GEO Satellite Market Report Scope & Overview:

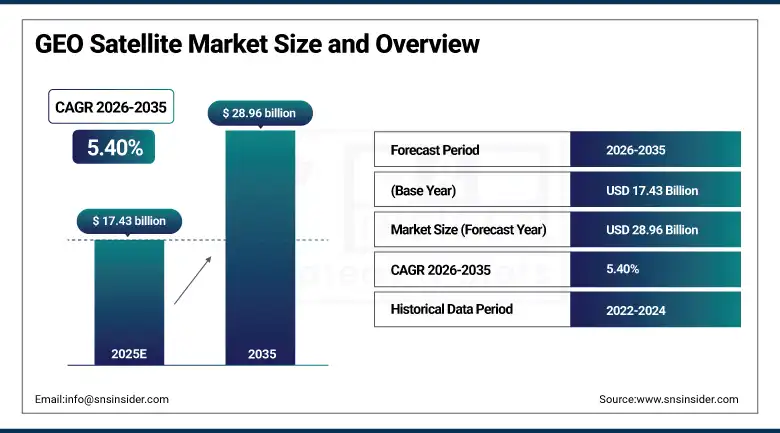

The GEO Satellite Market Size was valued at USD 17.43 billion in 2025 and is expected to reach USD 28.96 billion by 2035, growing at a CAGR of around 5.40% from 2026–2035.

The GEO Satellite Market is witnessing a consistent level of change fueled by growing needs for seamless, high-bandwidth communication, secure military connectivity, and global broadcast systems. The use of High Throughput Satellites (HTS), software-defined payloads, and hybrid integration between GEO and LEO systems is greatly increasing the efficiency and flexibility of communications networks in commercial and governmental settings. Broadband connectivity in rural and developing areas, alongside increasing demand for communication services in the marine, aerospace, and corporate sector, is contributing to market stability amid the rise of LEO systems.

Supporting this trend, SES S.A. successfully launched and began early deployment integration of its next-generation O3b mPOWER high-throughput satellite system expansion in 2024–2025, significantly enhancing global broadband capacity and demonstrating the shift toward scalable GEO-adjacent and hybrid orbital communication systems. In parallel, Eutelsat Group’s completion of its merger with OneWeb (2023–2024 integration phase) has strengthened GEO–LEO hybrid service capabilities, enabling seamless connectivity solutions across multiple orbital layers for government, enterprise, and mobility applications.

Additionally, NASA and NOAA continued modernization of GEO weather satellite infrastructure through the GOES-R series operational upgrades in 2024, improving real-time Earth observation, climate monitoring, and disaster prediction accuracy, reinforcing the strategic importance of GEO-based meteorological systems.

GEO Satellite Market Size and Forecast

-

Market Size in 2025: USD 17.43 Billion

-

Market Size by 2035: USD 28.96 Billion

-

CAGR: 5.40% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On GEO Satellite Market - Request Free Sample Report

GEO Satellite Market Trends

-

Rising demand for high-throughput GEO satellites (HTS) is significantly improving bandwidth efficiency and enabling cost-effective global broadband and enterprise connectivity services.

-

Increasing adoption of software-defined GEO satellite architectures is enhancing in-orbit flexibility, allowing dynamic reconfiguration of coverage, capacity allocation, and service delivery.

-

Rapid integration of AI-enabled network management, beamforming, and predictive satellite operations systems is improving service reliability, spectrum optimization, and operational efficiency.

-

Growing demand for hybrid GEO–LEO satellite networks is expanding seamless global connectivity, reducing latency limitations, and improving service continuity across mobility and defense applications.

-

Increasing government and defense investments in secure satellite communication infrastructure is accelerating procurement of resilient GEO platforms for command, control, surveillance, and strategic communication.

-

Rising demand for multi-mission GEO satellites (communication + imaging + navigation capabilities) is expanding payload flexibility and improving mission efficiency across commercial and governmental end users.

-

Expanding deployment of electric propulsion and lifespan-extension technologies is improving satellite endurance, reducing replacement cycles, and lowering long-term operational costs.

U.S. GEO Satellite Market Size Outlook:

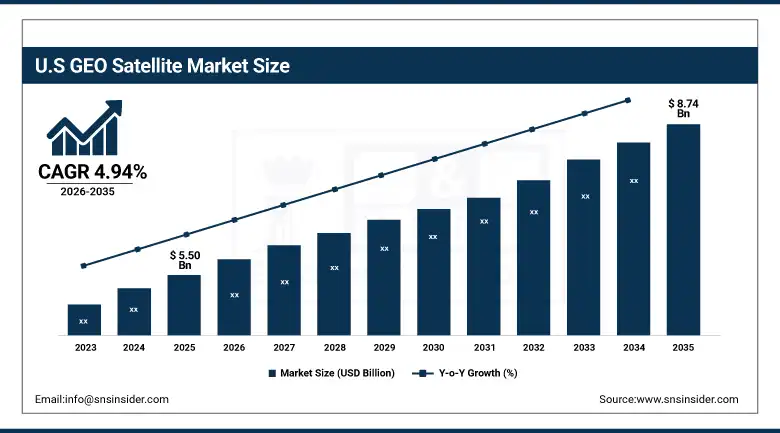

The U.S. GEO Satellite Market was valued at USD 5.50 billion in 2025 and is expected to reach USD 8.74 billion by 2035, growing at a CAGR of around 4.94% from 2026–2035. U.S. Market will maintain its position as the world's dominant market due to superior space infrastructure, military communications needs, and dominance of leading satellite companies including Lockheed Martin, Boeing, Northrop Grumman, and Viasat/Intelsat operational platforms. Continued high defense spending on satellite communications, missile detection, and secure space-based networks will bolster demand for GEO satellites.

Supporting this trend, SES successfully expanded its O3b mPOWER high-throughput satellite services in collaboration with U.S. enterprise and government users in 2024–2025, strengthening GEO–MEO hybrid connectivity for defense and maritime applications.

In addition, NASA and NOAA advanced the GOES-R Series GEO weather satellite program upgrades in 2024, improving real-time climate monitoring, hurricane tracking, and disaster response capabilities across the United States, reinforcing the strategic importance of GEO-based Earth observation infrastructure.

GEO Satellite Market Segment Highlights

-

By Application, Communication (Telecom, Broadband, DTH) dominated the GEO Satellite Market with 48.36% share in 2025, while Military & Defense Surveillance is the fastest-growing segment with a CAGR.

-

By Payload Type, Communication Payload dominated the market with 55.45% share in 2025, while Navigation Payload is the fastest-growing segment with a CAGR.

-

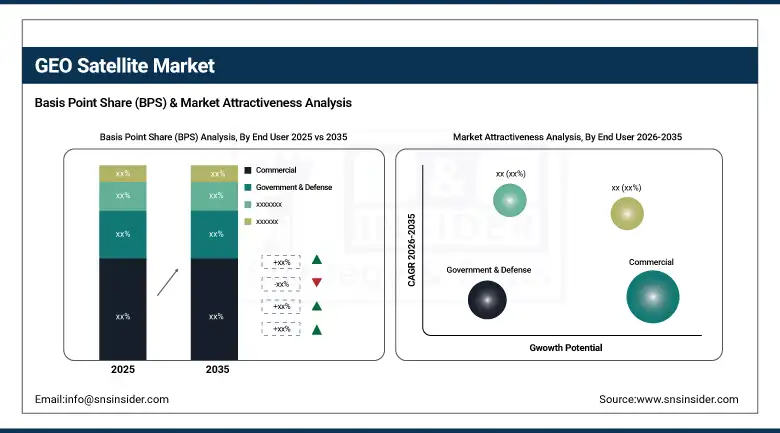

By End User, Commercial segment dominated the GEO Satellite Market with 52.85% share in 2025, while Government & Defense is the fastest-growing segment with a CAGR.

-

By Satellite Mass, Medium GEO Satellites dominated the market with 40.54% share in 2025, while Small GEO Satellites are the fastest-growing segment with a CAGR.

-

By Orbit Function, Traditional GEO Satellites dominated the market with 60.14% share in 2025, while Flexible / Software-Defined GEO Satellites are the fastest-growing segment with a CAGR.

By Application, Communication (Telecom, Broadband, DTH) segment dominates the GEO Satellite Market, Military & Defense Surveillance segment expected to grow fastest

The Communication (Telecom, Broadband, DTH) segment maintained its dominant position in the GEO Satellite Market, accounting for 48.36% of total revenue in 2025. The leadership of this type of satellite technology is attributed to the constant need for efficient satellite communications, direct-to-home television services, broadband services, and backbone communication systems in areas that lack connectivity. The use of GEO satellites in communication systems to provide efficient coverage and broadcast services has led to the dominance of this type of satellite technology.

The Military & Defense Surveillance application market is expected to grow at the fastest CAGR of 7.14% between 2026 and 2035. This growth will be due to the rising political tensions and modernization of defense communication systems.

By Payload Type, Communication Payload segment dominates the GEO Satellite Market, Navigation Payload segment expected to grow fastest

The Communication Payload segment held the largest share of 55.45% in 2025, Fuelled by widespread utilization of GEO satellites for broadband connections, broadcast transmissions, data transfers, and governmental communications. Constant need for greater bandwidth capability, higher spectral efficiency, and better coverage reliability has kept the Communication Payloads segment at the forefront of the GEO satellite industry.

The Navigation Payload segment is expected to grow at the highest CAGR during 2026–2035 due to increased demand for satellite-based augmentations and navigation services. Increased demand for navigation solutions in aviation, maritime, and defense applications and growing reliance on precise positioning data for future transportation and military applications is fuelling fast growth in navigation payloads on GEO satellites.

By End User, Commercial segment dominates the GEO Satellite Market, Government & Defense segment expected to grow fastest

The Commercial segment maintained the highest share of 52.85% in 2025, backed by the robust demand for satellite communications from telecom operators, broadcasters, ISPs, and other applications requiring enterprise connectivity solutions. Business organizations keep using GEO satellites for delivering bulk content broadcasting services, global broadband services, and integrating network solutions with the terrestrial and other non-geo satellites.

The Government & Defense segment is expected to witness the highest CAGR between 2026 and 2035, as there would be increasing investments in building satellite communication networks to strengthen security and enhance the capacity of conducting surveillance missions. There is an increasing focus on using satellites for the purpose of national security, disaster relief management, and strategic intelligence

By Satellite Mass, Large GEO Satellites segment dominates the GEO Satellite Market, Small GEO Satellites segment expected to grow fastest

The Large GEO Satellites segment maintained the highest share of 40.54% in 2025, due to their use in communication satellites used in high-capacity communication networks, broadcasting network and defense communications systems. These communication satellites can carry numerous high-power transponders and can also be used for wide-area coverage and can operate reliably over a long period of time. This is why they are considered ideal for both commercial and governmental space projects due to continuous improvement in their payload power ratio.

The Small GEO Satellites segment is projected to register the highest CAGR of during 2026–2035

By Orbit Function, Traditional GEO Satellites segment dominates the GEO Satellite Market, Flexible / Software-Defined GEO Satellites segment expected to grow fastest

The Traditional GEO Satellites segment held the dominant share of 60.14% in 2025, mainly because of its time-tested capabilities in providing broadcasting services, telecom backbones, and military communications. These satellites will remain predominant in use because of their proven reliability, stationary positions in orbit, and affordable coverage in fixed-service areas. Their deeply-rooted presence within the satellite communications framework will ensure their supremacy amid changing technologies.

The Flexible / Software-Defined GEO Satellites segment is expected to record the highest CAGR of during 2026–2035.

GEO Satellite Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

34.57% |

|

Europe |

Germany |

24.14% |

|

Asia Pacific |

China |

26.75% |

|

Middle East & Africa |

UAE |

8.04% |

|

Latin America |

Brazil |

6.50% |

North America GEO Satellite Market Insights

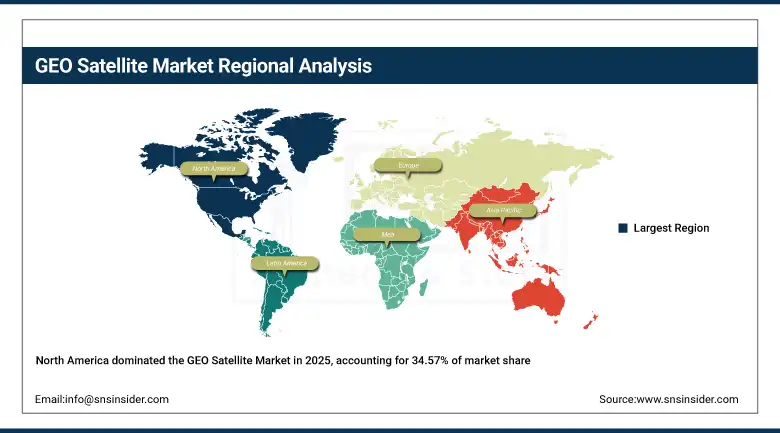

North America held the dominant position in the global GEO Satellite Market with 34.57% revenue share in 2025, motivated by the sophistication of its space infrastructure, dominance by top satellite firms, and massive demands for military communication systems. This area enjoys the presence of major players in the space industry like Lockheed Martin, Boeing, Northrop Grumman, and Viasat, as well as major commercial satellite companies like SES (US-based operations), Intelsat, and EchoStar. Constant need for security-oriented government communication networks, high-speed broadband communications, and enterprise-grade solutions enhances the supremacy of the region in the space market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the U.S. Department of Defense (DoD) has significantly expanded its investments in resilient satellite communications under programs such as Protected Tactical SATCOM (PTS) in 2024–2025, aimed at enhancing secure, jam-resistant GEO-based military communication networks.

In addition, NASA and NOAA continue modernization of the GOES-R series GEO weather satellites (ongoing 2024 upgrades), improving real-time Earth observation, disaster monitoring, and climate forecasting capabilities, reinforcing North America’s technological leadership in GEO satellite operations.

Asia Pacific GEO Satellite Market Insights

The Asia Pacific region is projected to register the highest CAGR of 6.32% during 2026–2035, in response to rapid growth in digital connectivity networks, greater satellite deployment initiatives, and higher requirements for broadband in far-flung areas. The main countries leading the market include China, India, Japan, and South Korea, with China contributing significantly because of its growing satellite communications network led by the state. High demand in maritime connectivity, aviation broadband services, and rural internet access is fast propelling the use of GEO satellites in the area.

Supporting this growth, China’s China Satellite Network Group (SatNet) continued accelerating its national satellite communication infrastructure rollout in 2024–2025, strengthening sovereign broadband and defense communication capabilities.

In addition, India’s ISRO successfully advanced its GSAT series expansion and initiated next-generation GSAT-20 (GSAT-N2) high-throughput satellite deployment in 2024, aimed at boosting broadband connectivity and supporting Digital India initiatives, reinforcing the region’s rapid GEO satellite expansion trajectory.

Europe GEO Satellite Market Insights

Europe held the second-largest share of the global GEO Satellite Market, supported by a mature space ecosystem, strong regulatory frameworks, and leading satellite operators such as SES S.A., Eutelsat Group, and Airbus Defence and Space. The region benefits from high adoption of GEO-based broadcasting, government communication services, and expanding demand for hybrid GEO–LEO connectivity solutions. Strong emphasis on space sustainability and digital sovereignty is also shaping long-term market growth.

Supporting this position, the European Space Agency (ESA) and Eutelsat successfully advanced the IRIS² secure satellite constellation program in 2024–2025, aimed at strengthening Europe’s sovereign satellite communication infrastructure.

Additionally, the EU’s Space Strategy for Security and Defence (updated in 2024) is accelerating investment in resilient satellite networks and next-generation GEO communication systems to enhance strategic autonomy and secure data transmission across member states.

Middle East & Africa and Latin America GEO Satellite Market Insights

The Middle East & Africa (MEA) and Latin America regions are witnessing steady growth in the GEO Satellite Market, driven by increasing investments in digital infrastructure, expanding telecom coverage, and rising demand for satellite-based connectivity in remote and underserved areas. In MEA, countries such as Saudi Arabia, UAE, and South Africa are leading adoption, supported by sovereign space initiatives and growing demand for secure defense communication systems.

Supporting this development, Saudi Arabia’s Saudi Space Commission advanced its national satellite communications strategy in 2024–2025, including expansion of GEO-based communication and Earth observation capabilities aligned with Vision 2030 digital transformation goals.

In Latin America, Brazil’s Telebras and national space agency (AEB) expanded GEO satellite-backed broadband programs in 2024, improving rural connectivity and public sector communication infrastructure, while also strengthening partnerships for regional satellite capacity leasing agreements.

GEO Satellite Market Growth Drivers:

-

Rising global demand for high-capacity, resilient, and always-on connectivity across defense, enterprise, aviation, maritime, and rural broadband sectors is driving sustained expansion of the GEO Satellite Market

The change in structure towards an interconnected global economy through digital means is the key driver behind the growth of the GEO Satellite Market. The importance of uninterrupted connectivity for essential functions like military communication, broadcasting, enterprise networking, and mobility services is elevating the significance of geostationary satellites. GEO satellite systems remain highly relevant because of their capacity to offer extensive coverage, uninterrupted signals, and large bandwidth capabilities, especially in areas where physical network infrastructures are either absent or financially impractical.

Supporting this trend, the U.S. Federal Communications Commission (FCC) Spectrum Frontiers framework and ongoing GEO–NGSO coordination policies (updated through 2024–2025) are actively enabling more efficient spectrum utilization for satellite broadband and reducing orbital interference, thereby improving GEO satellite operational efficiency.

In addition, the International Telecommunication Union (ITU) continues to allocate and regulate GEO orbital slots to ensure equitable global access to satellite resources, with increased filings observed in 2024–2025 driven by emerging markets expanding national satellite programs.

GEO Satellite Market Restraints:

-

High capital expenditure, limited launch affordability, and long development cycles associated with GEO satellite manufacturing, deployment, and orbital slot acquisition restraining rapid market expansion, particularly for emerging satellite operators and developing nations

The GEO Satellite Market has been highly restricted because of the very expensive initial capital requirements involved in developing, launching, and deploying a satellite into orbit along with the establishment of its ground segment components. The cost incurred on a single GEO satellite program ranges anywhere from hundreds of millions to billions of dollars, depending upon spacecraft and launch vehicle development costs, insurance premiums, and the integration of the satellite's ground segment. Another critical factor that hinders new participants from entering this market is the need for precise satellite orbital slot allocation.

GEO Satellite Market Opportunities:

-

Rapid expansion of digital satellite ecosystems driven by software-defined GEO platforms, AI-enabled network orchestration, and integrated multi-orbit connectivity creating strong new revenue opportunities across broadband, mobility, and defense communication markets

The biggest transformative possibility for the GEO Satellite Market is that of moving from conventional fixed-functionality satellites to a digital and software-enabled GEO architecture, which allows operators to allocate bandwidth, redefine the coverage footprint, and maximize spectral efficiency on an on-demand basis. This has opened up new opportunities for satellite companies to offer “capacity-as-a-service” offerings customized for enterprises, aviations, maritime, and governmental clients with fluctuating requirements.

Recent Developments:

-

2026: SES S.A. expanded its next-generation O3b mPOWER high-throughput satellite services globally, enhancing GEO–MEO hybrid connectivity capabilities for enterprise, maritime, and government users, with increased deployment across defense and mobility communication networks in North America and Europe.

-

2025: Eutelsat Group accelerated integration of its OneWeb low Earth orbit (LEO) assets with existing GEO infrastructure, advancing hybrid GEO–LEO service delivery models to support seamless global broadband connectivity for aviation, maritime, and remote enterprise customers across multiple regions.

-

2024: Intelsat successfully advanced its EpicNG high-throughput GEO satellite fleet optimization program, improving bandwidth efficiency and global coverage performance for commercial broadband, aviation connectivity, and media distribution services across transatlantic and Asia-Pacific routes.

-

2024: NASA and NOAA progressed modernization of the GOES-R series GEO weather satellite system, enhancing real-time Earth observation capabilities, severe weather forecasting accuracy, and disaster monitoring response through upgraded imaging sensors and advanced data transmission systems.

GEO Satellite Companies are:

-

SES S.A.

-

Intelsat

-

Eutelsat Group

-

Inmarsat (Viasat Inc.)

-

EchoStar Corporation

-

SKY Perfect JSAT Group

-

Arabsat (Arab Satellite Communications Organization)

-

Asia Satellite Telecommunications Co. Ltd. (AsiaSat)

-

Hispasat S.A.

-

Thaicom Public Company Limited

-

China Satellite Communications Co. Ltd. (China Satcom)

-

China Great Wall Industry Corporation (CGWIC)

-

Indian Space Research Organisation (ISRO)

-

Lockheed Martin Corporation

-

Boeing Defense, Space & Security

-

Northrop Grumman Corporation

-

Airbus Defence and Space

-

Thales Alenia Space

GEO Satellite Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.43 Billion |

| Market Size by 2035 | USD 28.96 Billion |

| CAGR | CAGR of 5.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Application (Communication, Broadcasting, Earth Observation & Meteorology, Military & Defense Surveillance, Navigation Augmentation Services) By Payload Type (Communication Payload, Imaging Payload, Navigation Payload, Scientific Payload) By End User (Commercial Operators, Government & Defense, Civil Organizations, Space Agencies) By Satellite Mass (Medium GEO Satellites, Small GEO Satellites, Large GEO Satellites) By Orbit Function (Traditional GEO Satellites, High-Throughput Satellites (HTS), Flexible / Software-Defined GEO Satellites) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SES S.A., Intelsat, Eutelsat Group, Telesat Corporation, Inmarsat (Viasat Inc.), EchoStar Corporation, SKY Perfect JSAT Group, Arabsat, AsiaSat, Hispasat, Avanti Communications, Thaicom Public Company Limited, China Satellite Communications Co. Ltd. (China Satcom), China Great Wall Industry Corporation (CGWIC), Indian Space Research Organisation (ISRO), Lockheed Martin Corporation, Boeing Defense, Space & Security, Northrop Grumman Corporation, Airbus Defence and Space, Thales Alenia Space |

Frequently Asked Questions

The GEO Satellite Market is expected to grow at a CAGR of 5.40% from 2026 to 2035.

The GEO Satellite Market was valued at USD 17.43 billion in 2025.

Rising global demand for continuous high-capacity connectivity, secure defense communications, and reliable broadcast and broadband services is the primary growth driver of the GEO Satellite Market.

The Communication (Telecom, Broadband, DTH) Application dominated the GEO Satellite Market in 2025.

North America dominated the GEO Satellite Market in 2025.

Get in Touch