Veneer Sheets Market Report Scope & Overview:

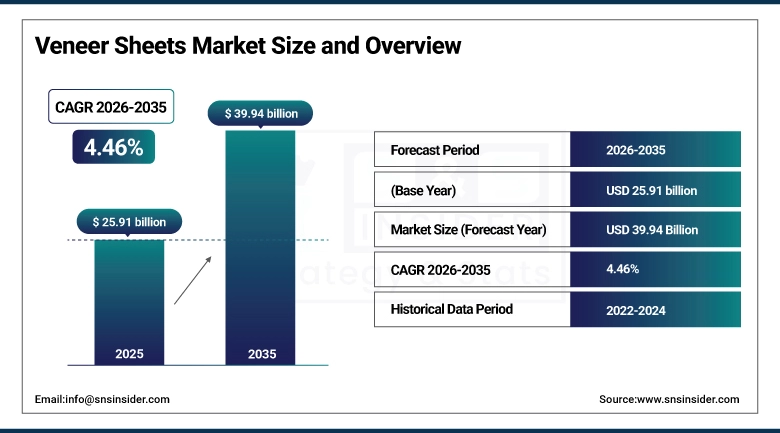

The Veneer Sheets Market size was valued at USD 25.91 Billion in 2025 and is projected to reach USD 39.94 Billion by 2035, growing at a CAGR of 4.46% during 2026-2035.

The Veneer Sheets Market is progressing steadily through the forecast period, underpinned by the global furniture manufacturing industry's sustained demand for thin decorative wood slices that apply the appearance and tactile quality of premium hardwood species to engineered wood substrate panels at a fraction of the material cost of solid wood construction.

Veneer Sheets Market Size and Forecast:

-

Market Size in 2025: USD 25.91 Billion

-

Market Size by 2035: USD 39.94 Billion

-

CAGR : 4.46% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Veneer Sheets Market - Request Free Sample Report

Key Veneer Sheets Market Trends

-

Rising demand for eco-friendly and sustainably sourced veneer sheets driven by green building and low-VOC interior materials.

-

Increasing adoption of engineered and reconstituted veneers offering uniform texture, cost efficiency, and design flexibility.

-

Growing use of decorative veneers in premium furniture and luxury interior applications across residential and commercial spaces.

-

Expansion of digital printing and advanced finishing technologies enabling customized veneer designs and patterns.

-

Strong growth in renovation and remodeling activities boosting demand for aesthetic wood-based surface materials.

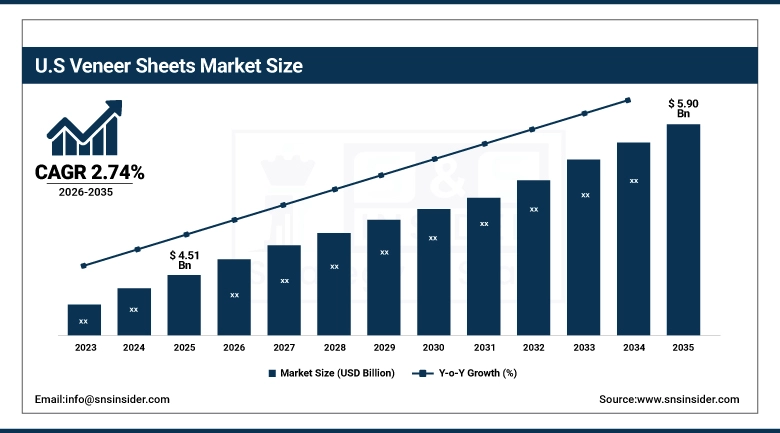

The U.S. Veneer Sheets Market size was valued at USD 4.51 Billion in 2025 and is projected to reach USD 5.90 Billion by 2035, growing at a CAGR of 2.74% during 2026-2035. The U.S. market is the dominant national market within North America, anchored by the country's large residential furniture manufacturing and kitchen cabinet industry that consumes veneer sheets in the production of cabinet doors, drawer fronts, and furniture panels sold through the home improvement retail, custom cabinetry, and wholesale furniture channels that collectively represent the most stable and consistent demand source for veneer products in the region.

Veneer Sheets Market Growth Drivers:

-

Veneer Sheets Market Growth Drivers Rising demand for premium interior design furniture manufacturing expansion and sustainable wood material adoption globally

The market for veneer sheets is currently undergoing significant growth owing to the rising demand for attractive and economical interior solutions in construction projects both residential and commercial. Urbanization along with the rise in disposable income levels is driving the manufacture of furniture, particularly in emerging countries. The growing inclination towards a wooden look with lower consumption of materials has led to the use of veneer sheets. The development of infrastructure in real estate, hospitality, and offices has further aided the growth of the market. Furthermore, technological developments in cutting and bonding processes have improved the quality and design of veneer sheets.

Veneer Sheets Market Restraints:

-

Veneer Sheets Market Restraints High raw material cost supply chain disruptions environmental regulations and limited hardwood availability constraints

There are some restraints in the veneer sheets market which might act as barriers to its growth such as changes in price levels and lack of quality timber sources as raw materials. Environmental laws governing deforestation activities lead to shortage in supply of raw materials for production. Transportation issues add to rising costs associated with manufacturing. The presence of competing man-made options also lowers demand for veneer sheets. Processing costs and reliance on trained manpower are other factors which hamper expansion for smaller manufacturers.

Veneer Sheets Market Opportunities:

-

Veneer Sheets Market Opportunities Growing green construction renovation demand digital printing innovation and emerging economy infrastructure development expansion

The global market for veneer sheets offers numerous opportunities due to rising use of sustainable construction materials and environmentally friendly interior decoration styles. Growing remodeling and renovation of both domestic and commercial structures will lead to high demand for decorative surfaces. Innovative technologies like digital printing and engineered veneers facilitate personalized designs, which will attract more consumers. Fast-paced construction activities in developing nations and the hotel and property industries will generate more growth opportunities. Moreover, growing emphasis on light and economical products will offer substantial growth opportunities for companies in the coming years.

Veneer Sheets Market Segment Analysis

-

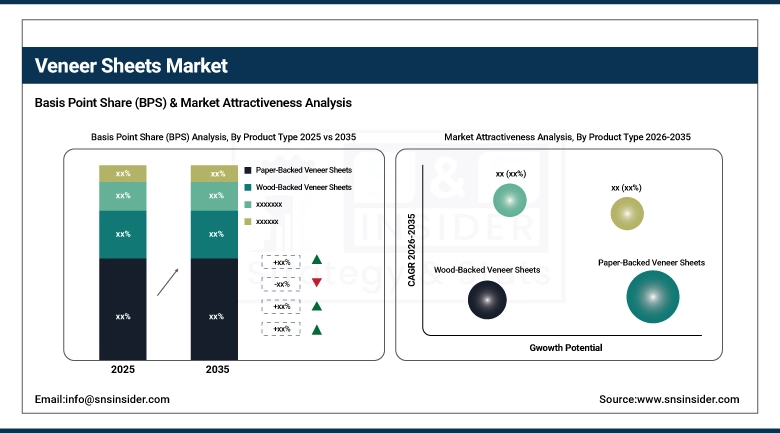

By Product Type, Paper-Backed Veneer Sheets dominated with 34.26% in 2025, and Engineered / Reconstituted Veneer Sheets are expected to grow at the fastest CAGR of 6.39% from 2026 to 2035.

-

By Wood Type / Raw Material, Hardwood Veneers dominated with 46.72% in 2025, and Engineered / Reconstituted Wood is expected to grow at the fastest CAGR of 6.23% from 2026 to 2035.

-

By Application, Furniture Manufacturing dominated with 41.87% in 2025, and Flooring & Others are expected to grow at the fastest CAGR of 5.80% from 2026 to 2035.

-

By End-Use Industry, Commercial (Offices, Hospitality, Retail) dominated with 44.62% in 2025, and Industrial is expected to grow at the fastest CAGR of 5.14% from 2026 to 2035.

By Product Type, Paper-Backed Veneer Sheets Lead Veneer Sheets Market While Engineered / Reconstituted Veneer Set for Fastest Growth 2026 to 2035

Product type-based veneer sheets market growth is seen with growing inclination towards flexible and cost-efficient decorative sheets that can be applied within the interiors of contemporary buildings. There is popularity among paper-backed veneer sheets on account of ease of use, design flexibility, and their adaptability to mass-scale furniture and panel making. Wood-backed veneer sheets are opted because of higher durability and sturdiness. The phenolic-backed veneer sheets have gained significance due to high resistance capability within the industrial environment. Growing popularity is also seen among engineered and reconstituted veneer sheets because of consistent design quality and effective wood resource utilization.

By Wood Type / Raw Material, Hardwood Veneers Lead Veneer Sheets Market While Engineered / Reconstituted Wood Shows Fastest Growth 2026 to 2035

Veneer Sheets by Types of Wood Market Drivers The primary driver for veneer sheets by types of wood market is hardwood veneer sheets because they are popular due to their excellent grain pattern, higher strength, and aesthetic appeal. Hardwood is also the most common source of wood used in premium housing and commercial construction projects. Softwood veneer sheets are commonly used for low-cost products where weight and economy are critical factors. Engineered and reconstituted wood products are becoming popular due to their sustainability benefits and uniform quality. They also reduce the reliance on natural wood. Bamboo and alternative wood products are also gaining traction in eco-friendly designs.

By Application, Furniture Manufacturing Leads Veneer Sheets Market While Flooring & Others Show Fastest Growth 2026 to 2035

The applications segment in the veneer sheets market is dominated by furniture manufacture as it continues to consume a bulk of these products in order to obtain wooden looks in its products at an affordable price. These products have been widely utilized in furniture such as cabinets, wardrobes, tables, and modular furniture in order to give natural wooden looks. The interior decoration segment has experienced increased utilization owing to the rising demand for luxurious and customized interiors. The segment for doors and windows also plays an important role as the use of veneer sheets gives the look of quality materials.

By End-Use Industry, Commercial Leads and Industrial Shows Fastest Growth in Veneer Sheets Market 2026 to 2035

The market of veneer sheets by end-use industry is highly dependent on the commercial industry that comprises offices, hospitality venues, retail stores, and corporate infrastructure development projects. The industry extensively uses veneer sheets to create elegant interior settings that not only improve aesthetic value but also project the brand identity of organizations. The residential sector plays an important role in demand creation because of increased construction activities in cities and modern interior solutions for houses. There are minimal applications in the industrial sector but stable growth is anticipated in installations that focus on utility purposes and require wood-based panels.

Veneer Sheets Market Regional Analysis

Europe Veneer Sheets Market Insights

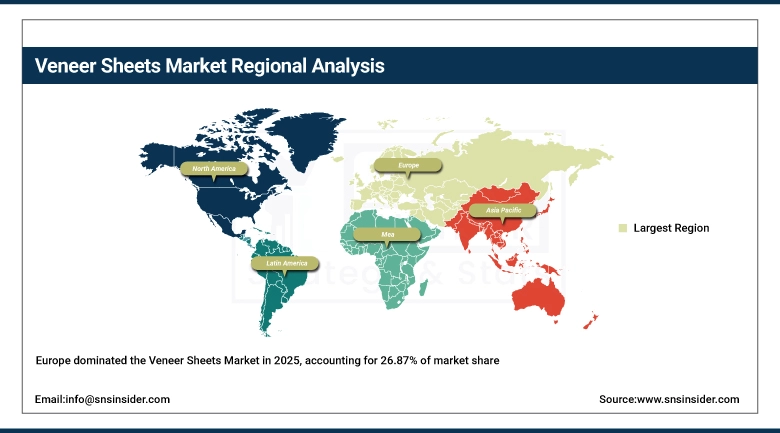

Europe held 26.87% at USD 6.96 Billion in 2025, growing at a CAGR of 3.52% through 2035. Europe is the global center of premium veneer processing technology and a significant producer of high-value sliced and engineered veneer sheets for the domestic and global market. Germany, Italy, France, and Belgium host the most technically advanced veneer processing and distribution companies in the world, including Danzer Group, DECOSPAN, Remy & Geiser, and Tabu SpA, whose product development and quality standards define the global premium natural veneer market. European furniture manufacturers in Italy, Germany, and Poland are among the highest-volume consumers of premium veneer sheets in the global market, with the Italian furniture industry's design leadership and German kitchen cabinet manufacturing's quality standards creating consistent demand for high-specification veneer products that commodity laminate alternatives cannot substitute in these market segments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Germany Veneer Sheets Market Insights

Germany was the leading national market for veneer sheets in Europe in 2025, driven by the country's large kitchen furniture and office furniture manufacturing industries that are among the most significant consumers of hardwood veneer sheets in Europe, the presence of Danzer Group's European headquarters and veneer processing operations, and a commercial construction and renovation market that specifies veneer-surfaced millwork and joinery in premium office, retail, and hospitality interior projects at quality levels consistent with Germany's position as Europe's largest commercial real estate market.

North America Veneer Sheets Market Insights

North America held a 22.13% share of the global Veneer Sheets Market in 2025 at USD 5.73 Billion, growing at the slowest regional CAGR of 3.07% through 2035. The region's moderate growth rate reflects the maturity of veneer adoption in its primary furniture and cabinetry manufacturing applications, where the installed base of production equipment and the established supplier relationships of North American furniture manufacturers with veneer distributors provide a stable but slowly growing demand base. The U.S. kitchen cabinet and residential furniture industries are the primary demand drivers, supplemented by commercial interior fit-out demand in the hospitality renovation and corporate office markets of major U.S. and Canadian cities. Danzer Group's North American distribution operations and Columbia Forest Products' domestic hardwood veneer production provide the most significant North American supply infrastructure alongside imports from European and Asian veneer producers.

U.S. Veneer Sheets Market Insights

The United States dominated North America's veneer sheets market at 78.64%, USD 4.51 Billion in 2025. The U.S. remains the largest national market in North America with demand anchored in residential furniture, kitchen cabinetry, and architectural millwork manufacturing that consumes hardwood veneers primarily in oak, cherry, maple, and walnut species.

Asia Pacific Veneer Sheets Market Insights

Asia Pacific is the largest and fastest-growing region at a CAGR of 5.59% through 2035, valued at USD 11.38 Billion in 2025 and projected to reach USD 19.56 Billion by 2035. China is the dominant national market and the world's largest single producer and consumer of veneer sheets, with a massive furniture manufacturing export industry that surfaces engineered wood panel products with decorative veneer for European, North American, and domestic consumption. Vietnam has become the world's fastest-growing furniture export manufacturing nation, with its veneer sheet consumption growing proportionally with the country's furniture production output that now targets global retail and online furniture brands seeking lower-cost manufacturing alternatives to Chinese production. India's expanding commercial real estate and premium residential construction market is generating growing demand for veneer-surfaced interior products, and the domestic Indian veneer industry is developing processing capacity to serve this demand alongside imports from Malaysian and Chinese veneer distributors.

China Veneer Sheets Market Insights

China is the market leader in the Asia-Pacific veneer sheets market owing to the presence of a huge furniture manufacturing industry wood processing industry export-oriented nature and high levels of construction activity. India trails behind with a fast-growing urban population demand for housing facilities interior design and furniture manufacturing industries.

Latin America (LATAM) and Middle East & Africa (MEA) Veneer Sheets Market Insights

Latin America was valued at USD 1.05 Billion in 2025 and is growing at a CAGR of 3.02% through 2035, with Brazil and Mexico representing the two primary national markets driven by domestic furniture manufacturing and construction sector demand. Brazil's large domestic furniture industry, which produces both for domestic consumption and limited export, is the primary veneer sheet consumer in the region, with the country's own hardwood resource base including eucalyptus plantation timber providing some domestic veneer raw material that supplements imports from Asian and European producers. Middle East and Africa was valued at USD 0.78 Billion in 2025 and is growing at the fastest regional CAGR of 6.14% through 2035, reaching USD 1.42 Billion by 2035, with Gulf state hospitality and luxury residential construction driving premium natural and engineered veneer demand in hotel room joinery, lobby cladding, and high-specification residential interior fit-out projects that collectively represent the highest per-square-meter specification value in the global market.

Competitive Landscape for Veneer Sheets Market:

Danzer Group, headquartered in Sylva, North Carolina with European headquarters in Wuerzburg, Germany, is one of the world's largest veneer producers and distributors, operating sawmills, veneer processing plants, and distribution facilities across North America and Europe that give it the most geographically comprehensive natural veneer supply infrastructure of any company in the market. Danzer's sliced veneer production from European and North American hardwood species including oak, walnut, cherry, and beech supplies furniture manufacturers, architectural millwork shops, and interior design material distributors across global markets, and the company's investment in digital veneer matching and inventory management systems allows large-project clients to specify and receive matched veneer lots for architectural paneling applications that require visual consistency across large wall areas.

-

In 2024, Danzer Group expanded its veneer processing capacity at its Ebersdorf, Germany facility to address growing order volumes from European commercial interior fit-out customers, with the expansion specifically focused on quarter-sliced oak and walnut veneer production lines where demand from premium office and hospitality interior design projects had extended delivery lead times beyond the committed scheduling windows for large-project clients.

DECOSPAN, headquartered in Menen, Belgium, is Europe's leading distributor and processor of natural and engineered veneer sheets, supplying an extensive range of wood species and backed veneer formats to furniture manufacturers, interior designers, and panel product producers across Europe and export markets. DECOSPAN's product range encompasses natural sliced veneers in more than 100 wood species, engineered and reconstituted veneers, and value-added finished veneer panels that allow customers to procure veneer products ready for immediate application rather than requiring in-house backing and finishing operations.

- In 2024, DECOSPAN launched an expanded range of FSC-certified reconstituted veneer sheets produced from plantation poplar and beech raw materials, specifically targeting furniture and interior design customers with mandatory sustainable sourcing procurement policies that require documented chain-of-custody certification for all wood materials used in their products, a requirement that natural exotic wood veneers frequently cannot meet due to the sourcing complexity of tropical hardwood supply chains.

Veneer Sheets Market Key Players:

-

Danzer Group

-

Tabu S.p.A.

-

Remy & Geiser GmbH

-

Lamigraf S.A.

-

Columbia Forest Products

-

Oakio

-

ALPI S.p.A.

-

Herzog Veneers

-

Shaanxi Wenyu International Wood Industry

-

Shandong Shengda Timber

-

Sri Venkateshwara Plywood Industries

-

Riken Technos

-

National Wood Products

-

Papoutsanis S.A.

-

RIESNER Furniere GmbH

-

Krono Group

-

Flexible Materials Inc.

-

Rosenthal & Rosenthal

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.91 Billion |

| Market Size by 2035 | USD 39.94 Billion |

| CAGR | CAGR of 4.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Paper-Backed Veneer Sheets, Wood-Backed Veneer Sheets, Phenolic-Backed Veneer Sheets, and Engineered / Reconstituted Veneer Sheets), • By Wood Type / Raw Material (Hardwood Veneers, Softwood Veneers, Engineered / Reconstituted Wood, and Bamboo & Alternative Materials) • By Application (Furniture Manufacturing, Interior Decoration (Wall Panels, Ceilings), Doors & Windows, and Flooring & Others) • By End-Use Industry (Residential, Commercial (Offices, Hospitality, Retail), and Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Arkema S.A., Allnex GmbH, Covestro AG, Celanese Corporation, DIC Corporation, Eastman Chemical Company, Evonik Industries AG, H.B. Fuller Company, Huntsman Corporation, Lubrizol Corporation, Momentive Performance Materials Inc., Nan Ya Plastics Corporation, Solvay S.A., Synthomer plc, Wanhua Chemical Group, Hexion Inc., ADEKA Corporation, Olin Corporation |

Frequently Asked Questions

Ans: Asia Pacific led the Veneer Sheets Market in 2025 with a 43.92% share.

Paper-Backed Veneer Sheets dominated the Veneer Sheets Market with a 34.26% share in 2025.

Ans: Key drivers include sustained demand from global furniture manufacturing and commercial interior fit-out activity, growing adoption of engineered and reconstituted veneer sheets as sustainable alternatives to natural rare wood veneers, and rapid Asia Pacific construction and interior decoration market expansion.

The Veneer Sheets Market size was USD 25.91 Billion in 2025 and is projected to reach USD 39.94 Billion by 2035.

The Veneer Sheets Market is expected to grow at a CAGR of 4.46% from 2026-2035.

Get in Touch