Electrical Resistor Market Report Scope & Overview:

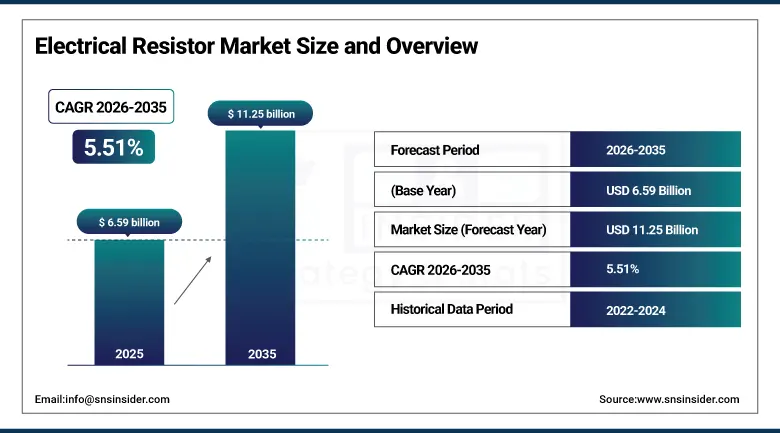

The Electrical Resistor Market was valued at USD 6.59 Billion in 2025 and is expected to reach USD 11.25 Billion by 2035, growing at a CAGR of 5.51% from 2026–2035.

The global electrical resistor market is advancing as the foundational passive component that limits, measures, or divides electrical current across virtually every electronic circuit in existence, creating an omnipresent demand base whose breadth spans consumer smartphones to industrial motor drives, automotive battery management systems, telecommunications infrastructure, and renewable energy power converters. Resistor technology is diversifying from traditional carbon composition and wire wound formulations toward precision thin-film and foil resistors whose temperature coefficient stability, noise performance, and miniaturization capabilities serve the demanding specifications of electric vehicle power management, 5G network infrastructure, and IoT sensing applications. Rising adoption in EV battery current sensing, ADAS radar systems, and smart energy metre electronics collectively sustains above-average commercial growth.

In December 2024, Vishay Intertechnology expanded its precision thin-film MELF resistor portfolio, introducing new case sizes with low temperature coefficient of resistance, tight tolerance, and resistance values extending to 10 MΩ for high-precision signal conditioning, medical instrumentation, and aerospace electronics applications. The portfolio expansion addressed the growing demand from automotive and industrial designers for precision resistors combining miniaturized surface-mount form factors with the stability and accuracy previously available only in larger through-hole precision component packages.

Market Size and Forecast

-

Market Size in 2026E: USD 6.95 Billion

-

Market Size by 2035: USD 11.25 Billion

-

CAGR: 5.51% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Electrical Resistor Market - Request Free Sample Report

Electrical Resistor Market Trends

-

EV battery management system shunt resistors for current sensing are driving growing demand for precision low-resistance foil and wirewound resistors.

-

5G base station power amplifier and antenna switching circuits are creating growing demand for high-frequency thin-film chip resistors with tight tolerances.

-

Miniaturization to 01005 and 0201 chip resistor case sizes is enabling denser PCB assembly in wearables, hearables, and compact IoT node designs.

-

Variable resistor integration in smart home lighting, audio processing, and sensor calibration systems is sustaining above-average potentiometer market growth.

-

Renewable energy inverter and solar panel junction box resistor content per installation is growing with global renewable capacity addition rates.

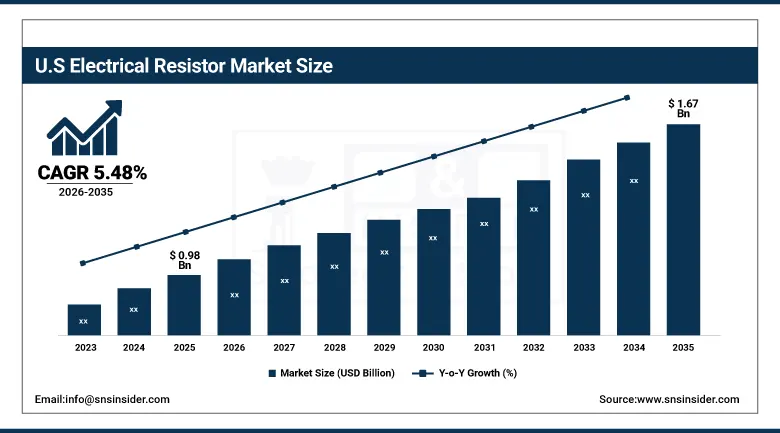

The U.S. Electrical Resistor Market Outlook

The U.S. Electrical Resistor Market was valued at approximately USD 0.98 Billion in 2025 and is expected to reach approximately USD 1.67 Billion by 2035, growing at a CAGR of approximately 5.48%.

The United States sustains a premium-specification resistor demand base through its aerospace and defense electronics procurement, advanced automotive electronics development, and industrial power electronics manufacturing. Vishay Intertechnology and Ohmite Manufacturing sustain U.S. market leadership through precision resistor technology for military, medical, and aerospace applications. The CHIPS Act’s domestic semiconductor manufacturing investment is creating new domestic electronics fabrication infrastructure whose PCB assembly requires systematic resistor procurement at scales that sustain above-market domestic demand growth.

In December 2024, YAGEO Corporation launched its PU1216 and PU2726 high-precision four-terminal shunt resistors targeting applications requiring stable low resistance measurement and high reliability, including EV battery current monitoring and industrial power electronics. The four-terminal Kelvin connection design eliminates contact resistance errors that conventional two-terminal shunt resistors introduce at the milliohm resistance values that EV battery current sensing requires, demonstrating the growing commercial sophistication of resistor specifications driven by electric vehicle powertrain electronics.

Electrical Resistor Market Segment Analysis

-

By Type, fixed resistors segment dominated the electrical resistor market with the largest share in 2025, while variable resistors are the fastest growing type driven by automation, smart home, and EV application adoption.

-

By Technology, thick-film segment dominated the electrical resistor market with the largest share in 2025 due to its cost efficiency in high-volume consumer electronics, while thin-film is the fastest growing at approximately 7.2% CAGR.

-

By Product, power supplies segment dominated the electrical resistor market with approximately 34.6% share in 2025, while electric motors are the fastest growing product application driven by industrial automation and EV motor controller demand.

-

By End Use, consumer electronics segment dominated the electrical resistor market with the largest share in 2025, while power generation is the fastest growing end use driven by renewable energy inverter and grid management electronics adoption.

By Type, fixed resistors dominate, variable resistors grow fastest

Fixed resistors retained the dominant type position with the largest share of the electrical resistor market in 2025. Their commercial primacy reflects the structural reality that fixed resistance values serve the overwhelming majority of circuit design requirements across consumer electronics, industrial control, automotive, telecommunications, and power management applications whose signal conditioning, voltage division, current limiting, and bias setting functions each require a specific resistance value that remains constant throughout the product’s operational lifetime. The annual production of fixed chip resistors exceeds one trillion units globally, concentrated in the 0402, 0201, and 0603 case sizes that dominate consumer electronics PCB assembly, creating a commercial scale that variable resistors cannot approach despite their above-average growth trajectory.

Variable resistors are growing fastest because the systematic expansion of adjustable control functions in smart home systems, industrial automation controllers, audio processing equipment, and EV battery management creates growing demand for potentiometers, rheostats, and digital potentiometers whose adjustable resistance enables user-configurable or software-controlled circuit parameter setting. Each new smart home device whose user interface incorporates rotary or slider control, each audio product whose tone and volume control requires analogue adjustment, and each industrial process controller whose setpoint calibration requires adjustable resistance creates variable resistor procurement above the baseline consumer electronics fixed resistor consumption volume.

By End Use, consumer electronics dominates, power generation grows fastest

Consumer electronics retained the dominant end use position with the largest share of the electrical resistor market in 2025. Smartphones, laptops, tablets, wearables, smart speakers, and gaming devices collectively represent the highest aggregate annual resistor consumption category, where the combination of extremely high annual production volumes exceeding four billion smartphones and laptops combined and the progressive density increase of PCB designs requiring more resistors per device creates a commercial base that no individual competing end use sector approaches. Each new generation of consumer electronics product whose performance advancement requires additional signal processing, power management, and sensing circuitry creates proportional increases in per-device resistor count that sustain revenue growth above unit shipment volume growth rates.

Power generation is the fastest-growing end use because the global renewable energy capacity addition programme, where over 400 GW of solar and wind capacity is being added annually, creates resistor demand in inverter power electronics, grid-tie protection circuits, and energy storage system battery management electronics whose per-MW installed capacity resistor content creates commercial procurement that scales directly with renewable energy investment. Solar panel junction box bypass diode protection resistors, grid inverter voltage divider networks, and smart metre power measurement shunt resistors collectively create a growing renewable energy infrastructure resistor demand whose commercial momentum reinforces with each year of above-trend renewable investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

52.4% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

43.8% |

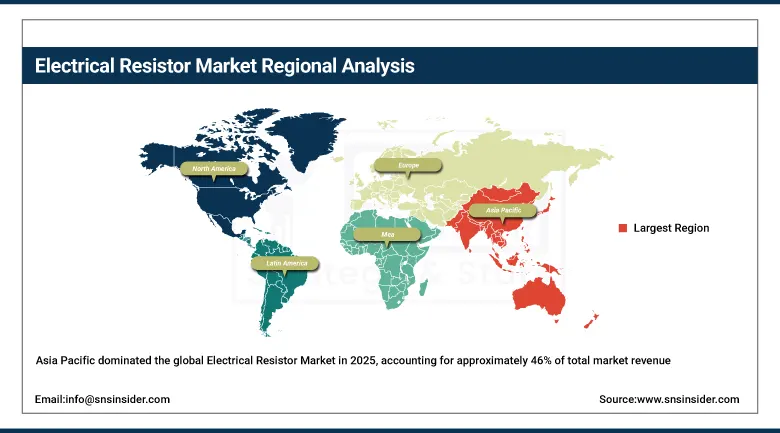

Asia Pacific Electrical Resistor Market Insights

Asia Pacific dominated the global Electrical Resistor Market in 2025, accounting for approximately 46% of total market revenue. This is driven by its concentration of consumer electronics manufacturing in China, Japan, South Korea, and Taiwan whose PCB assembly operations represent the world’s highest resistor consumption density. China accounts for approximately 52.4% of Asia Pacific revenues as the world’s largest electronics assembly hub whose smartphone, laptop, IoT device, and home appliance production collectively creates the highest national resistor procurement volume globally. Yageo, Walsin Technology, and Cyntec’s Taiwan-headquartered operations and Rohm, KOA, and Murata’s Japanese manufacturing sustain Asia Pacific’s leadership in both resistor production and market consumption.

South Korea’s Samsung Electro-Mechanics and LG Innotek contribute premium regional demand through their electronic component development, while India’s growing electronics manufacturing sector under the Production Linked Incentive scheme is progressively creating new domestic resistor procurement demand as smartphone and consumer electronics assembly investment increases. Southeast Asian electronics assembly operations in Vietnam, Malaysia, and Thailand sustain growing resistor consumption as production migrates from higher-cost Chinese coastal manufacturing to lower-cost ASEAN alternative locations.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Electrical Resistor Market Insights

North America sustained a significant electrical resistor market share in 2025 through its premium aerospace and defense electronics procurement, advanced automotive electronics development at North American OEM and Tier 1 supplier facilities, and industrial power electronics manufacturing whose precision specification requirements sustain above-commodity pricing for domestic resistor supply. The United States accounts for approximately 82.5% of North American revenues through Vishay Intertechnology’s global precision resistor leadership, the defense sector’s MIL-SPEC resistor procurement, and the semiconductor equipment industry’s precision resistor demand.

Canada contributes supplementary North American revenues through its growing clean technology manufacturing sector’s power electronics resistor demand, the telecommunications equipment industry’s 5G infrastructure deployment creating resistor procurement, and the resource extraction sector’s industrial motor drive and power management electronics whose operating environment requirements specify ruggedized wire wound and thick-film resistor configurations not found in standard consumer electronics.

Europe Electrical Resistor Market Insights

Europe is a technically sophisticated electrical resistor market where automotive electronics leadership, industrial automation equipment manufacturing, and precision instrumentation create consistent demand for high-specification resistor products whose performance requirements exceed standard consumer electronics equivalents. Germany accounts for approximately 24.6% of European revenues through its automotive industry’s ADAS and EV power management resistor procurement at Bosch, Continental, and Infineon, the industrial automation sector’s Siemens and Beckhoff electronics procurement, and the specialized scientific instrument industry’s precision resistor demand.

Switzerland’s medical device and precision instrument sector, the United Kingdom’s aerospace and defense electronics, and France’s energy sector instrumentation create premium secondary European market demand whose specification intensity sustains European resistor manufacturer investment in precision product development. Isabellenhutte’s German precision shunt resistor manufacturing and Bourns’ European operations sustain regional supply chain depth for demanding automotive and industrial applications.

MEA & Latin America Electrical Resistor Market Insights

Israel leads MEA revenues through its advanced defense electronics and semiconductor sectors’ precision resistor procurement, whose military and aerospace specification requirements create above-commodity demand density relative to regional GDP. The UAE’s growing electronics manufacturing and smart city infrastructure investment create expanding regional demand alongside Saudi Arabia’s Vision 2030 industrial diversification and technology infrastructure investment.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its consumer electronics assembly sector, the automotive industry’s growing vehicle electronics content, and the growing renewable energy sector’s power conversion electronics whose inverter and charge controller PCB assembly creates resistor demand. Mexico’s large electronics manufacturing export sector’s near-shoring expansion for the North American market creates growing resistor procurement aligned with automotive and industrial electronics assembly investment.

Market Dynamics

Growth Drivers: Electric vehicle electronics content expansion and 5G infrastructure deployment creating above-baseline resistor demand growth across premium application categories

The electrical resistor market’s most commercially significant structural growth driver is the electric vehicle revolution whose battery management system, motor controller, onboard charger, and ADAS electronics collectively represent substantially higher resistor content per vehicle than conventional internal combustion engine automobiles. Each EV battery management system’s current sensing shunt resistors, voltage divider networks, and balancing circuit components represent precision foil and wire wound resistor specifications whose per-unit value substantially exceeds the commodity thick-film resistors they replace in equivalent conventional vehicle electronics. 5G infrastructure deployment’s base station power amplifier and beamforming antenna circuit requirements create growing demand for high-frequency thin-film chip resistors whose superior signal integrity at millimeter wave frequencies and tight impedance matching tolerances sustain premium pricing above commodity market averages.

Restraints: Commoditization pressure on standard chip resistor pricing and raw material supply concentration creating margin and availability risks

The commodity chip resistor market’s intense pricing competition among Asian manufacturers whose high-volume thick-film 0402 and 0201 resistor production creates progressive average selling price decline that limits revenue growth from volume expansion alone in the standard consumer electronics resistor segment. Resistor paste raw material supply chain concentration for ruthenium oxide thick-film conductor paste and tantalum thin-film deposition materials creates procurement risk whose supply constraint manifestation creates manufacturing cost increases that high-volume producers’ thin margin structures cannot absorb without corresponding selling price increases that competitive market dynamics resist. Lead-free solder transition compliance and RoHS regulation across global electronics supply chains creates ongoing formulation investment that smaller resistor manufacturers whose R&D resources are limited find progressively burdensome.

Opportunities: Precision current sensing for EV and energy storage applications and high-power resistor development for industrial power electronics creating premium market expansion

The electric vehicle and stationary energy storage battery management market’s requirement for precision current sensing shunt resistors with milliohm resistance values, low temperature coefficient of resistance, and high power dissipation capability in compact surface-mount packages represents the most commercially attractive new precision resistor application category in recent decades. Each battery pack’s multiple current measurement points and cell voltage monitoring circuits create procurement for precision foil shunt resistors whose per-unit value of USD 2 to USD 10 substantially exceeds standard chip resistor commodity economics, creating a premium segment whose commercial scale grows directly with EV production volume.

Recent Developments:

-

2024: Vishay Intertechnology expanded its precision thin-film MELF resistor portfolio with new case sizes featuring low TCR, tight tolerance, and resistance values up to 10 MΩ, targeting high-precision signal conditioning, medical instrumentation, and aerospace electronics applications.

-

2024: YAGEO Corporation launched PU1216 and PU2726 four-terminal shunt resistors for EV battery current monitoring and industrial power electronics, featuring Kelvin connection design that eliminates contact resistance errors at milliohm measurement values.

-

2024: KOA Corporation introduced its WK73 series automotive-grade wirewound chip resistors for EV motor controller and power converter applications, providing AEC-Q200 qualification, high pulse load capability, and 5 W power ratings in standard 2512 surface-mount case size.

Electrical Resistor Market Key Players are:

-

Vishay Intertechnology Inc.

-

Yageo Corporation

-

Panasonic Holdings Corporation

-

KOA Corporation

-

Rohm Semiconductor GmbH

-

Murata Manufacturing Co. Ltd.

-

Bourns Inc.

-

Ohmite Manufacturing Company

-

Isabellenhutte Heusler GmbH

-

Susumu Co. Ltd.

-

Stackpole Electronics Inc.

-

TT Electronics PLC (IRC Advanced Film Division)

-

Caddock Electronics Inc.

-

Riedon Inc.

-

AVX Corporation (Kyocera AVX)

-

Walsin Technology Corporation

-

Kamaya Electric Co. Ltd.

-

Thin Film Technology Corp.

-

Cyntec Co. Ltd.

-

Viking Tech Corporation

Electrical Resistor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.59 Billion |

| Market Size by 2035 | USD 11.25 Billion |

| CAGR | CAGR of 5.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fixed Resistors, Variable Resistors) • By Technology (Thin-Film, Thick-Film, Wire-Wound, Foil, Others) • By Product (Power Supplies, Electric Motors, Inverters & Converters, Lighting, Consumer Electronics, Others) • By End Use (Consumer Electronics, Automotive, Industrial, Telecommunications, Aerospace & Defense, Power Generation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Vishay Intertechnology Inc., Yageo Corporation, Panasonic Holdings Corporation, KOA Corporation, Rohm Semiconductor GmbH, Murata Manufacturing Co. Ltd., Bourns Inc., Ohmite Manufacturing Company, Isabellenhütte Heusler GmbH, Susumu Co. Ltd., Stackpole Electronics Inc., TT Electronics PLC (IRC Advanced Film Division), Caddock Electronics Inc., Riedon Inc., AVX Corporation (Kyocera AVX), Walsin Technology Corporation, Kamaya Electric Co. Ltd., Thin Film Technology Corp., Cyntec Co. Ltd., and Viking Tech Corporation |

Frequently Asked Questions

The Electrical Resistor Market was valued at USD 6.59 Billion in 2025.

Electric vehicle power management and battery current sensing creating precision resistor demand, 5G infrastructure deployment requiring high-frequency thin-film resistors, and renewable energy inverter electronics expanding power resistor adoption are the primary growth factors.

Asia Pacific dominated the Electrical Resistor Market in 2025.

Get in Touch