Aircraft Mounts Market Report Scope & Overview:

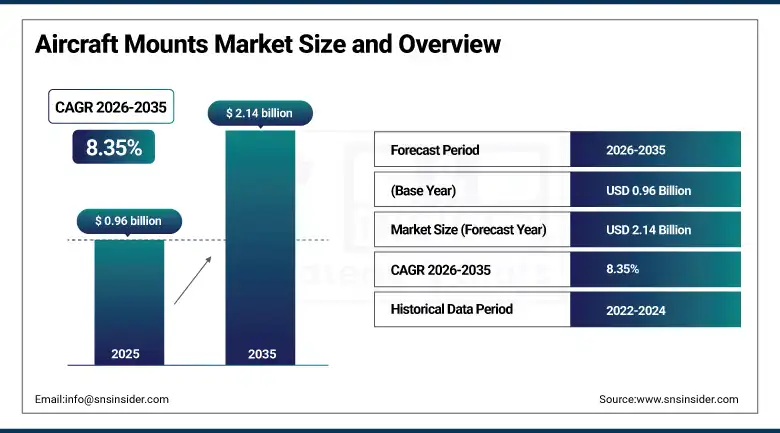

The aircraft mounts market was valued at USD 0.96 billion in 2025 and is expected to reach USD 2.14 billion by 2035, growing at a CAGR of 8.35% from 2026–2035.

Ask any aerospace engineer what keeps an aircraft running safely and they will tell you it is not just the engine; it is everything that holds the engine in place. Aircraft mounts are the unsung workhorses of aviation. They secure engines, avionics, landing gear, and structural panels, and they absorb the relentless vibration and shock loads that every flight generates. Demand for these components is climbing steadily, pulled along by a global commercial aviation sector that is ordering new aircraft faster than at any point since the mid-2010s. Airbus crossed the 12-unit-per-month mark on A350 production in 2025 while Boeing pressed hard to restore B737 MAX output. Each new airframe rolling off the line needs a full complement of mounts, and the math is simple: more aircraft means more mount demand.

Governments across the United States, Europe, and Asia Pacific continued to fund next-generation fighter programs, rotary-wing platforms, and unmanned systems throughout 2024 and 2025, all of which require specialized high-performance mount assemblies. Meanwhile, stricter cabin noise regulations from EASA and FAA have pushed airlines toward comprehensive interior mount upgrades across existing fleets, while the arrival of hybrid-electric propulsion programs has created genuinely new design challenges battery packs and electric motors impose thermal and vibration profiles that traditional elastomeric mounts were never engineered to handle. That gap between what the market needs and what legacy products can deliver is exactly where innovation and new spending is concentrated.

Market Size and Forecast

-

Market Size 2026E: USD 1.04 Billion

-

Market Size 2035: USD 2.14 Billion

-

CAGR: 8.35% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Aircraft Mounts Market - Request Free Sample Report

Aircraft Mounts Market Trends

-

Rising commercial aircraft production rates at Airbus and Boeing are accelerating OEM mount procurement, with Tier 1 suppliers expanding long-term supply agreements to keep pace with factory output schedules.

-

Introduction of hybrid-electric and fully electric propulsion architectures is creating demand for next-generation thermal-resistant and high-damping mount designs that conventional elastomer-based products cannot adequately address.

-

Increasingly stringent cabin noise and vibration targets from regulators are driving airline fleet-wide interior mount retrofit campaigns, giving aftermarket suppliers a growing and predictable revenue stream.

-

Additive manufacturing is finding early adoption among specialty mount producers, enabling complex internal geometries that improve vibration isolation performance while reducing component weight a critical metric for every gram-conscious airframe program.

-

Defense electrification and unmanned aerial vehicle proliferation are opening new mount application categories that go well beyond the scope of conventional commercial aviation mount specifications.

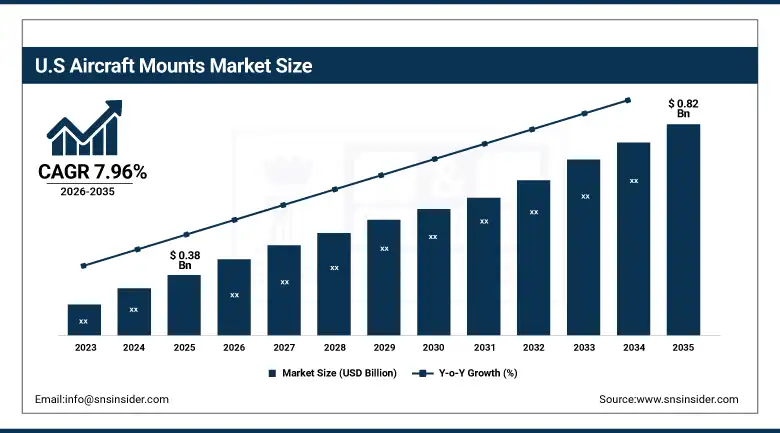

The U.S. Aircraft Mounts Market Size Outlook

The U.S. aircraft mounts market was valued at USD 0.38 billion in 2025 and is expected to reach around USD 0.82 billion by 2035, growing at a CAGR of 7.96% from 2026–2035.

The United States has long been the backbone of global aircraft mount supply. Lord Corporation, based in Cary, North Carolina, practically invented the modern aircraft elastomeric mount category, and the domestic supplier ecosystem that surrounds Boeing's commercial and defense programs in Washington, South Carolina, and Texas represents the densest concentration of mount production capability anywhere in the world. Defense spending is a particular tailwind the F-35 program alone, with its multi-decade production and maintenance lifecycle, generates sustained demand for specialized vibration isolation and engine mount assemblies. Commercial recovery has also been robust: U.S. carriers placed over 800 new narrowbody orders in the 2023–2025 period, all of which translate into forward OEM mount procurement commitments across the domestic supply chain.

TransDigm Group, one of America's largest aerospace component specialists, strengthened its aircraft mount portfolio through targeted acquisition and product line expansion in 2025, adding high-damping vibration isolation assemblies for next-generation narrowbody applications. The company's build-to-print manufacturing model and long-term MRO contract arrangements with major U.S. carriers reinforced the aftermarket revenue durability that has historically defined TransDigm's competitive positioning in the U.S. aerospace component market.

Aircraft Mounts Market Segment Analysis

-

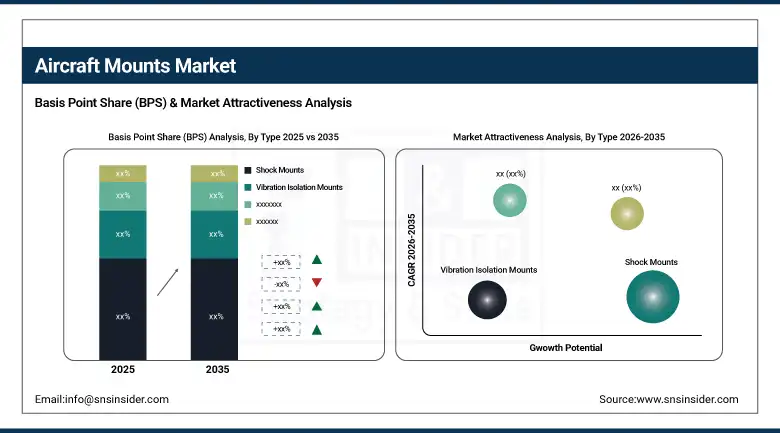

By Type, the shock mounts segment dominated the aircraft mounts market with 42.64% share in 2025, while the vibration isolation mounts segment is the fastest growing.

-

By Mount Position, the exterior mounts segment dominated the aircraft mounts market with 64.92% share in 2025, while the interior mounts segment is the fastest growing.

-

By Aircraft Type, the commercial aircraft segment dominated the aircraft mounts market with 67.10% share in 2025, while the business & general aviation segment is the fastest growing.

-

By End User, the OEM segment dominated the aircraft mounts market with 69.60% share in 2025, while the aftermarket/MRO segment is the fastest growing.

By Type, the shock mounts segment dominates the aircraft mounts market, while vibration isolation mounts are the fastest-growing segment.

Shock mounts held the leading revenue share of 42.64% in 2025, and it is not hard to see why. Every aircraft from a regional turboprop to a widebody freighter relies on shock mounts to protect engines, avionics, and structural sub-assemblies from the transient impact loads generated during ground operations, turbulence, and hard landings. The sheer breadth of shock mount applications across airframe types, combined with the component's relatively short service life compared to structural hardware, creates a high-volume and largely predictable replacement cycle. Certification requirements mean that approved shock mount assemblies cannot simply be substituted with cheaper alternatives mid-program, giving qualified suppliers a defensible competitive moat.

Vibration isolation mounts are where the real growth story sits. As aircraft carry more sensitive avionics, ISR payloads, and mission electronics and as airlines push for quieter cabins that meet increasingly tight noise targets the performance demands placed on vibration isolation products have risen sharply. Operators are replacing these mounts proactively rather than reactively to avoid unscheduled removals, which is creating predictable aftermarket demand that layers on top of OEM procurement. The broader electrification trend adds urgency: electric motors and battery packs introduce vibration signatures quite different from conventional turbofan engines, and mount suppliers are investing heavily in new elastomer compounds and active damping technologies to address them.

By Mount Position, the exterior mounts segment dominates the aircraft mounts market, while interior mounts are the fastest-growing segment.

Exterior mounts commanded 64.92% of market revenue in 2025, reflecting their critical role in securing the components most exposed to flight loads and environmental extremes engine nacelles, landing gear assemblies, wing attachment fittings, and external fuel systems. These applications demand materials that can withstand wide temperature swings, hydraulic fluid exposure, UV radiation, and the continuous cyclic loading of flight operations. Titanium, high-strength aluminum alloys, and specialty elastomers with FAR-rated fire resistance dominate exterior mount specifications. Because exterior mounts sit at the intersection of structural integrity and airworthiness, regulatory approval cycles are long and switching costs are high, which means established suppliers benefit from strong program continuity once qualified.

Interior mounts are growing faster, driven by two forces. First, passenger comfort expectations have shifted airlines competing on long-haul premium product quality have invested significantly in seat, galley, monument, and overhead bin mount systems that reduce vibration transmission into the cabin. Second, the proliferation of in-flight entertainment and connectivity equipment has created entirely new interior mount application categories that barely existed a decade ago. Each IFE screen, satellite antenna interface, and cabin Wi-Fi access point requires a certified mount solution, and with thousands of retrofit programs underway globally, the interior mount addressable market has expanded materially in recent years.

By Aircraft Type, the commercial aircraft segment dominates the aircraft mounts market, while business & general aviation is the fastest-growing segment.

Commercial aircraft accounted for 67.10% of market revenue in 2025, a dominance rooted in the sheer scale of global fleet operations. With over 28,000 commercial aircraft in active service worldwide and production rates climbing back toward pre-pandemic peaks, the OEM and aftermarket mount demand generated by this segment dwarfs all others. Narrowbody platforms the Boeing 737 MAX and Airbus A320 family are the volume workhorses, each requiring extensive mount assemblies for engines, auxiliary power units, avionics bays, and cabin interiors. Wide-body programs generate fewer units but command premium pricing due to the more complex and larger-format mount assemblies required.

Business and general aviation is the segment growing fastest on a percentage basis. The post-pandemic explosion in private aviation demand business jet backlog at Gulfstream, Dassault, Bombardier, and Textron remained extended well into 2025 is translating directly into mount procurement for new OEM deliveries. At the same time, the urban air mobility sector is adding a genuinely new dimension to business aviation mount demand. eVTOL platforms require vibration isolation and shock mount designs that differ fundamentally from conventional turbine aircraft applications, and first-mover suppliers in this nascent but rapidly expanding segment stand to benefit significantly as programs transition from certification to production.

By End User, the OEM segment dominates the aircraft mounts market, while the aftermarket/MRO segment is the fastest-growing.

The OEM channel provided 69.60% of the market value in 2025 due to the business model where mounts are bought directly from mount makers by airframe manufacturers through a long-term contract. In the OEM mount sales, the economics are characterized by the commitment to certain production volumes, multi-year contracts signed during program launch, and the qualification costs needed to secure first-article approval. Although OEM pricing is better compared to that of the aftermarket, the high volume assurance and long-term contracts help suppliers secure predictable revenue streams that enable them to plan for future capital investments and staffing needs.

The MRO segment continues to grow because the global fleet of passenger airliners is getting older but operating with increasingly heavy duty. After a quick recovery of the average utilization rates following 2022, there is increased wear due to high cycle operation. Mounts are increasingly supplied together with MRO service packages offered by MRO firms as part of power-by-the-hour agreements. In addition, condition-based maintenance and digital health monitoring systems are making airlines prefer pro-active mount replacements ahead of performance-related issues, thus favoring aftermarket growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.34% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

36.82% |

|

Middle East & Africa |

Saudi Arabia |

22.46% |

|

Latin America |

Brazil |

43.72% |

North America Aircraft Mounts Market Insights

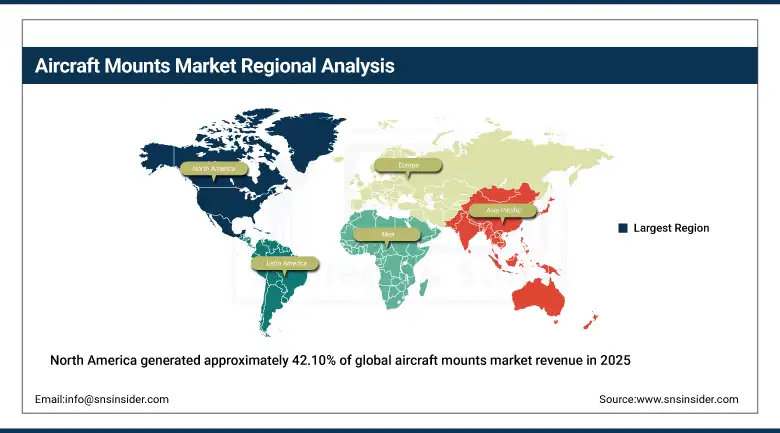

North America generated approximately 42.10% of global aircraft mounts market revenue in 2025. The United States is the clear regional anchor, housing Boeing's commercial and defense manufacturing network, the headquarters of several leading mount suppliers including Lord Corporation and TransDigm, and the world's largest commercial airline fleet by available seat miles. FAA certification requirements create a natural domestic competitive advantage for U.S.-based mount manufacturers whose products already hold the approvals needed to serve domestic carriers and OEM programs. Canada contributes meaningful supplementary demand, particularly through Bombardier's business jet production facilities in Montreal and the country's well-developed aerospace MRO sector.

The U.S. Department of Defense's continued investment in next-generation air platforms including the B-21 Raider bomber, the F/A-XX naval fighter program, and extensive rotary-wing modernization initiatives is sustaining a deep and diversified defense-sector mount procurement pipeline that insulates the North American market from the cyclical volatility that can affect commercial aviation-dependent supply chains. Defense mount programs typically operate on longer qualification and procurement timelines that provide revenue visibility extending well into the 2030s.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Aircraft Mounts Market Insights

Europe represented approximately 26.48% of global aircraft mounts market revenue in 2025. The Airbus A320 and A350 production ramp at facilities in Hamburg, Toulouse, Seville, and Broughton is the primary commercial demand engine, pulling mount procurement from a dense network of qualified European Tier 1 and Tier 2 suppliers. France, Germany, the United Kingdom, and Spain are the dominant national contributors, each hosting both OEM production facilities and established aerospace component manufacturers. Safran, Hutchinson (a TotalEnergies subsidiary), and Trelleborg all maintain significant aircraft mount operations within the region. The European defense spend surge following NATO's recommitment to national defense investment targets has added a new layer of demand from fighter, transport, and rotary-wing platform programs.

Airbus's announced production rate targets for the A320 family targeting 75 aircraft per month by 2027 represent one of the most significant OEM demand stimulus events in European aerospace component history. Qualifying to supply mount assemblies for A320-series production at this output level requires substantial investment in manufacturing capacity, quality systems, and raw material procurement, and suppliers that have secured long-term program positions are in the process of expanding production accordingly.

Asia Pacific Aircraft Mounts Market Insights

Asia Pacific is forecast to be the fastest-growing regional market during 2026–2035, projected at a CAGR of approximately 9.12%. China's COMAC C919 single-aisle program which delivered its first commercial aircraft in 2023 and has an extensive domestic order backlog is building out a new locally-sourced aerospace component supply chain, including mount assemblies, that will progressively reduce dependence on Western suppliers over the forecast period. India's civil aviation sector, which has become one of the world's fastest-growing airline markets by passenger volume, is generating escalating mount demand through new aircraft orders from IndiGo, Air India, and Akasa Air. Japan, South Korea, Australia, and Singapore each contribute meaningful regional demand through both airline fleet expansion and defense aircraft programs.

COMAC, the leading commercial aircraft producer in China, is developing its own local mount supplier network that complies with CAAC airworthiness regulations. Several Chinese companies that manufacture aerospace components have obtained or applied for approval to produce mounts from either elastomers or metals in connection with the assembly of the C919 aircraft. The emergence of local mounts will gradually drive down demand for imports during the forecast period 2026-2035, posing a challenge to foreign suppliers in retaining their market share in China.

Middle East & Africa and Latin America Aircraft Mounts Market Insights

The Middle East & Africa and Latin America regions are smaller but commercially relevant markets for aircraft mounts, collectively driven by fleet expansion across Gulf carrier operations, growing African airline capacity investment, and Latin American commercial aviation recovery. Emirates, Qatar Airways, and Etihad have among the world's most modern and rapidly expanding widebody fleets, generating aftermarket mount demand as aircraft age through their mid-life maintenance cycles. Saudi Arabia's Vision 2030 aviation ambitions including the development of a domestic aerospace manufacturing base are creating new regional production and procurement opportunities. Brazil's Embraer remains a globally significant narrow-body and business jet OEM whose production programs generate direct mount procurement demand from a regionally anchored supply chain.

Embraer's E2 family production expansion and its growing defense product portfolio including the KC-390 military transport aircraft represent sustained mount procurement anchors for Latin America's aircraft component supply ecosystem. The company's increasing success in export sales for both commercial and defense platforms extend the geographic reach of mount demand generated by Embraer-linked supply chains well beyond the Brazilian domestic market.

Market Dynamics

Growth Drivers: Recovering commercial aircraft production rates and escalating defense program investment are the twin engines powering aircraft mounts market growth globally.

The recovery of commercial aviation to and beyond pre-pandemic output levels has been the most consequential demand driver for the aircraft mounts market since 2022. Both Airbus and Boeing are operating well above 2019 production unit volumes, and the combined orderbook across the two manufacturers represents over ten years of production at current rates a forward demand signal that gives mount suppliers the confidence to invest in capacity expansion. Defense spending across NATO nations, driven by the geopolitical environment, has restored growth to military aircraft programs that experienced budget pressure in the preceding decade. New fighter, transport, and unmanned platform programs each carry multi-decade mount procurement profiles that extend well beyond the initial production run into the sustained MRO lifecycle.

Restraints: Raw material cost volatility and lengthy aerospace qualification cycles constrain new entrant growth and compress supplier margins during inflationary periods.

Specialty materials high-grade titanium alloys, aerospace-specification elastomers, and nickel superalloys experienced significant price and availability disruptions in the 2022–2024 period, and suppliers with fixed-price long-term OEM contracts absorbed meaningful margin compression as a result. The qualification requirements for aircraft mount assemblies are among the most stringent in aerospace component manufacturing. FAA, EASA, and CAAC approval processes can take two to five years from initial design to first-article approval, effectively ruling out rapid competitive response to market shifts and creating a barrier that small manufacturers struggle to overcome. These structural factors tend to concentrate market share among established players and slow the pace of innovation adoption.

Opportunities: The emergence of eVTOL platforms and hybrid-electric aircraft programs is creating entirely new mount application categories with no incumbent product heritage.

The urban air mobility sector is small today but growing rapidly. Archer, Joby, Lilium's successor programs, and numerous other eVTOL developers are advancing toward type certification with aircraft whose vibration and shock profiles differ substantially from any conventional platform. Electric motor mounts must manage high-frequency vibration at amplitudes and frequencies that conventional elastomeric mount compounds were not designed to handle. This gives mount suppliers with active materials expertise and computational mount design capabilities an opportunity to establish first-mover qualified positions on programs that could scale to thousands of units annually by the early 2030s. Suppliers that invest in eVTOL mount qualification today are building a competitive runway that will be difficult for latecomers to match.

Recent Developments

-

2025: Lord Corporation (Parker Hannifin) expanded its next-generation elastomeric mount product line with new high-temperature resistant formulations developed specifically for hybrid-electric propulsion applications, completing qualification testing across multiple OEM development programs and positioning the company for production supply agreements as these platforms advance toward certification.

-

2025: TransDigm Group completed the acquisition of a specialist aircraft vibration isolation mount manufacturer, adding proprietary active damping technology and an established military platform qualification base to its aerospace component portfolio, reinforcing its aftermarket-oriented business model with new OEM program content.

-

2024: Safran Landing Systems introduced an updated landing gear mount assembly architecture for next-generation widebody applications, incorporating additive-manufactured titanium load path components that reduced assembly weight by 12% while maintaining fatigue certification margin requirements under EASA CS-25 airworthiness standards.

-

2024: Hutchinson SA advanced the development of its composite-integrated mount system for COMAC C919 domestic supply qualification, completing analytical and test milestone requirements as part of the broader Chinese aviation sector's push to reduce dependence on Western aerospace component suppliers across key structural systems.

-

2023: Trelleborg Vibracoustic Aerospace extended its commercial aircraft interior mount product range to address new cabin monument and connectivity equipment installation applications, targeting the large-scale IFE and cabin connectivity retrofit market that accelerated significantly as airlines invested in premium passenger experience differentiation following pandemic recovery.

Aircraft Mounts Market Key Players are:

-

Lord Corporation (Parker Hannifin)

-

TransDigm Group

-

Hutchinson SA

-

Safran

-

Trelleborg

-

Meggitt PLC (Parker Hannifin)

-

Moog Inc.

-

Collins Aerospace (RTX)

-

Eaton Corporation

-

The VMC Group

-

Mayday Manufacturing

-

Cadence Aerospace

-

Barry Controls (Hutchinson)

-

IAC Acoustics

-

Senior Flexonics

-

Vibration Isolation Products (VIP)

-

GMT Rubber-Metal-Technic Ltd

-

Haigh-Farr Inc.

-

Aromat Corporation

-

Airbus (systems integration)

Aircraft Mounts Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.96 Billion |

| Market Size by 2035 | USD 2.14 Billion |

| CAGR | CAGR of 8.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Shock Mounts, Vibration Isolation Mounts, Engine Mounts, Airframe Mounts, Landing Gear Mounts, Others) • By Mount Position (Exterior Mounts, Interior Mounts) • By Aircraft Type (Commercial Aircraft, Military Aircraft, Business & General Aviation, Helicopters) • By End User (OEM, Aftermarket/MRO) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Lord Corporation (Parker Hannifin), TransDigm Group, Hutchinson SA, Safran, Trelleborg, Meggitt PLC (Parker Hannifin), Moog Inc., Collins Aerospace (RTX), Eaton Corporation, The VMC Group, Mayday Manufacturing, Cadence Aerospace, Barry Controls (Hutchinson), IAC Acoustics, Senior Flexonics, Vibration Isolation Products (VIP), GMT Rubber-Metal-Technic Ltd, Haigh-Farr Inc., Aromat Corporation, Airbus (systems integration) |

Frequently Asked Questions

The Aircraft Mounts market was valued at USD 0.96 billion in 2025.

Get in Touch