Less Lethal Ammunition Market Report Scope & Overview:

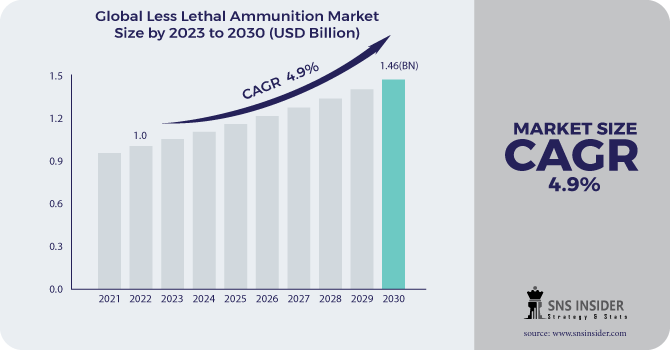

The Less Lethal Ammunition Market was valued at USD 998.7 million in 2023 and is projected to grow to USD 1620.6 million by 2032, achieving a CAGR of 5.1% during the forecast period from 2024 to 2032.

The growth in instances of unrest around the world as a result of various contentious laws and legislations enacted by governments worldwide has increased the need for weapons with a low risk of casualties. Human rights legislators and governments have approved regulations requiring the use of weapons that pose less risk of killing a suspect across numerous security and defence departments. Non-lethal weapons such as pepper spray, batons, and stun guns are a compact, economical, portable, and legal self-defense solution in a hazardous situation. Non-lethal weapons are very important in providing personal security for security workers. Furthermore, non-lethal weapons serve as the initial line of defence against an attack.

To get more information on Less Lethal Ammunition Market - Request Free Sample Report

Non-lethal weapons, such as tasers, flash-bang & smoke grenades, rubber bullets, and tear gas, are extremely effective in crowd control and military operations because they cause only minor to moderate harm to people's bodies. While the use of lethal weapons, such as opening fire on an unruly crowd, can have serious consequences for the lives of rioters and law enforcement personnel, as well as making the protests more aggressive, the use of non-lethal weapons can safely handle situations and are quite useful in managing unlawful events.

MARKET DYNAMICS

KEY DRIVERS

-

Rising Political Conflicts and Civil Unrest

-

Increasing Demand for Lead Load Ammunition Alternatives for Police Shooting

RESTRAINTS

-

Environmental and governmental regulations are strict.

OPPORTUNITIES

-

Increased Research and Development of Advanced and Eco-Friendly Less Lethal Ammunition

-

Increasing Funding for Law Enforcement Agencies to Use Less Lethal Ammunition

CHALLENGES

-

Less lethal ammunition trafficking and indiscriminate use

-

Concerns Among End Users

IMPACT OF COVID-19

The COVID's influence on the market for non-lethal weapons is unpredictable, and it is expected to remain in effect until the second quarter of 2021.

To contain the spread of the COVID-19 virus, governments around the world implemented harsh lockdown and made social distance essential. As a result, numerous organisations began work-from-home programme as safety precautions. This resulted in a sharp drop in demand for non-lethal firearms for personal use all around the world.

Furthermore, the nationwide lockdown compelled non-lethal weapons manufacturing plants to shut down partially or completely.

The negative effects of the COVID-19 pandemic have caused global delays in actions and projects aimed at developing breakthrough non-lethal weaponry alternatives.

The less lethal ammunition market is divided into law enforcement, military, self-defense, and others based on end user. The law enforcement segment is expected to develop at the fastest CAGR during the projection period. The growing militarization of law enforcement agencies around the world, as well as an increase in political disputes and civil unrest, can be contributed to the expansion of this category.

the shotgun weapon type category led the less lethal ammunition market, accounting for more than 54% of worldwide sales. The category dominated the entire LLA market and is predicted to grow at a significant CAGR during the forecast period due to the popularity of the 12-gauge calibre among end-users and manufacturers.

The launcher weapon category is also one of the most popular in the less-lethal ammunition market, which is expected to grow at a CAGR of 4.2 percent from 2021 to 2028. The segment is expected to rise due to the introduction of superior 40 mm calibre low-velocity cartridges with improved precision and dependability in all climatic situations.

Bullets made of rubber Due to the increasing use of 12-gauge shotguns and 40mm rubber bullets for mass control activities, this category dominated the market in 2022 and is predicted to increase at the greatest CAGR during the forecast period.

Rounds of Bean Bags The category is likely to expand during the projection period as law enforcement agencies increasingly deploy bean bag rounds for crowd control management.

Bullets made of polyethylene/plastic The increased use of polyethylene/plastic bullets by developing countries such as India is likely to fuel segment expansion.

Smoke and OC/CS Munitions The segment will increase at a favourable pace in the global market during the projected period due to the widespread use of smoke munitions for medium to long-distance law enforcement to ensure physical integrity.

Rounds of Flash Bang Flash bang rounds emit terrible noise between 140-180 DB, which is why they are accepted by all governments worldwide.

Paint balls are widely employed by law enforcement organisations for tactical combat training and crowd control activities, hence the segment will develop steadily over the projection period.

Others Wax bullets, wooden bullets, and sponge grenades are among the items under the Others category.

KEY MARKET SEGMENTATION

By Product Type

-

Gases and Sprays

-

Grenades

-

Taser Guns

-

Bullets

-

Others

By End User

-

Law Enforcement Agencies

-

Military

-

Citizens

By Weapon Type

-

Shotguns

-

Launchers

By Technology

-

Chemical

-

Electroshock

-

Mechanical and Kinetic

-

Acoustic/Light

-

Others

.png)

Need any customization research on Less Lethal Ammunition Market - Enquiry Now

REGIONAL ANALYSIS

North America dominated the market, accounting for more than 32% of total revenue. Because of its huge defense-spending budget each year, the United States is the major contributor to less lethal ammunition sales in North America, resulting in increased acquisition of LLA for law enforcement and military agencies. China's increased defence spending budget, Asia Pacific is likely to see significant growth in demand throughout the forecast period. Furthermore, escalating political tensions and civil unrest in some parts of India, particularly Kashmir, are projected to fuel demand for less lethal weaponry.

Due to a significant increase in crime rates in countries such as South Africa, Kenya, Nigeria, and Papua New Guinea, the Middle East Asia region is predicted to grow at the fastest pace of 7.8 percent over the forecast period. Furthermore, previous violent rallies against foreign migrants have compelled law enforcement authorities to arm themselves with riot control ammunition.

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS

The Major Players are Condor Non-Lethal Technologies, ISPRA by Ei Ltd., Rheinmentall AG, ALS Less-Lethal Systems, Inc., ASP, Inc., Combined Systems, Inc., Safariland, LLC, Zarc International Inc., Nonlethal Technologies, Inc., Pepperball Technologies, Inc., and other players.

Rheinmentall AG-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 998.7 Million |

| Market Size by 2032 | US$ 1620.6 Million |

| CAGR | CAGR of 5.1% From 2024 to 2032 |

| Base Year | 2022 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Rubber Bullets, Bean Bag Rounds, Plastic Bullets, Paintballs) • By End User (Law Enforcement Agencies, Military, and Citizens) • By Weapon Type (Shotguns, Launchers) • By Technology (Chemical, Electroshock, Mechanical and Kinetic, Acoustic/Light, and Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Condor Non-Lethal Technologies, ISPRA by Ei Ltd., Rheinmentall AG, ALS Less-Lethal Systems, Inc., ASP, Inc., Combined Systems, Inc., Safariland, LLC, Zarc International Inc., Nonlethal Technologies, Inc., Pepperball Technologies, Inc. |

| KEY DRIVERS | • Rising Political Conflicts and Civil Unrest • Increasing Demand for Lead Load Ammunition Alternatives for Police Shooting |

| Restraints | • Environmental and governmental regulations are strict. |

Frequently Asked Questions

Increased Research and Development of Advanced and Eco-Friendly Less Lethal Ammunition and Increasing Funding for Law Enforcement Agencies to Use Less Lethal Ammunition

Less lethal ammunition trafficking and indiscriminate use and Concerns Among End Users

Condor Non-Lethal Technologies, ISPRA by Ei Ltd., Rheinmentall AG, ALS Less-Lethal Systems, Inc., ASP, Inc., Combined Systems, Inc., Safariland, LLC, Zarc International Inc., Nonlethal Technologies, Inc., Pepperball Technologies, Inc.

According to SNS insiders, the Less Lethal Ammunition Market size was USD 0.956 billion in 2021 and is expected to reach USD 1.33 billion by 2028 with a CAGR of 4.9% over the forecasted period.

The sample for the Less Lethal Ammunition Market report is available on the website upon request. To obtain the sample report, you can also use the 24*7 chat support and direct call services.

Get in Touch