Load Break Switch Market Report Scope & Overview:

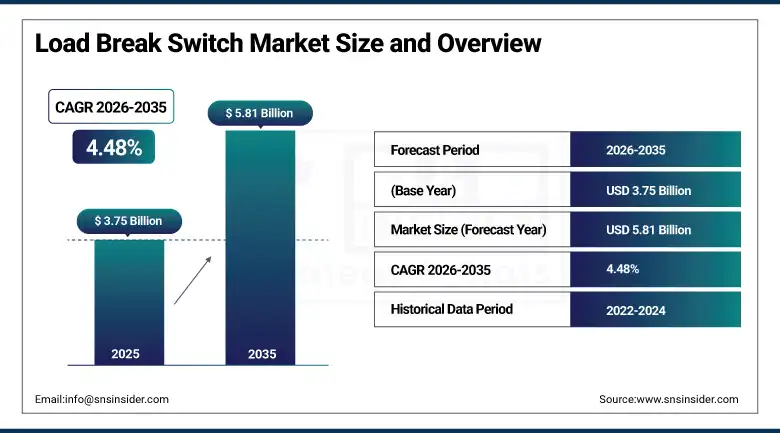

The Load Break Switch Market was valued at USD 3.75 Billion in 2025 and is expected to reach USD 5.81 Billion by 2035, growing at a CAGR of 4.48% from 2026–2035.

The load break switch is an electrical load switch used at medium voltage to connect, disconnect, and isolate power circuits at full load current safely. In contrast to ordinary disconnection switches that can only be operated when there is no electrical current flowing in the circuit, the load break switch can open the circuit even when there is load current in it. These devices are used extensively in utility, industrial, and renewable energy distribution networks.

In 2024, ABB Ltd. launched an enhanced range of SafeRing and SafePlus ring main units incorporating advanced load break switch technology with integrated digital sensors for real-time fault detection and remote switching capability via IEC 61850 communication protocol.

Market Size and Forecast

-

Market Size in 2026E: USD 3.92 Billion

-

Market Size by 2035: USD 5.81 Billion

-

CAGR: 4.48% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Load Break Switch Market - Request Free Sample Report

Load Break Switch Market Trends

-

Smart grid modernization is increasing demand for motorized and remotely operated load break switches that enable automated fault isolation, service restoration, and enhanced distribution network reliability

-

Expansion of renewable energy projects is creating new load break switch requirements for solar and wind power installations, supporting grid connection, protection, and operational flexibility

-

Growing regulatory focus on reducing SF6 emissions is accelerating the adoption of environmentally friendly load break switch technologies based on vacuum, dry air, and alternative insulation systems

-

Rapid deployment of electric vehicle charging infrastructure is driving demand for load break switches to support feeder protection, load management, and reliable power distribution

-

Compact and modular ring main unit solutions with integrated load break switches are gaining popularity in urban power networks due to their space efficiency, advanced monitoring, and simplified installation capabilities

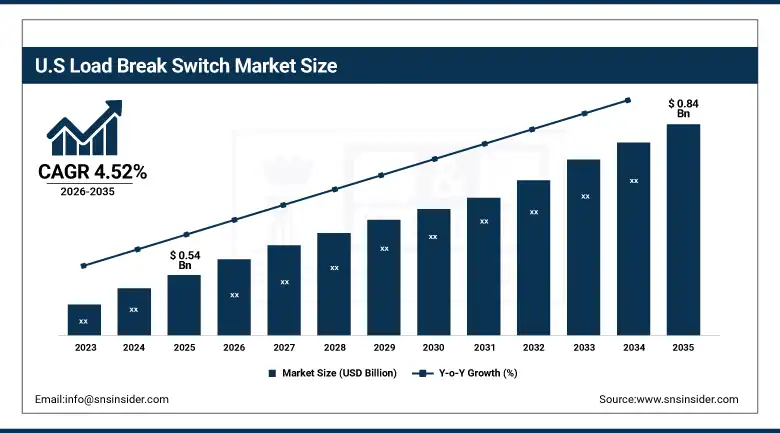

U.S. Load Break Switch Market Outlook

The U.S. Load Break Switch Market was valued at approximately USD 0.54 Billion in 2025 and is expected to reach approximately USD 0.84 Billion by 2035, growing at a CAGR of approximately 4.52%.

The load break switch market in the United States is experiencing positive impacts due to the implementation of various programs designed to enhance the reliability and efficiency of power grid distribution systems. Significant investments have been made in distribution automation, AMI, and smart grids, which are resulting in high demands for automated and remote controlled load break switches.

In October 2025, Eaton Corporation expanded its distribution automation portfolio with the launch of its next-generation Cooper Form 6 recloser and load break switch integration platform for utility distribution networks, combining automatic fault restoration capability with advanced analytics for outage cause prediction and maintenance scheduling optimisation.

Load Break Switch Market Segment Analysis

-

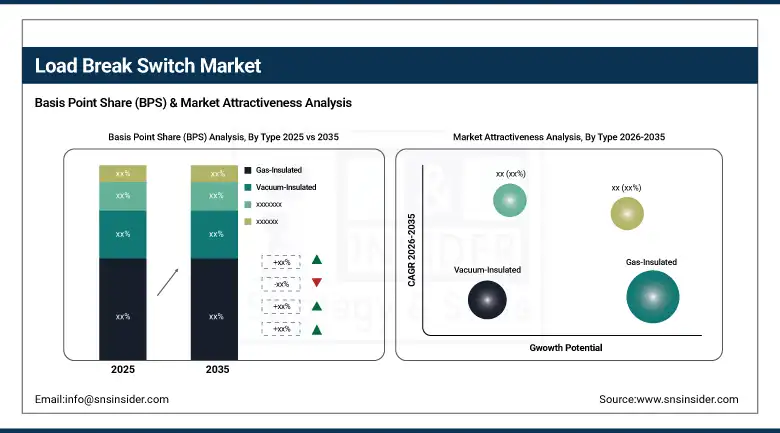

By Type, the Gas-Insulated segment dominated the Load Break Switch Market with approximately 58.40% share in 2025, while the Air-Insulated segment is the fastest growing.

-

By Voltage Level, the 15–25 kV segment dominated the Load Break Switch Market with approximately 42.60% share in 2025, while the Above 38 kV segment is the fastest growing.

-

By Operating Mechanism, the Manual segment dominated the Load Break Switch Market with approximately 61.80% share in 2025, while the Motorised/Automatic segment is the fastest growing.

-

By End User, the Utilities segment dominated the Load Break Switch Market with approximately 54.30% share in 2025, while the Renewable Energy segment is the fastest growing.

By Type, gas-insulated dominates, air-insulated grows fastest

The gas-insulated type was leading the market in 2025 owing to their excellent dielectric strength, compactness, and high reliability in operation. These switches have gained popularity across many sectors due to their ability to provide continuous operation and are mostly adopted in urban distribution systems, underground installations, and small substations where saving space is vital. The arc quenching properties of these devices allow for easy interrupting of loads as well as long-lasting service life. Nevertheless, the growing environmental awareness associated with greenhouse gases has spurred companies to explore other forms of insulating technologies, which is expected to drive future product developments.

The air-insulated switch is the most rapidly growing product type within the Load Break Switch Market, thanks to its cost efficiency, ease of installation, and reduced maintenance needs. As opposed to gas-insulated load break switches, air-insulated models don’t need any specialized gas handling equipment, reducing worries about SF6 emissions. In addition, their relatively low cost and easy operation make them a preferable choice for distribution at medium voltages. Investments in network expansion and automation of power grids are expected to boost their demand.

By End User, utilities dominate, renewable energy grows fastest

In 2025, the utilities accounted for the largest share of the global load break switch market owing to the widespread use of load break switches within medium-voltage power distribution systems. Such switches are widely employed by utilities for carrying out operations such as isolation of faults, maintenance, switching of loads, and network protection purposes, and thus, form an integral part of contemporary electrical infrastructure. In order to facilitate power distribution through distribution lines, substations, and transformers, load break switches are typically installed throughout these networks.

Renewable energy is the most rapidly growing end-user category within the Load Break Switch Market due to the booming popularity of solar and wind energy sources around the world. The increase in capital expenditures associated with large renewable energy power plants translates into an increasing demand for load break switches that can be utilized in collector substations, feeder protection circuits, and grid interconnection facilities. This type of equipment plays a crucial part in the process of secure and efficient functioning of energy generated in renewable sources.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

44.8% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

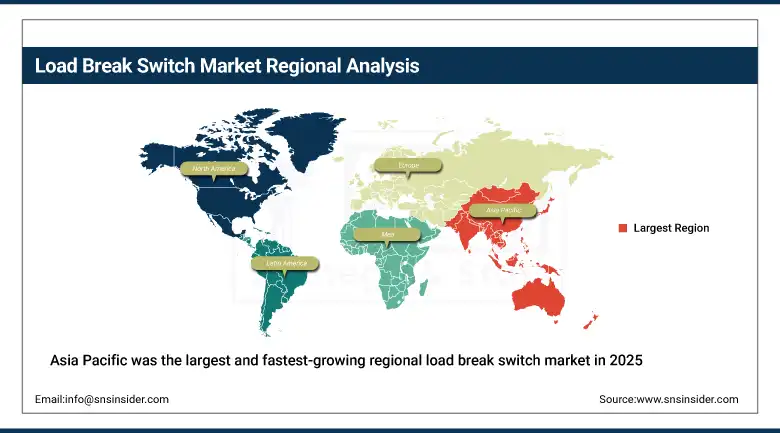

Asia Pacific Load Break Switch Market Insights

Asia Pacific was the largest and fastest-growing regional load break switch market in 2025, driven by rapid industrialisation, urbanisation, and substantial electricity infrastructure investment across China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues as both the world's largest electricity consumer and the most active investor in distribution network modernisation, whose State Grid Corporation and South Grid's smart grid programmes create the largest national load break switch procurement market globally.

India's growing electricity access programmes, distribution network quality improvement investment under the Revamped Distribution Sector Scheme, and the rapidly expanding renewable energy connection infrastructure are creating above-regional-average national market growth whose commercial momentum is progressively elevating India toward China as a load break switch market volume contributor.

Japan, South Korea, and Southeast Asian markets contribute consistent premium regional demand through their well-developed grid infrastructure, high grid reliability standards, and the progressive automation of existing distribution networks whose upgrade programmes create load break switch replacement and addition demand across mature but actively maintained grid assets.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Load Break Switch Market Insights

North America is set for rapid expansion in the load break switch market; driven by the Infrastructure Investment and Jobs Act's USD 65 billion electricity grid investment whose distribution automation and grid resilience components create systematic load break switch upgrade requirements across the U.S. utility sector.

The United States accounts for approximately 82.5% of North American revenues through its large investor-owned utility sector's capital programme investment, the growing distribution automation adoption driven by regulatory performance incentives, and the renewable energy grid connection infrastructure whose load break switch requirements are growing with each gigawatt of solar and wind capacity addition.

Europe Load Break Switch Market Insights

Europe held a significant share of the global Load Break Switch Market in 2025. Germany, France, the United Kingdom, Italy, and Spain are the leading national markets whose advanced power distribution infrastructure, high grid reliability standards, and progressive distribution automation investment create consistent and quality-sensitive load break switch demand. Germany accounts for approximately 28.5% of European revenues through its large transmission and distribution investment programme, the commercial presence of Siemens Energy and ABB's European operations, and the grid integration challenges of its high renewable energy penetration whose distribution network complexity creates automation and switching investment requirements.

The European Union's SF6 regulation whose proposed ban on SF6 in medium voltage switchgear will progressively drive load break switch product transition toward eco-friendly insulation alternatives over the 2025 to 2035 period, creating product lifecycle investment at both manufacturers developing alternative insulation designs and utilities planning equipment replacement programmes. European distribution automation investment under the EU's clean energy package is creating growing demand for motorised, remotely operable load break switch equipment at distribution substation and feeder sectionaliser level.

MEA & Latin America Load Break Switch Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class power infrastructure investment, the ambitious grid expansion programmes of Abu Dhabi and Dubai utilities, and the significant solar energy capacity addition at Noor Abu Dhabi and Mohammed Bin Rashid Al Maktoum Solar Park whose collection network load break switch requirements create substantial procurement. Saudi Arabia and Egypt contribute growing regional demand through their electricity network expansion and renewable energy grid connection programmes whose scale creates significant load break switch market development.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through the electricity distribution infrastructure investment of Enel Brasil, Energisa, and Equatorial Energia whose concession renewal programmes and distribution quality improvement obligations create systematic load break switch upgrade requirements. Chile, Colombia, and Mexico contribute growing secondary market demand through their renewable energy expansion, grid modernisation investment, and the growing adoption of distribution automation technology across their utility sectors.

Market Dynamics

Growth Drivers: Grid modernisation investment and renewable energy integration driving systematic load break switch upgrade and new installation demand globally

The market for load break switches is witnessing robust growth owing to growing investments for modernizing grids by both developed and developing countries. Distribution grids in the utility sector are being upgraded with smart and remote operated load break switches which enable automation and monitoring of the grid, help isolate faults, and restore power supply faster than ever before. The installation of such high-tech load break switches helps improve network performance and reliability.

Another factor contributing to the rapid growth of the load break switch market is the fast adoption of renewable energy sources for power generation. Renewable energy like solar power and wind energy bring challenges for the power grids in terms of bidirectional power flow, voltage fluctuations, and stability of the grid, among others. Thus, load break switches become crucial in addressing such issues.

Restraints: SF6 insulation phase-out regulatory uncertainty and the high cost of motorised switching upgrade in ageing distribution infrastructure constraining deployment economics

The switch from SF6 gas insulated load break switch is causing uncertainty in the market, especially in terms of future decisions by utility companies due to environmental regulations. Although SF6 gas insulated load break switches have been reliable, the possible restrictions that might be imposed on their use are prompting both users and manufacturers to consider other forms of insulation that include dry air, nitrogen, and vacuum. This trend is resulting in increased costs of research, development, and testing in addition to temporary problems with supply and acquisition of these switches.

Another disadvantage faced by the remotely operated and motorized load break switches is high installation costs. It is not only equipment costs that pose an obstacle for their use but also the associated communication, automation, and protective mechanisms.

Opportunities: EV charging infrastructure expansion and smart grid distribution automation programmes represent high-growth commercial frontiers for advanced load break switch adoption

With the growth of EV charging network infrastructure, there has been an emergence of many opportunities for the installation of load break switches in power distribution systems. Large-scale EV chargers need more sophisticated switching equipment to manage load balancing, fault isolation, and delivery of energy. With increasing adoption of charging stations in cities, shopping complexes, and transportation routes, utilities and operators are progressively deploying load break switches in their systems.

Moreover, the trend towards grid modernization via smarter grids has boosted the adoption of sophisticated and intelligent load break switches. Utilities are implementing self-healing grid concepts in which automatic circuit switching is used to improve fault handling. This way, the benefits of load break switches extend beyond simple circuit switching.

Recent Developments:

-

2025: Eaton Corporation launched its next-generation Cooper Form 6 recloser and load break switch integration platform for utility distribution networks, combining automatic fault restoration capability with cloud-connected analytics for outage cause prediction and maintenance scheduling optimisation.

-

2024: ABB launched enhanced SafeRing and SafePlus ring main units with integrated digital sensors for real-time fault detection and remote switching via IEC 61850 protocol, enabling utilities to upgrade existing installations with smart grid connectivity without replacing primary switchgear.

-

2023: Schneider Electric introduced its SM6 eco-design ring main unit incorporating vacuum load break switch technology with zero SF6 insulation across the complete switchgear range, providing utilities with a regulatory-compliant alternative to SF6-insulated ring main units for new substation installations and planned replacement programmes.

Load Break Switch Market Key Players

-

ABB Ltd.

-

Schneider Electric SE

-

Eaton Corporation PLC

-

Siemens Energy AG

-

General Electric Company (GE Vernova)

-

Mitsubishi Electric Corporation

-

Fuji Electric Co. Ltd.

-

Lucy Electric Group Ltd.

-

G&W Electric Company

-

Tavrida Electric AG

-

Entec Electric & Electronic Co. Ltd.

-

Tiepco International Inc.

-

Alfanar Group

-

NOJA Power Switchgear Pty Ltd.

-

Fault Current Limiter Technology Inc.

-

Hubbell Power Systems Inc.

-

S&C Electric Company

-

Cleaveland/Price Inc.

-

Alstom SA (GE Grid Solutions)

-

Ormazabal (Velatia Group)

Load Break Switch Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.75 Billion |

| Market Size by 2035 | USD 5.81 Billion |

| CAGR | CAGR of 4.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Gas-Insulated, Vacuum-Insulated, Air-Insulated, Oil-Insulated) • by Voltage Level (Below 15 kV, 15-25 kV, 25-38 kV, Above 38 kV) • by Installation (Indoor, Outdoor) • by Operating Mechanism (Manual, Motorised/Automatic) • by End User (Utilities, Industrial, Commercial, Renewable Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Schneider Electric SE, Eaton Corporation PLC, Siemens Energy AG, General Electric Company (GE Vernova), Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Lucy Electric Group Ltd., G&W Electric Company, Tavrida Electric AG, Entec Electric & Electronic Co. Ltd., Tiepco International Inc., Alfanar Group, NOJA Power Switchgear Pty Ltd., Fault Current Limiter Technology Inc., Hubbell Power Systems Inc., S&C Electric Company, Cleaveland/Price Inc., Alstom SA (GE Grid Solutions), Ormazabal (Velatia Group) |

Frequently Asked Questions

The Load Break Switch Market is expected to grow at a CAGR of 4.48% from 2026 to 2035.

The Load Break Switch Market was valued at USD 3.75 Billion in 2025.

Grid modernization, renewable energy integration, EV charging infrastructure expansion, smart grid automation deployment, and the transition toward SF6-free switching technologies are the primary factors driving growth in the Load Break Switch Market.

The Gas-Insulated segment dominated the Load Break Switch Market with the largest share in 2025 through its superior dielectric performance, compact dimensions, and maintenance-free operation advantage in utility and industrial applications, while the Air-Insulated segment is the fastest growing.

Asia Pacific was the largest and fastest-growing regional load break switch market in 2023, with China accounting for approximately 44.8%.

Get in Touch