Spacecraft Market Report Scope & Overview:

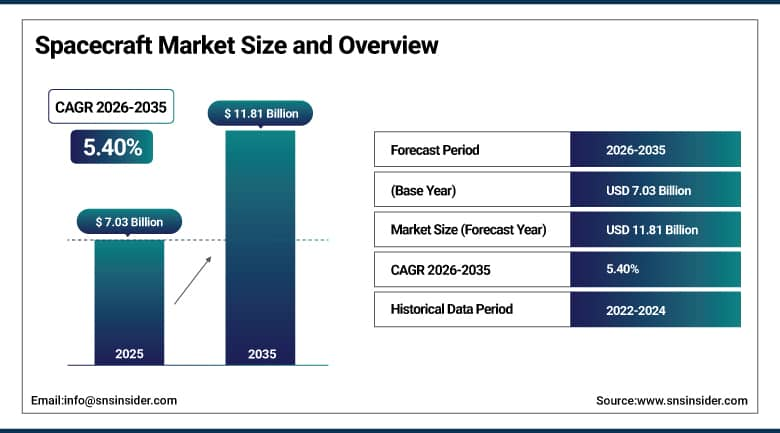

The Spacecraft market was valued at USD 7.03 billion in 2025 and is expected to reach USD 11.81 billion by 2035, growing at a CAGR of 5.40% from 2026–2035.

The spacecraft market is experiencing significant growth due to increasing commercial space operations, growing investments in satellites, increasing number of space exploration missions undertaken by governments, and rapid technology evolution within the entire space industry chain. Various space agencies and companies are focusing on spacecraft development efforts in order to facilitate communications, earth observation, deep space explorations, defense surveillance, and orbital infrastructure projects. The rise in use of reusable spacecraft, small spacecraft systems, autonomous navigation, artificial intelligence mission systems, and advanced propulsion system technologies will continue to shape the competitive environment.

SpaceX extended spacecraft manufacturing and space services in March 2026 via deployment missions that assisted in the realization of future satellite constellations and deep space travel goals. Innovations within the industry had a trend towards mission architectures involving reusability, automated docking, and spacecraft manufacturing techniques which aimed at cutting down mission expenses.

Market Size and Forecast:

-

Market Size 2026E: USD 7.36 Billion

-

Market Size 2035: USD 11.81 Billion

-

CAGR (2026 - 2035): 5.40%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Spacecraft Market - Request Free Sample Report

Spacecraft Market Trends:

-

Rising deployment of large-scale satellite constellations is accelerating demand for next-generation spacecraft platforms and orbital infrastructure.

-

Increasing commercialization of space activities is driving investments in privately developed spacecraft and orbital mission systems.

-

Rapid adoption of reusable spacecraft technologies is improving mission cost efficiency and long-term deployment economics.

-

Growing integration of AI-enabled autonomous navigation and onboard decision-making systems is enhancing mission reliability and operational performance.

-

Increasing investments in deep-space exploration programs and lunar mission initiatives are driving advanced spacecraft development globally.

The US Spacecraft Market Size Outlook:

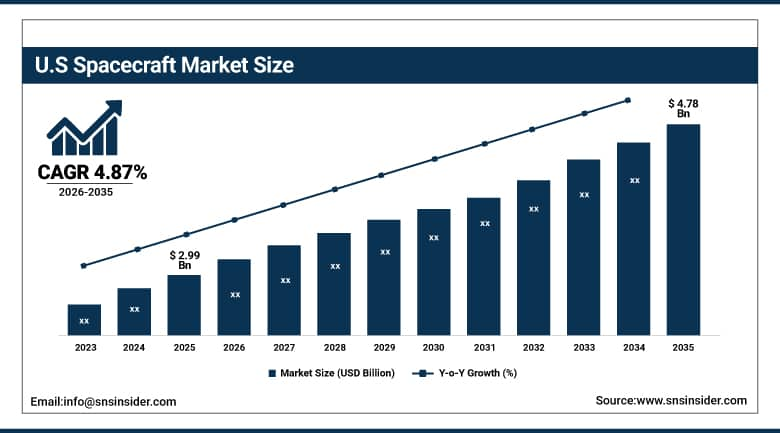

The U.S. Spacecraft market was valued at USD 2.99 billion in 2025 and is expected to reach around USD 4.78 billion by 2035, growing at a CAGR of 4.87% from 2026–2035.

The United States leads the world spacecraft market on account of its strength in innovations related to space technology, manufacture of spacecraft, and the involvement of major companies such as SpaceX, Lockheed Martin, Northrop Grumman, and Boeing Space. The strong backing of the American government, which is involved in national space programs, defense upgradation, and investments in moon landing and deep space missions as well as orbiting systems, ensures continuous growth in dominance by the country in the world spacecraft market.

In 2025, NASA and commercial partners expanded lunar mission and orbital infrastructure initiatives supporting long-duration human spaceflight systems and next-generation spacecraft development programs. In parallel, multiple private aerospace companies accelerated investments in reusable spacecraft platforms, autonomous docking technologies, and commercial orbital habitat systems to support the rapidly expanding space economy.

Spacecraft Market Segment Analysis:

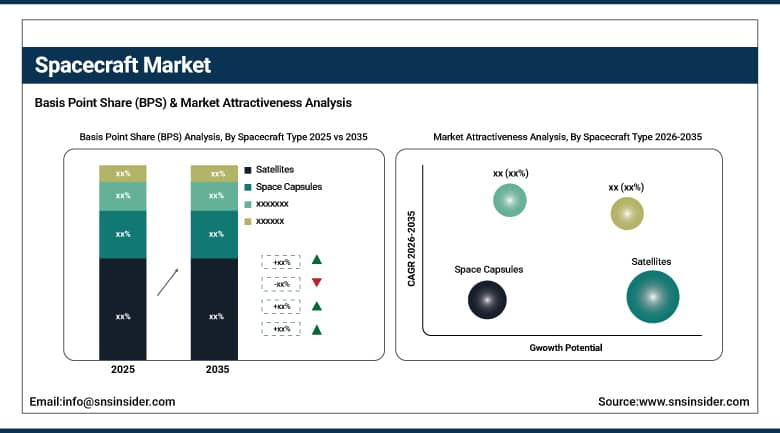

• By Spacecraft Type, satellites dominated the spacecraft market with 54.87% share in 2025; space stations / habitats recorded the fastest growth CAGR.

• By Application, communication dominated the spacecraft market with 31.29% share in 2025; space tourism is the fastest-growing segment CAGR.

• By Orbit Type, low earth orbit (LEO) dominated the spacecraft market with 46.54% share in 2025; sun-synchronous orbit (SSO) is the fastest-growing segment CAGR.

• By Subsystem, propulsion systems dominated the spacecraft market with 22.51% share in 2025; payload systems recorded the fastest growth CAGR.

• By End User, government & space agencies dominated the spacecraft market with 39.56% share in 2025; space tourism operators are the fastest-growing segment CAGR.

By Spacecraft Type, satellites dominates the spacecraft market, while space stations / habitats is the fastest-growing segment.

Satellites segment dominated the spacecraft market with the highest revenue share of about 54.87% in 2025 due to the increasing use of communication, Earth observation, navigation, and surveillance satellites around the world. Increased deployment of low-Earth orbit satellite constellations, the demand for increased broadband capability, an increase in intelligence applications from space, and investments by both government and private space companies have increased the global demand for satellite spacecraft platforms.

Space Stations / Habitats segment is estimated to have the highest CAGR during the period of 2026–2035. As a result of increased investments in commercial orbital stations, long-term human space flight missions, and future orbital infrastructure development projects. The growing emphasis on lunar flights, orbital facilities, and space habitation ventures has been fuelling demand.

By Application, communication dominates the spacecraft market, while space tourism is the fastest-growing segment.

Communication segment dominated the spacecraft market with the highest revenue share of about 31.29% in 2025 as a result of the growing demand for satellite-based broadband connections, telecommunications and broadcasting services. The increased use of satellites capable of transmitting vast amounts of data, along with the deployment of constellations in space, has been a major contributor to the growing activities of sending satellites into orbit around our planet.

Space Tourism segment is projected to register the fastest CAGR during the forecast period 2026–2035 due to higher commercial investments for suborbital and orbital flights. More engagement from private aerospace companies, heightened demand by consumers, and technological developments in reusable space crafts have been driving the growth of the sector. The future potential in the industry is huge in the context of further progress towards commercial space stations and flights.

By Orbit Type, low earth orbit (LEO) dominates the spacecraft market, while sun-synchronous orbit (SSO) is the fastest-growing segment.

Low Earth Orbit (LEO) segment dominated the spacecraft market with the highest revenue share of about 46.54% in 2025 due to the growing use of satellites for providing broadband communications, earth observations, defense surveillance, and low latency communications networks. Reduced launch costs, less signal delay, and suitability for small satellite systems have made their use more widespread. Investment in advanced communication networks and earth observation systems keeps fuelling the market for spacecrafts in LEO orbits.

Sun-Synchronous Orbit (SSO) segment is projected to experience the fastest CAGR during the forecast period of 2026–2035 as a result of increasing need for reliable imaging conditions in earth observation and remote sensing missions. Increasing application in environmental monitoring, climate evaluation, precision farming, and intelligence activities are some factors fuelling segment growth

By End User, government & space agencies dominate the spacecraft market, while space tourism operators are the fastest-growing segment.

Government & Space Agencies segment occupied the dominated share of the spacecraft market with 39.56% revenue share in 2025 due to enhanced spending on national space programs, missions for planetary explorations, defense monitoring systems, and satellites. Ongoing investments for lunar exploration programs, research programs, space flights, and national security projects have resulted in an increase in procurement of advanced spacecrafts.

Space Tourism Operators segment is likely to expand at the fastest CAGR during 2026–2035. These are attributed to the increasing commercialization of space flight operations and investments made in orbital tourism services across the globe. Private aerospace companies’ greater involvement, advancements in spacecraft design, and higher consumer demands for luxury travel experiences are some of the major factors that are contributing to growth.

By Subsystem, propulsion systems dominates the spacecraft market, while payload systems is the fastest-growing segment.

Propulsion Systems segment held the dominated revenue share of around 22.51% in 2025 because of the increasing need for higher manoeuvrability of spacecraft, transfer from one orbit to another, higher mission duration, and efficient fuels used by the spacecraft. The use of new propulsion systems like electric propulsion, advanced thrusters, and other propulsion technologies has increased demand in the market.

Payload Systems segment is anticipated to be growing at the fastest CAGR from 2026 to 2035. This is because of the growing need for high performance imaging, communication, science, and other mission-specific payloads. There are many good opportunities in the areas of earth observation satellites, intelligence satellites, and advanced research.

Spacecraft Market Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

89.54% |

|

Europe |

Germany |

25.96% |

|

Asia Pacific |

China |

42.69% |

|

Middle East & Africa |

UAE |

23.36% |

|

Latin America |

Brazil |

39.41% |

North America Spacecraft Market Insights

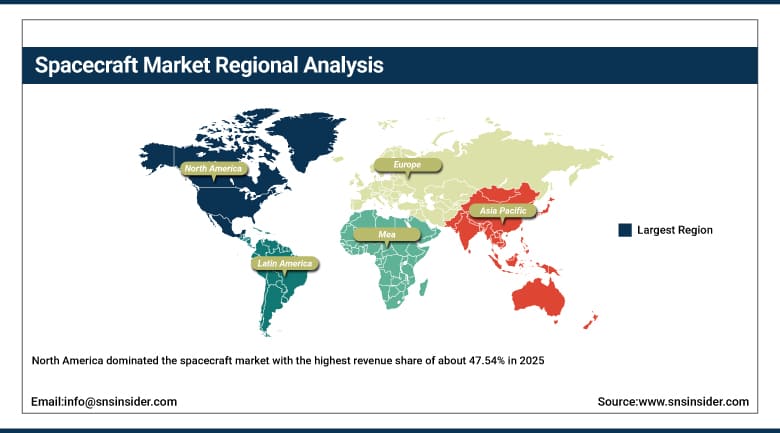

North America dominated the spacecraft market with the highest revenue share of about 47.54% in 2025 because of robust investment in commercial spacecraft programs, superior spacecraft manufacturing facilities, and extensive government backing in both the United States and Canada. Increased launches of communication satellites, defense spacecraft systems, manned spacecraft operations, and orbital systems projects contributed towards an increasing demand for the latest generation of spacecraft technology. The increasing involvement of aerospace companies in this industry, as well as continued investments in space exploration and space security efforts, has played a role in dominating the regional market.

As a result, more investments are being made in NASA explorations projects, thus resulting in spacecraft innovations and launches becoming faster. In the year 2025, space companies invested more money in orbital infrastructure systems and future lunar missions in order to ensure dominance of North America in the entire space industry around the world.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Spacecraft Market Insights

Europe is recognized as one of the most critical regions in the global spacecraft market due to the significant investments made in earth observation, space research, and next-generation space orbital projects. Nations like Germany, the United Kingdom, France, and Italy are still driving growth in the market via satellite manufacturing, space sustainability technologies, and exploration missions. The focus on developing advanced spacecraft, monitoring capabilities for the environment, and strategic space autonomy further drives the growth of the market in the region. As one of the supportive factors, collaborative space transportation and lunar mission initiatives in Europe have helped speed up spacecraft development.

Asia Pacific Spacecraft Market Insights

Asia Pacific segment is expected to grow at the fastest CAGR of about 6.59% from 2026–2035 due to the fast-growing space activities by nations, the increasing launches of spacecrafts, and growing investments in China, India, Japan, and Southeast Asia countries. The growing emphasis on communication satellites, deep space missions, defense surveillance systems, and launch services is expected to drive spacecraft demand in the region. Government support in space activities, increased use of satellite systems, and rising private sector investment are other factors fuelling market growth in the region during the forecast period. Underpinning the growth, China will continue its efforts in lunar exploration and orbital system deployment programs whereas India will ramp up its satellite programs and deep space capabilities.

Middle East & Africa and Latin America Spacecraft Market Insights

The Middle East & Africa (MEA) and Latin America regions are seeing continuous growth in the spacecraft market as a result of increased investment in national space programs, satellite launch programs, and aerospace infrastructure developments. Within the MEA region, the UAE, Saudi Arabia, and South Africa are taking the lead by way of increased investment in satellite technology, smart infrastructure, and space research. As for the Latin American region, Brazil and Mexico are leading market growth as a result of their satellite communication systems and aerospace development. In support of the trend, it can be seen that investments in space technology continue to grow within the MEA region because of the initiatives of UAE and Saudi Arabia.

Market Dynamics:

Growth Drivers: Rising commercialization of space activities and increasing investments in satellite constellations are accelerating spacecraft demand globally

Rising demand for sophisticated communication network systems, earth observation satellites, deep space missions, and space-based surveillance technology has led to increased usage of spacecraft technology all over the world. Governmental organizations and aerospace companies have become more interested in deploying state-of-the-art spacecraft to serve their navigation needs, orbital activities, research, and space ventures. Deployment of mega-constellation satellites, reusable spacecraft technology, and self-sufficient space technology will continue to boost market growth in the coming years. Growing partnerships between the private and governmental sector, increasing spacecraft production, and exploration of the Moon and other planets will also boost market demand.

Restraints: High spacecraft development costs and complex mission risks continue limiting broader market expansion globally

The high costs involved with the construction of the spacecraft and launching them have been cited as major challenges for the industry. Construction of spacecraft is an undertaking that requires thorough testing and sophisticated engineering capabilities, which in turn necessitate large amounts of investment in terms of money for the public and private sectors. The failure of a mission or even a problem encountered in the orbit can lead to serious consequences. Besides, the challenges of regulation, space debris, and insufficient infrastructure hinder the market entry in many emerging economies in space.

Opportunities: Advancements in reusable spacecraft systems and orbital infrastructure development are creating new long-term growth opportunities

Innovations within reusable spacecraft technology, autonomous spacecraft docking systems, spacecraft on-orbit services, and commercial spacecraft habitats have provided significant business opportunities to industry players. Growing participation of players in lunar mission explorations, space tourism, and other human spaceflight programs has widened the applicability of spacecraft worldwide. Commercial growth within space stations and orbital logistical support networks is also enabling efforts towards the development of new spacecraft technologies. Investments in advanced spacecraft operations through artificial intelligence, sustainable spacecraft propulsion systems, and deep-space transportation solutions will open up more revenue generation channels for the space sector in the future.

Recent Developments:

-

2026: SpaceX expanded next-generation spacecraft and orbital transportation initiatives supporting high-frequency mission deployment, autonomous docking capabilities, and advanced in-space mobility systems to strengthen long-duration mission infrastructure and deep-space operations.

-

2026: Blue Origin accelerated development of reusable spacecraft systems and lunar mission technologies through expanded partnerships focused on sustainable human spaceflight and next-generation orbital transportation architectures.

-

2025: Axiom Space advanced commercial orbital habitat initiatives with expanded infrastructure programs supporting private astronaut missions, orbital research capabilities, and future space station ecosystem development.

-

2025: Rocket Lab strengthened its spacecraft systems portfolio through increased satellite platform integration and next-generation deep-space mission support capabilities aimed at improving mission flexibility and spacecraft deployment efficiency.

Spacecraft Market Key Players are:

-

SpaceX

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Airbus Defence and Space

-

Boeing Defense, Space & Security

-

Thales Alenia Space

-

Maxar Technologies

-

Sierra Space

-

Blue Origin

-

Rocket Lab USA Inc.

-

L3Harris Technologies Inc.

-

RTX Corporation (Collins Aerospace Space Systems)

-

Mitsubishi Electric Corporation (Space Systems)

-

OHB SE

-

Ball Aerospace Technologies Corp.

-

Planet Labs PBC

-

Terran Orbital Corporation

-

Redwire Corporation

-

Firefly Aerospace

-

Axiom Space

Spacecraft Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.03 Billion |

| Market Size by 2035 | USD 11.81 Billion |

| CAGR | CAGR of 5.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Spacecraft Type (Satellites, Crewed Spacecraft, Cargo Spacecraft, Space Capsules, Space Stations / Habitats, Others) • By Application (Communication, Earth Observation & Remote Sensing, Navigation, Space Exploration, Space Tourism, Others) • By Orbit Type (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Earth Orbit (GEO), Sun-Synchronous Orbit (SSO), Polar Orbit, Others) • By Subsystem (Propulsion Systems, Communication Systems, Power Systems, Guidance, Navigation & Control Systems, Payload Systems, Others) • By End User (Government & Space Agencies, Commercial Space Companies, Defense Organizations, Research Institutions, Space Tourism Operators) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Lockheed Martin Corporation, Northrop Grumman Corporation, Airbus Defence and Space, Boeing Defense, Space & Security, Thales Alenia Space, Maxar Technologies, Sierra Space, Blue Origin, Rocket Lab USA Inc., L3Harris Technologies Inc., RTX Corporation (Collins Aerospace Space Systems), Mitsubishi Electric Corporation (Space Systems), OHB SE, Ball Aerospace Technologies Corp., Planet Labs PBC, Terran Orbital Corporation, Redwire Corporation, Firefly Aerospace, Axiom Space |

Frequently Asked Questions

The spacecraft market is expected to grow at a CAGR of 5.40% from 2026 to 2035

The spacecraft market was valued at USD 7.03 billion in 2025.

Rising investments in satellite constellations, deep-space exploration programs, commercial space missions, reusable spacecraft technologies, and orbital infrastructure development are driving demand for advanced spacecraft systems globally.

The satellites segment dominated the Spacecraft market in 2025.

North America dominated the Spacecraft market in 2025.

Get in Touch