Inspection Drones Market Report Scope & Overview:

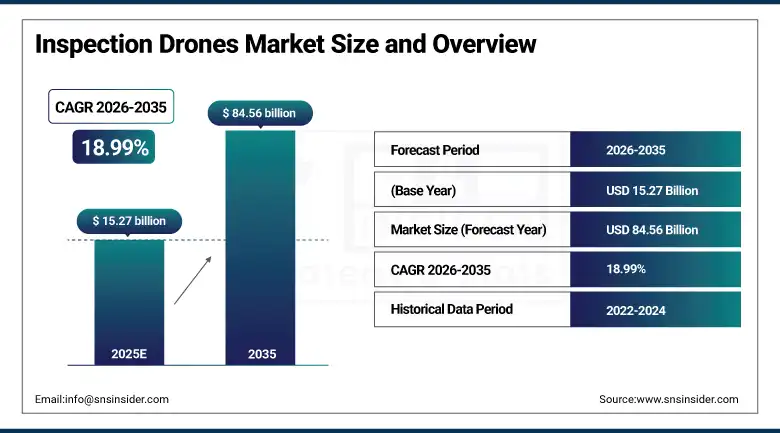

The Inspection Drones Market was valued at USD 15.27 billion in 2025 and is expected to reach USD 84.56 billion by 2035, growing at a CAGR of 18.99% from 2026–2035.

The Inspection Drones Market is experiencing strong growth driven by increasing demand for automated, cost-efficient, and safe asset inspection solutions across industries such as energy, infrastructure, oil & gas, mining, and telecommunications. In recent times, organizations are increasingly moving towards using inspection processes that involve drones in order to mitigate operational risks and improve the efficiency of inspection operations. The development of technology such as artificial intelligence analytics, advanced image resolution, LiDAR, thermal imagery sensors, and autonomous flight systems is greatly increasing the potential of inspection drones.

Supporting this trend, the International Energy Agency highlights the continued expansion of global energy infrastructure, including power grids and renewable assets such as wind and solar farms, which require frequent and precise inspection—directly increasing demand for drone-based monitoring solutions.

Additionally, the Federal Aviation Administration has been progressively enabling commercial drone operations through regulatory frameworks such as BVLOS (Beyond Visual Line of Sight) approvals, accelerating enterprise adoption across large-scale inspection use cases.

Inspection Drones Market Size and Forecast

-

Market Size in 2025: USD 15.27 Billion

-

Market Size by 2035: USD 84.56 Billion

-

CAGR: 18.99% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Inspection Drones Market - Request Free Sample Report

Inspection Drones Market Trends

-

Rising adoption of drone-based inspection across energy, utilities, and infrastructure sectors is significantly improving operational safety and reducing manual inspection risks.

-

Increasing shift toward Drone-as-a-Service (DaaS) models is enabling cost-effective deployment and scalability for enterprises without heavy upfront investments.

-

Rapid integration of AI-powered analytics, computer vision, and automated defect detection is enhancing inspection accuracy and real-time decision-making capabilities.

-

Growing demand for LiDAR, thermal imaging, and multispectral sensing technologies is enabling high-precision asset monitoring in complex and low-visibility environments.

-

Increasing regulatory support for Beyond Visual Line of Sight (BVLOS) operations is expanding large-scale inspection capabilities across geographically dispersed assets.

-

Rising focus on predictive maintenance and digital twin integration is transforming inspection workflows from reactive to data-driven and proactive asset management.

-

Expanding use of autonomous navigation, obstacle avoidance systems, and swarm drone technologies is driving innovation in scalable and high-efficiency inspection operations.

U.S. Inspection Drones Market Size Outlook:

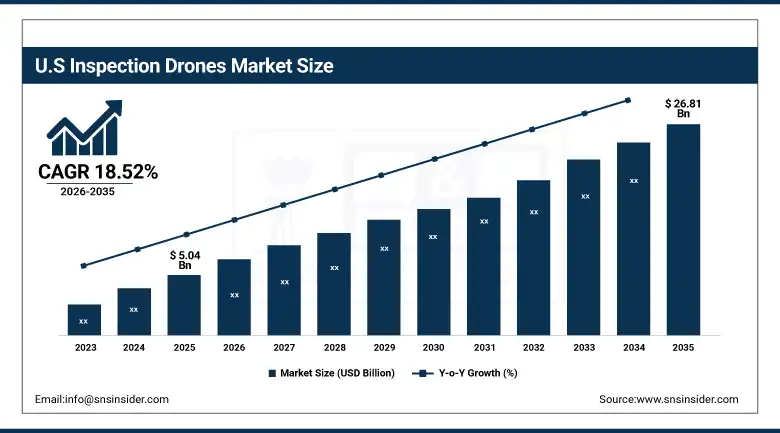

The U.S. Inspection Drones Market was valued at USD 5.04 billion in 2025 and is expected to reach USD 26.81 billion by 2035, growing at a CAGR of 18.52% from 2026–2035. The United States' Inspection Drone Market leads in the world due to its well-developed industrial structure, supportive government regulations, and market participants like Skydio, AeroVironment, Inc., and Teledyne FLIR LLC. Growing applications in various industries such as energy, utilities, telecommunication, and infrastructure, combined with BVLOS regulations, are helping in the rapid commercialization of the technology.

Supporting this trend, the Federal Aviation Administration continues to expand operational approvals for commercial drone usage, enabling wider deployment in inspection of power grids, pipelines, and transportation infrastructure.

In addition, recent developments highlight rapid innovation momentum. In 2024, Skydio enhanced its autonomous inspection platforms with advanced AI-driven navigation and analytics, while DJI expanded its enterprise drone portfolio with improved thermal imaging and inspection capabilities, reinforcing the U.S. market’s leadership in scalable, AI-powered inspection solutions.

Inspection Drones Market Segment Highlights

-

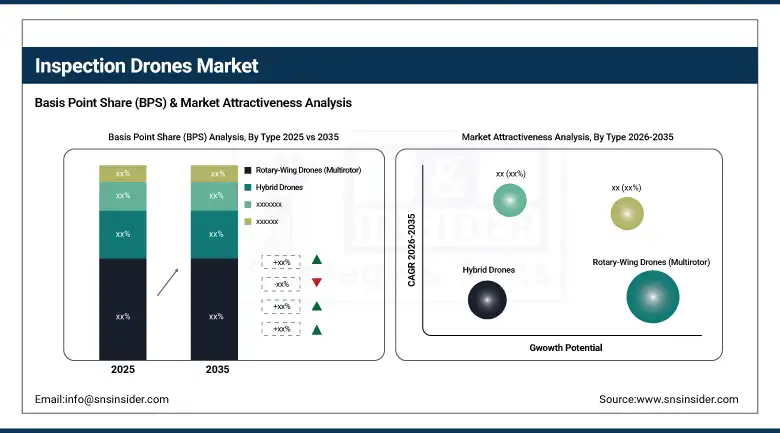

By Type, Rotary-Wing Drones (Multirotor) dominated the Inspection Drones Market with 55.36% share in 2025; Fixed-Wing Drones fastest growing CAGR

-

By Component, Hardware dominated the Inspection Drones Market with 60.45% share in 2025; Software fastest growing CAGR

-

By Application, Power & Utility Inspection dominated the Inspection Drones Market with 27.45% share in 2025; Infrastructure Inspection fastest growing CAGR

-

By Technology, Visual Imaging dominated the Inspection Drones Market with 42.21% share in 2025; AI & Machine Learning-Based Analytics fastest growing CAGR

-

By End User, Energy & Utilities dominated the Inspection Drones Market with 30.24% share in 2025; Construction & Infrastructure fastest growing

By Type, Rotary-Wing Drones (Multirotor) segment dominates the Inspection Drones Market, Fixed-Wing Drones segment expected to grow fastest

In 2025, the Rotary-Wing Drones (Multirotor) segment maintained its dominant position in the Inspection Drones Market, accounting for 55.36% of total revenue. This segment includes quadcopters, hexacopters, and octocopters, which are widely deployed due to their superior maneuverability, vertical take-off and landing (VTOL) capability, and ability to hover precisely during inspections.

From 2026 to 2035, the Fixed-Wing Drones segment is projected to record the highest CAGR. The fixed-wing systems have higher flight endurance, faster speed, and greater range to cover larger areas, making them perfect choices for large-scale inspection applications like pipeline inspection, transmission lines, and mine surveying. Growing use for corridor mapping, asset inspection, and terrain inspection, along with LiDAR technology and AI-based analysis integration, is creating more demand.

By Component, Hardware segment dominates the Inspection Drones Market, Software segment expected to grow fastest

The Hardware segment dominated the Inspection Drones Market in 2025, accounting for 60.45% of total revenue. This market segment includes drone bodies, propellers, cameras, sensors, and navigation systems, which constitute the fundamental backbone of inspection systems. The high demand for high-resolution imaging equipment, thermal imaging sensors, and LiDAR systems, combined with constant upgrading and replacement of hardware, ensures that revenues remain highly concentrated in this market segment.

The Software segment is expected to register the highest CAGR of during 2026–2035. This growth is Enabled by fast deployment of analytics platforms powered by AI, automation of defect detection, cloud computing, and digital twins. Organizations are using software tools to turn raw data collected from drones into useful information to facilitate predictive maintenance and informed decision-making.

By Application, Power & Utility Inspection segment dominates the Inspection Drones Market, Infrastructure Inspection segment expected to grow fastest

In 2025, the Power & Utility Inspection segment held the largest share of 27.45% in the Inspection Drones Market. This is because of the massive utilization of drones in the process of inspecting power transmission lines, substations, wind farms, and solar energy plants since manually conducting such inspections would be costly, inefficient, and dangerous. Due to the massive investments made globally in renewable energy systems and the development of electrical grids, there has been an increase in demand for reliable inspection techniques, and thus drones are key.

The Infrastructure Inspection segment is expected to register the highest CAGR of during the 2026–2035 forecast period. Rapid urbanization, smart city initiatives, and aging infrastructure across developed economies are driving demand for bridge, railway, road, and building inspections.

By Technology, Visual Imaging segment dominates the Inspection Drones Market, AI & Machine Learning-Based Analytics segment expected to grow fastest

The Visual Imaging segment maintained the highest technology share of 42.21% in the Inspection Drones Market till 2025. This is because of the wide range of applications, the economical nature of implementation, and the ease of implementation in different inspection scenarios ranging from infrastructure inspection, utility inspection, oil and gas inspection, and telecommunications inspection. High-definition cameras using RGB sensors are still the backbone of inspection technology that helps in capturing real-time visual information, which enables the inspector to detect visible defects such as cracks, corrosion, and structural damage on the surface. Improvement in camera technology has led to high-quality images and stable images, thus increasing efficiency.

The AI & Machine Learning-Based Analytics segment is projected to register the highest CAGR for during the 2026–2035 forecast period.

By End User, Energy & Utilities segment dominates the Inspection Drones Market, Construction & Infrastructure segment expected to grow fastest

The Energy & Utilities segment accounted for the largest share of 36.24% in the Inspection Drones Market in 2025. Such domination is fueled by the increased use of drones for inspecting power transmission lines, substations, wind turbines, and solar farms. The use of conventional methods of inspection is laborious and risky, and hence the use of drones is vital in improving efficiency and effectiveness of inspection process in such an environment. Increased investments in smart grids and renewable energy generation are some of the drivers of increasing demand for drones in this industry sector.

The Construction & Infrastructure segment is expected to register the highest CAGR of during the 2026–2035 forecast period.

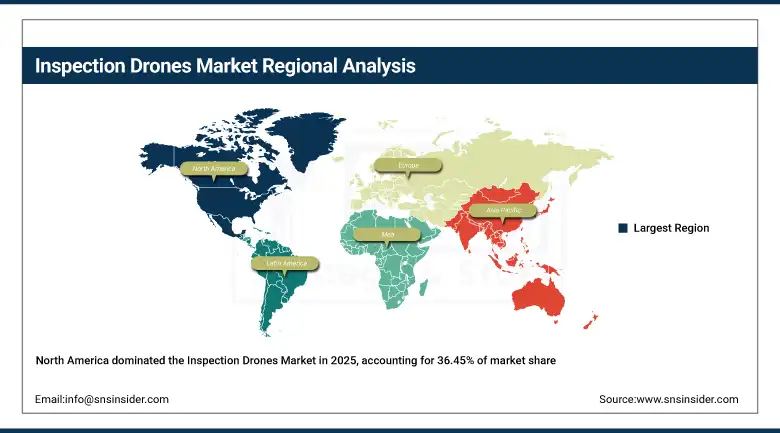

Inspection Drones Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

36.45% |

|

Europe |

Germany |

26.14% |

|

Asia Pacific |

China |

24.75% |

|

Middle East & Africa |

UAE |

7.04% |

|

Latin America |

Brazil |

5.62% |

North America Inspection Drones Market Insights

North America held the dominant position in the global Inspection Drones Market with 36.45% revenue share in 2025, backed by the availability of sophisticated industrial infrastructure, robust regulatory regimes, and early adoption of drones for inspections in energy, utilities, and infrastructure industries. The United States ranks highest among the regions in terms of Traditional-regional shares, thanks to the widespread use of drones in monitoring the electricity grid network, oil and gas pipelines, and telecommunications infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the Federal Aviation Administration continues to expand commercial drone operations through initiatives enabling Beyond Visual Line of Sight (BVLOS) and remote inspection capabilities, significantly enhancing scalability for enterprise deployments.

In addition, in 2024, Skydio expanded its autonomous inspection solutions with enhanced AI-driven navigation and asset inspection workflows, highlighting North America’s leadership in AI-powered and fully autonomous inspection ecosystems.

Asia Pacific Inspection Drones Market Insights

The Asia Pacific region is anticipated to register the highest CAGR of 19.66% over the forecast period of 2026–2035, Propelled by fast-paced industrialization, growing infrastructural networks, and advancements in automation technology within developing nations. Nations like China, India, Japan, South Korea, and Australia stand out as crucial markets, with China contributing of regional revenues because of its robust manufacturing capabilities and infrastructure development programs. Additionally, the growth potential of the region is boosted by rising investments in smart cities, renewable energy systems, and telecommunications networks, which are essential areas that necessitate ongoing inspection solutions.

Supporting this growth, the Civil Aviation Administration of China has progressively enabled commercial drone operations for industrial applications, facilitating wider deployment across infrastructure and energy sectors.

In addition, companies like DJI continue to advance enterprise drone platforms with improved imaging, thermal sensing, and automation capabilities, reinforcing Asia Pacific as a global manufacturing and innovation hub for inspection drones.

Europe Inspection Drones Market Insights

Europe was the second largest revenue generator for the global Inspection Drones Market. Europe’s market growth is driven by its regulatory compatibility, sustainability programs, and high drone use for renewable energy inspections. Countries like Germany, the UK, France, and the Netherlands are the top adopters of drones, especially for wind turbine inspections, solar farms, and transportation systems. Europe enjoys an advantage in terms of a well-developed industrial sector and automation technology.

Supporting this position, the European Union Aviation Safety Agency has implemented standardized drone regulations across member states, enabling seamless cross-border drone operations for commercial use.

In addition, the European Union’s investment programs focused on digitalization and green energy infrastructure are accelerating demand for drone-based inspection solutions, particularly in renewable energy asset management.

Middle East & Africa and Latin America Inspection Drones Market Insights

The Middle East & Africa (MEA) and Latin American markets are witnessing stable growth in the Inspection Drones Market owing to investments in energy, mining, and infrastructure development. The MEA region comprises nations like Saudi Arabia, UAE, and South Africa that have seen increased adoption of inspection drones due to significant oil & gas activities and infrastructure modernization projects. Likewise, the Latin American region has nations such as Brazil, Mexico, and Chile that are adopting drones in their mines and pipelines along with infrastructure assessment purposes.

Supporting development in these regions, government initiatives such as Saudi Arabia’s Vision 2030 are promoting adoption of advanced technologies, including drones, for industrial efficiency and digital transformation.

In addition, regulatory authorities such as Agência Nacional de Aviação Civil have streamlined drone operation guidelines, enabling broader commercial deployment across industries and improving accessibility for inspection service providers.

Inspection Drones Market Growth Drivers:

-

Rising demand for safe, cost-efficient, and automated inspection solutions across critical infrastructure is driving global adoption of inspection drones

Inspection drones are among the latest technological innovations adopted by several industries for various reasons. The transformation from traditional, labor-intensive inspection methods to automated asset inspection using drones represents one of the strongest structural factors driving the Inspection Drones Market. The energy sector, utility companies, and oil & gas firms have increasingly been focusing on technologies that will enable them to eliminate their workers' exposure to dangerous situations, minimize disruptions in production, and obtain fast and precise information about their assets.

Additionally, the Federal Aviation Administration has been progressively enabling commercial drone operations through expanded approvals and pilot programs supporting Beyond Visual Line of Sight (BVLOS) operations, directly facilitating large-scale industrial inspection deployments.

In addition, recent developments further validate this trend. In 2024, Skydio advanced its autonomous inspection capabilities with enhanced AI-driven navigation and real-time analytics for infrastructure and defense applications, while DJI strengthened its enterprise drone portfolio with improved thermal imaging and automated inspection features, underscoring the industry’s transition toward fully autonomous, intelligent inspection ecosystems.

Inspection Drones Market Restraints:

-

High initial investment and operational complexity associated with advanced inspection drone systems creating adoption barriers, particularly for small and mid-sized enterprises and organizations in emerging markets

The considerable cost implications related to implementing such highly developed solutions for inspection drones pose an important limitation to market growth, particularly for smaller firms with tighter financial budgets. Enterprise inspection drones fitted with LiDAR sensors, thermal imaging technology, AI-powered software analytics capabilities, and autonomous flight systems involve significant upfront investment, which can also be coupled with subscription fees for software, additional expenses on data analysis and maintenance, and specialized training for employees. Such high cost is further exacerbated by the necessity of following regulations and obtaining certifications, among other considerations.

Inspection Drones Market Opportunities:

-

Expansion of autonomous, scalable, and cost-efficient drone inspection ecosystems enabling broader adoption across SMEs, new industries, and emerging markets

The next wave of innovation in the Inspection Drones Market would focus on expanding access to high-end inspection technologies using the automation of processes, reduction in costs related to hardware equipment, and an increase in the use of service models for the deployment of technology. With the advent of fully autonomous drones featuring artificial intelligence-based navigation and analytics that connect to cloud servers, businesses are able to use their services extensively while relying on limited human input. This trend is likely to benefit most small and mid-size businesses, as well as utility providers in less developed regions, especially those from construction, agriculture, and telecoms sectors.

Recent Developments:

-

2026: Skydio continued expanding its autonomous inspection ecosystem with enhanced Dock and remote operations capabilities, enabling fully automated, continuous infrastructure monitoring for utilities, defense, and transportation sectors, while scaling enterprise deployments across North America and Europe.

-

2025: DJI strengthened its enterprise drone portfolio with upgrades to its Matrice and thermal imaging platforms, focusing on improved AI-based inspection workflows, extended flight endurance, and enhanced payload integration for industrial inspection use cases across energy and public safety sectors.

-

2024: Percepto advanced its “drone-in-a-box” autonomous inspection solutions with expanded AI-powered analytics and remote operations capabilities, enabling fully automated site monitoring for industrial assets such as oil & gas facilities and mining operations.

-

2024: Terra Drone Corporation expanded its global inspection services footprint through strategic deployments in energy and infrastructure sectors, leveraging AI-driven data analytics and digital twin integration to enhance large-scale asset inspection and maintenance operations.

Inspection Drones Companies are:

-

DJI

-

Skydio

-

Parrot SA

-

AeroVironment Inc.

-

Teledyne FLIR LLC

-

ideaForge Technology Ltd.

-

Delair SAS

-

Cyberhawk Innovations Ltd.

-

Percepto Ltd.

-

PrecisionHawk Inc.

-

DroneDeploy Inc.

-

Airobotics Ltd.

-

Autel Robotics Co. Ltd.

-

senseFly (AgEagle)

-

Azur Drones

-

Voliro AG

-

SkySpecs Inc.

-

Aerodyne Group

Inspection Drones Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.27 Billion |

| Market Size by 2035 | USD 84.56 Billion |

| CAGR | CAGR of 18.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fixed-Wing Drones, Rotary-Wing Drones (Multirotor), Hybrid Drones, Others) • By Component (Hardware (Airframe, Propulsion, Cameras, Sensors), Software (AI Analytics, Data Processing Platforms), Services (Inspection Services, Maintenance, Training), Others) • By Application (Infrastructure Inspection, Power & Utility Inspection, Oil & Gas Inspection, Mining Inspection, Telecommunications Inspection, Others) • By Technology (Visual Imaging, Thermal Imaging, LiDAR Scanning, AI & Machine Learning-Based Analytics, Government & Defense, Others) • By End-User (Energy & Utilities, Oil & Gas, Construction & Infrastructure, Mining, Telecommunications, Government & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DJI, Skydio, Terra Drone Corporation, Parrot SA, AeroVironment Inc., Teledyne FLIR LLC, ideaForge Technology Ltd., Delair SAS, Flyability SA, Cyberhawk Innovations Ltd., Percepto Ltd., PrecisionHawk Inc., DroneDeploy Inc., Airobotics Ltd., Autel Robotics Co. Ltd., senseFly (AgEagle), Azur Drones, Voliro AG, SkySpecs Inc., Aerodyne Group |

Frequently Asked Questions

The Inspection Drones Market is expected to grow at a CAGR of 18.99% from 2026 to 2035.

The Inspection Drones Market was valued at USD 15.27 billion in 2025.

Increasing demand for safe, cost-efficient, and automated inspection of critical infrastructure, reducing human risk and operational downtime, is the primary growth driver of the Inspection Drones Market.

The Rotary-Wing Drones (Multirotor) segment dominated the Inspection Drones Market in 2025.

North America dominated the Inspection Drones Market in 2025.

Get in Touch