Light Weapons Market Report Scope & Overview:

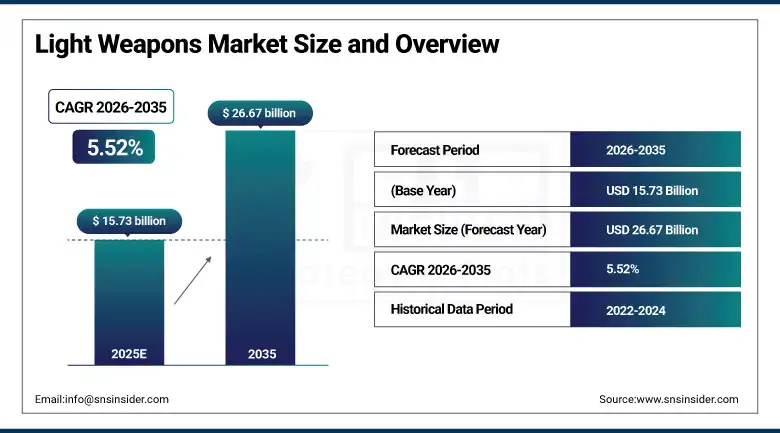

The Light Weapons Market was valued at USD 15.73 billion in 2025 and is expected to reach USD 26.67 billion by 2035, growing at a CAGR of 5.52% from 2026–2035.

The Light Weapons Market is witnessing significant growth on account of growing military expenditure across the globe, modernization projects, and acquisitions of portable, accurate, and modular arms. Growing geopolitical conflicts, asymmetric warfare, urban warfare situations, and border security issues are fueling the need for advanced light weapons like MANPADS, anti-tank guided weapons, grenade launchers, and machine guns equipped with smart technology.

As per the Stockholm International Peace Research Institute, global military expenditure reached a record USD 2.44 trillion in 2023, marking a significant rise compared to previous years, while multiple NATO and Asia-Pacific countries have announced higher defense budgets and accelerated infantry modernization programs

In April 2025, SIG Sauer, Inc. continued large-scale deliveries under the U.S. Army’s Next Generation Squad Weapon (NGSW) program, including the XM7 rifle and XM250 automatic rifle, aimed at replacing legacy infantry weapons with more advanced and lethal systems.

Light Weapons Market Size and Growth Forecast

-

Market Size in 2025: USD 15.73 Billion

-

Market Size by 2035: USD 26.67 Billion

-

CAGR: 5.52% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Light Weapons Market - Request Free Sample Report

Light Weapons Market Trends

-

Rising adoption of precision-guided anti-tank weapons and MANPADS is improving target engagement accuracy and battlefield effectiveness.

-

Increasing focus on infantry modernization programs is boosting procurement of next-generation rifles, machine guns, and shoulder-fired weapon systems.

-

Rapid integration of AI-enabled fire control systems, smart optics, and thermal targeting technologies is enhancing situational awareness and combat precision.

-

Growing demand for lightweight, portable, and modular weapon platforms is improving soldier mobility and faster tactical response.

-

Increasing defense modernization budgets and homeland security investments are accelerating procurement of advanced light weapon systems.

-

Rising adoption of vehicle-mounted and remotely operated light weapon systems is expanding operational flexibility and remote threat engagement capabilities.

-

Expanding use of laser-guided, infrared-guided, and multi-caliber weapon technologies is driving innovation in precision-strike and adaptable combat solutions.

U.S. Light Weapons Market Size Outlook:

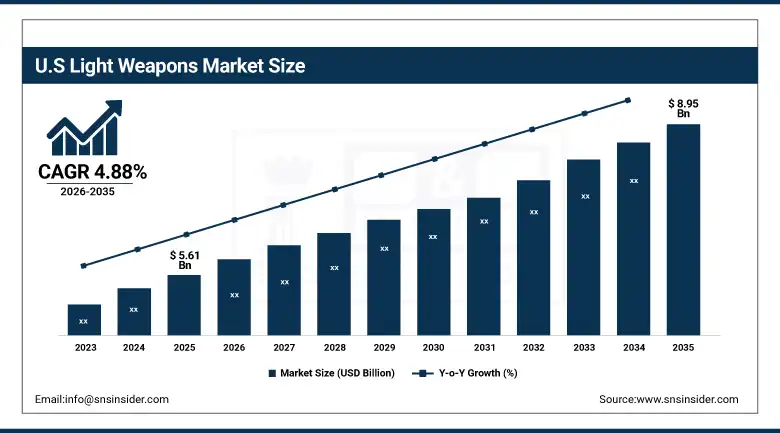

The U.S. Light Weapons Market was valued at USD 5.61 billion in 2025 and is expected to reach USD 8.95 billion by 2035, growing at a CAGR of 4.88% from 2026–2035. The U.S. Market holds the record for being the largest market globally based on factors such as its large defense budget, efforts geared towards the modernization of its military, and the presence of major players in the defense industry including the Lockheed Martin Corporation, RTX Corporation (Raytheon Technologies), SIG Sauer, Inc., and Northrop Grumman Corporation. The favorable procurement policy adopted by the United States Department of Defense and programs such as infantry modernization and next generation squad weapon have helped to boost uptake in the market.

Rising investments under the Next Generation Squad Weapon (NGSW) program and homeland security procurement continue to drive adoption of advanced rifles, machine guns, and guided portable weapon systems.

In addition, in 2025, SIG Sauer, Inc. continued deliveries of the XM7 and XM250 under the U.S. Army’s NGSW program, while the U.S. Department of Defense accelerated procurement of advanced anti-armor and shoulder-fired systems, reinforcing the U.S. as a major innovation and procurement hub in the global Light Weapons Market.

Light Weapons Market Segment Highlights

-

By Product Type, Machine Guns dominated the Light Weapons Market with 24.36% share in 2025; MANPADS (Man-Portable Air Defense Systems) fastest growing CAGR.

-

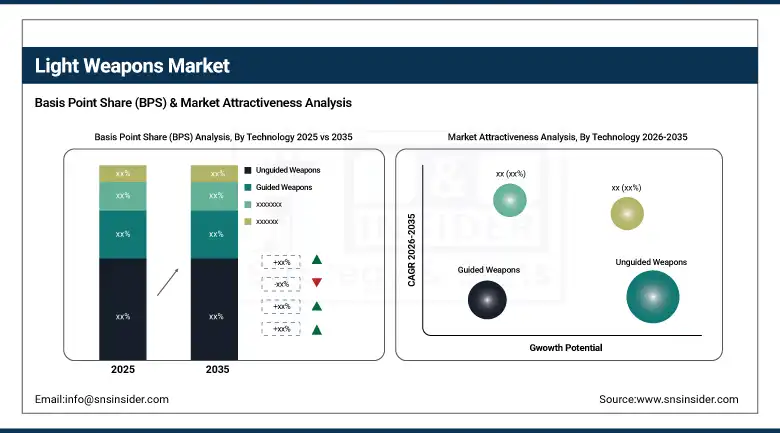

By Technology, Unguided Weapons dominated the Light Weapons Market with 39.45% share in 2025; Unguided Weapons also fastest growing CAGR.

-

By End User, Military / Armed Forces dominated the Light Weapons Market with 63.85% share in 2025; Special Forces / Tactical Units fastest growing CAGR.

-

By Mode of Operation, Individual / Shoulder-Fired Weapons dominated the Light Weapons Market with 46.54% share in 2025; Vehicle-Mounted Light Weapons fastest growing CAGR.

-

By Range, Short Range dominated the Light Weapons Market with 42.14% share in 2025; Long Range fastest growing CAGR.

By Product Type, Machine Guns segment dominates the Light Weapons Market, MANPADS segment expected to grow fastest

In 2025, the Machine Guns segment maintained its dominant position in the Light Weapons Market, accounting for approximately 24.36% of total revenue. This category encompasses general-purpose machine guns, squad automatic weapons, and heavy machine guns that can be carried by an individual. The continued importance on the battlefield, large-scale purchases through infantry modernization projects, and their flexibility in offensive as well as defensive roles ensure continued segment leadership.

From 2026 to 2035, the MANPADS (Man-Portable Air Defense Systems) segment is projected to record the highest CAGR. Rising concerns over low-altitude aerial threats including drones, helicopters, and close-air-support aircraft are driving accelerated procurement of portable air defense systems.

By Technology, Unguided Weapons segment dominates the Light Weapons Market, Unguided Weapons segment expected to grow fastest

The Unguided Weapons segment held the largest share of approximately 39.45% in the Light Weapons Market in 2025, driven in light of their efficiency, extensive use, and compatibility with regular infantry activities. The category comprises standard machine guns, RPGs, mortars, and grenade launchers, which continue to form the core of military and police armaments across the world.

The Unguided Weapons segment is also expected to register the highest CAGR of during the 2026–2035 forecast period. Growing procurement volumes in emerging markets, sustained ammunition compatibility, and increased demand for simple and rapidly deployable battlefield systems are supporting continued expansion

By End User, Military / Armed Forces segment dominates the Light Weapons Market, Special Forces / Tactical Units segment expected to grow fastest

The Military / Armed Forces segment maintained the highest end-user share of 63.85% in the Light Weapons Market in 2025. Military forces constitute the key source for machine guns, anti-tank guided missiles, man-portable air-defense systems (MANPADS), and grenade launchers required for infantry operations, armored warfare, and border protection operations.

The Special Forces / Tactical Units segment is projected to achieve the highest growth rate CAGR during 2026–2035. There is growing interest around the world in weapons designed for fast reaction, counterterrorism, and urban combat missions, resulting in the development of new, light, modular, and precision weapon systems suited to elite forces. The use of high-tech optical sights, silencers, artificial intelligence targeting devices, and portable anti-armor shoulder-fired weapons systems has been increasing.

By Mode of Operation, Individual / Shoulder-Fired Weapons segment dominates the Light Weapons Market, Vehicle-Mounted Light Weapons segment expected to grow fastest

The Individual / Shoulder-Fired Weapons segment maintained the highest mode of operation share of approximately 46.54% in the Light Weapons Market till 2025. This is due to their extensive use in infantry combat, border patrol operations, and urban warfare scenarios, along with their portability, lower operational complexity, and rapid deployment capability across military and law enforcement forces.

The Vehicle-Mounted Light Weapons segment is projected to register the highest CAGR of during the 2026–2035 forecast period.

By Range, Short Range segment dominates the Light Weapons Market, Long Range segment expected to grow fastest

The Short Range segment maintained the highest range share of approximately 42.14% in the Light Weapons Market till 2025. This is because of its widespread use in close-combat operations, tactical urban warfare, and law enforcement engagements where rapid response and high maneuverability are critical in short-distance threat neutralization.

The Long-Range segment is projected to register the highest CAGR during the 2026–2035 forecast period.

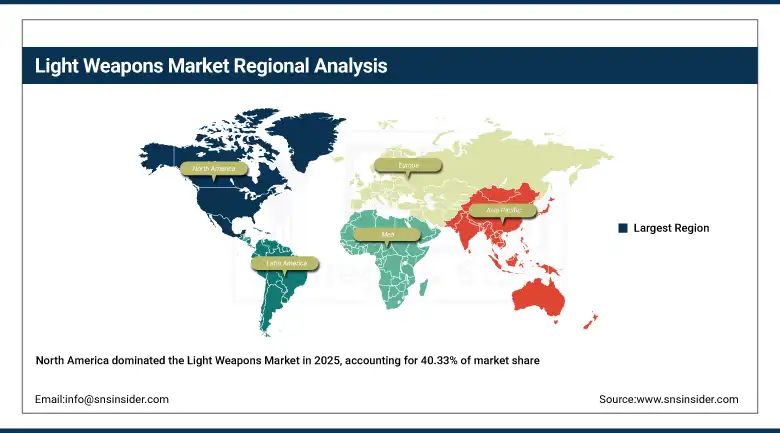

Light Weapons Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40.33% |

|

Europe |

Germany |

26.14% |

|

Asia Pacific |

China |

24.75% |

|

Middle East & Africa |

UAE |

5.04% |

|

Latin America |

Brazil |

3.74% |

North America Light Weapons Market Insights

North America was the leading market for the global Light Weapons Market with around 40.33% share of revenues in 2025, due to North America’s unparalleled military expenditure, military modernization schemes, robust manufacturing abilities within the country, and the purchase of next-generation infantry weapons systems. North America was dominated by the United States, which was backed up by major programs like NGSW, border security enhancement initiatives, and anti-armor and shoulder-fired weapons procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the U.S. Department of Defense continues to expand investments in infantry modernization, precision-guided munitions, and smart-enabled fire control systems to improve battlefield effectiveness and force protection.

In addition, under the U.S. Army’s FY2025–2030 procurement roadmap, plans include the acquisition of approximately 111,428 XM7 rifles, 13,334 XM250 automatic rifles, and 124,749 XM157 fire control optics, highlighting the scale of operational modernization and reinforcing North America’s leadership in advanced soldier lethality programs.

Asia Pacific Light Weapons Market Insights

The Asia-Pacific region is forecasted to grow at a CAGR of 6.12%, which can be attributed to increasing political instabilities in the region, rise in defense expenditure, local manufacture of arms, and huge modernization of armed forces. The major drivers of growth in this market include China, India, Japan, South Korea, and Australia, with China being the largest revenue contributor in the region. The rapid growth rate in the market is also influenced by large spending on border security and air defense systems.

Additionally, China has significantly increased procurement of advanced infantry combat systems and portable air-defense platforms, while Japan’s 2025 defense budget includes expanded allocations for stand-off missiles, next-generation rifles, and integrated soldier modernization programs.

Europe Light Weapons Market Insights

Europe held the second-largest revenue share in the global Light Weapons Market, accounting for approximately 26.14% in 2025, driven by increased NATO-aligned defense spending, rising procurement linked to regional security concerns, and strong presence of leading defense manufacturers. Countries such as Germany, the United Kingdom, France, and Italy are key contributors, supported by investments in infantry modernization, anti-armor systems, and precision-guided portable weapons.

Supporting this position, the European Defence Agency and various EU-backed defense initiatives continue to fund collaborative programs for advanced weapon systems, soldier modernization, and ammunition interoperability.

In addition, European manufacturers such as Rheinmetall AG, Saab AB, and Thales Group have expanded production of anti-tank guided missiles, portable air-defense systems, and smart optics to meet rising procurement demand across NATO member states.

Middle East & Africa and Latin America Light Weapons Market Insights

The MEA and Latin America regions show sustained growth for the Light Weapons Market, owing to the increased modernization of the defense sector, rising need for border security, and growing expenditure on defense and security operations. The major countries that contribute to growth in the MEA region include Saudi Arabia, UAE, Israel, and South Africa, due to diversified national defense programs and high acquisition of anti-armor and assault weapons as well as border security equipment.

In Latin America, countries such as Brazil, Mexico, and Colombia are driving demand due to increasing focus on counter-narcotics operations, anti-smuggling enforcement, and urban law enforcement modernization. Brazil remains the largest regional contributor, supported by domestic production capabilities and ongoing procurement of modern assault rifles, machine guns, and tactical weapon systems for military and federal police forces.

Additionally, in 2024–2025, Brazil increased procurement of next-generation infantry rifles and tactical systems for border security and organized crime operations, while several Middle Eastern countries expanded acquisitions of portable air-defense systems, anti-drone weapons, and advanced smart optics to strengthen operational readiness and national security capabilities.

Light Weapons Market Growth Drivers:

-

Rising geopolitical tensions, military modernization programs, and increasing demand for advanced infantry weapon systems driving global adoption of light weapons

The rising magnitude of geopolitical tensions, boundary disagreements, asymmetric warfare, and transnational security challenges represents the primary structural impetus behind the Light Weapons Market. The international community is witnessing a trend wherein national administrations are making efforts to procure light arms that can increase infantry effectiveness, facilitate force maneuverability, and ensure mission readiness. Contemporary military forces are gradually moving away from conventional firearms and investing in futuristic rifle technologies, guided anti-tank missiles, MANPADS, and artificial intelligence-driven fire control mechanisms to counter modern battlefield threats.

In addition, the North Atlantic Treaty Organization reported that in 2024, more than 23 member countries were expected to meet or exceed the alliance’s 2% of GDP defense spending target, resulting in increased procurement of advanced infantry weapons, anti-armor systems, and portable air-defense platforms across member states, reinforcing long-term global demand for light weapons.

Light Weapons Market Restraints:

-

Stringent export regulations, arms trade restrictions, and high procurement costs of advanced guided weapon systems creating adoption barriers across several countries

The highly regulated nature of international armament exports along with the extremely costly nature of advanced light weapons is a major constraint in the market, especially in developing nations, smaller armies, or countries under sanctions and trade limitations due to geopolitics. The deployment of advanced weaponry like the man-portable air defense system, anti-tank guided weaponry, and intelligent fire control systems demands considerable funding, specialized skills, and proper maintenance, which makes the purchase quite difficult for smaller budget armed forces.

Light Weapons Market Opportunities:

-

Accelerating development of lightweight smart weapon systems, AI-enabled targeting solutions, and modular combat platforms creating new growth pathways for infantry modernization and next-generation battlefield capabilities

Opportunities for future expansion in the market for Light Weapons will be based on advances that make light weapons more effective by making them smaller, more accurate, and intelligent. Defense companies that produce weapons that are lightweight, modifiable, and have multiple roles will cater to the rising need for enhanced soldier mobility, quick deployment, and adaptability to different types of battles. The development of artificial intelligence-enabled fire control systems and other sophisticated tools, such as smart optics and thermal imagers, will increase light weapons' applicability in drone combat and urban and special missions’ warfare.

Recent Developments:

-

2026: SIG Sauer, Inc. is expected to further scale production and international deployment of the XM7 rifle and XM250 automatic rifle under the U.S. Army’s Next Generation Squad Weapon (NGSW) program, alongside expanded fielding of the XM157 Fire Control optic, strengthening next-generation infantry lethality and smart-targeting capabilities.

-

2025: Rheinmetall AG expanded production capacity for ammunition, portable anti-tank systems, and infantry weapon components across its European facilities to meet rising demand from NATO members and allied nations amid accelerated defense procurement and replenishment programs.

-

2024: Saab AB secured additional international contracts and increased deliveries of its Carl-Gustaf M4 recoilless rifle system and related ammunition, driven by growing demand for lightweight anti-armor and multi-role infantry weapon systems across Europe and Asia-Pacific.

-

2024: Lockheed Martin Corporation and RTX Corporation (Raytheon Technologies) continued expanding production and modernization programs for the Javelin anti-tank guided missile system and Stinger MANPADS to support replenishment requirements and increased military aid commitments globally.

Light Weapons Companies are:

-

RTX Corporation (Raytheon Technologies)

-

Northrop Grumman Corporation

-

BAE Systems plc

-

General Dynamics Corporation

-

FN Herstal

-

Colt's Manufacturing Company LLC

-

SIG Sauer, Inc.

-

Beretta Holding S.A.

-

Israel Weapon Industries (IWI)

-

Rheinmetall AG

-

Thales Group

-

Saab AB

-

Leonardo S.p.A.

-

MBDA

-

Nammo AS

-

ST Engineering

-

Bharat Dynamics Limited (BDL)

-

Denel SOC Ltd.

Light Weapons Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.73 Billion |

| Market Size by 2035 | USD 26.67 Billion |

| CAGR | CAGR of 5.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Machine Guns, Grenade Launchers, MANPADS (Man-Portable Air Defense Systems), Anti-Tank Guided Weapons / Launchers, Rocket-Propelled Grenades (RPGs), Others) • By Technology (Unguided Weapons, Guided Weapons, Laser-Guided Systems, Infrared / Thermal Targeting Systems, Smart / AI-Integrated Fire Control Systems) • By End User (Military / Armed Forces, Homeland Security / Border Security, Law Enforcement Agencies, Special Forces / Tactical Units) • By Mode of Operation (Individual / Shoulder-Fired Weapons,Crew-Served Weapons, Vehicle-Mounted Light Weapons) • By Range (Short Range, Medium Range, Long Range) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, RTX Corporation (Raytheon Technologies), Northrop Grumman Corporation, BAE Systems plc, General Dynamics Corporation, FN Herstal, Heckler & Koch GmbH, Colt's Manufacturing Company LLC, SIG Sauer, Inc., Beretta Holding S.A., Israel Weapon Industries (IWI), Rheinmetall AG, Thales Group, Saab AB, Leonardo S.p.A., MBDA, Nammo AS, ST Engineering, Bharat Dynamics Limited (BDL), Denel SOC Ltd. |

Frequently Asked Questions

The Light Weapons Market is expected to grow at a CAGR of 5.52% from 2026 to 2035.

The Light Weapons Market was valued at USD 15.73 billion in 2025.

Rising geopolitical tensions, military modernization programs, and increasing demand for advanced infantry weapon systems are the primary growth drivers of the Light Weapons Market.

The Unguided Weapons segment dominated the Light Weapons Market in 2025.

North America dominated the Light Weapons Market in 2025.

Get in Touch