Vision Screeners Market Report Scope & Overview:

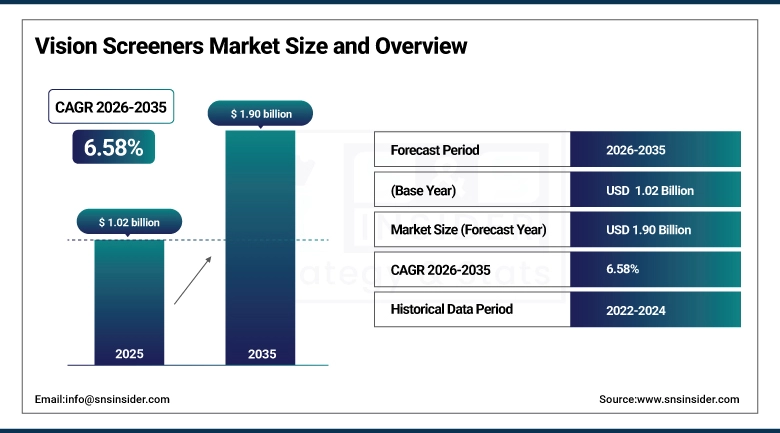

The Vision Screeners Market was valued at USD 1.02 Billion in 2025 and is expected to reach USD 1.90 Billion by 2035, growing at a CAGR of 6.58% from 2026–2035.

The Vision Screeners Market is witnessing strong growth driven by the rising global burden of uncorrected refractive errors, increasing prevalence of pediatric vision disorders such as myopia, and growing adoption of early-stage vision screening programs in schools and community healthcare systems. Technological advancements in automated autorefractors, handheld portable screening devices, AI-enabled diagnostic algorithms, and cloud-connected tele-ophthalmology platforms are significantly improving screening accuracy, speed, and accessibility across large populations.

Supporting this trend, the World Health Organization (WHO) has highlighted that at least 2.2 billion people globally suffer from vision impairment or blindness, with nearly half of these cases being preventable or untreated, reinforcing the urgent need for early detection through vision screening programs.

In parallel, regulatory and technological advancements are supporting market expansion. The U.S. Food and Drug Administration (FDA) has been actively clearing advanced digital ophthalmic devices, including AI-assisted diagnostic and screening tools, enabling faster adoption of automated vision screening systems in clinical and non-clinical settings.

Market Size and Forecast:

-

Market Size in 2025: USD 1.02 Billion

-

Market Size by 2035: USD 1.90 Billion

-

CAGR: 6.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vision Screeners Market - Request Free Sample Report

Vision Screeners Market Trends:

-

Rising prevalence of uncorrected refractive errors, myopia, and pediatric vision disorders is significantly increasing demand for early-stage vision screening across schools and primary care settings.

-

Expanding implementation of school-based and community vision screening programs is accelerating large-scale adoption of portable and handheld screening devices globally.

-

Rapid integration of AI-enabled diagnostic algorithms and automated refraction systems is enhancing screening accuracy, reducing dependency on specialist ophthalmologists, and improving workflow efficiency.

-

Increasing adoption of portable, handheld, and smartphone-enabled vision screening devices is improving accessibility in remote, rural, and low-resource healthcare environments.

-

Growing shift toward preventive eye health management and early detection initiatives is strengthening demand for routine mass vision screening across pediatric and geriatric populations.

-

Rising deployment of cloud-connected and tele-ophthalmology integrated screening systems is enabling real-time data sharing, remote diagnosis, and centralized vision health monitoring.

-

Expanding use of digital imaging, photoscreening, and autorefractor-based technologies is driving innovation in fast, non-invasive, and highly scalable vision assessment solutions.

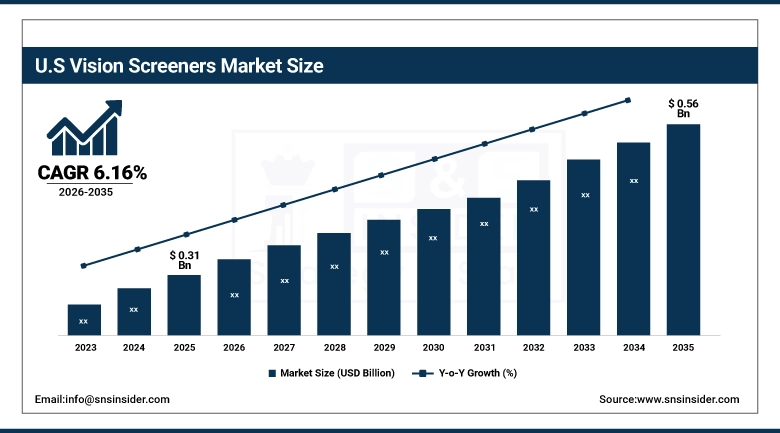

U.S. Vision Screeners Market was valued at USD 0.31 Billion in 2025 and is expected to reach around USD 0.56 Billion by 2035, growing at a CAGR of 6.16% from 2026–2035.

U.S. Vision Screeners Market is the world’s largest market due to highly developed pediatric and general healthcare screening services network, wide adoption of autorefractor and artificial intelligence screening equipment, and the presence of effective school vision screening programs in different states. Top med-tech companies like Topcon, Welch Allyn (Hillrom/Baxter), Carl Zeiss Meditec, and NIDEK are among the main leaders who develop innovations related to handheld and portable vision screening solutions.

Supporting this growth, the U.S. Centers for Disease Control and Prevention (CDC) reports that more than 9% of children aged 6–17 years have diagnosed vision disorders, reinforcing the need for early and routine screening in schools and pediatric care centers.

In addition, regulatory advancement by the U.S. Food and Drug Administration (FDA) has supported market expansion through clearances of AI-enabled diagnostic and ophthalmic screening systems, enabling faster adoption of automated vision screening technologies in both clinical and community healthcare environments, strengthening the U.S. position as a key innovation hub in preventive eye care.

Vision Screeners Market Segment Highlights:

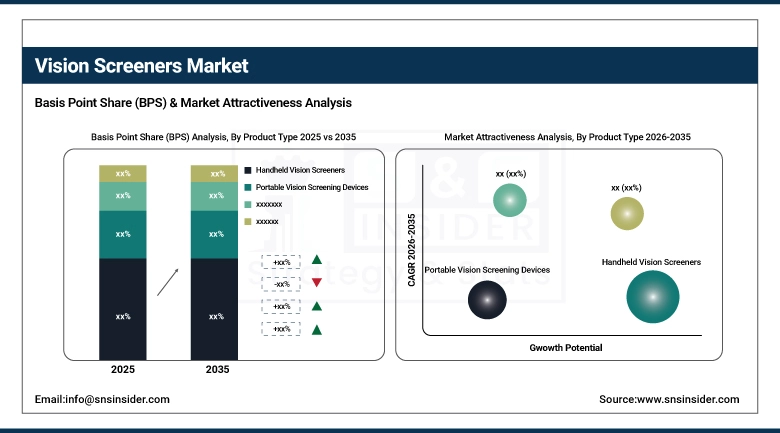

• By Product Type, Handheld Vision Screeners dominated the Vision Screeners Market with 26.36% share in 2025; Portable Vision Screening Devices is the fastest-growing segment CAGR

• By Technology Type, Autorefractor-based Screening dominated the Vision Screeners Market with 30.45% share in 2025; Digital / AI-based Vision Screening is the fastest-growing segment CAGR

• By End User, Hospitals & Eye Clinics dominated the Vision Screeners Market with 38.24% share in 2025; Schools & Educational Institutions is the fastest-growing segment CAGR

• By Application, Pediatric Vision Screening dominated the Vision Screeners Market with 32.51% share in 2025; Preventive Eye Health Check-ups is the fastest-growing segment CAGR

By Product, Handheld Vision Screeners segment dominates the Vision Screeners Market, Portable Vision Screening Devices segment expected to grow fastest

In 2025, the Handheld Vision Screeners segment maintained its dominant position in the Vision Screeners Market, accounting for 26.36% of total revenue. Such leadership is motivated by the extensive usage of this method in pediatrics screenings, vision tests conducted in schools, and even in family medicine practices because of its portable nature and relatively low cost.

From 2026 to 2035, the Portable Vision Screening Devices segment is projected to record the highest CAGR. Increased decentralization in healthcare, demand for portable screening units, and increased focus on community-based eye health campaigns are some factors accelerating its acceptance rate.

By Technology Type, Autorefractor-based Screening segment dominates the Vision Screeners Market, Digital / AI-based Vision Screening segment expected to grow fastest

The Autorefractor-based Screening segment held the largest share of 30.45% in 2025, driven by its established clinical acceptance, high diagnostic accuracy, and extensive deployment in routine eye examinations and pediatric screening programs. Its ability to deliver quick objective refraction results has made it a core technology across hospitals, optometry clinics, and school-based screening initiatives.

The Digital / AI-based Vision Screening segment is expected to register the highest CAGR during the 2026–2035 forecast period. The adoption of intelligent screening systems through software-based screening networks will be driven by the increasing demand for cost-effective and efficient vision screening systems that provide wide coverage. The integration of artificial intelligence in these systems enables high predictive precision, analysis, and connection to telemedicine infrastructure.

By End User, Hospitals & Eye Clinics segment dominates the Vision Screeners Market, Schools & Educational Institutions segment expected to grow fastest

The Hospitals & Eye Clinics segment maintained the highest end-user share of 38.24% in 2025. This dominance is made possible through adequate clinical facilities, well-trained eye specialists, and frequent use of modern visual screening equipment for both diagnosis and prevention purposes. Furthermore, hospitals act as referral centers for difficult ophthalmological tests, highlighting their critical position within visual screening processes.

The Schools & Educational Institutions segment is projected to achieve the highest growth rate during 2026–2035.

By Application, Pediatric Vision Screening segment dominates the Vision Screeners Market, Preventive Eye Health Check-ups segment expected to grow fastest

The Pediatric Vision Screening segment held the largest share of 32.51% in 2025, as a result of the rising trend in cases of visual disorders among children, including myopia, amblyopia, and un-diagnosed visual impairments. The importance of pediatric screening lies in the importance of detecting and treating visual disorders during their earliest stages, which have been highlighted by the widespread practice of screening at school level.

The Preventive Eye Health Check-ups segment is expected to record the highest CAGR during the 2026–2035 forecast period.

Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

35.43% |

|

Europe |

Germany |

25.14% |

|

Asia Pacific |

China |

20.75% |

|

Middle East & Africa |

UAE |

11.04% |

|

Latin America |

Brazil |

7.64% |

North America Vision Screeners Market Insights

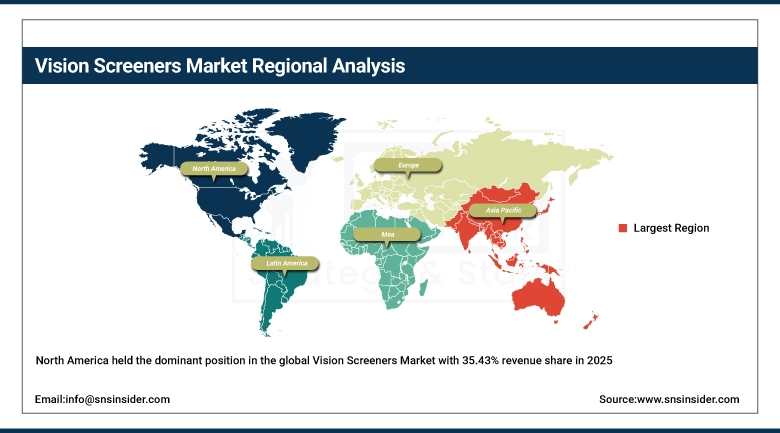

North America held the dominant position in the global Vision Screeners Market with 35.43% revenue share in 2025, This is due to the country’s well-developed infrastructure for pediatric ophthalmic care, high penetration rates of automated vision testing technologies, strong market presence of med-tech leaders, and high prevalence of school-based vision tests. The US is the regional leader, backed by the high penetration rate of handheld autorefractors, AI-based screening solutions, and mandatory pediatric vision testing procedures.

Supporting this dominance, the U.S. Centers for Disease Control and Prevention (CDC) emphasizes that vision disorders remain one of the most common childhood conditions, significantly reinforcing early screening initiatives in schools and pediatric clinics.

Additionally, the American Academy of Pediatrics (AAP) continues to recommend structured vision screening at multiple developmental stages, driving consistent demand for portable and automated screening devices across primary care settings.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Vision Screeners Market Insights

The Asia Pacific region will witness the highest growth rate of 7.77%, owing to the growing prevalence of myopia cases, increased awareness about eye health checks in schools, high spending on healthcare services, and government-driven eye care prevention activities. Countries such as China, India, Japan, South Korea, and Australia will dominate the market, with China holding strong market share around the region.

Supporting this growth, China’s National Health Commission (NHC) has prioritized child vision health under its national myopia prevention strategy, mandating regular school-based eye screening programs across urban and rural regions.

In Japan, the Ministry of Health, Labour and Welfare (MHLW) has expanded reimbursement support for digital ophthalmic diagnostics and preventive eye examinations, accelerating adoption of automated screening technologies in aging populations.

Europe Vision Screeners Market Insights

Europe accounted for of global revenue share in 2025,driven by strong public healthcare systems, well-established optometry networks, and widespread implementation of preventive vision screening programs in schools and community healthcare centers. Key markets such as Germany, the United Kingdom, France, and Italy continue to lead adoption due to structured national vision health programs and strong emphasis on early detection of pediatric refractive errors.

Supporting this position, the European Commission’s EU4Health Program has increased funding for preventive healthcare initiatives, including early diagnosis of vision disorders in children and aging populations.

Additionally, increasing integration of digital health technologies across European ophthalmology systems is strengthening adoption of AI-enabled screening platforms and portable diagnostic devices across both public and private healthcare providers.

Latin America, Middle East & Africa (LAMEA) Vision Screeners Market Insights

Vision Screeners Market is experiencing stable growth in Latin America and the Middle East & Africa region, driven by enhanced healthcare facilities, awareness about preventable visual impairment, and increased investment in eye care programs. Some of the countries showing strong growth in this region include Brazil, Mexico, Saudi Arabia, the United Arab Emirates (UAE), and South Africa.

Supporting this development, Brazil’s Ministry of Health (Ministério da Saúde) has expanded national child vision screening initiatives under its primary healthcare programs, improving early detection of refractive errors in underserved populations.

In the Middle East, Saudi Arabia’s Ministry of Health Vision 2030 healthcare transformation program is actively investing in digital healthcare expansion, including preventive ophthalmic screening services and deployment of portable diagnostic devices across primary care centers.

Vision Screeners Market Growth Drivers:

-

Rising prevalence of childhood vision disorders and strong global shift toward early detection and preventive eye care is driving rapid adoption of vision screening technologies worldwide

The strongest force that propels the Vision Screeners Market forward is the rising number of uncorrected refractive errors worldwide, with myopia being the most common type that poses a serious public health issue. There is growing emphasis on detecting such vision-related problems early on to avoid permanent visual impairment, poor academic results among children, and low productivity levels among adults. As a result, the need for efficient vision testing technologies, which do not depend on ophthalmologists' availability, is growing rapidly.

Supporting this growth, the World Health Organization (WHO) estimates that at least 2.2 billion people globally have vision impairment or blindness, with nearly 1 billion cases being preventable or untreated, highlighting a significant unmet need for early screening and intervention.

Additionally, the American Academy of Pediatrics (AAP) continues to recommend routine vision screening at multiple childhood developmental stages, reinforcing structured screening adoption across primary care and educational systems in the United States and influencing global best practices.

Vision Screeners Market Restraints:

-

High upfront cost of advanced vision screening systems and limited affordability in small clinics and public health programs is restraining large-scale adoption of vision screening technologies

The major obstacle that impedes the growth of the Vision Screeners Market is the considerable capital that has to be invested in order to purchase sophisticated diagnostic tools like autorefractor-based vision screeners, AI-driven vision screening devices, and ophthalmic instruments. Though highly accurate and scalable, the cost involved in buying, licensing, calibration, and maintenance of such technology may be prohibitively expensive for small clinics, individual optometry centers, and community health care facilities in developing countries.

Vision Screeners Market Opportunities:

-

Rapid expansion of school-based vision screening programs and integration of AI-enabled portable diagnostic tools is unlocking large-scale preventive eye care opportunities across pediatric populations globally

The most important growth area for the Vision Screeners Market is associated with the growing trend across the world toward systematic and comprehensive preventive programs of vision screening, especially in educational establishments, clinics, and other medical centers. Increasing emphasis on early identification of refractive error and amblyopia in children creates a stable demand base for vision screeners that are easy to deploy and process many subjects. This trend helps vision screener manufacturers diversify into new areas beyond clinical settings.

Recent Developments:

-

2026: Topcon Corporation advanced its global rollout of next-generation AI-assisted handheld vision screening systems, expanding deployments across school screening programs in Asia-Pacific and North America. The company strengthened integration of cloud-based screening data platforms, enabling real-time remote monitoring of pediatric vision health outcomes across multi-location screening networks.

-

2026: Carl Zeiss Meditec AG expanded its digital ophthalmic screening ecosystem, enhancing portable vision screening solutions with AI-driven refractive error detection and automated risk classification tools. The company also increased adoption of its connected screening platforms across primary care and optometry chains in Europe and the U.S., supporting large-scale preventive eye health programs.

-

2025: Welch Allyn (Hillrom/Baxter) strengthened its dominance in primary care and school-based vision screening through expanded deployment of portable autorefractor devices across pediatric and community health programs in North America. The company also enhanced device interoperability with electronic health record (EHR) systems, improving screening workflow efficiency and referral accuracy in large healthcare networks.

-

2025: Plusoptix GmbH expanded its global footprint in pediatric vision screening devices, particularly in Europe and emerging markets, by introducing upgraded handheld photoscreeners with faster screening cycles and improved accuracy for amblyopia and refractive error detection. The company also increased collaborations with school health initiatives and pediatric ophthalmology programs, strengthening early diagnosis adoption rates.

Vision Screeners Market Key Players:

-

Hill-Rom Holdings (Welch Allyn)

-

NIDEK Co., Ltd.

-

Honeywell International Inc.

-

Essilor Instruments (EssilorLuxottica)

-

Plusoptix GmbH

-

Adaptica S.r.l.

-

Depisteo

-

Reichert Technologies (AMETEK)

-

OCULUS Optikgeräte GmbH

-

Visionix (Luneau Technology)

-

Huvitz Co., Ltd.

-

Keeler Ltd.

-

Stereo Optical Company Inc.

-

Medizs Inc.

-

Smart Vision Labs

-

Kowa Company Ltd.

-

Haag-Streit AG

Vision Screeners Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.02 Billion |

| Market Size by 2035 | USD 1.90 Billion |

| CAGR | CAGR of 6.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Handheld Vision Screeners, Table-top / Desktop Vision Screeners, Portable Vision Screening Devices, Spot Vision Screeners (Autorefractor-based), Software-based / AI-enabled Screening Systems, Others) • By Technology Type (Autorefractor-based Screening, Photoscreening Technology, Wavefront Aberrometry, Digital / AI-based Vision Screening, Retinal Imaging-based Screening, Others) • By End User (Hospitals & Eye Clinics, Schools & Educational Institutions, Pediatric Care Centers, Optical Retail Chains, Community Health Programs / NGOs, Others) • By Application (Pediatric Vision Screening, Adult Vision Screening, Occupational Vision Testing, Geriatric Eye Screening, Preventive Eye Health Check-ups, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Topcon Corporation, Hill-Rom Holdings (Welch Allyn), Carl Zeiss Meditec AG, NIDEK Co., Ltd., Canon Medical Systems Corporation, Honeywell International Inc., Essilor Instruments (EssilorLuxottica), Plusoptix GmbH, Adaptica S.r.l., Depisteo, Reichert Technologies (AMETEK), OCULUS Optikgeräte GmbH, Visionix (Luneau Technology), Huvitz Co., Ltd., Keeler Ltd., Stereo Optical Company Inc., Medizs Inc., Smart Vision Labs, Kowa Company Ltd., Haag-Streit AG |

Frequently Asked Questions

North America dominated the Vision Screeners Market in 2025.

The Handheld Vision Screeners segment dominated the Vision Screeners Market in 2025.

Rising prevalence of pediatric vision disorders, increasing global myopia burden, and growing emphasis on early detection through school-based and preventive eye screening programs is the primary growth driver of the Vision Screeners Market.

The Vision Screeners Market was valued at USD 1.02 billion in 2025.

The Vision Screeners Market is expected to grow at a CAGR of 6.58% from 2026 to 2035.

Get in Touch