Viral Inactivation Market Report Scope & Overview:

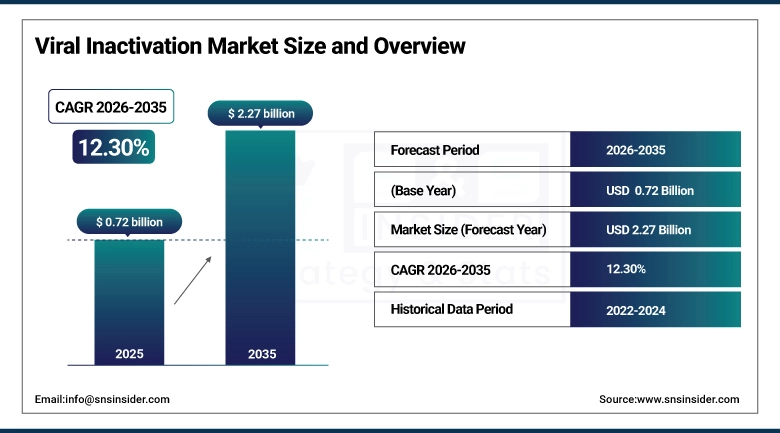

The Viral Inactivation Market was valued at USD 0.72 Billion in 2025 and is expected to reach USD 2.27 Billion by 2035, growing at a CAGR of 12.30% from 2026–2035.

The market for Viral Inactivation is experiencing significant growth owing to the fast growth in the manufacturing process of biologics and biosimilars, growing demand for virus safety in the production process of monoclonal antibodies and recombinant proteins, and rising trend of outsourcing bioprocessing operations to CMOs/CDMOs. The complexity associated with advanced therapies, like cell and gene therapy, has increased the demand for reliable methods of viral inactivation and clearance.

Supporting this trend, the International Society for Pharmaceutical Engineering (ISPE) has highlighted a significant increase in biologics manufacturing capacity expansion projects globally, particularly in North America and Asia-Pacific, which is directly driving demand for advanced viral inactivation solutions in both commercial and clinical production environments.

In parallel, regulatory harmonization initiatives such as the ICH Q5A(R2) guideline update on viral safety evaluation of biotechnology products have strengthened global compliance frameworks, accelerating adoption of standardized viral inactivation methods across the biopharmaceutical industry.

Market Size and Forecast:

-

Market Size in 2025: USD 0.72 Billion

-

Market Size by 2035: USD 2.27 Billion

-

CAGR: 12.30% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Viral Inactivation Market - Request Free Sample Report

Viral Inactivation Market Trends:

-

Rising adoption of monoclonal antibodies, biosimilars, and recombinant biologics is significantly increasing the demand for robust viral inactivation steps in downstream bioprocessing.

-

Expanding pipeline of cell and gene therapies is driving the need for highly validated viral clearance technologies to ensure product safety and regulatory compliance.

-

Increasing outsourcing of biologics manufacturing to CMOs and CDMOs is accelerating standardized adoption of scalable viral inactivation systems across global production facilities.

-

Rapid integration of advanced filtration technologies, including nanofiltration and membrane-based systems, is enhancing viral removal efficiency and process reliability.

-

Growing implementation of single-use bioprocessing systems is improving contamination control and enabling more efficient and flexible viral inactivation workflows.

-

Increasing regulatory emphasis on viral safety validation by agencies such as FDA, EMA, and ICH is strengthening compliance-driven adoption of multi-step viral inactivation strategies.

-

Rising use of low pH, solvent/detergent, and hybrid inactivation methods is improving process robustness across diverse biologics manufacturing platforms.

-

Expanding investment in continuous bioprocessing and automated downstream systems is enabling higher throughput and consistent viral clearance performance.

-

Increasing demand for high-purity vaccines and plasma-derived therapeutics is reinforcing the critical role of viral inactivation in ensuring product safety and global supply reliability.

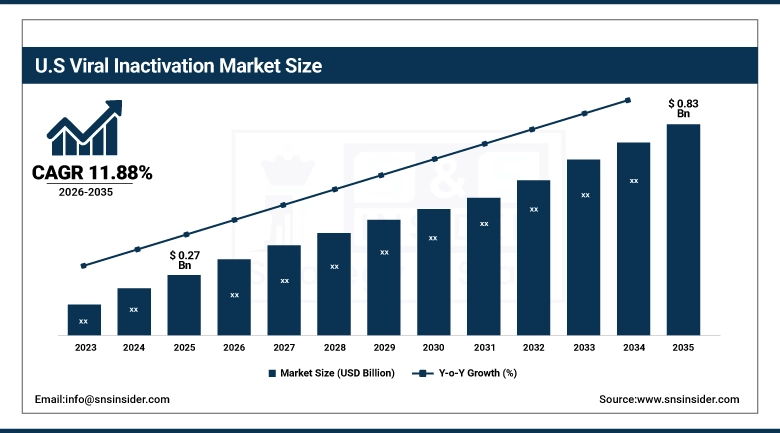

The U.S. Viral Inactivation Market was valued at USD 0.27 Billion in 2025 and is expected to reach around USD 0.83 Billion by 2035, growing at a CAGR of 11.88% from 2026–2035.

The United States holds the highest market share among all countries globally because of its highly advanced manufacturing process, presence of major manufacturers of biological drugs, and CDMOs. Increase in the use of monoclonal antibodies, recombinant proteins, vaccines, and cell and gene therapy is boosting the demand for efficient and safe viral inactivation methods during the production process.

Supporting this growth, the U.S. Food and Drug Administration (FDA) continues to enforce stringent viral safety requirements for biologics and biosimilars approval pathways, ensuring consistent adoption of validated viral inactivation protocols in manufacturing processes.

Additionally, sustained funding from the National Institutes of Health (NIH) toward biologics, vaccine development, and advanced therapeutic platforms is reinforcing long-term demand for viral safety technologies in preclinical and translational research environments.

Viral Inactivation Market Segment Highlights:

-

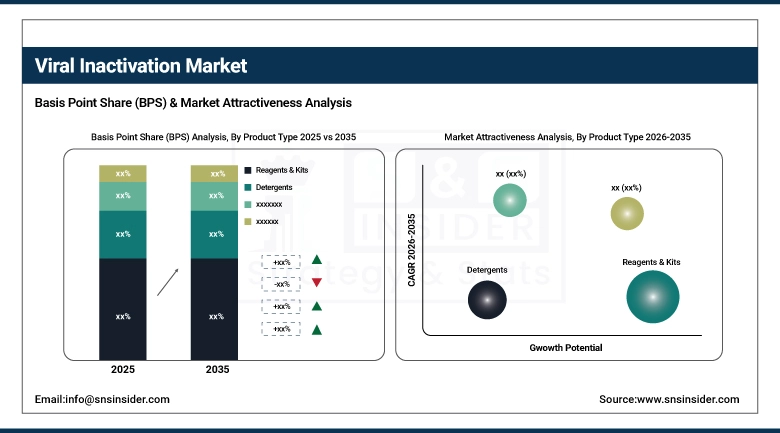

By Product Type, Reagents & Kits dominated the Viral Inactivation Market with 41.36% share in 2025; Pathogen Reduction Systems is the fastest-growing segment

-

By Method, Solvent/Detergent (S/D) Inactivation dominated the Viral Inactivation Market with 44.15% share in 2025; Low pH Inactivation is the fastest-growing segment.

-

By Application, Monoclonal Antibody Production dominated the Viral Inactivation Market with 33.85% share in 2025; Cell and advanced biologics-related applications (captured under Others) are the fastest-growing segment.

-

By End-User, Pharmaceutical & Biopharmaceutical Companies dominated the Viral Inactivation Market with 46.24% share in 2025; Contract Manufacturing Organizations (CMOs/CDMOs) are the fastest-growing segment

-

By Scale of Operation Preclinical & R&D Scale dominated the Viral Inactivation Market with 32.51% share in 2025; Commercial Manufacturing Scale is the fastest-growing segment.

By Product Type, Reagents & Kits segment dominates the Viral Inactivation Market, Pathogen Reduction Systems expected to grow fastest

In 2025, the Reagents & Kits segment maintained its dominant position in the Viral Inactivation Market, accounting for 41.36% of total revenue. This leadership is primarily attributed to their widespread use across biopharmaceutical manufacturing workflows, ease of integration into standardized viral safety protocols, and high reliability in ensuring consistent viral clearance outcomes. Reagents and kits are extensively utilized in monoclonal antibody production, recombinant protein manufacturing, and vaccine development, where validated and reproducible viral inactivation steps are critical for regulatory compliance.

From 2026 to 2035, the Pathogen Reduction Systems segment is projected to record the highest CAGR. This rapid growth is driven by increasing demand for advanced, multi-modal viral safety solutions capable of addressing emerging and complex biologics such as cell and gene therapies.

By Method, Solvent/Detergent (S/D) Inactivation segment dominates the Viral Inactivation Market, Low pH Inactivation segment expected to grow fastest

The Solvent/Detergent (S/D) Inactivation segment held the largest share of 44.15% in 2025, The process is propelled by its longstanding regulatory approval, proven efficacy against enveloped viruses, and extensive application in plasma-based therapies and monoclonal antibody production. Its reliability, scalability, and suitability for biologics manufacturing have positioned it as the gold standard for viral inactivation techniques worldwide.

The Low pH Inactivation segment is expected to register the highest CAGR during the 2026–2035 forecast period. Growth is primarily supported by increasing adoption in monoclonal antibody purification processes, where low pH conditions provide efficient viral clearance with minimal impact on product integrity.

By Application, Monoclonal Antibody Production segment dominates the Viral Inactivation Market, Cell & Gene Therapy-related applications (included under Others) expected to grow fastest

In 2025, the Monoclonal Antibody Production segment maintained its dominant position in the Viral Inactivation Market, accounting for 33.85% of total revenue. The dominance is fueled by the huge global demand for therapeutic antibodies for oncology, autoimmune diseases, and infections, where viral safety testing is an absolute requirement for production. The robust existing manufacturing processes and large-scale production of biological products strengthen its leadership in the marketplace.

From 2026 to 2035, cell and advanced biologics-related applications (included under Others) are projected to record the highest CAGR. This growth is fueled by the rapid expansion of cell therapy, gene therapy, and regenerative medicine pipelines, where stringent viral safety requirements are essential.

By End-User, Pharmaceutical & Biopharmaceutical Companies segment dominates the Viral Inactivation Market, CMOs/CDMOs segment expected to grow fastest

The Pharmaceutical & Biopharmaceutical Companies segment maintained the highest end-user share of 46.24% in 2025. The dominance stems from the strength of their internal capacity to manufacture biological drugs, their ability to produce monoclonal antibodies and recombinant proteins in large quantities, and their strict internal quality controls on validation of viral safety. They remain committed to investing in integrated platforms for viral inactivation to comply with regulations and maintain product purity.

The Contract Manufacturing Organizations (CMOs/CDMOs) segment is projected to achieve the highest growth rate during 2026–2035.

By Scale of Operation, Preclinical & R&D Scale segment dominates the Viral Inactivation Market, Commercial Manufacturing Scale segment expected to grow fastest

The Preclinical & R&D Scale segment held the largest share of 32.51% in 2025. This dominance arises from the widespread application of viral inactivation procedures at the early stages of biologics development such as feasibility testing, proof of concept investigation, and preclinical safety assessment. The rising number of activities in gene therapy, monoclonal antibodies, and recombinant protein drugs has greatly boosted the need for small-scale and adaptable viral inactivation technologies.

The Commercial Manufacturing Scale segment is projected to register the highest CAGR during 2026–2035.

Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

43.59% |

|

Europe |

Germany |

27.44% |

|

Asia Pacific |

China |

23.89% |

|

Middle East & Africa |

UAE |

3.04% |

|

Latin America |

Brazil |

2.04% |

North America Viral Inactivation Market Insights

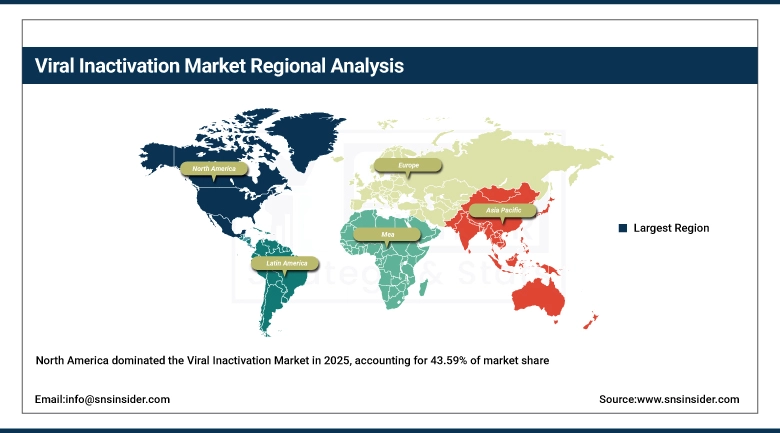

North America held the dominant position in the global Viral Inactivation Market with 43.59% revenue share in 2025, owing to the sophistication of its biologics manufacturing ecosystem, robust regulatory compliance regime, and early use of viral safety technology validation processes. The geographical area features an abundance of monoclonal antibody manufacturers, vaccine makers, and contract development and manufacturing organizations (CDMOs), in addition to solvent/detergent treatment processes, nanofiltration technologies, and low pH inactivation methodologies being used by commercial manufacturers. North America holds the biggest market share within the geographic region, bolstered by robust biologics pipelines, extensive outsourcing practices, and growing infrastructure for good manufacturing practice (GMP)-compliant manufacturing capacity.

Supporting this dominance, the U.S. Food and Drug Administration (FDA) continues to enforce stringent viral safety requirements for biologics and biosimilars, ensuring mandatory implementation of multi-step viral inactivation and clearance validation across production workflows. This regulatory rigor is significantly strengthening technology adoption across both clinical and commercial manufacturing environments.

Additionally, increasing investments in biologics manufacturing capacity expansion by leading CDMOs and biopharma companies are accelerating deployment of advanced viral inactivation platforms, particularly in monoclonal antibody and cell-based therapeutic production lines.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Viral Inactivation Market Insights

The Asia Pacific region is projected to register the highest CAGR of 13.33% from 2026–2035, driven by rapid expansion of biologics manufacturing capabilities, increasing outsourcing of production services, and strong government support for biotechnology infrastructure development. Countries such as China, India, Japan, South Korea, and Singapore are emerging as key contributors, with China and India leading in large-scale CDMO expansion and cost-efficient biologics production.

Supporting this growth, regulatory authorities such as China’s National Medical Products Administration (NMPA) and India’s Central Drugs Standard Control Organization (CDSCO) are increasingly aligning with global GMP standards, promoting adoption of validated viral inactivation protocols in both domestic and export-oriented biologics manufacturing.

In addition, rapid expansion of vaccine production capacity, rising investment in biosimilars development, and growing presence of global pharmaceutical companies in Asia Pacific are accelerating adoption of scalable viral safety technologies across the region.

Europe Viral Inactivation Market Insights

In 2025, Europe accounted for a substantial market share in the global market because of its extensive research ecosystem in biologics, highly developed pharmaceutical production capabilities, and a well-developed regulatory landscape favoring the development of advanced therapies. Countries such as Germany, UK, Switzerland, and France have been prominent users of virus inactivation techniques due to a high presence of biopharmaceutical companies and dedicated CDMOs.

Supporting this position, the European Medicines Agency (EMA) continues to enforce strict viral safety guidelines for biologics and advanced therapy medicinal products (ATMPs), ensuring standardized implementation of viral inactivation and clearance validation across manufacturing processes.

Additionally, increasing adoption of continuous bioprocessing technologies, expansion of GMP-certified CDMO capacity, and strong funding under EU research frameworks are reinforcing Europe’s role as a key hub for innovation-driven viral safety solutions.

Latin America, Middle East & Africa (LAMEA) Viral Inactivation Market Insights

The LAMEA region is experiencing steady growth in the Viral Inactivation Market, driven by gradual expansion of biopharmaceutical manufacturing capabilities, increasing participation in global vaccine supply chains, and rising awareness of biologics-based therapies. Countries such as Brazil, Mexico, South Africa, Saudi Arabia, and the UAE are emerging as important contributors to regional demand, particularly in vaccine production and plasma-derived therapeutics.

Governments in the Middle East, especially in Saudi Arabia and the UAE, are actively investing in biotechnology clusters and precision medicine initiatives, enabling early adoption of viral safety technologies and strengthening regional biomanufacturing capabilities.

In addition, increasing collaborations between local healthcare authorities and global pharmaceutical companies are enhancing technology transfer, improving GMP compliance, and gradually expanding the adoption of viral inactivation systems in emerging markets.

Viral Inactivation Market Growth Drivers:

-

Rising demand for biologics, vaccines, and advanced therapies is driving strong adoption of validated viral inactivation technologies across global biopharmaceutical manufacturing pipelines

Key Structural Drivers for the Viral Inactivation Market are attributed to the fast-growing trend of biologics manufacturing, which includes monoclonal antibodies, recombinant proteins, vaccines, and plasma products that need to be made free from viruses because this is required by law. With more diverse and complicated biologics pipelines, companies are resorting to viral inactivation methods that include solvent detergent process, low pH treatment, and nanofiltration.

Supporting this growth, the International Society for Pharmaceutical Engineering (ISPE)highlights a continuous global expansion of biologics manufacturing capacity, particularly in North America and Asia Pacific, where new production facilities are increasingly designed with built-in viral inactivation and closed-system processing technologies to meet stringent regulatory expectations.

Additionally, regulatory momentum from global agencies such as the U.S. FDA and European Medicines Agency (EMA) is reinforcing mandatory viral safety validation across all biologics and biosimilars, accelerating adoption of multi-step viral inactivation protocols and advanced filtration-based technologies in both early-stage and large-scale manufacturing.

Viral Inactivation Market Restraints:

-

High process complexity and validation intensity of viral inactivation workflows is increasing operational burden and limiting scalability, especially for small and mid-sized biopharma manufacturers

The key limitation in the Viral Inactivation Market is the extremely complicated multi-stage viral safety testing process that is needed during the manufacturing of biologic products. Techniques such as solvent/detergent treatment, low pH viral inactivation, heat treatment, and nanofiltration need to be thoroughly optimized, tested, and monitored for their ability to fully eliminate viruses without impacting product safety.

Viral Inactivation Market Opportunities:

-

Expansion of integrated biologics manufacturing ecosystems and advanced purification technologies is creating strong opportunities for scalable, high-efficiency viral safety solutions across global production networks

The largest opportunity that exists in the Viral Inactivation Market is the fast evolution of the worldwide biologics manufacturing to an ecosystem of end-to-end manufacturing processes, whereby viral safety is part of the process itself, rather than being done separately. This is due to the ever-growing complexity of biologics manufacturing, such as that of monoclonal antibodies, biosimilar and plasma derived drugs.

Recent Developments:

-

2026: Lonza Group expanded its global biologics manufacturing network with enhanced viral safety integration across new large-scale CDMO facilities in the U.S. and Europe, incorporating advanced solvent/detergent and nanofiltration systems to support rising demand for monoclonal antibody and cell therapy production.

-

2026: Thermo Fisher Scientific strengthened its bioprocessing portfolio by upgrading its viral safety workflow solutions, including improved single-use filtration systems and automated viral clearance validation tools, supporting faster scale-up of biologics manufacturing in North America and Asia-Pacific.

-

2025: Merck KGaA (MilliporeSigma) launched next-generation viral filtration and inactivation consumables designed for high-throughput biologics production, enhancing process efficiency and regulatory compliance for monoclonal antibody and recombinant protein manufacturing.

-

2025: Sartorius AG expanded its integrated bioprocess solutions portfolio with advanced low pH viral inactivation and closed-system processing technologies, aimed at improving scalability and consistency in commercial biologics production environments globally.

Viral Inactivation Market Key Players:

-

Sartorius AG

-

Thermo Fisher Scientific Inc.

-

Cytiva (Danaher Corporation)

-

WuXi AppTec

-

Pall Corporation (Danaher)

-

Texcell SA

-

Eurofins Scientific

-

SGS SA

-

Cerus Corporation

-

Terumo Blood and Cell Technologies

-

Rad Source Technologies Inc.

-

Bio-Rad Laboratories

-

Parker Hannifin Corporation

-

Catalent Inc.

-

Boehringer Ingelheim BioXcellence

-

Clean Cells (Sartorius Group)

-

Syngene International Ltd.

Viral Inactivation Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.72 Billion |

| Market Size by 2035 | USD 2.27 Billion |

| CAGR | CAGR of 12.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Reagents & Kits, Detergents (Solvent/Detergent Systems), pH Adjustment Solutions, Pathogen Reduction Systems, Viral Filtration Systems, Other Consumables) • By Method (Solvent/Detergent (S/D) Inactivation, Heat Treatment (Pasteurization), Low pH Inactivation, UV-C Irradiation, Nanofiltration-Based Inactivation, Others) • By Application (Monoclonal Antibody Production, Vaccines, Blood & Plasma Derivatives, Recombinant Proteins, Cell & Gene Therapy Products, Stem Cell Research, Others) • By End-User (Pharmaceutical & Biopharmaceutical Companies, Contract Manufacturing Organizations (CMOs/CDMOs), Research Institutes & Academic Laboratories, Blood Banks & Plasma Fractionation Centers, Biotechnology Companies) • By Scale of Operation (Preclinical & R&D Scale, Clinical Scale, Commercial Manufacturing Scale) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Merck KGaA, Sartorius AG, Charles River Laboratories, Thermo Fisher Scientific Inc., Lonza Group, Cytiva (Danaher Corporation), WuXi AppTec, Pall Corporation (Danaher), Texcell SA, Eurofins Scientific, SGS SA, Cerus Corporation, Terumo Blood and Cell Technologies, Rad Source Technologies Inc., Bio-Rad Laboratories, Parker Hannifin Corporation, Catalent Inc., Boehringer Ingelheim BioXcellence, Clean Cells (Sartorius Group), Syngene International Ltd. |

Frequently Asked Questions

North America dominated the Viral Inactivation Market in 2025.

The Reagents & Kits segment dominated the Viral Inactivation Market in 2025.

Rapid expansion of biologics, including monoclonal antibodies, vaccines, and advanced therapeutics, is the primary growth driver of the Viral Inactivation Market.

The Viral Inactivation Market was valued at USD 0.72 billion in 2025.

The Viral Inactivation Market is expected to grow at a CAGR of 12.30% from 2026 to 2035.

Get in Touch