Data Relay Satellite Market Report Scope & Overview:

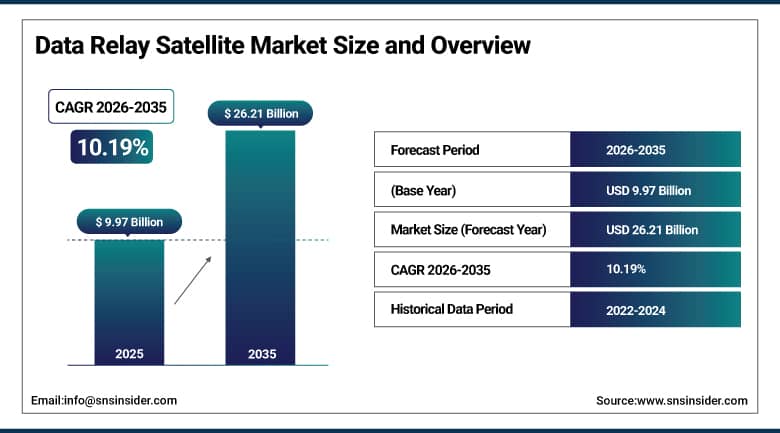

The Data Relay Satellite Market was valued at USD 9.97 billion in 2025 and is expected to reach USD 26.21 billion by 2035, growing at a CAGR of 10.19% from 2026–2035.

The data relay satellite market is experiencing rapid growth due to increased demand for high-speed space-to-ground communications and inter-satellite communications for Earth observation, defense ISR missions, and deep space explorations. The growing number of LEO mega-constellations, hybrid communication systems combining multiple orbits, and advanced relay satellites is greatly increasing the capacity for data transfer globally, decreasing latencies, and providing real-time mission-critical communications. The increased adoption of optical inter-satellite communication, AI-driven network routing, and high-throughput relay systems using Ka- and X-bands is also contributing to improved bandwidth efficiency and resilience.

In April 2025, multiple space agencies and defense organizations expanded investments in next-generation optical inter-satellite communication programs aimed at enabling ultra-low latency data relay between LEO and GEO satellite layers.

Market Size and Forecast

-

Market Size 2026E: USD 10.95 Billion

-

Market Size 2035: USD 26.21 Billion

-

CAGR (2026 - 2035): 10.19%

-

Fastest Growing Region: Asia Pacific

-

Largest Region : North America

To Get More Information On Data Relay Satellite Market - Request Free Sample Report

Data Relay Satellite Market Trends

-

Increasing adoption of hybrid multi-orbit systems is improving continuous space communication coverage.

-

Rapid growth of laser inter-satellite links is enhancing bandwidth and transmission efficiency.

-

AI-driven autonomous routing is optimizing real-time satellite data relay performance.

-

Expanding demand from defense, Earth observation, and deep space missions is driving market growth.

-

Rising use of Ka-band and X-band systems is strengthening high-capacity secure communication.

-

Growing investment in space-based broadband and global tracking systems is accelerating relay infrastructure expansion.

The US Data Relay Satellite Market Size Outlook

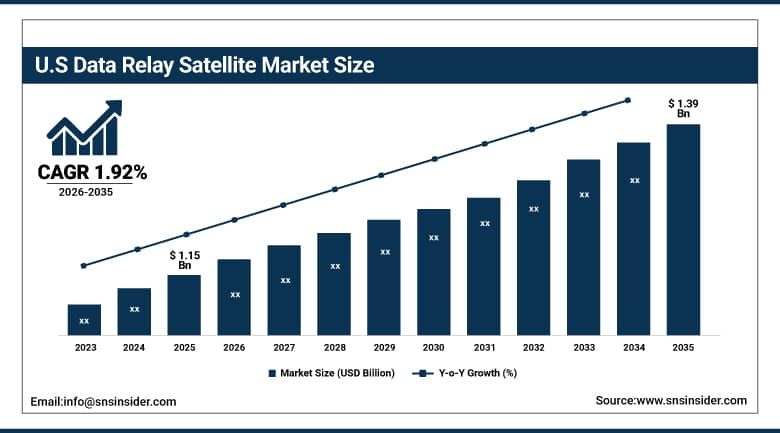

The U.S. Data Relay Satellite market was valued at USD 1.15 billion in 2025 and is expected to reach around USD 1.39 billion by 2035, growing at a CAGR of 1.92% from 2026–2035.

The U.S. data relay satellite market is currently experiencing a revolution which is being propelled by major new-generation optical intersatellite communication projects initiated by organizations such as NASA, ESA and international space agencies, with the ultimate objective of facilitating rapid transfer of high-speed data from LEO, MEO, GEO satellites and space exploration missions. The development of these technologies has greatly improved the ability to transfer data from real-time Earth observations, lunar and Martian missions, as well as disaster response operations via laser crosslinks and autonomous AI-driven data routing.

In 2025, key aerospace and defense stakeholders including SpaceX, Airbus Defence and Space, and Thales Group, alongside NASA, ESA, and allied defense organizations, expanded strategic investments in optical communication payloads, inter-satellite laser link testing, and hybrid RF–optical relay network deployment programs.

Data Relay Satellite Market Segment Analysis

-

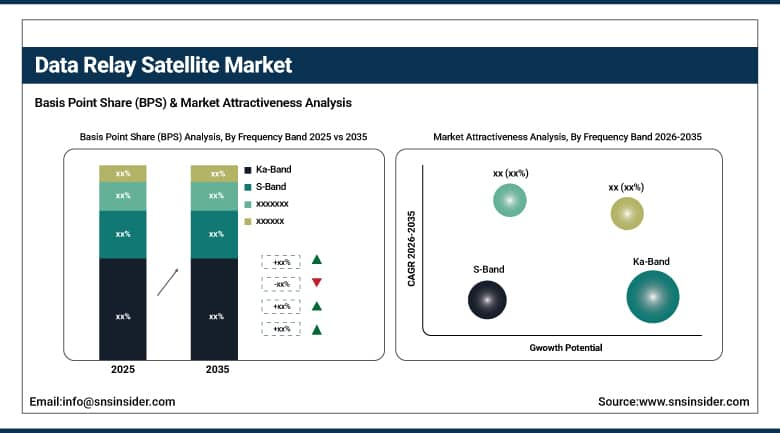

By Frequency Band, ka-band dominated the market with 31.56% share in 2025; s-band is estimated to be the fastest-growing segment.

-

By Orbit Type, geostationary earth orbit (GEO) relay satellites dominated the data relay satellite market with 48.77% share in 2025; low earth orbit (LEO) relay constellation nodes recorded the fastest CAGR.

-

By Component, space segment dominated the market with 62.36% share in 2025; user segment (terminals, transceivers, modems) recorded the fastest CAGR.

-

By Application, military & defense communications dominated the market with 34.45% share in 2025; space exploration & deep space missions recorded the fastest CAGR.

By Frequency Band, ka-band dominates the data relay satellite market, while s-band is the fastest-growing segment.

Ka-Band accounted for the leading share of about 31.56% in 2025, driven by the high level of performance in ultra-high-throughput communication, the system is quite appropriate for use in Earth observation, high resolution imaging, broadband relay and security services in defense communications. Its use in multi-gigabit satellite communications, as well as in relay communication networks in the coming generation, makes it more dominant.

S-Band is expected to grow at the fastest CAGR during 2026–2035, supported by its reliability in low power, efficient communication systems, and excellent performance in poor weather. This band has been increasingly used in small satellites, CubeSats, space network systems using IoT, and telemetry at low data rates.

By Orbit Type, geostationary earth orbit (GEO) relay satellites dominate the data relay satellite market, while low earth orbit (LEO) relay constellation nodes are the fastest-growing segment.

GEO segment held the largest share of about 48.77% in 2025, supported by its powerful capacity to offer constant and wide area coverage of stable communications support for mission-critical operations in defense and space agencies and extensive earth observation studies. The GEO satellite is still the main component of conventional space communications systems, owing to their ability to offer uninterrupted data exchange from the satellites to ground stations.

LEO relay constellation nodes are projected to register the fastest CAGR during 2026–2035, fuelled by rapid expansion of mega-constellations, increasing demand for ultra-low latency communication, and growing reliance on real-time data transmission from Earth observation satellites, UAVs, and autonomous space systems.

By Component, space segment dominates the data relay satellite market, while user segment is the fastest-growing segment.

Space Segment held the largest share of about 62.36% in 2025, supported through the implementation of sophisticated relay satellite technology, payload technologies, and multi-orbit constellations in the defense, civil space, and commercial communications domains. This segment is aided by steady investments into relay infrastructure in geosynchronous orbits (GEO) and low Earth orbit (LEO), as well as by growing reliance on hybrid optical and RF communication systems.

User Segment is projected to register the fastest CAGR during 2026–2035, driven by the growing adoption of high-tech ground terminals, phased array antenna technology, high-end transceivers, and software-defined modem technologies. Rising utilization in mobile platforms, unmanned systems, UAVs, maritime solutions, and future satellite broadband communication networks will continue to drive demand forward.

By Application, military & defense communications dominate the data relay satellite market, while space exploration & deep space missions are the fastest-growing segment.

Military & Defense segment held the highest share of about 34.45% in 2025, driven by growing dependence on secure and encrypted and real-time ISR data relay systems, battlefield communication networks, surveillance activities, and strategic command and control communications networks. Growing geopolitical uncertainties and modernization efforts for defense satellite systems are driving even more demand for reliable and jam-proof communication networks.

Space Exploration & Deep Space Missions is projected to grow at the fastest CAGR during 2026–2035, backed by the development of more extensive lunar exploration projects, missions to Mars, asteroid exploration missions, and space science missions that explore deep space. Growing demand for constant and reliable communication of large amounts of data among spacecraft, relay satellites in orbit, and earth-bound control stations is making way for new communication technologies.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

86.49% |

|

Europe |

Germany |

25.56% |

|

Asia Pacific |

China |

42.27% |

|

Middle East & Africa |

UAE |

16.65% |

|

Latin America |

Brazil |

34.89% |

North America Data Relay Satellite Market Insights

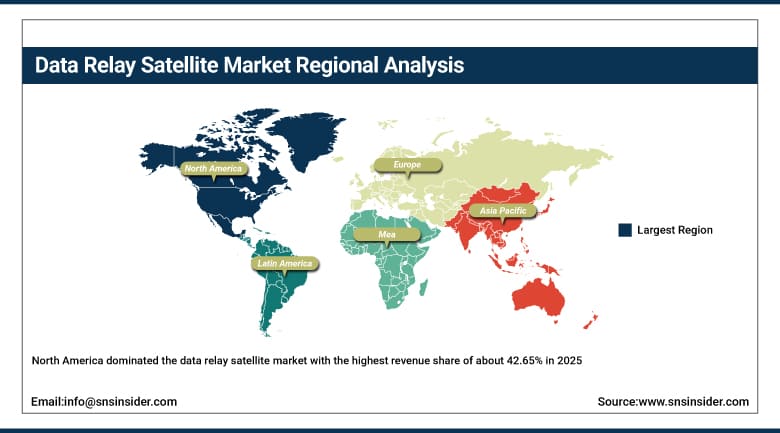

North America dominated the data relay satellite market with the highest revenue share of about 42.65% in 2025 due to strong presence of advanced space infrastructure, high defense space spending, and leadership in satellite communication technologies across the United States and Canada. The region benefits from extensive deployment of GEO and emerging LEO relay systems supported by NASA, the U.S. Department of Defense, and leading private space companies. Strong demand for secure ISR data relay, deep-space mission support, and real-time Earth observation transmission continues to reinforce regional dominance. Increasing integration of optical communication systems and multi-orbit satellite architectures is further strengthening the region’s technological leadership in data relay networks. NASA’s Artemis program is accelerating demand for lunar relay communication systems, driving development of next-generation deep-space data relay satellites for continuous Earth–Moon connectivity.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Data Relay Satellite Market Insights

Europe holds a significant position in the data relay satellite market driven by strong contributions from the European Space Agency (ESA), advanced satellite manufacturing ecosystem, and increasing focus on sovereign space communication capabilities. Countries such as Germany, France, and the UK are actively investing in secure space-based communication infrastructure and Earth observation data relay systems. The region also benefits from strong regulatory emphasis on space sustainability, interoperability, and cross-border satellite communication programs. Growing adoption of optical inter-satellite links and collaborative EU space initiatives continues to enhance Europe’s role in global data relay networks.ESA’s EDRS (European Data Relay System) expansion is enhancing high-speed laser-based data transmission between LEO satellites and ground stations, improving near-real-time Earth observation capabilities.

Asia Pacific Data Relay Satellite Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 11.32% from 2026-2035 emerging as a high-growth region in the data relay satellite market, supported by rapid expansion of space programs in China, India, Japan, and South Korea. The region is witnessing strong investments in satellite constellations, space exploration missions, and national communication infrastructure development. Increasing deployment of Earth observation satellites, smart city programs, and defense modernization initiatives is driving demand for robust data relay systems. Government-backed space agencies and rising participation of private space companies are accelerating innovation in multi-orbit communication architectures across the region. ISRO is expanding its satellite communication and relay capabilities under Gaganyaan and future interplanetary missions, strengthening India’s autonomous space communication infrastructure.

Middle East & Africa and Latin America Data Relay Satellite Market Insights

Middle East & Africa (MEA) and Latin America regions are gradually expanding their presence in the data relay satellite market through investments in satellite communication infrastructure, defense modernization, and space program development. In MEA, countries such as the UAE and Saudi Arabia are actively investing in space technologies and national satellite programs, while in Latin America, Brazil and Mexico are improving Earth observation and communication satellite capabilities. Increasing demand for secure connectivity, disaster monitoring, and remote sensing applications is driving adoption of satellite relay systems across both regions.UAE’s Mohammed Bin Rashid Space Centre (MBRSC) is expanding satellite communication capabilities to support Earth observation and interplanetary missions such as Mars exploration programs.

Market Dynamics:

Growth Drivers: Expanding demand for real-time satellite communication and multi-orbit connectivity networks is accelerating market adoption

Growing demand for continuous, high-speed, and low-latency satellite communication is significantly driving the data relay satellite market. Increasing deployment of LEO satellite constellations, Earth observation systems, and deep-space missions has created strong need for uninterrupted data relay infrastructure between space assets and ground stations. Rising reliance on real-time ISR data in defense operations, climate monitoring, and disaster management is further boosting adoption. Additionally, advancements in inter-satellite laser communication, GEO–LEO hybrid relay systems, and autonomous data routing technologies are enhancing transmission efficiency. Growing investments in space exploration programs and commercial satellite networks are further strengthening long-term market expansion.

Restraints: High deployment costs and orbital infrastructure complexity are limiting large-scale market scalability

The data relay satellite market faces significant restraints due to high costs associated with satellite manufacturing, launch operations, and orbital deployment of relay infrastructure. Developing and maintaining GEO and LEO relay networks requires advanced technology integration, increasing overall capital expenditure for space agencies and private operators. Additionally, complex orbital coordination, frequency spectrum allocation challenges, and regulatory constraints slow down system deployment. Vulnerability to space debris, signal interference, and cybersecurity risks in space communication networks further restrict seamless adoption. Limited standardization across multi-orbit systems and dependence on long development cycles also act as barriers to rapid commercialization in emerging space economies.

Opportunities: Expansion of deep-space missions and AI-enabled autonomous satellite networks is creating strong growth potential

Rising investments in lunar exploration, Mars missions, and deep-space communication systems are creating significant opportunities for the data relay satellite market. Growing adoption of AI-enabled autonomous satellite networks is enabling intelligent routing of data across multi-orbit relay systems, improving efficiency and reducing latency. The development of optical inter-satellite communication, quantum-encrypted data transfer, and software-defined satellite architectures is further transforming the market landscape. Increasing participation of private space companies in satellite-as-a-service models is expanding commercial opportunities. Additionally, integration of data relay systems with 5G/6G non-terrestrial networks (NTN) and IoT-based satellite applications is opening new revenue streams globally.

Recent Developments

-

2026: NASA advanced its Artemis lunar communication program by progressing next-generation data relay satellites integrating laser and RF communication systems. These upgrades aim to support continuous, high-speed Earth–Moon data transmission for crewed missions and lunar surface operations.

-

2026: The U.S. Space Force expanded its resilient LEO satellite communication network under its proliferated architecture program, focusing on secure, jam-resistant inter-satellite links and real-time defense data relay capabilities.

-

2025: ESA upgraded the European Data Relay System (EDRS) with enhanced laser communication terminals, improving high-speed Earth observation data transfer between LEO satellites and ground stations for environmental and security applications.

-

2025: China’s Tianlian relay satellite network was enhanced by CASC to improve deep-space and lunar mission communication, strengthening continuous data transmission between spacecraft and Earth control centres.

Data Relay Satellite Market Key Players are:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Airbus Defence and Space

-

Thales Group

-

Boeing

-

L3Harris Technologies

-

RTX Corporation

-

Maxar Technologies

-

SES S.A.

-

Eutelsat Group

-

Telesat

-

Viasat Inc.

-

Iridium Communications Inc.

-

Kratos Defense & Security Solutions

-

Honeywell

-

OHB SE

-

Surrey Satellite Technology Ltd

-

Rocket Lab USA Inc.

-

SpaceX

-

China Satellite Communications Co., Ltd.

Data Relay Satellite Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.97 Billion |

| Market Size by 2035 | USD 26.21 Billion |

| CAGR | CAGR of 10.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Orbit Type (Geostationary Earth Orbit (GEO) Relay Satellites, Medium Earth Orbit (MEO) Relay Satellites, Low Earth Orbit (LEO) Relay Constellation Nodes) • By Component (Space Segment (Relay Satellites, Constellation Nodes), Ground Segment (Ground Stations, Control Centers, Antennas), User Segment (Terminals, Transceivers, Modems)) • By Frequency Band (Ka-Band,S-Band Ku-Band, X-Band) • By Application (Military & Defense Communications,Earth Observation Data Relay Space Exploration & Deep Space Missions, Maritime & Aviation Tracking, Disaster Monitoring & Emergency Response) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin, Northrop Grumman, Airbus Defence and Space, Thales Group, Boeing, L3Harris Technologies, RTX Corporation, Maxar Technologies, SES S.A., Eutelsat Group, Telesat, Viasat Inc, Iridium Communications Inc, Kratos Defense & Security Solutions, Honeywell, OHB SE, Surrey Satellite Technology Ltd, Rocket Lab USA Inc, SpaceX, China Satellite Communications Co., Ltd. |

Frequently Asked Questions

The Data Relay Satellite market is expected to grow at a CAGR of 9.97% from 2026 to 2035.

The Data Relay Satellite market was valued at USD 26.21 billion in 2025.

Rising investments in deep space exploration, Earth observation constellations, defense satellite communications, and multi-orbit relay architectures are driving demand for advanced Data Relay Satellite systems globally.

The Geostationary Earth Orbit (GEO) Relay Satellites segment dominated the Data Relay Satellite market in 2025.

North America dominated the Data Relay Satellite market in 2025.

Get in Touch