Molded Interconnect Device (MID) Market Report Scope & Overview:

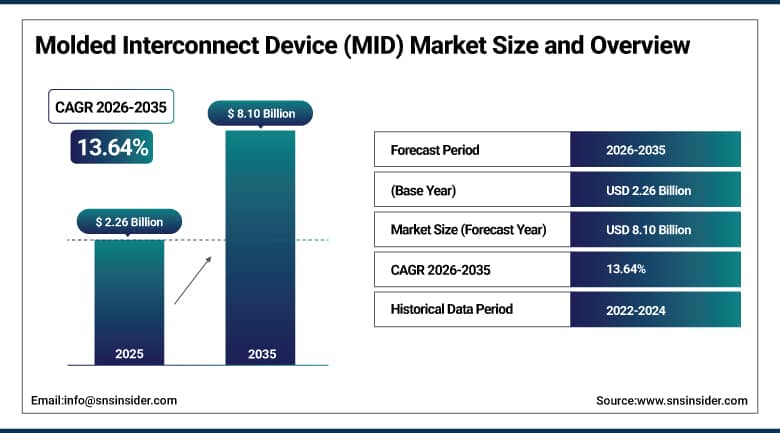

The Molded Interconnect Device (MID) Market was valued at USD 2.26 Billion in 2025 and is expected to reach USD 8.10 Billion by 2035, growing at a CAGR of 13.64% from 2026–2035.

The global molded interconnect device market is growing at an exceptional pace. Molded interconnect devices are injection-molded thermoplastic substrates with integrated conductive circuit patterns that merge mechanical and electronic functions into a single three-dimensional component, enabling manufacturers to create smaller, lighter, and more multifunctional devices that replace conventional printed circuit board and connector assemblies. The market is driven by the adoption of MID in various applications across automotive, consumer electronics, medical, and industrial sectors to provide compact and multifunctional design. MID’s maximum utilization in 5G antennas, automotive sensors, and medical devices results from its slim, cost-effective, and lightweight features, with durability in adverse conditions confirmed by reliability testing for extreme temperature, vibration, and moisture resilience.

In 2024, HARTING Technology Group expanded its MID production capability with new LDS-processed 3D-MID connectors for automotive applications, specifically targeting EV battery management system sensor integration where the combination of mechanical housing and electrical connectivity in a single LDS-structured component reduces weight, connector count, and assembly time. The development demonstrates the commercial direction of MID technology toward automotive electrification applications whose EV content growth creates above-average premium MID specification adoption.

Market Size and Forecast:

-

Market Size in 2026E: USD 2.57 Billion

-

Market Size by 2035: USD 8.10 Billion

-

CAGR: 13.64% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Molded Interconnect Device (MID) Market - Request Free Sample Report

Molded Interconnect Device (MID) Market Trends:

-

Increasing adoption of LDS technology for 5G antennas is driving MID demand by enabling compact, lightweight, and high-performance antenna integration in smartphones and telecommunications equipment

-

Growing use of MID technology in electric vehicles is supporting integration of sensors, battery management components, and connectivity systems while reducing weight and assembly complexity

-

Rising adoption of MIDs in medical wearables and implantable devices is driven by the need for miniaturization, reliability, and biocompatible electronic integration

-

Expansion of AR/VR devices is creating demand for MIDs that support advanced antenna placement, sensor integration, and precision optical alignment within compact form factors

-

Industry 4.0 and smart factory initiatives are increasing MID deployment in industrial sensors, IIoT devices, and automation systems requiring compact and multifunctional electronic components

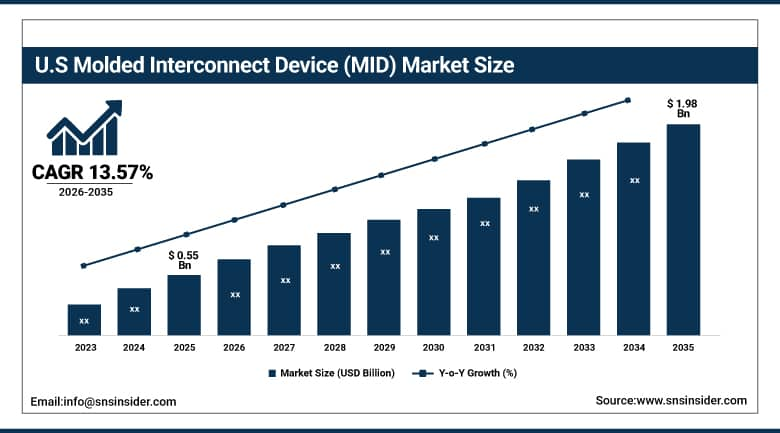

U.S. Molded Interconnect Device (MID) Market Outlook:

The U.S. Molded Interconnect Device (MID) Market was valued at approximately USD 0.55 Billion in 2025 and is expected to reach approximately USD 1.98 Billion by 2035, growing at a CAGR of approximately 13.57%.

The U.S. is the most commercially significant MID market within the fastest-growing North American region. LPKF Laser & Electronics’ LDS system commercial presence, TE Connectivity’s MID connector programme, and Molex’s 3D-MID product line collectively serve the domestic automotive, medical, and consumer electronics markets. The U.S.’s advanced automotive OEM’s EV transition, the medical device sector’s premium miniaturization specification, and the defense electronics’ compact multifunctional component requirement create the most commercially diverse national MID application deployment.

TE Connectivity launched a new line of LDS-structured MID connectors for EV thermal management systems in 2024, providing a single injection-molded thermoplastic component that integrates coolant temperature sensors, connector terminals, and mounting features into a single LDS-structured part. The product’s 40% weight reduction and 35% assembly cost reduction versus conventional multi-component alternatives demonstrates the commercial ROI that sustains automotive OEM specification motivation for premium MID solutions in EV powertrain thermal management applications.

Molded Interconnect Device (MID) Market Segment Analysis:

-

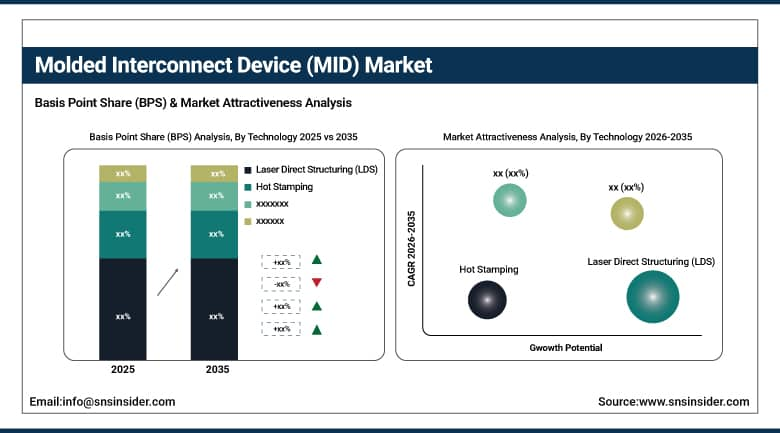

By Technology, the Laser Direct Structuring (LDS) segment dominated the Molded Interconnect Device Market with 45.2% share in 2025, while the Two-Shot Molding (2K-MID) segment is projected to have the highest CAGR.

-

By Product Type, the Antennae & Connectivity Modules segment dominated the Molded Interconnect Device Market with approximately 42% share in 2025, while the Sensors segment is the fastest growing.

-

By End-User Industry, the Automotive & EV segment dominated the Molded Interconnect Device Market with approximately 38% share in 2025, while the Consumer Electronics segment is the fastest growing.

By Technology, LDS dominates, two-shot molding grows fastest

Laser direct structuring retained the dominant technology position with 45.2% of the molded interconnect device market in 2025. LDS’s commercial primacy reflects its position as the most commercially mature and design-flexible MID manufacturing process whose laser activation of a special additive-doped thermoplastic creates precisely defined conductive track pathways on three-dimensional surfaces with circuit feature resolution that two-shot molding and hot stamping alternatives cannot match. Each LDS-structured smartphone antenna that enables multi-band 5G performance in an ultra-thin handset form factor creates OEM procurement whose aggregate across billions of annual smartphone units creates commercial scale. LPKF Laser & Electronics’ LPKF LDS system’s market leadership, Sinco Plastics’ LDS material innovation, and DSM Engineering Plastics’ Stanyl LDS compounds collectively create the LDS commercial ecosystem whose technological maturity sustains its dominant market position.

Two-shot molding is the fastest-growing technology because its cost-effective high-volume production capability, improved mechanical bond between conductive and non-conductive plastic regions, and suitability for applications requiring above-standard mechanical durability create specification preference in automotive, industrial, and consumer electronics applications where LDS’s per-unit cost premium creates ROI constraint. Each automotive switch, connector, and industrial sensor housing that specifies two-shot MID for its mechanical durability advantage creates procurement whose industrial scale volume sustains above-LDS growth rates.

By Product, antennae & connectivity modules dominate, sensors grow fastest

Antennae and connectivity modules retained the dominant product type position with approximately 42% of the molded interconnect device market in 2025. The smartphone’s multi-band 5G antenna integration using LDS-structured MID antenna substrates, IoT module’s Wi-Fi and Bluetooth antenna MID housing, and automotive telematics unit’s V2X communication antenna collectively creates the most commercially significant aggregate MID product category. Each new 5G smartphone model’s antenna design creates MID specification whose complexity compounds with 5G’s millimeter wave frequency band’s demanding antenna geometry requirement. The wireless communication ecosystem’s progressive expansion into new frequency bands and spatial multiplexing architectures creates growing per-device antenna MID complexity that sustains commercial value growth.

Sensors are the fastest-growing product because automotive ADAS radar sensor MID housing, EV battery pack temperature sensor integration, medical wearable biosensor substrate, and industrial IoT condition monitoring transducer collectively create multiple simultaneous above-average growth vectors in a single product category. Each ADAS-equipped vehicle whose radar sensor housing integrates antenna, connector, and mounting features creates premium automotive MID specification. Each implantable medical device whose biosensor requires biocompatible MID substrate creates healthcare application procurement whose regulatory compliance requirement sustains premium commercial relationships.

By End User, automotive dominates, consumer electronics grows fastest

Automotive and EV retained the dominant end-user position with approximately 38% of the molded interconnect device market in 2025. The automotive sector’s progressive electrification and ADAS feature expansion creates the most commercially concentrated premium MID procurement whose per-vehicle content increase compounds with EV adoption’s extraordinary commercial pace. Each EV battery management system’s sensor integration, ADAS radar and LiDAR housing’s connector integration, and interior ambient lighting’s LED driver MID collectively create above-average per-vehicle MID content whose commercial value compounds with the global vehicle fleet’s electrification progression. The automotive OEM’s weight reduction, assembly simplification, and reliability specification creates MID’s commercial case whose ROI measurement sustains above-conventional-component premium specification.

Consumer electronics is the fastest-growing end user because 5G smartphone’s antenna complexity, TWS wireless earphone’s miniaturization challenge, AR/VR headset’s multifunctional housing requirement, and smartwatch’s compact PCB-less sensor integration create volume MID adoption whose unit count at billions of annual consumer device shipments creates extraordinary commercial scale. Each new consumer device generation that adopts LDS-structured MID for antenna, sensor, or connector integration creates procurement whose aggregate compounds with the consumer electronics replacement cycle.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

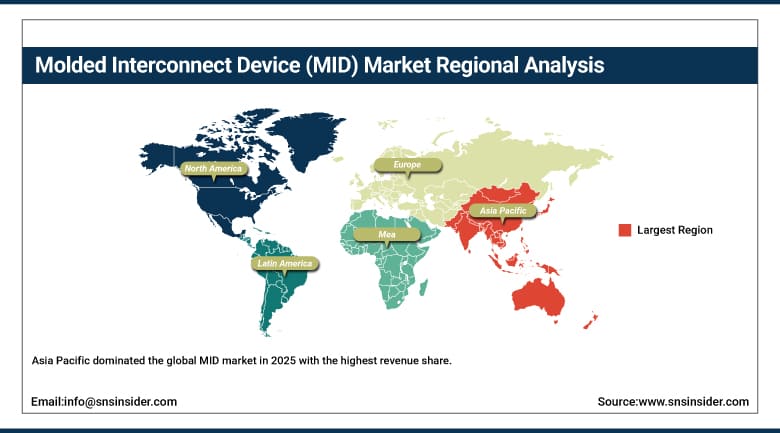

Asia Pacific Molded Interconnect Device (MID) Market Insights

Asia Pacific dominated the global MID market in 2025 with the highest revenue share, supported by its dominant electronics manufacturing ecosystem, high production capacity, and increasing investments in advanced technologies. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary smartphone manufacturing scale, the automotive industry’s EV transition, and the domestic electronics component manufacturing ecosystem.

South Korea’s Samsung and LG Electronics, Japan’s automotive and electronics industries, and India’s growing electronics manufacturing create significant secondary markets.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Molded Interconnect Device (MID) Market Insights

North America is the fastest-growing regional MID market, driven by automotive EV transition’s sensor integration demand, medical device miniaturization, and the defense electronics’ compact multifunctional component specification. The United States accounts for approximately 87.4% of North American revenues through TE Connectivity, Molex, and LPKF’s commercial operations.

Canada and Mexico contribute approximately 12.6% through the automotive manufacturing sector’s MID adoption and the electronics manufacturing base.

Europe Molded Interconnect Device (MID) Market Insights

Europe is a technically sophisticated MID market where HARTING Technology Group’s German operations, LPKF Laser & Electronics’ headquarters, and the automotive industry’s premium electronic specification create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive OEM’s MID procurement and the precision electronics industry.

France, the United Kingdom, and the Netherlands are significant secondary markets where aerospace electronics, medical device manufacturing, and automotive procurement create consistent MID demand.

MEA & Latin America MID Market Insights

UAE leads MEA revenues at approximately 38.4% through its advanced electronics manufacturing investment and the aerospace sector’s compact component specification. Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector and the growing electronics assembly industry.

Market Dynamics:

Growth Drivers: Miniaturization demand in consumer electronics and automotive EV sensor integration

The adoption of MID in automotive, consumer electronics, medical, and industrial applications to provide compact and multifunctional design is the MID market’s most commercially certain structural growth driver. Each electronic device generation that increases functional density while maintaining or reducing form factor creates MID specification motivation whose ROI measurement in component count reduction, weight saving, and assembly simplification creates economic justification. The smartphone’s progressive 5G antenna complexity increase creates per-unit LDS-structured MID demand whose premium specification sustains commercial relationships.

Automotive electrification’s extraordinary EV sensor content increase creates structural MID demand whose per-vehicle content growth compounds with EV adoption pace. Each EV’s battery management system, ADAS sensor suite, and interior HMI electronics creates MID application opportunity whose mechanical and electrical function integration creates weight and assembly cost reduction that sustains OEM specification motivation.

Restraints: High initial tooling investment and limited thermoplastic material compatibility

LDS process’ requirement for specially formulated thermoplastic compounds containing laser-activatable additives creates material selection constraint whose qualified material list limits designer freedom in thermoplastic material specification. Each application whose operating temperature, chemical exposure, or flame-retardant requirement creates material selection challenge creates engineering investment that moderates adoption pace.

Initial tooling investment for MID mold and LDS laser programming creates capital barrier for low-volume or prototype applications whose economics cannot justify MID investment over conventional PCB-plus-housing multi-component assembly.

Opportunities: 5G network equipment MID antenna and AR/VR immersive device integration

5G base station antenna panel and small cell antenna MID integration creates above-average infrastructure MID procurement whose per-installation antenna complexity creates premium LDS-structured procurement that compounds with 5G network densification investment.

AR/VR headset’s optical assembly mounting, antenna integration, and sensor housing creates premium consumer electronics MID specification whose complex 3D geometry requirement creates LDS adoption motivation that flat PCB alternatives cannot satisfy equivalently.

Recent Developments:

-

2024: HARTING Technology Group expanded its MID production capability in 2024 with new LDS-processed 3D-MID connectors for automotive EV battery management system sensor integration, achieving 40% weight reduction versus conventional multi-component assemblies.

-

2024: TE Connectivity launched a new line of LDS-structured MID connectors for EV thermal management systems in 2024, providing 40% weight reduction and 35% assembly cost reduction versus conventional multi-component alternatives in EV powertrain applications.

-

2024: LPKF Laser & Electronics expanded its LPKF Fusion3D LDS system portfolio in 2024 with enhanced throughput and resolution capability targeting high-volume 5G smartphone antenna production and automotive sensor MID manufacturing in Asia Pacific.

Molded Interconnect Device (MID) Market Key Players:

-

HARTING Technology Group

-

TE Connectivity Ltd.

-

Molex LLC

-

LPKF Laser & Electronics SE

-

Photon Dynamics

-

BCS Automotive Interface Solutions

-

Dyconex AG

-

Taoglas Group Holdings

-

Schreiner Group GmbH & Co. KG

-

Shibaura Mechatronics Corporation

-

Wuerth Elektronik GmbH & Co. KG

-

Cirtran Corporation

-

SelectConnect Technologies

-

MacDermid Alpha Electronics Solutions

-

Sinco Plastics Pte. Ltd.

-

Celanese Corporation

-

DSM Engineering Plastics

-

Lanxess AG

-

SABIC Innovative Plastics

-

RTP Company

Molded Interconnect Device (MID) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.26 Billion |

| Market Size by 2035 | USD 8.10 Billion |

| CAGR | CAGR of 13.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Technology (Laser Direct Structuring/LDS, Two-Shot Molding/2K-MID, Hot Stamping, 3D Printing/Additive Manufacturing, Others) • by Product Type (Antennae & Connectivity Modules, Connectors & Switches, Sensors, Lighting & LED Systems, Others) • by End-User Industry (Automotive & EV, Consumer Electronics, Medical Devices & Healthcare, Industrial Automation, Aerospace & Defense, Telecommunications) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | HARTING Technology Group, TE Connectivity Ltd., Molex LLC, LPKF Laser & Electronics SE, Photon Dynamics, BCS Automotive Interface Solutions, Dyconex AG, Taoglas Group Holdings, Schreiner Group GmbH & Co. KG, Shibaura Mechatronics Corporation, Wuerth Elektronik GmbH & Co. KG, Cirtran Corporation, SelectConnect Technologies, MacDermid Alpha Electronics Solutions, Sinco Plastics Pte. Ltd., Celanese Corporation, DSM Engineering Plastics, Lanxess AG, SABIC Innovative Plastics, RTP Company |

Frequently Asked Questions

The Molded Interconnect Device (MID) Market is expected to grow at a CAGR of 13.64% from 2026 to 2035.

The Molded Interconnect Device (MID) Market was valued at USD 2.26 Billion in 2025.

Adoption of MID in automotive, consumer electronics, medical, and industrial applications to provide compact and multifunctional design, with maximum utilization in 5G antennas, automotive sensors, and medical devices resulting from MID’s slim, cost-effective, and lightweight features.

Laser Direct Structuring (LDS) dominated the MID Market with 45.2% share in 2025 as confirmed by SNS Insider, while Two-Shot Molding is projected to have the highest CAGR.

Asia Pacific dominated the Molded Interconnect Device (MID) Market in 2025, while North America is the fastest-growing region.

Get in Touch