Military Protective Eyewear Market Report Scope & Overview:

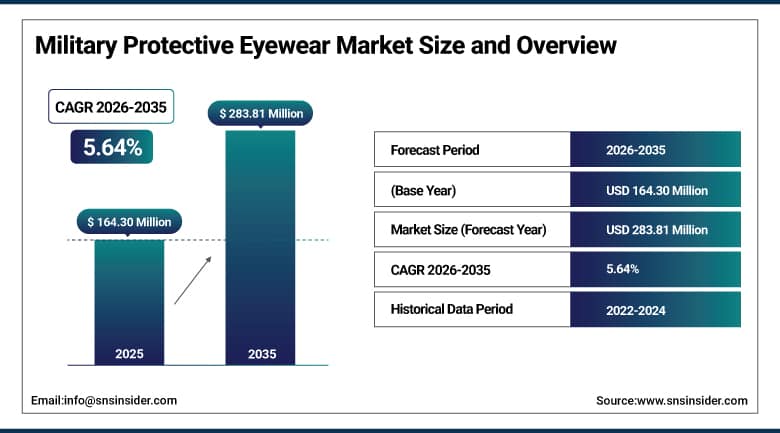

The Military Protective Eyewear Market was valued at USD 164.30 Million in 2025 and is expected to reach USD 283.81 Million by 2035, growing at a CAGR of 5.64% from 2026–2035.

The military protective eyewear market is experiencing consistent growth owing to increased adoption of innovative soldier protection gears as well as ballistic protection solutions among armies, navies, air forces, specialforces, and homeland security departments. Rising modernization of defense forces coupled with high demand for improved battlefield protection is supporting this trend. Moreover, growing adoption of advanced technology like ballistic resistant lenses, laser resistant coating technology, anti-fogging and anti-scratching lens technologies, ultraviolet protection technology, and photochromic lens material is propelling the market growth. The growth is being further driven by the rising adoption of lightweight polycarbonate-based smart eyewear systems. Modernization of warfare, border security, and field tactics operations is also driving demand in the market.

The governmental regulations related to defense equipment standards, soldier safety protocols, ballistic protection requirements, and military procurement frameworks such as NATO defense equipment standards, the U.S. Department of Defense (DoD) soldier protection guidelines, European Defence Agency (EDA) safety protocols, ISO ballistic and optical safety standards, and MIL-PRF (Military Performance Specification) eyewear certification requirements are significantly influencing military protective eyewear design, manufacturing, and deployment. In addition, the U.S. Army modernization programs, India’s defense capability enhancement initiatives, China’s military equipment modernization strategies, and European Union defense cooperation frameworks are further accelerating market adoption.

Market Size and Forecast

- Market Size 2026E: USD 173.24 Million

- Market Size 2035: USD 283.81 Million

- CAGR (2026 - 2035): 5.64%

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Military Protective Eyewear Market - Request Free Sample Report

Military Protective Eyewear Market Trends

- Growing defense modernization programs and soldier safety initiatives are accelerating procurement of advanced military-grade protective eyewear globally.

- Integration of protective eyewear with helmets, night vision devices, and AR-based systems is improving situational awareness in modern warfare.

- Expansion of lightweight polycarbonate and composite lens materials is enhancing durability, comfort, and long-duration wearability for soldiers.

- Rising deployment of laser protective eyewear is driven by expanding use of directed energy systems and advanced military targeting technologies.

- Increasing integration of anti-fog, anti-scratch, and UV protection coatings is improving visibility and operational performance in extreme battlefield environments.

- Growing adoption of advanced ballistic and laser protective eyewear is increasing demand across modern military combat and tactical operations worldwide.

Military Protective Eyewear Market Size Outlook

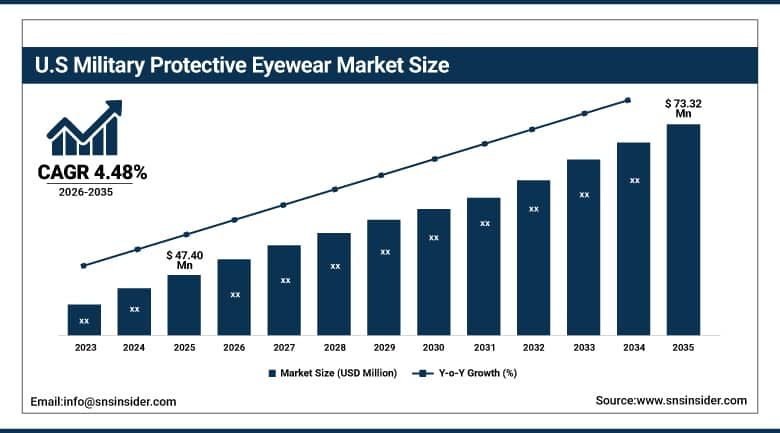

The U.S. Military Protective Eyewear Market in the United States was valued at USD 47.40 million in 2025 and is expected to reach around USD 73.32 million by 2035, growing at a CAGR of 4.48% from 2026–2035.

The U.S. military protective eyewear market is highly advanced and strongly driven by extensive defense modernization programs and large-scale procurement by the U.S. Department of Defense. Growth is supported by increasing demand from the U.S. Army, Navy, Air Force, Marine Corps, and Special Operations Forces for ballistic safety glasses, tactical goggles, laser protective eyewear, and integrated helmet-compatible systems. Rising focus on soldier survivability, mission effectiveness, and eye injury prevention is further accelerating adoption across combat and training operations. Major companies such as 3M, Honeywell International, Oakley Standard Issue, Revision Military, ESS Eyewear, Gentex Corporation, and Wiley X are strengthening their defense-grade product portfolios in the U.S. market.

The U.S. government initiatives such as soldier safety programs offered by the U.S. Department of Defense (DoD), MIL-PRF optical standards for eyewear, OSHA safety guidelines at training facilities, and NDAA budgetary provisions are playing a major role in driving product innovation and procurement. Other key drivers include rising defense budgets, advancements in soldier technology, and developments in optical protection technology.

Military Protective Eyewear Market Segment Analysis

-

By Device, ballistic safety glasses dominated the military protective eyewear market with a 32.40% share in 2025, while integrated helmet mounted displays is the fastest-growing segment.

-

By Technology, ballistic impact protection technology dominated the military protective eyewear market with a 34.80% share in 2025, while photochromic lens technology is the fastest-growing segment.

-

By Application, combat operations dominated the military protective eyewear market with a 36.50% share in 2025, while special forces operations is the fastest-growing segment.

-

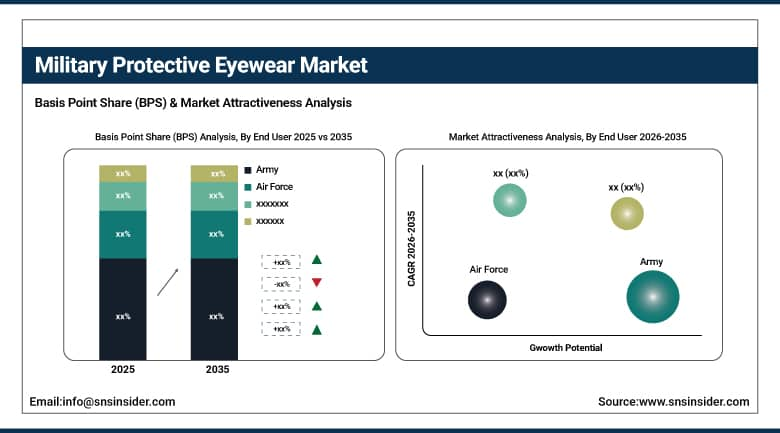

By End User, the army dominated the military protective eyewear market with a 38.60% share in 2025, while special operations forces is the fastest-growing segment.

By End User, the Army dominated the military protective eyewear market, while special operations forces is the fastest growing segment.

Army segment holds the dominant market position in the Military Protective Eyewear Market, owing to the significant deployment of troops and procurement of protective gear on a continuous basis by infantrymen and combatants. Growing exposure to battlefields, modernization initiatives, and safety concerns among soldiers boost the demand for military protective eyewear products. The growing adoption of ballistic safety glasses and tactical goggles is the main reason behind the strong performance of the segment in the global market.

Special operations forces segment is anticipated to be the fastest-growing CAGR of the market during the forecast period between 2026 and 2035. This is attributed to the increasing demand for highly effective, lightweight, and technologically-advanced protective eyewear in special operations forces. Asymmetric warfare, counter-terrorism missions, and covert missions have raised the need for high-quality optical protection systems. Laser protection capability and integration with helmets boost its adoption rapidly.

By Device, ballistic safety glasses dominated the military protective eyewear market, while integrated helmet mounted displays is the fastest growing segment.

Ballistic safety glasses segment held the top position in terms of the dominated revenue share in the military protective eyewear market in 2025. This segment enjoys dominance owing to its extensive use in every military force in providing basic eye protection. They are cost-effective, highly durable, and conform to military standards of safety. Moreover, due to their lightweight structure, easy deployment and compatibility with other headgear, they are dominating this segment.

Integrated helmet mounted Displays segment will register the fastest CAGR during 2026-2035. Factors such as rising investments in next-generation technologies, rising adoption of advanced soldier systems with vision, communication, and targeting systems, enhanced situational awareness and real-time battlefield data availability have been fueling their adoption. Furthermore, increasing modernization initiatives in the defense sector, rise in demand for network-centric warfare along with augmented reality technology integration has been contributing to the fast-paced growth of this segment.

By Technology, ballistic impact protection technology dominated the military protective eyewear market, while photochromic lens technology is the fastest growing segment.

Ballistic impact protection technology segment captured the dominated market share in terms of revenue in the military protective eyewear market in 2025. The reason behind this trend can be attributed to growing demand for high-end products that protect the soldiers from shrapnel and debris and any high-speed impacts while operating in the combat zones. Furthermore, rising military protection standards and increasing modernization of the military have also been contributing to growing sales.

Photochromic lens technology segment will register a fastest CAGR from 2026 - 2035 owing to rising demand for advanced photochromic lenses technology among the defense organizations. This technology helps soldiers to see clearly by adapting the tint of the lens depending upon the environmental surroundings. Rising deployment of photochromic lenses in the battlefields where various terrains such as deserts and snowy areas are being used for military training is driving the rapid adoption.

By Application, combat operations dominated the military protective eyewear market, while special forces operations is the fastest growing segment.

Combat operations segment emerged as the dominated leader in the Military Protective Eyewear Market, accounting for the largest share of revenue in 2025. The reason behind such dominance is the deployment of troops in various combat zones that require constant eye protection. The increased risk on the battlefield, presence of shrapnel, and harsh environment are driving the demand. The standardization of protective equipment among infantry and massive procurements by military organizations are boosting market adoption.

Special forces operations segment is likely to witness the fastest CAGR during 2026-2035. The growing expenditure towards elite military units that have mission-specific requirements for eyewear is expected to fuel market growth. Light-weight, high-performance, and integrated systems boost the compatibility with night vision devices. The expanding scope of anti-terrorism missions and covert operations has been boosting the demand for cutting-edge protective eyewear products.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.40% |

|

Europe |

Germany |

21.90% |

|

Asia Pacific |

China |

28.10% |

|

Middle East & Africa |

UAE |

6.40% |

|

Latin America |

Brazil |

6.80% |

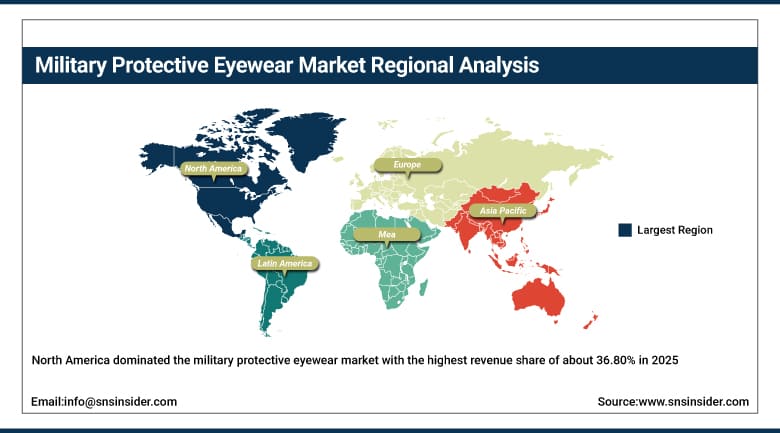

North America Military Protective Eyewear Market Insights

North America dominated the military protective eyewear market with the highest revenue share of about 36.80% in 2025 due to strong defense spending, advanced soldier protection programs, and large-scale procurement by the United States Department of Defense and allied defense agencies. The region shows high adoption of ballistic safety glasses, tactical goggles, laser protective eyewear, and integrated helmet-compatible systems across combat and training operations. Strong presence of key players such as 3M, Honeywell International, Revision Military, ESS Eyewear, Oakley Standard Issue, Gentex Corporation, and Wiley X further strengthens market growth.

Strict military safety standards such as MIL-PRF eyewear specifications, the U.S. Department of Defense procurement guidelines, OSHA safety compliance for training environments, and NATO interoperability standards are significantly influencing product development and adoption. Consequently, rising focus on soldier survivability, battlefield vision protection, and modernization of personal protection systems has supported sustained market growth in the Military Protective Eyewear Market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Military Protective Eyewear Market Insights

The European region is considered to be one of the most important regions of the military protective eyewear market due to high defense modernization initiatives along with an emphasis on enhancing safety measures and overall operational efficiency. Advanced military protective eyewear products are being increasingly procured by countries such as Germany, France, United Kingdom, Italy, and Spain. Growing demand is being witnessed for laser protective eyewear, anti-fog ballistic glasses, and tactical goggles among others for military and training purposes. Regulations like European Defence Agency (EDA), NATO defence equipment compatibility, ISO optical safety standards, and EU defense procurement regulations are encouraging the use of advanced military protective eyewear products.

Asia Pacific Military Protective Eyewear Market Insights

Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2035 due to rapid military modernization, rising defense budgets, and expanding armed forces across the region. Increasing focus on border security, counter-terrorism operations, and tactical mission readiness is driving strong demand for advanced protective eyewear systems. Growing adoption of ballistic safety glasses and integrated soldier protection equipment is further accelerating market expansion. Government initiatives supporting defense manufacturing, modernization programs, and self-reliance in military equipment are significantly boosting domestic production and procurement. Rising geopolitical tensions, increasing military training activities, and low penetration of advanced protective eyewear systems are further contributing to strong regional growth.

Middle East & Africa and Latin America Military Protective Eyewear Market Insights

Middle East & Africa and Latin America regions is expected to show stable growth owing to the growing trend of defense modernization, improvement in border security, and rise in counterterrorism activities. Several nations including UAE, Saudi Arabia, South Africa, Brazil, and Mexico are now showing greater interest in the installation of advanced military eyewear protection technology for armed forces and special units. Increasing expenditure on military infrastructure, expanding defense purchasing programs, and growing emphasis on soldier safety are among some of the major factors influencing the growth of the market in both regions.

Market Dynamics:

Growth Drivers: Rising Defense Modernization and Soldier Protection Equipment Demand Across Global Armed Forces

Growing defense modernization initiatives around the world are increasingly becoming a key determinant of demand for military eye protection devices. National governments are making serious investments towards improved survivability and effectiveness among their soldiers by means of new protective gear. Growing political tensions and border disputes between nations have been fueling acquisition of ballistic safety glasses, tactical goggles, and laser protection glasses. The use of enhanced technologies like polycarbonate lens technology and anti-fog coatings improves operational efficiency. Regular training exercises of soldiers in various branches of the military are contributing to market growth.

Restraints: Product Standardization Challenges and Strict Military Certification Requirements

Military compliance standards that are highly rigorous along with a complicated approval process involved make up formidable barriers for companies dealing with manufacturing of protective eyewear. Complying with MIL-PRF, NATO or defense agency standards necessitates rigorous testing processes which consequently extend the time and expense incurred for product development. The lack of global standardized standards results in disjointed approval and procurement processes across various countries and defense agencies. Safety testing criteria for ballistics protection, optics or durability further slows down the approval process due to stringent safety requirements. Such issues hinder rapid market commercialization of cutting-edge eyewear technology.

Opportunities: Integration of Smart and AR-Based Protective Eyewear Systems in Defense Applications

Advances in smart eyewear with built-in augmented reality and heads up display technology is creating many possibilities in the field of defense. Such technology increases situational awareness through data visualization in real time. The investments made in modernization of soldiers are helping the use of eyewear systems that can be used with night vision goggles and provide assistance in aiming. Growing demand for multi-purpose wearable technology is leading to innovations in light-weight eyewear with augmented reality capabilities. Future soldier systems have been under investigation by defense organizations, thereby creating great opportunities for manufacturers.

Recent Developments

- 2026: Honeywell International enhanced its military protective eyewear with improved ballistic and laser protection technologies for modern combat environments. The development focuses on better soldier safety, optical clarity, and mission performance in extreme battlefield conditions.

- 2025: Oakley Standard Issue expanded its military eyewear range with upgraded ballistic-rated and helmet-compatible designs for armed forces. The development emphasizes improved field vision, night operation compatibility, and enhanced soldier comfort.

- 2024: Revision Military introduced advanced tactical eyewear for special operations forces with improved modular compatibility and helmet integration. The innovation focuses on better durability, lightweight design, and superior optical performance in mission environments.

- 2024: ESS Eyewear strengthened its defense eyewear portfolio with advanced anti-fog and ballistic protection goggles for military use. The enhancement focuses on improved visibility, environmental adaptability, and combat readiness.

Military Protective Eyewear Market Key Players are:

- 3M

- Oakley Standard Issue

- Revision Military

- ESS Eyewear

- Wiley X

- Smith Optics

- Honeywell International

- Bolle Safety

- MCR Safety

- Gentex Corporation

- Thales Group

- BAE Systems

- Elbit Systems

- Safariland Group

- Avon Protection

- POC Sports

- Pilla Performance Eyewear

- Uvex Safety Group

- Armorsource

- Survitec Group

Military Protective Eyewear Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 163.30 Million |

| Market Size by 2035 | USD 283.81 Million |

| CAGR | CAGR of 5.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | * By Device (Ballistic Safety Glasses, Tactical Goggles, Laser Protective Eyewear, Integrated Helmet Mounted Displays, Protective Visors) * By Technology (Ballistic Impact Protection Technology, Laser Protection Technology, Anti-Fog Coating Technology, UV Protection Technology, Photochromic Lens Technology) * By Application (Combat Operations, Training & Simulation, Surveillance & Reconnaissance, Special Forces Operations, Border Security Operations) * By End User (Army, Navy, Air Force, Special Operations Forces, Homeland Security Agencies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M, Oakley Standard Issue, Revision Military, ESS Eyewear, Wiley X, Smith Optics, Honeywell International, Bolle Safety, MCR Safety, Gentex Corporation, Thales Group, BAE Systems, Elbit Systems, Safariland Group, Avon Protection, POC Sports, Pilla Performance Eyewear, Uvex Safety Group, Armorsource, Survitec Group |

Frequently Asked Questions

The military protective eyewear market is expected to grow at a CAGR of 5.64% from 2026 to 2035.

The military protective eyewear market was valued at USD 164.30 Million in 2025.

Rising defense modernization programs and increasing demand for soldier safety equipment are driving the market. Adoption of ballistic protection, laser resistance, and advanced optical technologies supports market growth.

The Army segment dominated the military protective eyewear market in 2025.

North America dominated the military protective eyewear market in 2025.

Get in Touch