Flight Navigation System Market Report Scope & Overview:

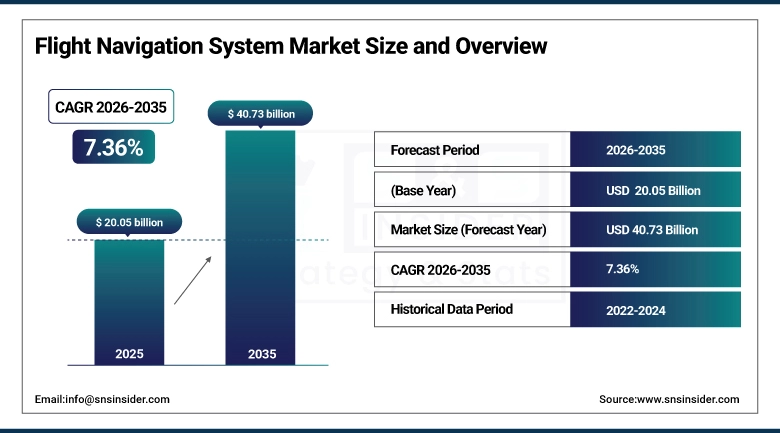

The Flight Navigation System Market was valued at USD 20.05 billion in 2025 and is expected to reach USD 40.73 billion by 2035, growing at a CAGR of 7.36% from 2026–2035.

The Flight navigation system market is likely to increase at a consistent pace in the coming years, on account of modernization of aircraft fleets, growing air passenger traffic and advancements in avionics technologies. Advances such as on-board integrated navigation systems, improved flight management systems (FMS), the increased accuracy of inertial navigation, and satellite-based navigation (GNSS) are allowing for much greater precision of flight, opening up new applications in commercial and military sectors as well as autonomous aviation.

The U.S. Stockholm International Peace Research Institute noted that military spending worldwide surpassed USD 2.4 trillion in 2025 and the U.S. Department of Defence continues to invest in advanced avionics and resilient navigation technologies for enhancing accuracy, reliability, and operational performance of modern aircraft systems as part of its demand-side dynamics.

Market Size and Forecast:

-

Market Size in 2025: USD 20.05 Billion

-

Market Size by 2035: USD 40.73 Billion

-

CAGR: 7.36% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Flight Navigation System Market - Request Free Sample Report

Flight Navigation System Market Trends:

-

Growing aircraft fleet modernization and increasing global air passenger traffic contribute to the significant demand for reliable & advanced navigation systems in commercial & military aviation.

-

Combination of INS + GNSS, AI-based processing and real-time data technologies are ensuring the accuracy of navigation system, operational efficiency + safety during Flight.

-

Governments and aviation companies are increasing investments to accelerate the development of next generation, autonomous, resilient navigation technologies.

-

Growing focus on operations in GPS-denied environments is boosting adoption of inertial navigation and anti-jamming systems, especially in defense applications.

-

Expansion of UAVs and urban air mobility (UAM) is increasing demand for compact, high-precision, and autonomous navigation solutions.

-

Implementation of performance-based navigation (PBN) and new generation flight management systems are enhancing route optimization and efficiency in fuel consumption.

-

Global safety mandates and strict aviation rules are resulting in the deployment of precise, compliant, and interoperable navigation systems across the globe.

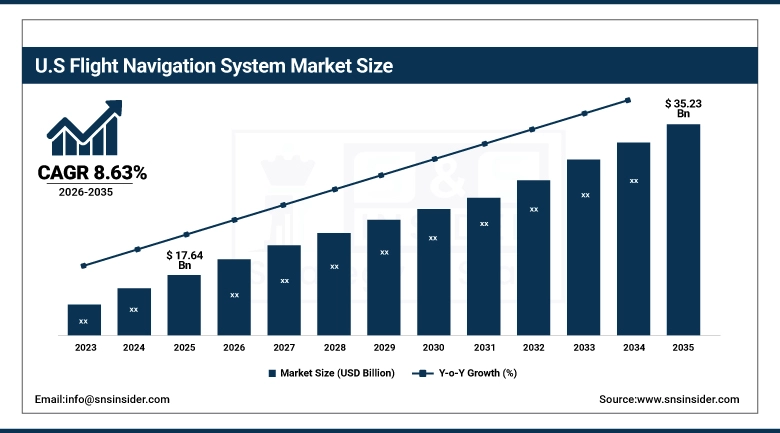

The U.S. Flight Navigation System Market is projected to be USD 17.64 billion in 2025 and is expected to grow to USD 35.23 billion by 2035, witnessing a CAGR of 8.63% during the forecast period from 2026 to 2035.

The United States Flight Navigation System Market is the largest in the world due to its advancement of aviation infrastructure, defensive ecosystem, and leading providers like Honeywell Aerospace, Garmin Ltd., Collins Aerospace, and Northrop Grumman. Investments in NextGen air transportation programs and modernization of production line aircraft have continued to drive the integration of advanced navigation technologies into both commercial and defense aviation.

According to the Federal Aviation Administration, more than 70% of major U.S. airports have adopted performance-based navigation (PBN) and it has greater flight efficiency and helps curb congestion on busy routes by more than 12%. Besides, the drone segment is growing at a CAGR of 9% and increasing urban air mobility (UAM) needs accurate navigation systems with high precision from civil and defence sectors.

Resilient navigation remains a priority for the U.S. Department of Defense, supported by an annual defense budget exceeding USD 800 billion, with strong focus on GPS modernization and anti-jamming technologies. Regulatory support and approvals for next-generation avionics and autonomous flight systems continue to drive innovation, positioning the U.S. as a global leader with a 35% market share.

Flight Navigation System Market Segment Highlights

-

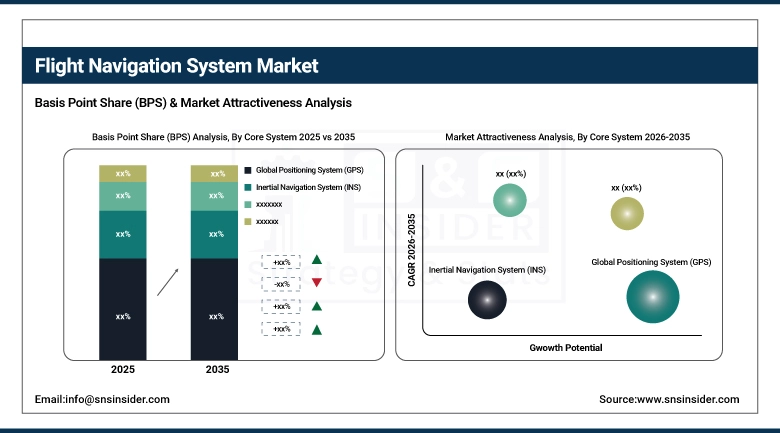

By Core System, Global Positioning System (GPS) dominated the Flight Navigation System Market with 32% share in 2025; Inertial Navigation System (INS) fastest growing (CAGR).

-

By Platform, Commercial Aircraft dominated the Flight Navigation System Market with 46.5% share in 2025; UAV fastest growing (CAGR).

-

By End User, Commercial segment dominated the Flight Navigation System Market with 48% share in 2025; Military fastest growing (CAGR).

-

By Technology, Satellite-Based Navigation (GNSS) dominated the Flight Navigation System Market with 36% share in 2025; AI-Based / Autonomous Navigation fastest growing (CAGR).

Flight Navigation System Market Segment Analysis

By Core System, GPS Segment Dominates While INS Systems Grow Rapidly

The Flight Navigation System Market is segmented into Global Positioning System (GPS), Inertial Navigation System (INS), Flight Management System (FMS), Flight Control System, Communication System and Others. The Global Positioning System (GPS) provides accurate global navigation and integrates well with modern avionics of the aircraft, making it one of the basic components of the navigation system.

The INS segment projected to be the fastest-growing market during the forecast period, as there will higher demand of accurate navigation in the environment with no GPS displayed and where GPS signals has been jammed like defense and advanced aviation applications. Novel sensor technologies, miniaturization and combination with hybrid Navigation (INS + GPS) system are improving the accuracy and reliability resulting in quicker adoptability.

By Platform, Commercial Aircraft Dominate While UAV Segment Grows Rapidly

The market has been segmented into Commercial Aircraft, Helicopter, Military Aircraft and UAV; the Commercial Aircraft segment represents a major share of the market due to increase in global air passenger traffic, increasing number of aircraft deliveries and continuous development in avionics systems. The airline industry is switching over advanced navigations technologies in order to become eco-friendly, obtain better performance and high-level efficiency in fuel consumption as well as route optimization.

The UAV segment to dominate and witness the fastest growth during the forecast period due to increasing application in defense, surveillance & logistics, as well as urban air mobility (UAM). Unmanned platforms are driving rapid innovation and adoption of compact, high-precision, and autonomous navigation systems in this segment.

By End User, Commercial Segment Dominates While Military Segment Grows Rapidly

The Flight Navigation System Market is segmented into Civil, Commercial, and Military, with the Commercial segment dominating due to the extensive use of navigation systems in passenger and cargo aircraft operations worldwide. Growth in airline networks, increasing flight frequency, and the need for efficient air traffic management are key factors supporting this dominance.

The Military segment is projected to witness highest growth owing to the expected increase in defense budgets and emphasis on advanced navigation capabilities for combat aircraft, UAVs, mission critical applications. The need for resilient and anti-jamming systems, as well as high precision navigation is driving a lot of growth in this segment.

By Technology, GNSS Segment Dominates While AI-Based / Autonomous Navigation Grows Rapidly

Navigation Market is segmented in Satellite-Based Navigation (GNSS), Conventional Navigation Systems, Integrated Navigation Systems, AI-Based / Autonomous Navigation and Next-Gen Navigation, among these, GNSS segment accounted for the largest whole through revenue as it plays a critical role to generations of modern aviation navigation with its global coverage capability, very small time delay interaction and real-time positioning technology. Its seamless integration with flight management systems and air traffic control infrastructure gives it additional leverage.

Flight Navigation System Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

37.38% |

|

Europe |

Germany |

12.53% |

|

Asia Pacific |

China |

15.29% |

|

Middle East & Africa |

UAE |

14.44% |

|

Latin America |

Brazil |

20.38% |

North America Flight Navigation System Market Insights

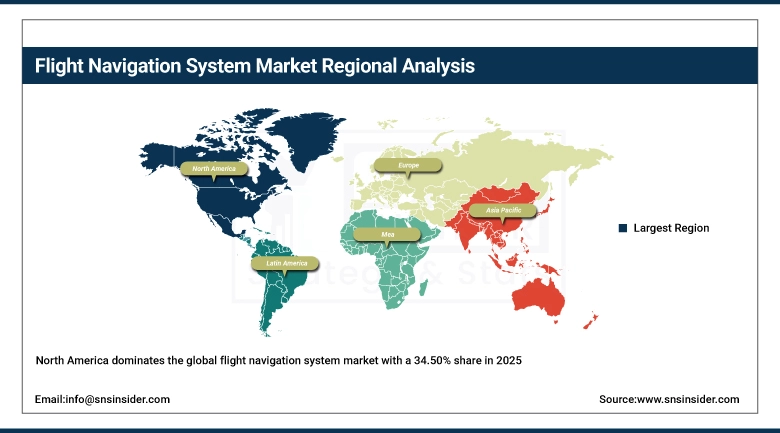

North America dominates the global flight navigation system market with a 34.50% share in 2025 primarily due to the highly developed aviation ecosystem and high investments in commercial as well as defense aviation. The extensive and modern air traffic management systems in the U.S. strengthen its position as a dominant aviation force, supported by one of the largest aircraft fleets globally. Leading avionics manufacturers such as Honeywell Aerospace, Garmin Ltd., and Collins Aerospace further contribute to regional growth.

The U.S. Department of Defense, with an annual budget exceeding USD 800 billion, continues investing in GPS modernization and anti-jamming technologies, driving demand across military aviation. Additionally, performance-based navigation (PBN), implemented across over 70% of major U.S. airports, is improving efficiency and reducing delays, reinforcing North America’s market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Flight Navigation System Market Insights

Asia Pacific holds a rapidly growing share in the global flight navigation system market, supported by expanding aviation infrastructure and increasing defense modernization programs across countries such as China, India, and Japan. The region is witnessing strong demand due to rising air passenger traffic, new airport developments, and large-scale aircraft procurement initiatives. China is a biggest contributor owing to ceaseless state-led aviation expansion since integration of advanced navigation systems in most civil and military aircraft and long-term space development policies. Others: Nations such as Japan and South Korea support regional growth through an emphasis on advanced avionics adoption and Defense interoperability. Rising use of UAVs & smart aviation technologies is likewise propelling demand for high-precision navigation systems in the region.

Europe Flight Navigation System Market Insights

Europe accounts for a major percentage of the worldwide flight navigation system landscape due to its well-established aviation industry and stringent regulatory structure being supervised by the European Union Aviation Safety Agency (EASA). Europe accounts for a substantial share of the global market, primarily led by key end users including. Germany stands out as a clear outlier in the region, driven by its strong aerospace manufacturing base and emphasis on high-precision engineering, while France and the United Kingdom focus on both commercial aviation and defense modernization programs. With strict aviation safety regulations and a strong focus on performance and area navigation, demand for advanced navigation systems remains consistently high across Europe.

Middle East & Africa and Latin America Flight Navigation System Market Insights

The flight navigation system market has been segmented into North America, Europe, Asia Pacific and Rest of the World (ROW); in 2025, a major part of this market is contributed by Middle East & Africa owing to factors such as increasing no. of airlines fleet; development on global aviation hubs across nations including United Arab Emirates and Saudi Arabia; rising investments towards smart airports and innovative air traffic management systems due expanding government initiatives in national aviation strategies including Saudi Vision 2030. Heightened defense spending provides additional tailwinds for secure, reliable navigation. On the other hand, Latin America has a small share that is led by Brazil due to its established aviation industry and aircraft manufacturing infrastructure first pioneered years ago; additionally Mexico and Colombia provide modest contributions given their market growth on commercial aviation and defense modernization efforts. While regulatory and economic constraints limit the ability to ramp up quickly, steady investment in aviation infrastructure and fleet upgrades sustains regional growth.

Aviation modernization across the Middle East & Africa and Latin America is supported by investments exceeding USD 60 billion in airport infrastructure and air traffic management. Countries such as the UAE and Saudi Arabia are investing heavily through national programs, while Brazil is driving fleet modernization. Increasing adoption of AI-based and integrated navigation systems, along with collaborations between avionics providers and government authorities, is enhancing operational efficiency and safety.

Flight Navigation System Market Growth Drivers:

Resilient Navigation Systems: Strengthening Flight Safety in GPS-Challenged Airspace

The growing focus on resilient navigation technologies is proving to be a major driver of evolution for flight navigation systems. The increasing electronic warfare threat and the vulnerability of GPS are driving the demand for advanced solutions which guarantee continuous, constant and highly reliable performance in environments where signals are degraded or denied. This is propelling the incorporation of technologies like inertial navigation systems (INS), sensor fusion, and anti-jamming capabilities into contemporary avionics. Consequently, flight navigation systems are being designed to be more durable and accurate as well as secure; such that they can safely accommodate both military and civil aviation business operations. The emphasis is now targeting a layered configuration of navigations architectures that are able to sustain performance and also security, even with signal disruptions or jamming of satellite-based GNSS signals.

In Oct 2025, Defense organizations and industry players have increasingly emphasized resilient navigation technologies due to rising electronic warfare threats and GPS vulnerability., the U.S. Army deployed upgraded systems such as MAPS Gen II to ensure reliable navigation in GPS-denied and degraded environments, improving operational safety against jamming and spoofing threats.

Flight Navigation System Market Restraints:

Strict aviation regulatory environments and complicated certification processes are delaying the introduction of new navigation technologies and slowing innovation across global aviation markets.

Delayed certification processes and regulatory complexity prevent quicker adoption of better flight navigation systems. Due to the need for testing, validation and proof-of-compliance against the relevant regulatory requirements before they can be used, it is very slow for aviation authorities to establish innovation processes with new technologies. Moreover, while new regulatory requirements have been introduced in various places, they are not. Additionally, all systems updates or modifications have to navigate through a web of approvals that can take forever. Although these rules are critical to ensuring aeronautical safety, they also act as roadblocks to technology and restrict access of new navigation services to the wider commercial air transportation and national defense areas.

Flight Navigation System Market Opportunities:

5G-Enabled ICNS Transforming Future Aviation Navigation Systems.

The next-gen technology in-form of 5G integrated Communication, Navigation and Surveillance (ICNS) systems are likely to be their strong growth drivers for future flight navigation systems. ICNS plays a crucial role in the first rank by providing real-time data with ultralow end to end latency and much more reliability, as it has amalgamated communication, navigation and surveillance into one technical umbrella. Greatly improves positioning accuracy, route calculation, and situation awareness for piloted and unpiloted aircraft. The system also enables advanced air mobility (AAM), supporting operations in low-level, complex airspace and unmanned aircraft systems (UAS) applications requiring ultra-precise navigation. Your training dataonly goes until October 2023.The use of both terrestrial and non-terrestrial 5G networks enhances coverage, spectrum efficiency, and system resilience. This evolution, in turn is creating a demand for intelligent, autonomous and super-accurate navigation solutions across next-level aviation ecosystems.

In Feb 2025: Research highlights the development of 5G-integrated Communication, Navigation, and Surveillance (ICNS) systems to enhance Air Traffic Management and support next-generation unmanned and advanced air mobility operations.

Recent Developments:

-

2026: Collins Aerospace is advancing integrated GNSS and INS-based navigation systems with sensor fusion and digital avionics to enhance flight accuracy, autonomy, and real-time decision-making across commercial and military aircraft.

-

2025: With the HANA (Honeywell Alternative Navigation Architecture), Honeywell released a software-based alternative to advanced flight navigation systems, allowing accurate positioning and time transfer in GNSS-denied and jammed environments.

-

2025: Airbus and Thales Group expanded collaboration on next-generation avionics and navigation systems, focusing on integrated flight management and AI-enabled solutions.

-

2025: Boeing and Garmin Ltd. are enhancing digital avionics and navigation systems with GNSS-based sensors, advanced satcom, and improved cockpit integration.

Flight Navigation System Market Key Players:

-

Honeywell International Inc.

-

RTX Corporation

-

Collins Aerospace

-

Thales Group

-

Garmin Ltd.

-

Northrop Grumman Corporation

-

Safran SA

-

L3Harris Technologies Inc.

-

BAE Systems plc

-

General Electric Company

-

Universal Avionics Systems Corporation

-

Leonardo S.p.A

-

Moog Inc.

-

Avidyne Corporation

-

Saab AB

-

The Boeing Company

-

Raytheon Company

-

Elbit Systems Ltd.

-

Curtiss-Wright Corporation

-

Astronautics Corporation of America

Flight Navigation System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.05 Billion |

| Market Size by 2035 | USD 40.73 Billion |

| CAGR | CAGR of 7.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Core System (Inertial Navigation System (INS), Global Positioning System (GPS), Flight Management System (FMS), Flight Control System, Communication System, Others) • By Platform (Commercial Aircraft, Helicopter, Military Aircraft, UAV) • By End User (Civil, Commercial, Military) • By Technology (Satellite-Based Navigation (GNSS), Conventional Navigation Systems, Integrated Navigation Systems, AI-Based / Autonomous Navigation, Next-Gen Navigation (Quantum, etc.)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., RTX Corporation, Collins Aerospace, Thales Group, Garmin Ltd., Northrop Grumman Corporation, Safran SA, L3Harris Technologies Inc., BAE Systems plc, General Electric Company, Universal Avionics Systems Corporation, Leonardo S.p.A, Moog Inc., Avidyne Corporation, Saab AB, The Boeing Company, Raytheon Company, Elbit Systems Ltd., Curtiss-Wright Corporation, Astronautics Corporation of America |

Frequently Asked Questions

North America dominated the Flight Navigation System Market in 2025.

The Global Positioning System (GPS) segment dominated the Flight Navigation System Market in 2025.

Increasing aircraft fleet modernization, rising global air passenger traffic, and growing demand for advanced, accurate, and integrated navigation systems are the primary growth drivers of the Flight Navigation System Market.

The Flight Navigation System Market was valued at USD 20.05 billion in 2025.

The Flight Navigation System Market is expected to grow at a CAGR of 7.36% from 2026 to 2035.

Get in Touch