis

-

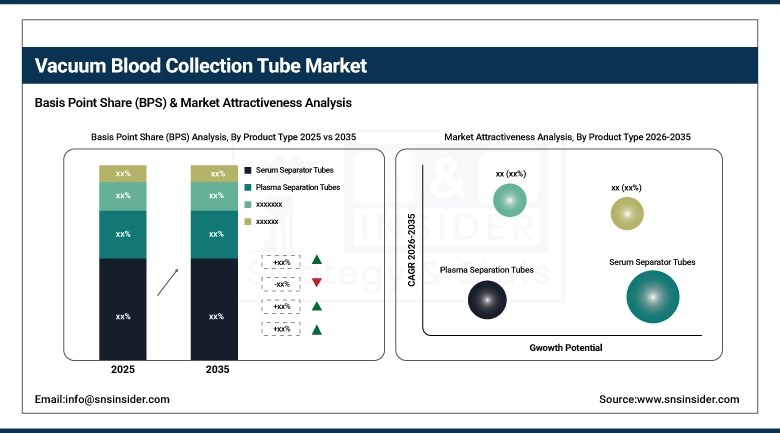

By Product Type: Serum Separator Tubes led with 34.8% share, while EDTA Tubes is the fastest-growing segment with CAGR of 7.1%.

-

By Additive Type: Anticoagulants led with 46.2% share, while Gel Separators is the fastest-growing segment with CAGR of 6.8%.

-

By Application: Clinical Diagnostics led with 57.4% share, while Research & Academic Laboratories is the fastest-growing segment with CAGR of 6.5%.

-

By End User: Diagnostic Laboratories led with 43.9% share, while Blood Collection Centers is the fastest-growing segment with CAGR of 6.9%.

By Product Type: Serum Separator Tubes led, while EDTA Tubes is the fastest-growing segment

Serum Separator Tubes dominate the market because they enable rapid and efficient separation of serum from whole blood, ensuring high-quality samples for clinical diagnostics, routine testing, and research applications. Their compatibility with automated analyzers, standardized performance, and reliability make them widely preferred in hospitals, diagnostic laboratories, and blood collection centers. They also minimize hemolysis and improve test accuracy, which enhances clinical decision-making. Due to their broad adoption across multiple applications and end users, serum separator tubes continue to generate significant revenue and remain the leading product segment in the vacuum blood collection tube market.

EDTA Tubes are the fastest-growing product segment due to their critical role in hematology, molecular testing, and specialized blood analysis. They preserve blood samples by preventing coagulation, allowing accurate cell counting and DNA/RNA-based assays. Rising adoption in research laboratories, increasing demand for molecular diagnostics, and the growth of automated hematology workflows are driving market expansion. EDTA tubes’ stability, ease of handling, and compatibility with modern diagnostic instruments make them highly preferred for advanced testing. Continuous innovation in tube design and global focus on laboratory efficiency support their rapid growth trajectory.

By Additive Type: Anticoagulants led, while Gel Separators is the fastest-growing segment

Anticoagulants dominate the additive type segment because they prevent blood clotting, ensuring that samples remain viable for hematology, coagulation, and molecular analyses. Their widespread use in clinical diagnostics, hospitals, and research laboratories maintains consistent demand. These additives support accurate and reproducible results, making them indispensable in high-volume laboratories. The segment’s dominance is strengthened by the need for standardized sample collection protocols and compatibility with automated analyzers. Reliable anticoagulant tubes contribute to enhanced laboratory efficiency, improved diagnostic outcomes, and reduced sample rejection, ensuring their leading position in the vacuum blood collection tube market.

Gel Separators are the fastest-growing additive segment due to their ability to create a physical barrier between blood cells and plasma or serum after centrifugation. This feature ensures high-quality samples with minimal contamination, enabling accurate and reliable diagnostic results. Growing adoption in clinical laboratories and diagnostic centers, along with rising automation in blood testing, is driving demand. Gel separator tubes improve workflow efficiency, reduce processing time, and enhance sample stability. Increasing awareness among healthcare providers about sample integrity and the need for standardized procedures supports their rapid growth in both clinical and research applications.

By Application: Clinical Diagnostics led, while Research & Academic Laboratories is the fastest-growing segment

Clinical Diagnostics dominates the market as the largest application segment due to the extensive use of vacuum blood collection tubes in routine blood tests, disease diagnosis, and patient monitoring. Hospitals and diagnostic laboratories rely on these tubes for accurate, reproducible, and high-throughput testing. Their compatibility with automated analyzers, standardization, and reliability make them indispensable for routine and specialized testing. The segment’s dominance is reinforced by the high volume of tests conducted globally and the growing prevalence of chronic diseases. Clinical diagnostics remains the primary driver of revenue in the vacuum blood collection tube market.

Research & Academic Laboratories are the fastest-growing application segment as demand rises for precise sample collection in biomedical research, drug development, and molecular biology studies. Vacuum blood collection tubes support high-quality sample preservation, enable reproducible experimental results, and are compatible with advanced laboratory instruments. Increasing investments in research infrastructure, growth of biotechnology and pharmaceutical research, and rising academic research programs globally are driving adoption. These laboratories increasingly require specialized tubes for innovative assays, molecular testing, and analytical research, accelerating the growth of this segment faster than traditional clinical diagnostic applications.

By End User: Diagnostic Laboratories led, while Blood Collection Centers is the fastest-growing segment

Diagnostic Laboratories dominate the end-user segment because they process large volumes of blood samples for routine testing, specialized diagnostics, and clinical monitoring. Vacuum blood collection tubes are essential in these laboratories for reliable, reproducible results and workflow efficiency. Their integration with automated analyzers and quality control protocols ensures high-throughput operations. Diagnostic laboratories are central to hospitals, research institutions, and private healthcare networks, which reinforces their market dominance. Consistent demand for blood testing, clinical monitoring, and diagnostic services makes this segment the largest contributor to revenue in the vacuum blood collection tube market.

Blood Collection Centers are the fastest-growing end-user segment due to the increasing focus on community blood donation, mobile collection programs, and preventive health initiatives. These centers require standardized and reliable vacuum blood collection tubes to ensure sample integrity during collection, storage, and transportation. The growth of voluntary blood donation drives, government health programs, and mobile clinics is boosting demand. Blood collection centers also require tubes compatible with high-throughput screening for infectious diseases and blood typing, driving their adoption. Rising awareness and improved collection infrastructure contribute to the rapid growth of this end-user segment globally.

Regional Insights:

North America Vacuum Blood Collection Tube Market Insights

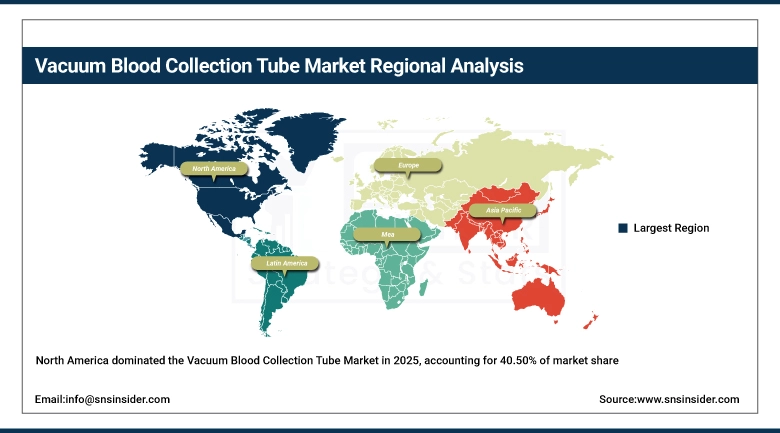

North America dominated the Vacuum Blood Collection Tube Market with a 40.50% share in 2025 due to advanced healthcare infrastructure, high adoption of automated blood collection systems, and strong presence of leading diagnostic and laboratory equipment manufacturers. Growing demand for efficient sample collection, supportive reimbursement policies, and focus on clinical accuracy further strengthened the region’s market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Vacuum Blood Collection Tube Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 6.07% from 2026–2035, driven by rising healthcare infrastructure investments, increasing diagnostic testing, and growing awareness of efficient and safe blood collection methods. Expanding hospital networks, adoption of modern laboratory technologies, and increasing prevalence of chronic diseases accelerate market growth across the region.

Europe Vacuum Blood Collection Tube Market Insights

Europe held a significant share in the Vacuum Blood Collection Tube Market in 2025, supported by well-established healthcare systems, high adoption of automated and standardized blood collection processes, and strong presence of key manufacturers. Growing demand for diagnostic testing, stringent regulatory standards, and focus on laboratory efficiency further strengthened Europe’s market position.

Middle East & Africa and Latin America Vacuum Blood Collection Tube Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Vacuum Blood Collection Tube Market in 2025, driven by increasing healthcare infrastructure investments, rising diagnostic testing demand, and growing awareness of safe and efficient blood collection methods. Expanding hospital networks, government initiatives to improve clinical diagnostics, and adoption of modern laboratory technologies supported regional market development.

Competitive Landscape:

Becton, Dickinson and Company (BD) is a global medical technology leader specializing in medical devices, laboratory equipment, and diagnostic products, including vacuum blood collection tubes. BD is renowned for its high-quality, reliable, and safe products that support accurate blood collection and testing. The company focuses on innovation, safety, and workflow efficiency, serving hospitals, laboratories, and diagnostic centers worldwide. Its advanced vacuum blood collection systems enhance patient safety, reduce contamination risks, and ensure precise sample handling.

-

June 2024, BD launched the BD Vacutainer Plus line featuring Eco-Safe Tubes made with 30% less plastic and chlorine-free stoppers, alongside BD One Digital ID a 2D Data Matrix code on every tube for full pre-analytical traceability.

Terumo Corporation, headquartered in Japan, is a leading global healthcare company offering a wide range of medical devices, including vacuum blood collection tubes. Terumo focuses on product innovation, safety, and quality to improve clinical outcomes. Its blood collection tubes are designed to ensure sample integrity, reduce contamination, and optimize laboratory workflows. Terumo’s strong global presence and commitment to research and development make it a trusted provider of high-performance medical and diagnostic solutions in hospitals and laboratories worldwide.

-

November 2023, Terumo introduced a Vacuum Integrity Indicator (VII) on its Terumo Blood Collection Tubes, a visual seal that changes color if vacuum is compromised during storage or transport.

Greiner Bio-One International GmbH, based in Austria, is a prominent manufacturer of laboratory and diagnostic products, including vacuum blood collection tubes. The company emphasizes precision, reliability, and safety in its product portfolio, supporting accurate blood sampling and analysis. Greiner Bio-One invests in research and development to enhance usability, sample integrity, and workflow efficiency. Its solutions are widely used in hospitals, diagnostic laboratories, and research institutions, establishing the company as a key player in the global blood collection and diagnostics market.

-

February 2025, Greiner Bio-One launched VACUETTE 360° Traceability, embedding QR codes on all vacuum blood collection tubes that link to a cloud-based platform for real-time lot tracking, compliance documentation, and CO₂ footprint data.

Vacuum Blood Collection Tube Market Key Players:

-

Becton, Dickinson and Company (BD)

-

Terumo Corporation

-

Greiner Bio-One International GmbH

-

Sarstedt AG & Co. KG

-

Cardinal Health

-

Sekisui Chemical Co., Ltd.

-

FL Medical S.r.l.

-

Hongyu Medical

-

Improve Medical Instruments Co., Ltd.

-

TUD SDN BHD

-

Sanli Medical

-

Gong Dong Medical

-

CDRICH

-

Xinle Medical Co., Ltd.

-

Lingen Precision Medical

-

WEGO

-

Kang Jian Medical

-

Poly Medicure Ltd.

-

AB Medical, Inc.

-

CML Biotech Pvt. Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.28 Billion |

| Market Size by 2035 | USD 4.94 Billion |

| CAGR | CAGR of 4.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Serum Separator Tubes, Plasma Separation Tubes, EDTA Tubes, Heparin Tubes, Sodium Citrate Tubes) • By Additive Type (Clot Activators, Anticoagulants, Gel Separators) • By Application (Clinical Diagnostics, Blood Banks, Research & Academic Laboratories) • By End User (Hospitals, Diagnostic Laboratories, Blood Collection Centers, Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Becton, Dickinson and Company (BD), Terumo Corporation, Greiner Bio-One International GmbH, Sarstedt AG & Co. KG, Cardinal Health, Sekisui Chemical Co., Ltd., FL Medical S.r.l., Hongyu Medical, Improve Medical Instruments Co., Ltd., TUD SDN BHD, Sanli Medical, Gong Dong Medical, CDRICH, Xinle Medical Co., Ltd., Lingen Precision Medical, WEGO, Kang Jian Medical, Poly Medicure Ltd., AB Medical, Inc., CML Biotech Pvt. Ltd. |

Frequently Asked Questions

The Vacuum Blood Collection Tube Market is valued at USD 3.28 Billion in 2025 and is projected to grow significantly over the forecast period.

The market is expected to reach USD 4.94 Billion by 2035, driven by increasing demand for diagnostic testing and blood sampling procedures.

The market is anticipated to grow at a CAGR of 4.18% during the forecast period from 2026 to 2035.

Key drivers include rising prevalence of chronic diseases, increasing diagnostic testing, advancements in healthcare infrastructure, and growing demand for safe blood collection methods.

Vacuum blood collection tubes are used for collecting, transporting, and storing blood samples for laboratory analysis and diagnostic testing.

Get in Touch