Naval ISR Market Report Scope & Overview:

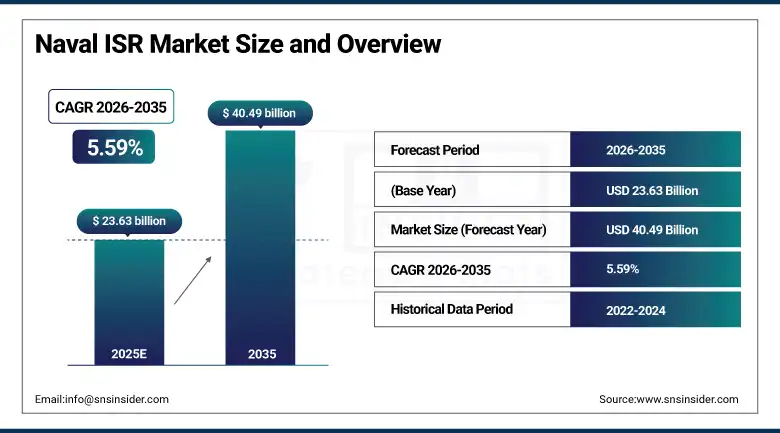

The Naval ISR Market was valued at USD 23.63 billion in 2025 and is expected to reach USD 40.49 billion by 2035, growing at a CAGR of 5.59% from 2026-2035.

The Naval ISR Market is experiencing consistent growth because of the increasing threats related to maritime security, geopolitical conflicts, and the importance of situational awareness in naval operations. Modern naval forces require advanced capabilities related to ISR in order to increase domain awareness and detect threats. Advances in technology, including the use of artificial intelligence in analytics, multi-sensor integration, satellite surveillance, unmanned aerial vehicles (UAVs), unmanned surface vehicles (USVs), unmanned underwater vehicles (UUVs), and state-of-the-art radar and electro-optic systems, are providing significant improvements in naval operations.

Supporting this trend, leading defense agencies are significantly increasing investments in maritime surveillance and reconnaissance capabilities to address evolving security challenges. For instance, the U.S. Department of Defense allocated over USD 800 billion in its recent budget cycles, with a substantial portion directed toward ISR modernization, unmanned systems, and naval intelligence programs.

In addition, regulatory and procurement bodies are accelerating the deployment of next-generation ISR technologies. The U.S. Navy continues to expand its integration of unmanned platforms and AI-enabled sensor networks under programs such as Project Overmatch, aimed at enhancing real-time data sharing and decision superiority.

Naval ISR Market Size and Forecast

-

Market Size in 2025: USD 23.63 Billion

-

Market Size by 2035: USD 40.49 Billion

-

CAGR: 5.59% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Naval ISR Market - Request Free Sample Report

Naval ISR Market Trends

-

Increasing adoption of AI-enabled analytics and multi-sensor fusion is enhancing real-time decision-making and situational awareness in naval operations.

-

Rapid deployment of unmanned platforms such as UAVs, USVs, and UUVs is transforming maritime surveillance and reconnaissance capabilities.

-

Growing focus on network-centric warfare and secure data-sharing systems is improving interoperability across naval and joint forces.

-

Rising investments by organizations like the U.S. Department of Defense are accelerating modernization of ISR infrastructure and next-generation technologies.

-

Increased emphasis on maritime domain awareness programs by alliances such as the North Atlantic Treaty Organization is strengthening coastal and deep-sea security.

-

Integration of advanced radar, electro-optical/infrared (EO/IR), and electronic warfare systems is improving threat detection accuracy.

-

Growing importance of cybersecurity in ISR systems is driving the development of resilient and secure naval communication networks.

-

Rising geopolitical tensions and protection of critical sea lanes are boosting demand for continuous naval intelligence and surveillance operations.

-

Advancements in edge computing and real-time data processing are enabling faster analysis and reduced latency in ISR missions.

U.S. Naval ISR Market Size Outlook:

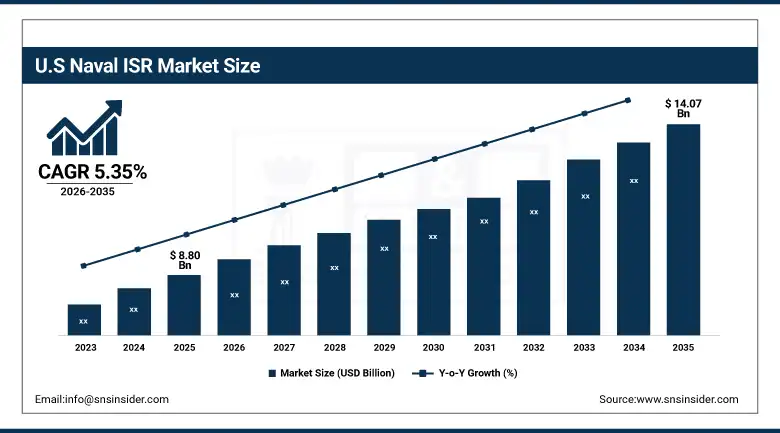

The U.S. Naval ISR Market was valued at USD 8.80 billion in 2025 and is expected to reach USD 14.07 billion by 2035, growing at a CAGR of 5.35% from 2026-2035. The U.S. Navy Intelligence, Surveillance, and Reconnaissance market is considered the largest in the world, supported by robust military expenditures, state-of-the-art naval platforms, and renowned defense manufacturers like Lockheed Martin, Northrop Grumman, Raytheon Technologies, and General Dynamics. The consistent financial backing provided by the United States Department of Defense, along with ongoing initiatives for naval modernization, is fueling the adoption of cutting-edge ISR technologies.

Supporting this trend, recent naval modernization programs highlight the accelerating shift toward unmanned and AI-enabled ISR capabilities. In April 2026, the U.S. Navy successfully conducted the first test flight of the MQ-25A Stingray unmanned aerial system, capable of carrying up to 15,000 pounds of fuel and extending the operational range of carrier-based aircraft marking a major milestone in integrating autonomous platforms into naval ISR and surveillance missions.

In addition, evolving geopolitical conflicts and real-world deployments are accelerating ISR innovation and operational use cases. The emergence of sea-drone warfare, demonstrated in regions such as the Black Sea and Middle East, has significantly increased demand for autonomous surveillance and strike capabilities, with unmanned surface vehicle deployments projected to nearly double from 2,036 units in 2025 to over 4,000 units by 2030.

Naval ISR Market Segment Highlights

-

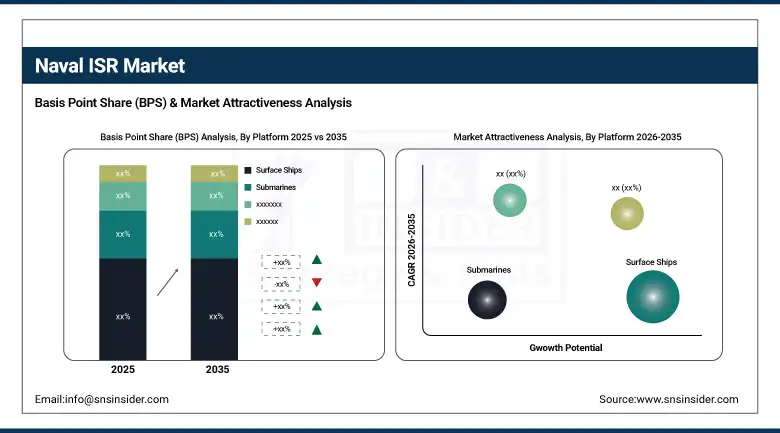

By Platform, Surface Ships dominated the Naval ISR Market with 29.78% share in 2025; Unmanned Aerial Vehicles (UAVs) fastest growing (CAGR).

-

By System Type, Radar Systems dominated the Naval ISR Market with 24.55% share in 2025; SIGINT Systems fastest growing (CAGR).

-

By Application, Surveillance dominated the Naval ISR Market with 28.68% share in 2025; Maritime Security fastest growing (CAGR).

-

By End User, Navy dominated the Naval ISR Market with 49.28% share in 2025; Coast Guard fastest growing (CAGR).

By Platform, Surface Ships segment dominates the Naval ISR Market, Unmanned Aerial Vehicles (UAVs) segment expected to grow fastest

The Surface Ships segment continued to remain the leader in the Naval ISR market in 2025, having generated revenues worth about 29.78% of the total market value. It comprises destroyers, frigates, corvettes, and patrol ships fitted with sophisticated radar, electronic warfare, sonar, and communication technologies.

The Unmanned Aerial Vehicles (UAVs) segment is expected to exhibit the fastest CAGR during 2026 to 2035 in the Naval ISR market. The increasing use of UAVs launched from carriers and ships for the purposes of intelligence, surveillance, and reconnaissance is revolutionizing maritime warfare through real-time surveillance at lower costs.

By System Type, Radar Systems segment dominates the Naval ISR Market, SIGINT Systems segment expected to grow fastest

The Radar Systems sector dominated the market share of the Naval ISR Market in 2025, capturing an estimated market revenue share of about 24.55%. This was due to the use of radar technology in detecting targets at a distance, tracking, navigation, and identifying threats in the maritime environment. Modern naval radar systems such as phased array radar and multifunctional radars have been extensively used in surface ships, submarines, and coastal areas.

Between 2026 and 2035, the SIGINT (Signals Intelligence) Systems category will post the highest CAGR. The growing need for electronic intelligence gathering and communications intercept and analysis are some of the factors driving the increasing adoption of SIGINT products and services. There is a rising demand for monitoring and analyzing signals from rival nations’ communication, radar, and electronic activity in the maritime domain.

By Application, Surveillance segment dominates the Naval ISR Market, Maritime Security segment expected to grow fastest

The Surveillance segment was the leading market contributor in 2025, representing around 28.68% of the Naval ISR Market share. The dominance of the segment can be attributed to the need for uninterrupted surveillance of marine territories such as territorial waters, exclusive economic zones (EEZs), and hazardous zones. Naval ISR systems are heavily utilized for conducting persistent surveillance missions to detect any threat, track vessels, and maintain situational awareness.

The Maritime Security segment is expected to exhibit the highest CAGR between 2026 and 2035. Growing issues associated with piracy, poaching, smuggling, terrorism, and securing crucial maritime assets have led to an increase in the demand for ISR-based maritime security solutions. Governments and defense organizations are making substantial investments in coast surveillance systems and maritime domain awareness systems.

By End User, Navy segment dominates the Naval ISR Market, Coast Guard segment expected to grow fastest

During 2025, the Navy category dominated the Naval ISR Market in terms of a notable market share of about 49.28%. This market dominance can be attributed to the massive purchases of ISR solutions by navies for their naval fleets that include surface ships, submarines, and carrier strike groups. The rising interest in ISR technology by navies is due to the requirement to conduct operations in challenging maritime situations.

The Coast Guard segment is expected to show the highest CAGR during 2026-2035. Rising responsibilities with respect to coastal surveillance, border security, search and rescue, and law enforcement activities are some of the factors behind the increased adoption of ISR solutions by coast guards. The need for cost-effective and quick response surveillance solutions in the form of UAVs and coastguard radars is contributing towards growth in this segment.

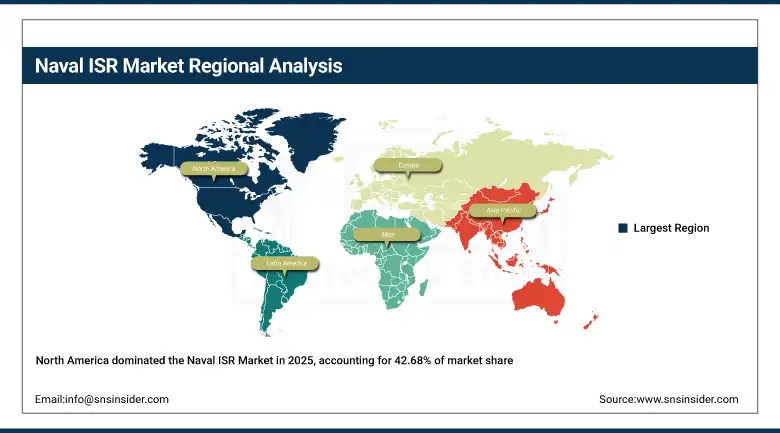

Naval ISR Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

42.68% |

|

Europe |

Germany |

25.46% |

|

Asia Pacific |

China |

21.17% |

|

Middle East & Africa |

UAE |

4.04% |

|

Latin America |

Brazil |

6.65% |

North America Naval ISR Market Insights

The North America dominated the Naval ISR market of the world with 42.68% revenue share in 2025 due to increased defense expenditure, state-of-the-art naval facilities, and presence of major contractors including Lockheed Martin and Northrop Grumman. In terms of regional performance, the US have significant amount of the North America region’s share owing to consistent naval upgrades and investment in AI-powered ISR technology. Canada also contributes meaningfully to the region’s growth, driven by its focus on coastal surveillance, Arctic security, and modernization of naval communication systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the U.S. Department of Defense continues to allocate substantial funding toward maritime intelligence and surveillance capabilities, with billions directed annually to ISR modernization, unmanned systems, and naval digital transformation programs.

In addition, Canada is strengthening its regional ISR capabilities through Arctic surveillance and maritime security initiatives. The Royal Canadian Navy is investing in next-generation surveillance systems and sensor integration programs to enhance monitoring across vast coastal and polar regions, reinforcing North America’s leadership in advanced naval ISR deployment and innovation.

Asia Pacific Naval ISR Market Insights

The Asia-Pacific region is projected to hold the largest CAGR of 6.93%, owing to fast-growing naval capabilities, increasing concerns over maritime security, and substantial defense spending. China, India, Japan, South Korea, and Australia constitute the major growth countries within the region, with China contributing the highest market revenue share in the region. The Asia-Pacific market is witnessing steady growth due to territorial conflicts, blue-water navies, and increasing maritime domain awareness within the Indo-Pacific region.

Supporting this growth, the National Development and Reform Commission has prioritized defense technology advancement, including AI-driven surveillance and unmanned maritime systems, under its strategic initiatives.

Additionally, Japan and India are significantly increasing investments in naval ISR capabilities, with programs focused on satellite surveillance, coastal radar networks, and integration of unmanned platforms, further accelerating regional adoption of advanced ISR systems.

Europe Naval ISR Market Insights

Europe emerged as the important region in terms of revenue share in the global Naval ISR market, contributing significant share in 2025, owing to high defense budget allocation, advanced naval capabilities, and regional security mechanisms within the region. Nations like Germany, UK, France, and Netherlands are at the forefront of deploying next generation ISR systems, backed by modernization initiatives in their navies along with growing concerns of maritime domain awareness in the Baltic, North Sea, and Arctic zones.

Supporting this position, the European Commission, through initiatives such as Horizon Europe, has allocated significant funding toward defense innovation, including AI-enabled surveillance systems, unmanned maritime platforms, and advanced sensor technologies.

In addition, collaborative defense efforts under the European Defence Agency are strengthening interoperability and joint ISR capabilities among member states, while evolving regulatory and procurement frameworks are enhancing standardization and accelerating deployment of advanced naval ISR solutions across Europe.

Middle East & Africa and Latin America Naval ISR Market Insights

The Middle East and Africa and Latin American regions have been witnessing gradual but consistent growth within the Naval ISR market, backed by increased defense spending, growing demands for maritime security, and greater emphasis on coastal surveillance and protection of important maritime routes. Within the MEA region, nations like Saudi Arabia, UAE, and South Africa have been at the forefront of implementing this technology owing to their policies for modernizing their defense forces and securing important strategic waterways and offshore resources. In Latin America, countries such as Brazil, Mexico, and Chile are increasingly investing in ISR capabilities to strengthen coastal defense, safeguard trade routes, and counter illicit maritime activities.

Supporting development in these regions, Saudi Arabia’s Vision 2030 includes significant investments in advanced defense technologies, including maritime surveillance systems, unmanned platforms, and integrated ISR networks to enhance national security capabilities.

In Brazil, increasing focus on maritime domain awareness and anti-smuggling operations is driving procurement of coastal radar systems, patrol vessels, and ISR technologies, supported by defense modernization programs and regional security initiatives aimed at strengthening naval and coast guard capabilities.

Naval ISR Market Growth Drivers:

-

Rising demand for real-time maritime situational awareness and threat detection is driving global adoption of advanced Naval ISR systems

The paradigm shift from platform-based warfare operations to data-centric and network-based strategies is the strongest structural force driving the growth in the Naval ISR market space. Today’s navies are in need of intelligence, surveillance, and reconnaissance solutions capable of providing continuous coverage over expansive maritime areas as well as asymmetric threats to facilitate faster and more effective decisions. As a result, defense institutions worldwide are moving towards creating an ISR capability ecosystem that will leverage technologies such as satellites, unmanned vehicles, sensors, and artificial intelligence.

Supporting this growth, the U.S. Department of Defense has significantly expanded funding for ISR modernization and unmanned maritime systems, while the U.S. Navy continues to scale deployment of UAVs, autonomous surface vessels, and integrated sensor networks, highlighting a sustained increase in ISR-driven naval operations and reinforcing the critical role of advanced surveillance capabilities in modern maritime defense.

Naval ISR Market Restraints:

-

High capital investment and lifecycle costs of advanced ISR systems creating adoption barriers, particularly for smaller naval forces and emerging economies

The considerable expense involved in acquiring, incorporating, and sustaining modern Naval ISR technologies is an important limitation to market growth. Modern ISR technologies like long-distance radars, satellites for observation, SIGINT systems, and unmanned aerial vehicles call for a huge amount of initial capital expenditure coupled with expenditures related to maintenance, software updates, data processing, and qualified staff. The issue is complicated by the requirement for a secure communication system, cyber security, and integration with the existing naval combat systems.

Naval ISR Market Opportunities:

-

Accelerating development of cost-effective unmanned systems and AI-enabled ISR technologies creating new growth pathways for broader naval adoption

The next stage of growth in the Naval ISR market is all about the democratization of cutting-edge technology in the area of surveillance, achieved via the miniaturization and cost-efficiency of technology, as well as the smart use of automation. With smaller, more affordable unmanned vehicles like UAVs, USVs, and UUVs becoming more available, smaller navies and coast guards can now benefit from ISR systems without the need to spend heavily on elaborate infrastructure.

Recent Developments:

-

2026: Lockheed Martin advanced its naval ISR portfolio through expanded deployment of AI-enabled sensor fusion and maritime surveillance systems under U.S. Navy modernization programs, enhancing real-time data integration and multi-domain operational awareness across surface and unmanned platforms.

-

2025: Northrop Grumman reported increased adoption of its MQ-4C Triton unmanned aerial system, strengthening long-endurance maritime ISR capabilities with enhanced wide-area surveillance, autonomous operations, and improved data-sharing across naval command networks.

-

2025: BAE Systems expanded its naval electronic warfare and ISR solutions by integrating advanced SIGINT and cyber-electromagnetic capabilities into maritime platforms, supporting enhanced threat detection and electronic intelligence gathering for global naval forces.

-

2025: Raytheon Technologies strengthened its radar and sensor portfolio with next-generation maritime surveillance systems, including upgrades to AESA radar technologies and integrated ISR solutions, improving target tracking accuracy and situational awareness in complex naval environments.

Naval ISR Companies are:

-

Northrop Grumman

-

BAE Systems

-

Raytheon Technologies

-

General Dynamics

-

Thales Group

-

Saab AB

-

Elbit Systems

-

L3Harris Technologies

-

Boeing Defense

-

Airbus Defence and Space

-

Naval Group

-

Huntington Ingalls Industries

-

Israel Aerospace Industries (IAI)

-

Mitsubishi Heavy Industries

-

Rolls-Royce Defense

-

ST Engineering

-

Kongsberg Gruppen

-

Ultra Electronics

Naval ISR Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.63 Billion |

| Market Size by 2035 | USD 40.49 Billion |

| CAGR | CAGR of 5.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Surface Ships, Submarines, Unmanned Aerial Vehicles (UAVs), Unmanned Underwater Vehicles (UUVs), Satellites, Others), • By System Type (Radar Systems, Electro-Optical / Infrared (EO/IR) Systems, Acoustic / Sonar Sensors, SIGINT Systems, Communication Systems, Electronic Warfare Systems, Others), • By Application (Surveillance, Reconnaissance, Target Acquisition, Battle Damage Assessment, Maritime Security, Communication Relay, Others), • By End User (Navy, Coast Guard, Marine Corps, Defense Intelligence Agencies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin, Northrop Grumman, BAE Systems, Raytheon Technologies, General Dynamics, Thales Group, Leonardo S.p.A., Saab AB, Elbit Systems, L3Harris Technologies, Boeing Defense, Airbus Defence and Space, Naval Group, Huntington Ingalls Industries, Israel Aerospace Industries (IAI), Mitsubishi Heavy Industries, Rolls-Royce Defense, ST Engineering, Kongsberg Gruppen, Ultra Electronics. |

Frequently Asked Questions

The Naval ISR Market is expected to grow at a CAGR of 5.59% from 2026 to 2035.

The Naval ISR Market was valued at USD 23.63 billion in 2025.

The major growth factor driving the Naval ISR market is the increasing need for enhanced maritime domain awareness and real-time situational intelligence.

The Radar Systems segment dominated the Naval ISR Market in 2025.

North America dominated the Naval ISR Market in 2025.

Get in Touch