Vertebral Augmentation Market Report Scope & Overview:

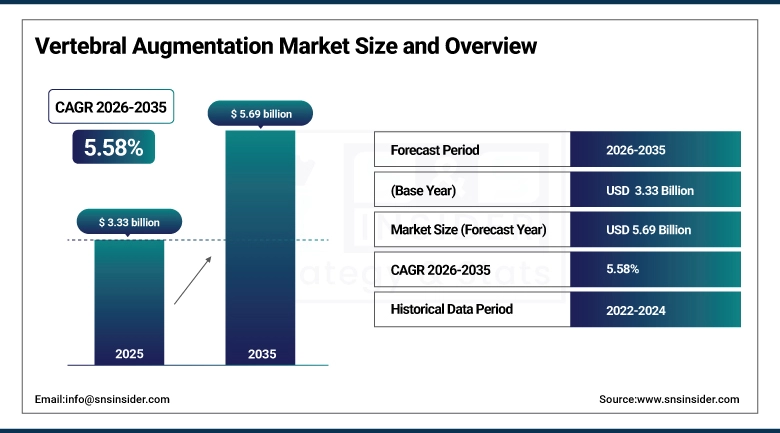

The Vertebral Augmentation Market was valued at USD 3.33 billion in 2025 and is expected to reach USD 5.69 billion by 2035, growing at a CAGR of 5.58% from 2026-2035.

The Vertebral Augmentation Market is largely propelled by the growing number of vertebral compression fractures due to osteoporosis and increasing elderly populations globally. The growing inclination toward minimally invasive surgical techniques like kyphoplasty and vertebroplasty, which help patients recover quickly and stay in hospitals for less time, is a major contributor. Growth is additionally being accelerated through innovations in bio-materials and bone cement, as well as an increased use of ambulatory surgery centers.

Supporting this trend, the International Osteoporosis Foundation estimates that over 200 million people worldwide suffer from osteoporosis, with nearly 1 in 3 women and 1 in 5 men over the age of 50 expected to experience osteoporotic fractures in their lifetime.

In addition, regulatory bodies such as the U.S. Food and Drug Administration have been actively supporting innovation in spinal intervention technologies. In recent years, the agency has cleared and approved several advanced bone cement formulations, image-guided systems, and minimally invasive spinal devices aimed at improving procedural safety and clinical outcomes.

Vertebral Augmentation Market Size and Forecast

-

Market Size in 2025: USD 3.33 Billion

-

Market Size by 2035: USD 5.69 Billion

-

CAGR: 5.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vertebral Augmentation Market - Request Free Sample Report

Vertebral Augmentation Market Trends

-

Rising prevalence of osteoporosis and vertebral compression fractures is significantly increasing procedural volumes worldwide.

-

Growing preference for minimally invasive spine procedures is driving adoption of vertebroplasty and kyphoplasty techniques.

-

Technological advancements in image-guided navigation and robotic-assisted systems are improving procedural accuracy and safety.

-

Increasing use of advanced bone cement formulations is enhancing biomechanical stability and reducing complications such as leakage.

-

Expansion of outpatient and ambulatory surgical centers is shifting procedures away from traditional hospital settings.

-

Integration of AI and real-time imaging technologies is supporting better surgical planning and outcomes.

-

Rising healthcare investments in emerging economies are improving access to advanced spinal treatments.

-

Strategic collaborations and product innovations by key players are intensifying market competition and technological progress.

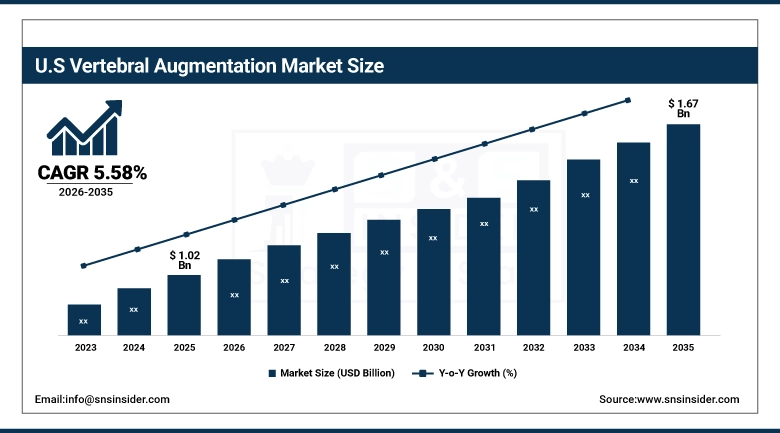

U.S. Vertebral Augmentation Market was valued at USD 1.02 billion in 2025 and is expected to reach USD 1.67 billion by 2035, growing at a CAGR of 5.58% from 2026-2035.

U.S. Vertebral Augmentation Market is witnessing significant growth, fueled by growing instances of osteoporosis and spinal fractures amongst elderly patients. The increased utilization of minimally-invasive techniques like vertebroplasty and kyphoplasty, coupled with favorable market dynamics for the same, is driving demand. Technological innovations in image guided and robot-assisted systems have improved surgical outcomes.

Supporting this trend, the Centers for Disease Control and Prevention highlights that osteoporosis affects millions of Americans, contributing to over 1.5 million fractures annually, with vertebral compression fractures among the most common. This growing burden of age-related bone disorders is expanding the eligible patient pool for vertebral augmentation procedures such as kyphoplasty and vertebroplasty across the United States.

In addition, the U.S. Food and Drug Administration continue to accelerate approvals and clearances for advanced spinal technologies, including innovative bone cement systems and image-guided minimally invasive devices.

Vertebral Augmentation Market Segment Highlights

-

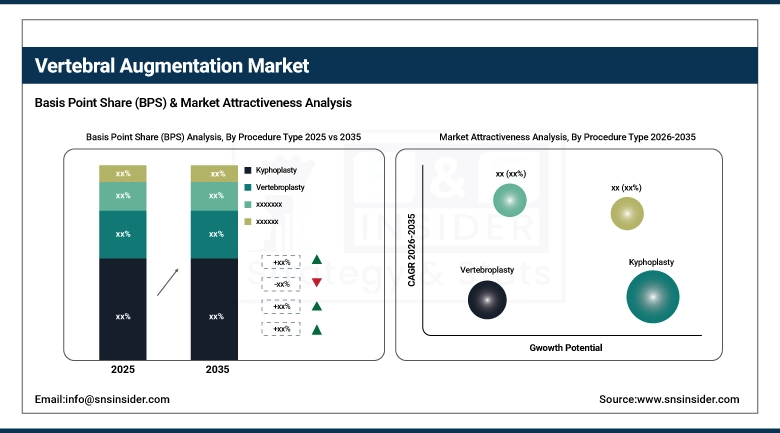

By Procedure Type, Kyphoplasty dominated the Vertebral Augmentation Market with 45.43% share in 2025; Balloon Kyphoplasty fastest growing (CAGR).

-

By Material Type, Bone Cement (PMMA) dominated the Vertebral Augmentation Market with 49.61% share in 2025; Hybrid Materials (cement + biologics) fastest growing (CAGR).

-

By Application, Osteoporosis-related fractures dominated the Vertebral Augmentation Market with 54.78% share in 2025; Metastatic lesions fastest growing (CAGR).

-

By End User, Hospitals dominated the Vertebral Augmentation Market with 48.59% share in 2025; Ambulatory Surgical Centers (ASCs) fastest growing (CAGR).

Vertebral Augmentation Market Segment Analysis

By Procedure Type, Kyphoplasty segment dominates the Vertebral Augmentation Market, Balloon Kyphoplasty expected to grow fastest

The Kyphoplasty segment held its market dominance in the Vertebral Augmentation Market in 2025, contributing around 45.43% to the total revenue generated. This is credited to its effectiveness in restoring the height of the vertebral body, fixing spinal deformations, and offering quick pain relief in comparison to vertebroplasty.

Between 2026 and 2035, the Balloon Kyphoplasty segment is expected to register the fastest CAGR due to sustained innovation in technology and rising inclination towards precision-oriented spinal surgery. The application of inflatable bone tamp enables the creation of cavities and efficient delivery of bone cement.

By Material Type, Bone Cement (PMMA) segment dominates the Vertebral Augmentation Market, Hybrid Materials expected to grow fastest

In 2025, the Bone Cement (PMMA) product type captured the biggest market share in the Vertebral Augmentation Market, contributing nearly 49.61% towards the overall market revenue. It holds a high market position owing to clinical popularity, mechanical properties, and instant vertebral stability in compression fractures. PMMA cement will remain the most preferred choice because of its low cost, ease of handling, and history of successful applications.

From 2026 to 2035, the Hybrid Materials (cement + biologics) segment is projected to register the highest CAGR, supported by growing interest in regenerative and biologically integrated solutions. These materials combine structural support with enhanced bone healing and biocompatibility, reducing long-term complications and improving patient outcomes.

By Application, Osteoporosis-related fractures segment dominates the Vertebral Augmentation Market, Metastatic lesions expected to grow fastest

Osteoporosis-related fractures held a share of about 54.78% of the total revenue, being the highest revenue-generating application segment of the Vertebral Augmentation Market in 2025. The widespread occurrence of osteoporosis cases, especially among elderly patients, has been the key factor behind the rising number of vertebral compression fractures worldwide.

The fastest growth rate in terms of CAGR is projected to be recorded by the Metastatic lesions segment from 2026 to 2035 due to the growing global cancer epidemic and the rising prevalence of spinal metastasis. Vertebral augmentation procedures have become popular as a palliative approach to stabilize vertebrae, relieve pain, and improve patient quality of life.

By End User, Hospitals segment dominates the Vertebral Augmentation Market, Ambulatory Surgical Centers (ASCs) expected to grow fastest

In 2025, the Hospitals segment accounted for the largest market share of 48.59%. Hospitals are still considered the most favorable venue for carrying out vertebral augmentation operations because of the sophisticated imaging equipment, skilled medical practitioners, and follow-up care. The capability of hospitals to manage complicated and risky situations will further cement their dominance in the market.

During the forecast period from 2026 to 2035, ASCs are predicted to witness the fastest growth rate in terms of CAGR. The trend towards outpatient surgery and efficient and less expensive healthcare is the driving force behind the demand for ASCs. ASCs provide faster surgeries, shorter hospital stays, and lower costs compared to hospitals. The advent of technology that promotes safe and efficient minimally invasive procedures will further bolster the trend.

Vertebral Augmentation Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38.71% |

|

Europe |

Germany |

24.55% |

|

Asia Pacific |

China |

22.76% |

|

Middle East & Africa |

UAE |

6.30% |

|

Latin America |

Brazil |

7.68% |

North America Vertebral Augmentation Market Insights

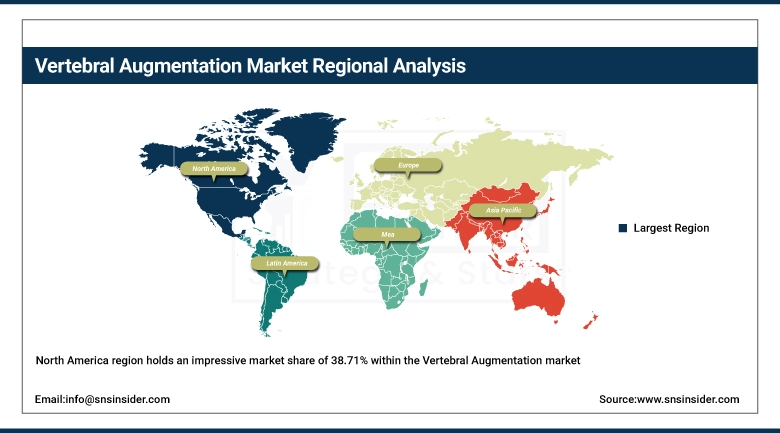

The North America region holds an impressive market share of 38.71% within the Vertebral Augmentation market, due to the high incidence of osteoporosis and vertebral compression fractures. The high number of elderly patients in the region, well-established health care infrastructure, adoption of minimally invasive spinal surgeries, and positive reimbursement scenarios are driving the market growth in this region. Apart from this, the region has been witnessing consistent technological developments in the field of kyphoplasty devices and bone cements, along with the presence of key medical device companies.

Supporting this dominance, the Centers for Medicare & Medicaid Services has continued to expand reimbursement coverage for minimally invasive spinal procedures, including vertebral augmentation performed in hospital outpatient departments and ambulatory surgical centers. This has significantly improved patient access and encouraged wider adoption of kyphoplasty and vertebroplasty across the region.

According to the American Academy of Orthopaedic Surgeons, vertebral compression fractures affect 100 of thousands of patients annually in North America, largely driven by osteoporosis and aging demographics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Vertebral Augmentation Market Insights

The Asia Pacific market for Vertebral Augmentation is one of the fastest-growing markets, with CAGR at 6.50%. The market is being fueled by the fast-growing population of older people and the increasing occurrence of osteoporotic fractures in nations such as China, Japan, and India. Better healthcare infrastructure, rising knowledge about minimally invasive spine surgery, and the growing trend of medical tourism are driving adoption rates. Healthcare access investments by governments and the entry of multinational players into the market have also contributed to growth. In addition, there is an increase in the availability of new technology in kyphoplasty procedures.

Supporting this growth, the National Health Commission of the People's Republic of China has prioritized osteoporosis management and elderly care within national health programs, promoting early diagnosis and wider access to minimally invasive spinal treatments across public hospitals. This has accelerated the adoption of vertebral augmentation procedures, particularly in urban tertiary care centers.

In addition, Japan’s Ministry of Health, Labour and Welfare has expanded reimbursement frameworks for advanced spinal interventions, including kyphoplasty for osteoporotic vertebral fractures. Combined with the country’s rapidly aging population and strong clinical infrastructure, these policies are significantly driving procedural volumes and supporting sustained market growth across the Asia Pacific region.

Europe Vertebral Augmentation Market Insights

The Europe region plays a major role in the Vertebral Augmentation market, due to increasing numbers of elderly patients and a high incidence of osteoporotic vertebral fractures in nations like Germany, France, and the United Kingdom. The existence of a mature healthcare infrastructure and positive reimbursement environment makes the use of minimally invasive spinal procedures feasible. There is also a rising trend in awareness about early diagnosis and treatment, coupled with innovations in kyphoplasty techniques, which is contributing positively to the growth of the market.

Supporting this position, the European Commission has prioritized musculoskeletal health and active aging initiatives under its regional health programs, encouraging early diagnosis and management of osteoporosis across member states. This has increased awareness and screening rates for vertebral compression fractures, thereby supporting higher adoption of minimally invasive procedures such as kyphoplasty and vertebroplasty across Europe.

In addition, Germany’s Federal Joint Committee (G-BA) has reinforced reimbursement frameworks for advanced spinal interventions within its statutory health insurance system. Coupled with Germany’s strong hospital infrastructure and high procedural volumes in orthopedic and spine care.

Middle East & Africa and Latin America Vertebral Augmentation Market Insights

The Middle East & Africa and Latin America markets have shown consistent growth in the Vertebral Augmentation market due to factors such as increased healthcare services availability, increase in osteoporosis cases, and awareness about minimally invasive techniques for spine care. In the Middle Eastern region, nations like Saudi Arabia and UAE have been making significant investments in their healthcare programs, leading to advancements in spine care treatment technology and the establishment of hospitals equipped with advanced technology. On the African continent, gradual developments in healthcare facilities along with the emphasis on non-communicable diseases are facilitating the early adoption of vertebral augmentation methods.

Supporting development in these regions, Saudi Arabia’s Ministry of Health Saudi Arabia has been advancing national healthcare transformation initiatives by expanding specialized orthopedic and spine care services, including the adoption of minimally invasive procedures for vertebral compression fractures.

In Brazil, the Agência Nacional de Vigilância Sanitária (ANVISA) has continued to enhance regulatory pathways for innovative spinal devices, including bone cement technologies and kyphoplasty systems. This streamlined approval environment, combined with growing investments in private healthcare infrastructure, is facilitating faster adoption of vertebral augmentation procedures across both public and private healthcare networks.

Vertebral Augmentation Market Growth Drivers:

-

Rising prevalence of osteoporosis and vertebral compression fractures driving global adoption of vertebral augmentation procedures

The escalating prevalence of osteoporosis, especially in elderly individuals, is one of the critical structural factors shaping the market dynamics of the Vertebral Augmentation market. VCFs represent one of the most prevalent types of fragility fractures, which cause debilitating symptoms such as chronic pain and loss of mobility, significantly impacting the patient’s quality of life. As patients become aware of the benefits offered by minimal interventions like kyphoplasty and vertebroplasty, which alleviate pain instantly and help restore spinal stability, physicians too prefer such procedures over traditional conservative approaches.

Supporting this growth, the International Osteoporosis Foundation reports that osteoporosis affects over 200 million people worldwide and is responsible for millions of fractures annually, with vertebral fractures being the most frequent.

The World Health Organization further emphasizes that musculoskeletal conditions are a leading cause of disability globally, significantly impacting mobility and independence, particularly in older adults. This growing disease burden is accelerating demand for effective, minimally invasive vertebral augmentation procedures as healthcare providers aim to improve quality of life and functional outcomes.

Vertebral Augmentation Market Restraints:

-

High procedural costs and reimbursement limitations restricting widespread adoption of vertebral augmentation

High costs related to vertebral augmentation surgery, such as those involved in kyphoplasty system, balloon and bone cement products, constitute the most prominent hurdle to the growth of the market. These procedures usually demand sophisticated imaging equipment, expertise, and an institution setting, hence increasing the cost of care. Additionally, lack of proper reimbursement in many developing nations poses another challenge. Small-scale hospitals will take time to adopt the technology because of high capital requirements, whereas patients will prefer conservative pain management techniques due to economic considerations.

Vertebral Augmentation Market Opportunities:

-

Advancements in biomaterials and outpatient care expansion creating new growth opportunities in vertebral augmentation

The advancement in next-generation biomaterials, such as bioactive cements and biohybrid systems that incorporate biologics, is paving the way for better patient results and bone regeneration in clinical settings. This progress in science is improving safety, decreasing the risk of complications like cement extravasation, and widening the scope of application of vertebroplasty interventions. In parallel, the trend toward ASCs and outpatient spine surgery is facilitating economical care pathways and improving accessibility and volume of treatments. Physicians are more willing to allocate financial resources to support their minimally invasive spine practice.

Recent Developments:

-

2025: Medtronic expanded its spine portfolio with advanced vertebral augmentation systems, including next-generation kyphoplasty balloons and high-viscosity bone cement solutions designed to improve fracture stabilization and reduce leakage risk. The company also strengthened its image-guided spine surgery ecosystem, supporting more precise and efficient minimally invasive vertebral procedures across global hospital networks.

-

2026: Stryker enhanced its spinal intervention offerings through upgrades to its vertebral augmentation product line, focusing on improved cement delivery systems and procedural efficiency. The company also expanded integration between its navigation technologies and spine solutions, enabling better accuracy and workflow optimization in minimally invasive vertebral fracture treatments.

-

2025: DePuy Synthes advanced its minimally invasive spine portfolio by introducing innovative vertebral augmentation solutions and expanding its biomaterials capabilities. The company emphasized clinical education initiatives and surgeon training programs to accelerate adoption of kyphoplasty procedures and improve patient outcomes in osteoporotic fracture management.

-

2025: Zimmer Biomet strengthened its spine segment by launching enhanced bone cement technologies and minimally invasive vertebral augmentation tools aimed at improving procedural safety and consistency. The company also focused on expanding its presence in outpatient settings, supporting the growing shift toward ambulatory surgical centers for spine interventions.

Vertebral Augmentation Market Key Players

Some of the Vertebral Augmentation Market Companies

-

Medtronic

-

Stryker

-

DePuy Synthes (Johnson & Johnson)

-

Zimmer Biomet

-

Globus Medical

-

NuVasive

-

B. Braun Melsungen AG

-

K2M (part of Stryker)

-

Orthofix Medical

-

Alphatec Spine

-

Cook Medical

-

Osseon Therapeutics

-

Spine Wave

-

Vexim (subsidiary of Stryker)

-

Benvenue Medical

-

Izi Medical Products

-

Medacta International

-

Tecres S.p.A.

-

Spirit Spine

-

Joimax GmbH

Vertebral Augmentation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.33 Billion |

| Market Size by 2035 | USD 5.69 Billion |

| CAGR | CAGR of 5.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Procedure Type (Kyphoplasty, Vertebroplasty, Balloon Kyphoplasty, Others), • By Material Type (Bone Cement (PMMA), Biomaterials, Bone Grafts, Hybrid Materials (cement + biologics), Others), • By Application (Osteoporosis-related fractures, Spinal fractures (trauma), Tumor-related vertebral collapse, Metastatic lesions, Others), • By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Research & Academic Institutes, Others), |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic, Stryker, DePuy Synthes (Johnson & Johnson), Zimmer Biomet, Globus Medical, NuVasive, B. Braun Melsungen AG, K2M (part of Stryker), Orthofix Medical, Alphatec Spine, Cook Medical, Osseon Therapeutics, Spine Wave, Vexim (subsidiary of Stryker), Benvenue Medical, Izi Medical Products, Medacta International, Tecres S.p.A., Spirit Spine, Joimax GmbH. |

Frequently Asked Questions

North America dominated the Vertebral Augmentation Market in 2025.

The Kyphoplasty segment dominated the Vertebral Augmentation Market in 2025.

The major growth factor rising global burden of osteoporosis, vertebral compression fractures, faster recovery times, minimal scarring, reduced postoperative complications.

The Vertebral Augmentation Market was valued at USD 3.33 billion in 2025.

The Vertebral Augmentation Market is expected to grow at a CAGR of 5.58% from 2026 to 2035.

Get in Touch