Atomic Clock Market Report Scope & Overview:

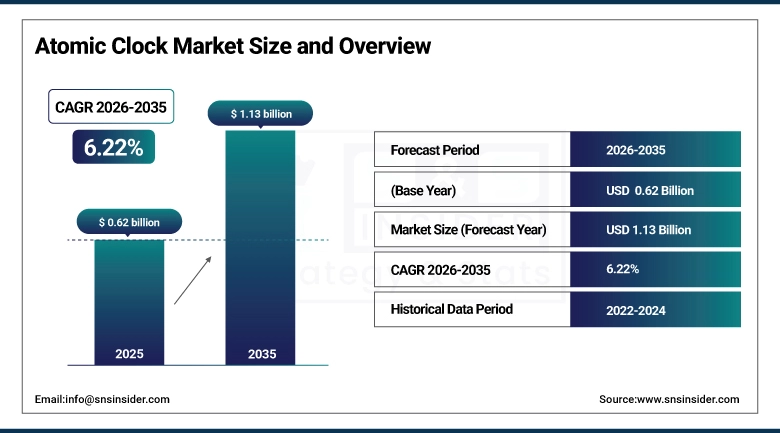

The Atomic Clock Market was valued at USD 0.62 billion in 2025 and is expected to reach USD 1.13 billion by 2035, growing at a CAGR of 6.22% from 2026–2035.

Atomic Clocks Market is expected to register steady growth due to rapid development of GNSS navigational systems, increasing demand for time synchronizing technology in emerging 5G/6G telecommunication network deployments, and growing need for robust military timing systems which do not rely on GPS technology. Growing adoption of chip scale atomic clock technology in portable applications and military & aerospace sector along with advanced communication equipment will provide additional impetus to market growth. At the same time, advances in optical atomic clock systems have enabled the industry to achieve higher levels of accuracy.

In parallel, global initiatives such as GPS modernization programs (GPS III and GPS IIIF), Europe’s Galileo expansion, China’s BeiDou Phase IV deployment, and India’s NavIC enhancement program are significantly increasing reliance on onboard atomic clocks for satellite positioning accuracy.

Additionally, telecom standardization bodies such as the 3rd Generation Partnership Project (3GPP) are driving stricter timing precision requirements for 5G and emerging 6G networks, accelerating adoption of atomic clock-based synchronization solutions across telecom infrastructure worldwide.

Atomic Clock Market Size and Forecast

-

Market Size in 2025: USD 0.62 Billion

-

Market Size by 2035: USD 1.13 Billion

-

CAGR: 6.22% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Atomic Clock Market - Request Free Sample Report

Atomic Clock Market Trends

-

Rising adoption of GNSS and satellite navigation systems is increasing demand for ultra-precise atomic clock-based timing synchronization.

-

Expansion of 5G/6G networks is accelerating deployment of high-accuracy timing infrastructure across telecom ecosystems.

-

Growing integration of chip-scale atomic clocks (CSACs) in defense, UAVs, and portable systems is improving GPS-denied operational capability.

-

Advancements in optical atomic clocks are driving next-generation ultra-precision timing for research and space applications.

-

Increasing focus on GPS-independent and anti-jamming navigation systems is boosting demand for resilient timing solutions.

-

Satellite modernization programs (GPS, Galileo, BeiDou, NavIC) are expanding reliance on onboard atomic clocks for positioning accuracy.

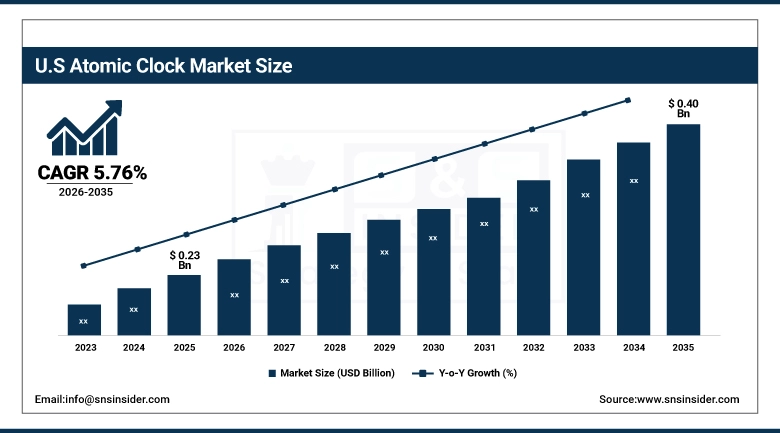

The U.S. Atomic Clock Market was valued at USD 0.23 billion in 2025 and is expected to reach around USD 0.40 billion by 2035, growing at a CAGR of 5.76% from 2026–2035.

The United States is considered to have the biggest share in the global market of atomic clocks because of the presence of advanced GNSS technology (GPS), defense navigation and time systems, as well as mass application of synchronization systems at 5G/6G telecommunication networks, aircraft systems, and finance systems needing nanosecond accuracy. It also shows great leadership in this area through extensive use of atomic clocks in satellite navigation and secure military communication, and even quantum time system development, thus being the center of the global market of atomic clocks.

Supporting this growth, agencies such as the National Institute of Standards and Technology (NIST) are advancing next-generation timekeeping systems, including optical atomic clock research and ultra-stable frequency standards, strengthening the country’s leadership in precision timing innovation.

Additionally, continuous investments from the U.S. Department of Defense (DoD) and NASA in GPS modernization programs (GPS III and GPS IIIF) and resilient, anti-jamming navigation systems are accelerating adoption of advanced atomic clock technologies across military and space-based platforms.

Atomic Clock Market Segment Highlights

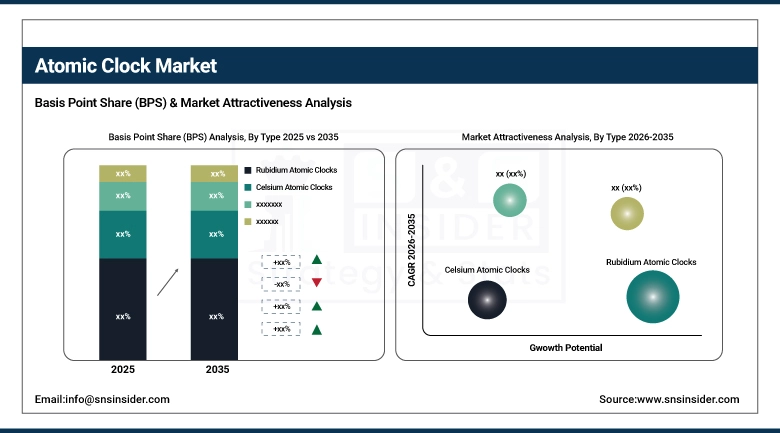

• By Type, Rubidium Atomic Clocks dominated the Atomic Clock Market with 32.36% share in 2025; Optical Atomic Clocks are the fastest growing segment

• By Platform, Space-Based Systems (satellites/GNSS) dominated the Atomic Clock Market with 38.15% share in 2025; Portable & Embedded Systems (CSAC-based devices) are the fastest growing segment

• By Application, GNSS & Navigation Systems (GPS, Galileo, BeiDou, NavIC) dominated the Atomic Clock Market with 30.85% share in 2025; Telecommunications (5G/6G synchronization) is the fastest growing segment

• By End User, Government & Defense Agencies dominated the Atomic Clock Market with 40.24% share in 2025; Telecom Operators are the fastest growing segment

By Type, Rubidium Atomic Clocks segment dominates the Atomic Clock Market, Optical Atomic Clocks expected to grow fastest

In 2025, the Rubidium Atomic Clocks segment maintained its dominant position in the Atomic Clock Market, accounting for 32.36% of total revenue. The effectiveness of this leadership comes from the strength in its stability, efficiency, and widespread use in GNSS devices, telecom networks, and space navigation systems. The rubidium oscillator finds extensive usage in industries for medium precision timekeeping requirements due to its reliability, thus making it the most widely utilized atomic clock technology in the world.

From 2026 to 2035, the Optical Atomic Clocks segment is projected to register the highest CAGR. This rapid growth is driven by breakthroughs in ultra-precision timekeeping, significantly higher accuracy compared to traditional microwave-based clocks, and increasing adoption in advanced scientific research, deep-space missions, and next-generation metrology systems requiring extreme time stability.

By Platform, Space-Based Systems (satellites/GNSS) segment dominates the Atomic Clock Market, Portable & Embedded Systems (CSAC-based devices) expected to grow fastest

In 2025, the Space-Based Systems (satellites/GNSS) segment held the largest share of 38.15% in the Atomic Clock Market, due to its essential importance in navigation satellites of the world like GPS, Galileo, BeiDou, and NavIC. Such systems require accurate atomic clocks that help in maintaining precise positions and time synchronization worldwide, thus becoming crucial in civilian, military, and aerospace missions.

From 2026 to 2035, the Portable & Embedded Systems (CSAC-based devices) segment is expected to register the highest CAGR. Growth is fueled by increasing demand for miniaturized, low-power atomic clocks in defense electronics, UAVs, autonomous systems, and field-deployable communication platforms where GPS-denied or jammed environments require independent timing resilience.

By Application, GNSS & Navigation Systems segment dominates the Atomic Clock Market, Telecommunications (5G/6G synchronization) segment expected to grow fastest

In 2025, the GNSS & Navigation Systems segment maintained the highest application share of 30.85% in the Atomic Clock Market. The dominance stems from the fundamental requirement for these GPS-based satellite navigation systems to use timekeeping based on atomic clocks to be able to achieve precision in geolocation and navigation. In other words, GNSS systems constitute the essential infrastructure that is used for geolocation and timing services. This makes GNSS the primary application domain for the usage of atomic clocks.

The Telecommunications (5G/6G synchronization) segment is projected to achieve the highest growth rate during 2026–2035.

By End User, Government & Defense Agencies segment dominates the Atomic Clock Market, Telecom Operators segment expected to grow fastest

In 2025, the Government & Defense Agencies segment maintained the highest end-user share of 40.24% in the Atomic Clock Market. The cause for this domination lies in the heavy use of atomic clocks in military navigations, communications, missiles, radar, and satellite defense. These defense departments are very dependent on precise timing for accurate operations and protection against any kind of jamming of their GPS signals, thus, forming the largest user base for atomic clock technology.

The Telecom Operators segment is projected to register the highest growth rate during 2026–2035.

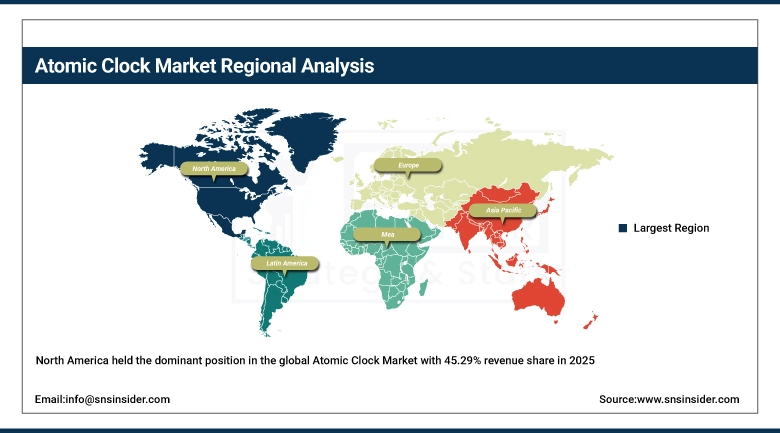

Atomic Clock Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

45.29% |

|

Europe |

Germany |

25.31% |

|

Asia Pacific |

China |

20.49% |

|

Middle East & Africa |

UAE |

4.87% |

|

Latin America |

Brazil |

4.04% |

North America Atomic Clock Market Insights

North America held the dominant position in the global Atomic Clock Market with 45.29% revenue share in 2025, supported by its well-developed GNSS infrastructure, robust defense navigation network, and early implementation of timing technologies. The sector is aided by its vast use of atomic clocks in GPS, satellite communications, and 5G/6G synchronization networks, as well as integration of rubidium and cesium-based timing solutions. North America is expected to dominate the regional market, backed by GPS upgrade initiatives, substantial investment in defense, and widespread usage of atomic timing in secure communication and navigation systems.

Supporting this dominance, the National Institute of Standards and Technology (NIST) continues to advance ultra-precise timekeeping research, including optical atomic clock development and next-generation frequency standards, strengthening North America’s leadership in global timing infrastructure.

Additionally, ongoing investments in GPS III and GPS IIIF modernization programs, expansion of satellite-based navigation services, and increasing adoption of atomic clock synchronization in high-frequency trading and data center operations are further reinforcing regional demand for high-stability timing solutions across multiple industries.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Atomic Clock Market Insights

The Asia Pacific region is projected to register the highest CAGR of 7.54% from 2026–2035, The driving forces behind this trend include the fast-growing satellite navigation system market, rapid development of telecom infrastructure, and investments in military modernization projects. China, India, Japan, and South Korea have been identified as major players in this sector, with their domestic GNSS satellite navigation systems, including BeiDou and NavIC, experiencing substantial development and depending largely on atomic clocks installed aboard spacecrafts.

Supporting this growth, national space and defense agencies such as China National Space Administration (CNSA) and the Indian Space Research Organisation (ISRO) are expanding satellite constellations and next-generation navigation capabilities, significantly increasing demand for high-stability atomic timekeeping systems. Regulatory and infrastructure initiatives supporting 5G/6G rollout across the region are further driving adoption of atomic clock-based synchronization in telecom networks and data centers.

In addition, rapid growth in aerospace manufacturing, increasing UAV deployment, and rising participation of regional players in global satellite programs are accelerating integration of chip-scale and rubidium atomic clocks across both defense and commercial applications.

Europe Atomic Clock Market Insights

In 2025, Europe had a considerable stake in the international market because of the strength of their satellite navigation programs, their well-developed aerospace industry, and good infrastructure for precision timekeeping research. For instance, nations like Germany, France, the UK, and Switzerland have been major users of atomic clocks because of their participation in the Galileo satellite navigation system.

Supporting this position, the European Space Agency (ESA) and national metrology institutes such as PTB (Germany) are actively advancing next-generation optical atomic clock research and space-based time synchronization systems, enhancing Europe’s leadership in precision timing innovation. The European Union’s continued investment in secure navigation and resilient timing infrastructure is also strengthening adoption across defense and telecom sectors.

Additionally, expansion of 5G network synchronization requirements, growing demand for GPS-independent timing systems, and increasing use of atomic clocks in financial trading and scientific applications are reinforcing Europe’s role as a stable but innovation-driven regional market.

Latin America, Middle East & Africa (LAMEA) Atomic Clock Market Insights

It is evident that there has been consistent growth in the Atomic Clocks market in LAMEA owing to the slow but continuous rise in satellite navigation usage, increased defense upgrades, and growing telecom infrastructure development investments. Some of the nations that have shown prominence in the Atomic Clock Market include Brazil, Mexico, South Africa, Saudi Arabia, and UAE.

Governments in the Middle East are actively investing in advanced aerospace and defense programs, including satellite navigation initiatives and smart infrastructure development, which is increasing the adoption of atomic clock-based timing systems for secure communication and positioning accuracy.

In addition, increasing collaboration with global aerospace and defense companies, along with gradual expansion of 5G infrastructure and satellite-based services, is improving access to high-precision timing technologies across emerging markets, supporting long-term adoption of atomic clock systems in the region.

Atomic Clock Market Growth Drivers:

-

Rising reliance on atomic clock-based precision timing in GNSS, telecommunications, and defense systems is driving strong global adoption of ultra-stable synchronization technologies across critical infrastructure networks

The major structural driver in the Atomic Clock Market comes from the growing reliance on accurate time synchronization in the global navigation satellite systems like GPS, Galileo, BeiDou, and NavIC, 5G and 6G telecom networks, aircraft, and military communications systems, where a few nanoseconds' difference in the timing can cause major impacts on the accuracy of location detection and overall system performance. With the increasing complexity of today's digital architecture, atomic clocks have become an essential part of ensuring continuous and highly accurate timekeeping.

Additionally, large-scale global infrastructure initiatives such as GPS III modernization in the United States, Galileo expansion in Europe, BeiDou enhancement in China, and NavIC scaling in India are significantly increasing onboard atomic clock deployment in satellite constellations.

At the same time, rising investment in 5G/6G network densification and GPS-independent, anti-jamming defense navigation systems is accelerating the integration of rubidium, cesium, and chip-scale atomic clocks across telecom, aerospace, and military ecosystems worldwide.

Atomic Clock Market Restraints:

-

High dependence on ultra-precise calibration, complex infrastructure integration, and high-cost deployment of atomic clock systems is limiting scalability across cost-sensitive commercial applications

In the Atomic Clock Market, the main limiting factor is the high level of technological complexity and the high cost involved in manufacturing atomic frequency standards, which necessitate precise calibration, control of environmental factors, and special equipment, such as vacuum systems, lasers, and oscillators. The incorporation of atomic clocks in Global Navigation Satellite Systems (GNSS) satellites, telecommunication facilities, military applications, and aerospace technologies also requires extensive coordination within complex systems, making validation lengthy and costly.

Atomic Clock Market Opportunities:

-

Expansion of global precision navigation, next-generation satellite constellations, and ultra-low latency digital infrastructure is creating strong opportunities for advanced atomic clock deployment across critical timing-dependent systems

The most important opportunity in the Atomic Clock Market is the rapid development of the GNSS systems of tomorrow, the 5G/6G telecommunications network, and the space-based navigation system, where accurate time synchronization is crucial. The complexity of digital networks, which include autonomous systems, smart defense systems, high-frequency trading, and even edge computing, necessitates a stable timekeeping system that transcends mere GPS dependency. Moreover, the invention of optical atomic clocks and CSACs presents opportunities for new avenues of business that will allow for highly accurate, low-energy consumption, and extremely small atomic clock devices, thus making them appropriate for use in aviation, UAVs, autonomous systems, and telecommunication networks.

Recent Developments:

-

2026: U.S. Department of Defense (DoD) advanced deployment of GPS-independent timing systems across defense communication and navigation platforms, integrating next-generation rubidium and chip-scale atomic clocks to strengthen resilience against jamming and spoofing in contested environments.

-

2026: European Space Agency (ESA) expanded its Galileo modernization program with enhanced onboard atomic clock integration, improving satellite navigation accuracy and supporting next-generation space-based timing synchronization infrastructure across Europe.

-

2025: National Institute of Standards and Technology (NIST) progressed optical atomic clock research programs, demonstrating significantly higher time stability benchmarks that are expected to redefine global time standards and future precision metrology systems.

-

2025: China National Space Administration (CNSA) enhanced BeiDou satellite constellation capabilities with upgraded high-precision atomic clocks, strengthening global positioning accuracy and expanding timing services for commercial and defense navigation applications.

Atomic Clock Market Key Players

Some of the Atomic Clock Market Companies

-

Microchip Technology Inc. (Microsemi)

-

Safran Electronics & Defense

-

Orolia (Safran Positioning Technologies)

-

AccuBeat Ltd.

-

Oscilloquartz (ADVA / Adtran Timing)

-

Stanford Research Systems

-

Excelitas Technologies Corp.

-

IQD Frequency Products (Würth Elektronik)

-

VREMYA-CH JSC

-

SpectraDynamics Inc.

-

Fei-Zyfer Inc.

-

Trimble Inc.

-

Keysight Technologies

-

Thales Group

-

Leonardo S.p.A.

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

Raytheon Technologies (RTX)

-

Honeywell International Inc.

-

General Atomics

Atomic Clock Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.62 Billion |

| Market Size by 2035 | USD 1.13 Billion |

| CAGR | CAGR of 6.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Type (Cesium Atomic Clocks, Rubidium Atomic Clocks, Hydrogen Maser Clocks, Optical Atomic Clocks, Chip-Scale Atomic Clocks (CSAC)) By Platform (Ground-Based Systems, Space-Based Systems (satellites/GNSS), Airborne Platforms, Portable & Embedded Systems (CSAC-based devices)) By Application (GNSS & Navigation Systems (GPS, Galileo, BeiDou, NavIC), Telecommunications (5G/6G synchronization), Aerospace & Defense Systems (radar, missile guidance, satellites), Scientific Research & Metrology (time standards, labs), Financial Systems (high-frequency trading), Space & Deep-Space Communication) By End User (Government & Defense Agencies, Telecom Operators, Aerospace & Space Organizations, Research Institutes & National Laboratories, Financial Institutions) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microchip Technology Inc. (Microsemi), Safran Electronics & Defense, Orolia (Safran Positioning Technologies), AccuBeat Ltd., Oscilloquartz (ADVA / Adtran Timing), Stanford Research Systems, Excelitas Technologies Corp., IQD Frequency Products (Würth Elektronik), VREMYA-CH JSC, SpectraDynamics Inc., Fei-Zyfer Inc., Trimble Inc., Keysight Technologies, Thales Group, Leonardo S.p.A., Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies (RTX), Honeywell International Inc., General Atomics |

Frequently Asked Questions

North America dominated the Atomic Clock Market in 2025.

The Rubidium Atomic Clocks segment dominated the Atomic Clock Market in 2025.

Rapid expansion of GNSS, 5G/6G telecom networks, and defense navigation systems is the primary growth driver of the Atomic Clock Market.

The Atomic Clock Market was valued at USD 0.62 billion in 2025.

The Atomic Clock Market is expected to grow at a CAGR of 6.22% from 2026 to 2035.

Get in Touch