Chemotherapy Market Report Scope & Overview:

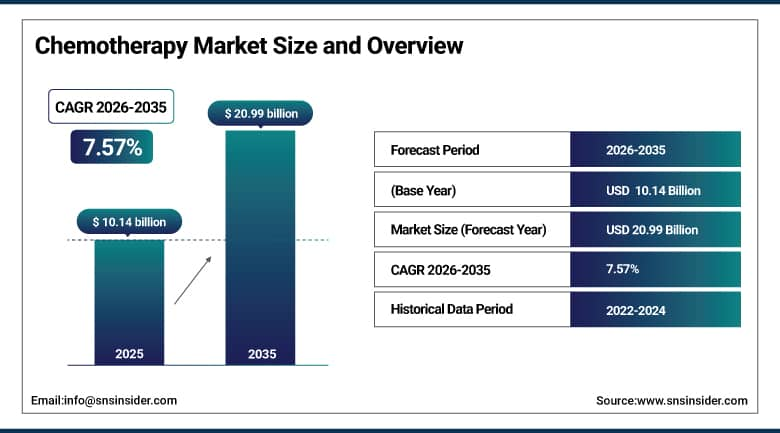

The Chemotherapy Market Size is valued at USD 10.14 Billion in 2025 and is projected to reach USD 20.99 Billion by 2035, growing at a CAGR of 7.57% during the forecast period 2026–2035.

The Chemotherapy Market analysis report offers a comprehensive overview of the growth opportunities in the oncology treatment and cancer care market. Factors that are contributing to market growth in this sector include a high prevalence of cancer, improved chemotherapy formulations, hospital infrastructure, and the increasing use of targeted therapy.

Chemotherapy usage exceeded 10 billion treatment doses in 2025, driven by rising cancer incidence and growing adoption of advanced oncology therapies.

Market Size and Forecast:

-

Market Size in 2025: USD 10.14 Billion

-

Market Size by 2035: USD 20.99 Billion

-

CAGR: 7.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Chemotherapy Market - Request Free Sample Report

Chemotherapy Market Trends:

-

Rising cancer prevalence and early diagnosis initiatives are accelerating demand for chemotherapy treatments.

-

Integration of targeted therapies and combination regimens is expanding chemotherapy’s effectiveness across multiple cancer types.

-

Growing investment in advanced drug formulations and personalized oncology solutions is enhancing treatment precision and patient outcomes.

-

Expansion of hospital networks, oncology centers, and home care services is improving accessibility and treatment delivery.

-

Clinical research and real-world evidence supporting efficacy and safety are strengthening physician confidence and market adoption.

-

Increasing focus on supportive care and combination with immunotherapy is boosting overall treatment adoption and patient quality of life.

U.S. Chemotherapy Market Insights:

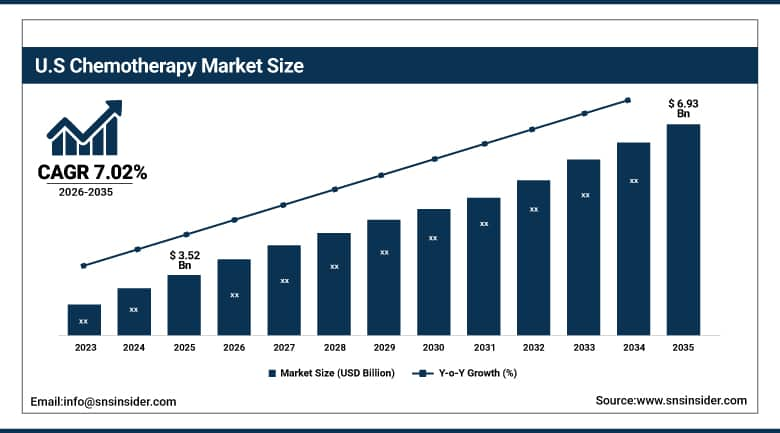

The U.S. Chemotherapy Market is projected to grow from USD 3.52 Billion in 2025 to USD 6.93 Billion by 2035, at a CAGR of 7.02%. The growth is driven by the factors such as increasing prevalence of cancer, well-developed healthcare infrastructure, rising penetration of targeted and combination therapies, significant presence of the cancer centers, constant investment toward research and development activities along with the availability of innovative therapy options in hospitals and facilities.

Chemotherapy Market Growth Drivers:

-

Increasing cancer prevalence and adoption of advanced oncology therapies significantly driving chemotherapy market growth.

One of the major growth drivers in the Chemotherapy Market is the rise in the prevalence of cancer, along with the increasing rate of adoption of advanced cancer treatment methodologies. As the healthcare industry and patients seek the most effective cancer treatment methodologies, the demand for chemotherapy drugs also increases. New advancements in cancer treatment methodologies are increasing the efficacy of cancer treatment, thereby boosting the overall growth of the Chemotherapy Market.

Over 65% of cancer patients received chemotherapy treatments in 2025, driven by rising cancer prevalence and adoption of advanced oncology therapies.

Chemotherapy Market Restraints:

-

Severe side effects and high treatment costs are limiting widespread adoption of chemotherapy therapies.

The most significant restraint in the Chemotherapy Market is the high incidence rate of severe side effects, which in turn raises the cost of the treatment. Chemotherapy is known to induce nausea, fatigue, suppression of the immune system, and long-term health consequences. Therefore, this acts as a restraint in the growth of the market, as the high incidence rate of severe side effects acts as a barrier to the growth of the market.

Chemotherapy Market Opportunities:

-

Growing investment in targeted therapies and personalized oncology solutions is creating new growth opportunities in chemotherapy.

The Chemotherapy Market is likely to experience a major opportunity with the increased investments in targeted therapies and personalized oncology products. This is due to pharmaceutical companies are now coming up with precision chemotherapy products and combinations that are more effective and safer for patients based on their profiles. This is attributed to the increased demand for effective therapies and survival rates in cancer patients. This has led to increased collaborations and innovations in the market.

Over 42% of new oncology treatment protocols in 2025 integrated targeted or personalized chemotherapy regimens, driving market growth and adoption.

Chemotherapy Market Segmentation Analysis:

-

By Drug Type, Antimetabolites held the largest market share of 28.45% in 2025, while Topoisomerase Inhibitors are expected to grow at the fastest CAGR of 8.92% during 2026–2035.

-

By Route of Administration, Intravenous segment accounted for the highest market share of 61.37% in 2025, while Oral administration is projected to register the fastest CAGR of 9.14% through 2026–2035.

-

By Cancer Indication, Lung Cancer dominated with a 24.18% market share in 2025, whereas Blood Cancer is anticipated to grow at the fastest CAGR of 8.76% during the forecast period.

-

By Distribution Channel, Hospital Pharmacies captured the highest market share of 57.21% in 2025, while Online Pharmacies are projected to grow at the fastest CAGR of 10.12% during the forecast period.

-

By End User, Hospitals & Clinics held the largest share of 52.63% in 2025, while Home Care is expected to expand at the fastest CAGR of 9.38% through 2026–2035.

By End User, Hospitals & Clinics Dominated While Home Care Is Fastest Growing:

Hospitals & Clinics segment dominated the market owing to their advanced infrastructure, numerous skilled oncology professionals present there and ability to manage complex chemotherapy procedures in controlled environments. In 2025, more than 9 million chemotherapy procedures were performed in hospitals, which remained the leading provider.

Home Care is the fastest-growing segment, driven by increasing demand for home-based treatment options, lower hospitalization costs and growth of home infusion services. Advancements in portable drug delivery systems and remote patient monitoring technologies drove home-based chemotherapy cases to over 1.5 million by 2025.

By Drug Type, Antimetabolites Dominated While Topoisomerase Inhibitors Are Fastest Growing:

Antimetabolites segment dominated the market owing to their wide applicability across multiple cancer types, and their ability to impair DNA and RNA synthesis. Their widespread use in first-line treatment regimens confirms that they already represent a quality standard of care. Antimetabolite-based therapies were used in over 5 million treatment courses in 2025.

Topoisomerase Inhibitors are the fastest-growing segment, owing to targeted oncology drugs and combinations. By 2025, their use soared beyond 2 million administrations as the practice of medicine moved toward more accurate and effective treatments that helped patients achieve better outcomes.

By Route of Administration, Intravenous Dominated While Oral Is Fastest Growing:

Intravenous segment dominated the market as it allows direct and controlled administration of a drug into the bloodstream, which ensures rapid action with high bioavailability. It remains the most common delivery method for complex chemotherapy regimens in hospitals and oncology centers. There were more than 8 million intravenous procedures in 2025.

Oral is the fastest-growing segment owing to growing patient preference toward convenience, decreasing dependency on hospitals for treatment and home-based treatment. In 2025, over 3 million oral chemotherapy prescriptions were written following continued advances in drug formulations and increasing adoption of patient-centric care models.

By Cancer Indication, Lung Cancer Dominated While Blood Cancer Is Fastest Growing:

Lung Cancer segment dominated the market owing to high prevalence and major dependence on chemotherapy as a first-line treatment method. It accounts for a sizable portion of oncology therapies across hospitals and specialty centers. Lung cancer chemotherapy treatments reached over 4 million cycles in 2025, demonstrating its high demand.

Blood Cancer is the fastest-growing segment, attributed to increasing cases of leukemia, lymphoma, and multiple myeloma, and improved diagnosis and survival rates. In 2025, blood cancer treatments had exceeded 2.5 million sessions for blood cancers due to dependence on chemotherapy in hematological malignancies and long-term care protocols.

By Function / Health Benefit, Stress & Anxiety Relief Dominated While Cognitive / Brain Health Is Fastest Growing:

Stress & Anxiety Relief segment dominated the market in 2025 due to increasing stress levels and growing demand for natural adaptogenic solutions. The numbers came about Ashwagandha use-cases health management with more than 430 million ashwagandha products consumed for stress management specifically.

Cognitive / Brain Health is the fastest growing segment, with a better understanding of its benefits in relation to mental performance, focus and memory. By 2025, there were products targeting younger student and professional consumers and aging populations that will be focused on brain health alone over more than 120 million unit sales.

Regional Analysis:

North America Chemotherapy Market Insights:

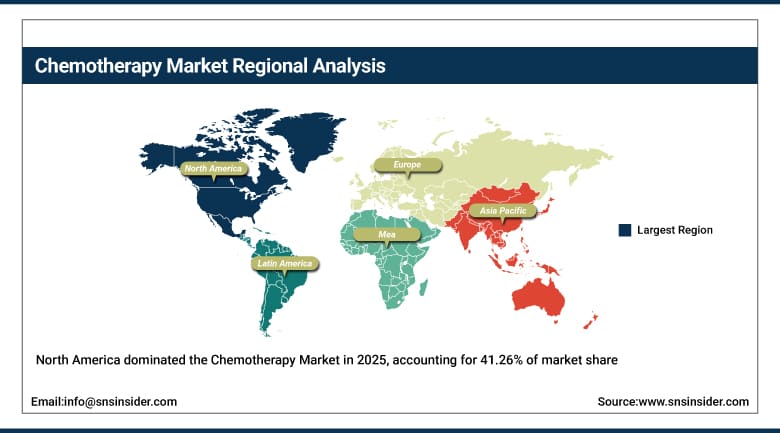

North America dominated the Chemotherapy Market with a market share of 41.26%, backed by a high incidence rate of cancer cases and strong healthcare infrastructure. The region has widespread availability of specialized cancer treatment centers, strong reimbursement systems, and high adoption rates for innovative treatment regimens. The presence of prominent pharmaceutical companies and research activities is also driving growth in this market. In addition, increasing trends in targeted therapy, combination therapy, early diagnosis campaigns, and advanced drug delivery systems are further adding to the region’s strong hold in chemotherapy adoption and treatment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Chemotherapy Market Insights:

The U.S. Chemotherapy Market is driven by the presence of well-advanced healthcare infrastructure, the prevalence of cancer, and the adoption of cutting-edge cancer therapies. Additionally, the presence of major pharmaceutical companies and clinical research provides a boost to the market’s expansion. Moreover, favorable reimbursement policies and early diagnosis initiatives are also contributing factors.

Asia-Pacific Chemotherapy Market Insights:

The Asia-Pacific Chemotherapy Market is the fastest-growing regional segment, projected to expand at a CAGR of 9.36% during the forecast period. Factors including increasing cancer incidences, advancements in healthcare infrastructure and availability of cancer therapies in developing markets such as India and China works to the growth of the market. Higher investments in hospitals & centers and better awareness about early diagnosis are encouraging adoption. Additionally, huge patient base, rising healthcare expenditure coupled with higher adoption of advance chemotherapy regimens and combination therapies in countries including Asia Pacific are further propelling the market growth.

India Chemotherapy Market Insights:

The India Chemotherapy Market is driven by a high cancer burden, rising healthcare infrastructure, and improving access to oncology treatments. This is further backed by increasing awareness of early detection, government initiatives in healthcare, and improving affordability of cancer treatments. Presence of oncology centers, rising hospital beds, and improving chemotherapy regimens are also contributing factors for India in the Asia-Pacific market.

Europe Chemotherapy Market Insights:

Europe is a prominent Chemotherapy Market region, supported by an advanced healthcare infrastructure and heavy focus on oncology service. A few of the major factors driving the market include increasing incidence rates, rising usage of advanced chemotherapy techniques and availability of specialized treatment centers. Insulin is first given in the hospital until blood glucose levels stabilize. Further, growing interest in developing novel drugs, increasing usage of combination chemotherapy, and availability of precision oncology services are also helping the market grow in the region.

Germany Chemotherapy Market Insights:

The Germany Chemotherapy Market is supported by a robust healthcare infrastructure, a well-equipped oncology environment, and a high adoption of modern therapeutic approaches. Increasing incidence of cancer cases, government support for healthcare services, and comprehensive insurance plans drive the adoption of therapies. Steadily rising clinical research activity, well-equipped cancer centers, and increasing adoption of targeted and combination chemotherapy support the market.

Latin America Chemotherapy Market Insights:

The Latin America Chemotherapy Market is growing due to the increasing rate of cancer prevalence, improvements in healthcare infrastructure, and availability of cancer therapy in countries such as Brazil, Mexico, and Argentina. Increasing awareness of early diagnosis, government initiatives in healthcare, improvements in hospital infrastructure, and gradual improvements in reimbursement systems are boosting the adoption of advanced chemotherapy regimens in this region.

Middle East and Africa Chemotherapy Market Insights:

The Middle East & Africa Chemotherapy Market is driven by factors which includes increase in cancer prevalence rates, improvements in healthcare infrastructure, and access to oncology treatments in regions such as UAE, Saudi Arabia, and South Africa. It is also fueled by government initiatives in healthcare, an increase in the number of hospitals, and a rise in early detection and advanced chemotherapy treatments.

Competitive Landscape:

F. Hoffmann-La Roche Ltd. is a Swiss multinational healthcare company is focused in oncology, diagnostics and personalized medicine. To complement this, it has continued to innovate in the design of chemotherapeutic drugs and targeted biologics providing them a dominant position in the chemotherapy market. By providing integrated diagnostics and therapeutics, Roche can ensure precision treatment selection to optimise outcomes. Its substantial investment in R&D, effective distribution network and partnerships has consolidated its leadership as a key player oncology and chemotherapy.

-

In January 2025, F. Hoffmann-La Roche Ltd. received approval for Itovebi (inavolisib) for advanced breast cancer. This launch strengthens its oncology portfolio, expands targeted chemotherapy combinations, and reinforces Roche’s leadership by addressing resistant cancer types and enhancing precision-based treatment approaches.

Novartis AG is a pharmaceutical leader headquartered in Switzerland, with a best at developing drugs in oncology and chemotherapy. The company is developing next-generation cancer therapies by combining these with targeted and precision medicine. Novartis continues to dominate with its robust research landscape, strategic purchases, and a strong oncology drug pipeline. With its broad-reaching pipeline, ongoing innovation, and focus on high-value specialty medicines, it has extended its leadership in both the chemotherapy and broader cancer treatment market.

-

In November 2025, Novartis AG supported the commercial rollout of its radioligand therapy Pluvicto through expanded manufacturing and supply. This development improves accessibility to advanced cancer treatments, strengthens its oncology pipeline, and reinforces Novartis’ position in next-generation chemotherapy alternatives and precision oncology markets.

Pfizer Inc. is a leading U.S.-based biopharmaceutical company that has a diversified oncology portfolio ranging from chemotherapy drugs to sophisticated cancer therapies. Extensive R&D, manufacturing capabilities, and partnerships have made the company leader. Pfizer is heavily involved in proprietary and clinical development of drugs for cancer. It has become a reference for the chemotherapy market owing to its good market access, brand recognition and consistent local introduction of effective oncology solutions, well contributing to making advances in cancer care.

-

In February 2026, Pfizer Inc. received full FDA approval for BRAFTOVI in combination with chemotherapy for metastatic colorectal cancer. This approval enhances treatment outcomes, expands Pfizer’s oncology portfolio, and reinforces its dominance in chemotherapy-based combination therapies and targeted cancer treatment markets.

Chemotherapy Market Key Players:

-

F. Hoffmann-La Roche Ltd.

-

Novartis AG

-

Pfizer Inc.

-

Merck & Co., Inc.

-

Johnson & Johnson Services, Inc.

-

Eli Lilly and Company

-

GlaxoSmithKline plc

-

Sanofi SA

-

Bristol-Myers Squibb Company

-

Bayer AG

-

AstraZeneca Pharmaceuticals

-

Takeda Pharmaceutical Company Limited

-

Amgen Inc.

-

Celgene Corporation

-

Almatic Pharma LLC

-

Puma Biotechnology Inc.

-

Clovis Oncology Inc.

-

Gilead Sciences Inc.

-

Biogen Inc.

-

Teva Pharmaceutical Industries Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.14 Billion |

| Market Size by 2035 | USD 20.99 Billion |

| CAGR | CAGR of 7.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Alkylating Agents, Antimetabolites, Anti-tumor Antibiotics, Topoisomerase Inhibitors, Mitotic Inhibitors, Others) • By Route of Administration (Intravenous, Oral, Subcutaneous, Intramuscular, Intraperitoneal, Intrathecal / Intraventricular, Topical) • By Cancer Indication (Breast Cancer, Lung Cancer, Colorectal Cancer, Blood Cancer, Prostate Cancer, Ovarian Cancer, Stomach & Other Cancers) • By End User (Hospitals & Clinics, Oncology Centers, Pharmacies, Home Care) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F. Hoffmann-La Roche Ltd., Novartis AG, Pfizer Inc., Merck & Co., Inc., Johnson & Johnson Services, Inc., Eli Lilly and Company, GlaxoSmithKline plc, Sanofi SA, Bristol-Myers Squibb Company, Bayer AG, AstraZeneca Pharmaceuticals, Takeda Pharmaceutical Company Limited, Amgen Inc., Celgene Corporation, Almatic Pharma LLC, Puma Biotechnology Inc., Clovis Oncology Inc., Gilead Sciences Inc., Biogen Inc., Teva Pharmaceutical Industries Ltd. |

Frequently Asked Questions

The Chemotherapy Market is projected to grow at a CAGR of 7.57% during 2026–2035.

The market is valued at USD 10.14 Billion in 2025 and is projected to reach USD 20.99 Billion by 2035.

Growth is driven by rising cancer cases, adoption of advanced combination therapies, expanding oncology infrastructure, and increasing R&D investment.

By Drug Type, Antimetabolites dominated with a 28.45% share, while Topoisomerase Inhibitors are projected to grow at the fastest CAGR of 8.92% during 2026–2035.

North America dominated with a 41.26% share in 2025, while Asia-Pacific is the fastest-growing region, projected to expand at a CAGR of 9.36% during 2026–2035.

Get in Touch