Neurostimulation Devices Market Report Scope & Overview:

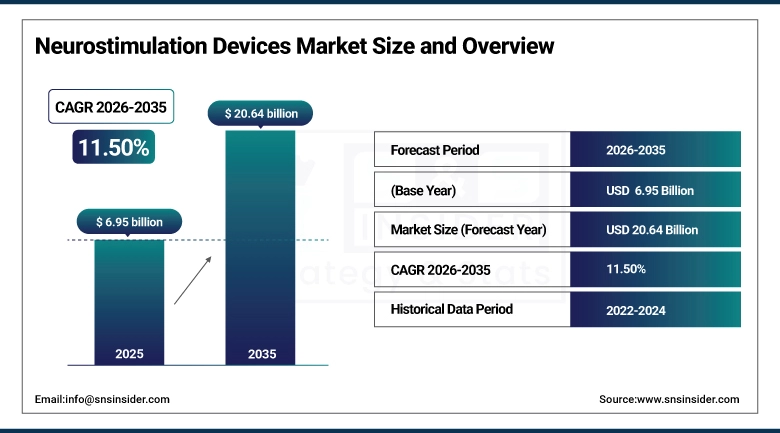

The Neurostimulation Devices Market was estimated at USD 6.95 billion in 2025 and is expected to reach USD 20.64 billion by 2035 and grow at a CAGR of 11.50% over the forecast period of 2026-2035.

The neurostimulation devices market is expanding due to the increasing prevalence of chronic pain, neurological disorders, and movement-related conditions such as Parkinson’s disease and epilepsy. Rising adoption of advanced implantable and non-invasive neurostimulation technologies, combined with growing awareness among patients and healthcare providers, is driving demand. Additionally, technological innovations, improved reimbursement policies, and the shift toward minimally invasive therapies are fueling market growth, making neurostimulation devices an increasingly preferred treatment option across the U.S. healthcare sector.

84% of U.S. healthcare providers integrated neurostimulation devices into standard care pathways propelled by rising neurological disease burden, technological advances, and favorable reimbursement shifts establishing neuromodulation as a cornerstone of modern, minimally invasive therapy.

Market Size and Forecast

-

Market Size in 2025: USD 6.95 Billion

-

Market Size by 2035: USD 20.64 Billion

-

CAGR: 11.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

Neurostimulation Devices Market Trends

-

Rising adoption of spinal cord and deep brain stimulators for chronic pain and neurological disorder management

-

Integration of AI and remote monitoring features to improve patient outcomes and device personalization

-

Growing preference for minimally invasive implantation techniques to reduce recovery time and surgical complications

-

Expansion of applications across Parkinson’s disease, epilepsy, depression, and other neurological disorder treatments

-

Increasing demand for rechargeable and MRI-compatible neurostimulation devices enhancing patient convenience and treatment flexibility

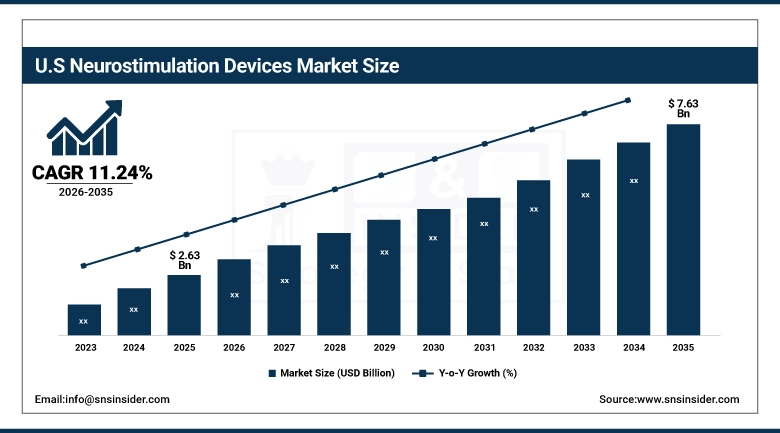

The U.S. Neurostimulation Devices Market is valued at USD 2.63 billion in 2025 and is expected to reach USD 7.63 billion by 2035, growing at a CAGR of 11.24% from 2026-2035.

The U.S. neurostimulation devices market is growing due to rising cases of chronic pain, neurological disorders, and movement-related conditions. Increased adoption of advanced implantable and non-invasive devices, coupled with technological advancements and greater awareness among healthcare providers and patients, is driving demand and market expansion.

Neurostimulation Devices Market Growth Drivers:

-

Rising prevalence of neurological disorders, chronic pain, and movement disorders is driving demand for neurostimulation devices as effective, long-term therapeutic solutions

The global rise in conditions such as Parkinson’s disease, epilepsy, chronic back pain, and migraine is significantly increasing demand for neurostimulation therapies. Neurostimulation devices, including spinal cord stimulators, deep brain stimulators, and vagus nerve stimulators, offer effective, long-term management of symptoms where conventional therapies may fail. Growing awareness among physicians and patients about these therapies, coupled with increasing healthcare expenditure and better access to specialized treatment centers, is fueling market adoption. Both developed and emerging markets are witnessing higher acceptance, as these devices improve quality of life and provide an alternative to lifelong medication dependency.

82% of neurology practices reported increased demand for neurostimulation devices driven by the rising global burden of neurological disorders, chronic pain, and movement conditions solidifying their role as essential long-term therapeutic solutions.

-

Technological advancements in implantable and non-invasive neurostimulation systems are improving treatment efficacy, patient outcomes, and expanding clinical applications worldwide

Recent innovations in neurostimulation technology, such as rechargeable implantable devices, wearable stimulators, and non-invasive transcutaneous systems, are enhancing treatment precision and safety. Advanced programming capabilities and closed-loop systems allow personalized stimulation therapy, improving patient outcomes and reducing side effects. Additionally, the development of minimally invasive and outpatient-compatible devices has expanded adoption in clinical practice. These technological improvements are encouraging physicians to recommend neurostimulation therapies more frequently and support broader applications for movement disorders, chronic pain, and psychiatric conditions. Continuous innovation drives confidence among patients and healthcare providers, boosting global market growth.

79% of neurology and pain management centers adopted next-generation implantable and non-invasive neurostimulation systems enhancing treatment precision, reducing recovery times, and broadening clinical use across conditions like depression, epilepsy, and chronic pain.

Neurostimulation Devices Market Restraints:

-

High device costs, surgical risks, and limited reimbursement coverage restrict adoption of neurostimulation therapies, particularly in cost-sensitive and developing healthcare markets

Neurostimulation devices are often expensive, with high upfront costs for implants, surgeries, and follow-up programming. Surgical procedures carry risks such as infection, device migration, or neurological complications, which can deter patients. Additionally, limited or inconsistent insurance reimbursement in certain regions increases out-of-pocket expenses, making these therapies inaccessible for many. These financial and clinical barriers are particularly pronounced in developing economies, where healthcare infrastructure and funding are limited. Consequently, market growth may be slower in cost-sensitive areas despite rising clinical demand, restricting the widespread adoption of neurostimulation therapies globally.

73% of patients in cost-sensitive and developing markets faced barriers to neurostimulation therapy due to high device costs, surgical risks, and insufficient reimbursement limiting widespread clinical adoption despite therapeutic benefits.

-

Stringent regulatory approvals and lengthy clinical validation processes delay product commercialization and increase development costs for neurostimulation device manufacturers

Neurostimulation devices must undergo rigorous clinical trials and obtain regulatory approvals from authorities such as the FDA, CE, or equivalent national agencies. The process is time-consuming and expensive, involving multiple phases of testing to ensure safety and efficacy. Delays in approvals can postpone product launches, affect revenue timelines, and increase research and development costs. Compliance with varying regulatory requirements across countries further complicates market entry. These factors may discourage smaller manufacturers from entering the market and can slow overall innovation and adoption rates, posing challenges for the growth of the neurostimulation devices industry.

75% of neurostimulation device manufacturers experienced delayed market entry due to stringent regulatory requirements and prolonged clinical validation adding an average of 18–24 months to development timelines and significantly increasing R&D expenditures.

Neurostimulation Devices Market Opportunities:

-

Growing geriatric population and increasing awareness of neuromodulation therapies create opportunities for expanded use of neurostimulation devices across multiple neurological indications

The aging global population is more susceptible to chronic pain, movement disorders, and neurological diseases, creating a larger patient pool for neurostimulation therapies. Increased awareness among healthcare providers and patients about the benefits of neuromodulation has also expanded treatment adoption. Neurostimulation devices are being recognized as alternatives to pharmacological therapies, particularly for patients with treatment-resistant conditions. Expanding use cases across epilepsy, Parkinson’s, depression, and migraine management provide manufacturers opportunities to target diverse clinical indications. Demographic trends combined with better disease diagnosis and awareness campaigns are expected to drive long-term market growth globally.

80% of neurology clinics expanded neurostimulation therapy adoption driven by a growing geriatric population and heightened awareness extending use across epilepsy, Parkinson’s, chronic pain, and other neurological conditions.

-

Rising investments in research, personalized medicine, and minimally invasive technologies present opportunities for innovation and next-generation neurostimulation device development globally

Significant R&D funding from private investors, government grants, and healthcare institutions is accelerating the development of advanced neurostimulation solutions. Personalized devices, closed-loop systems, and minimally invasive procedures are transforming patient care by improving precision, safety, and treatment outcomes. Additionally, integration with digital health technologies and remote monitoring enhances device utility and patient compliance. These innovations open avenues for product differentiation and market expansion, especially in emerging and untapped regions. Companies investing in next-generation neurostimulation technologies can gain competitive advantage, improve patient adoption, and contribute to sustainable growth in the global neurostimulation devices market.

78% of neurotechnology firms accelerated next-generation neurostimulation device development leveraging advances in personalized medicine, minimally invasive techniques, and targeted neuromodulation to meet evolving clinical demands.

Neurostimulation Devices Market Segmentation Analysis

-

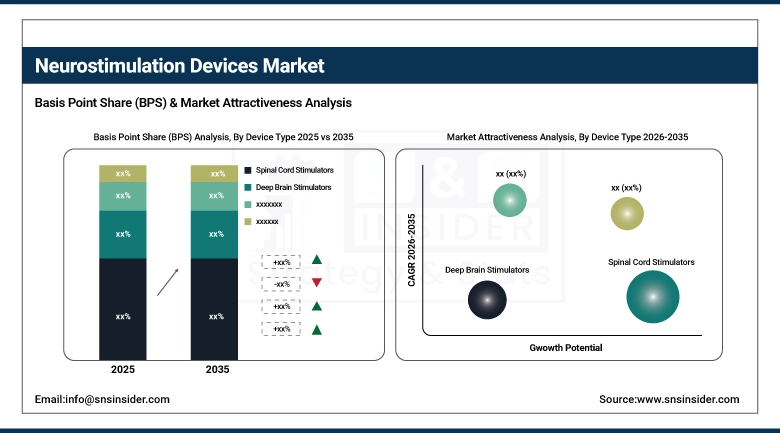

By Device Type: Spinal Cord Stimulators led with 39.6% share, while Deep Brain Stimulators is the fastest-growing segment with CAGR of 15.8%.

-

By Technology: Implantable Neurostimulation Devices led with 63.2% share, while Wearable Neurostimulation Devices is the fastest-growing segment with CAGR of 16.4%.

-

By Application: Chronic Pain Management led with 44.9% share, while Depression is the fastest-growing segment with CAGR of 17.1%.

-

By End User: Hospitals led with 52.7% share, while Ambulatory Surgical Centers is the fastest-growing segment with CAGR of 15.3%.

By Device Type: Spinal Cord Stimulators led, while Deep Brain Stimulators is the fastest-growing segment.

Spinal Cord Stimulators dominate the neurostimulation devices market due to their extensive clinical use in managing chronic and neuropathic pain conditions. Their proven efficacy, long-term safety profile, and growing adoption in pain management protocols make them the preferred choice among clinicians. Increasing prevalence of spinal injuries, failed back surgery syndrome, and degenerative disc diseases further supports demand. Technological advancements such as rechargeable systems, MRI-compatible designs, and improved programming capabilities have enhanced patient outcomes, reinforcing their strong presence across hospitals and specialty pain clinics globally.

Deep Brain Stimulators are the fastest-growing device segment owing to rising incidence of neurological disorders such as Parkinson’s disease, essential tremor, and dystonia. Increasing clinical acceptance of neuromodulation for movement and psychiatric disorders, combined with expanding indications and improved surgical precision, is driving adoption. Advancements in targeting accuracy, adaptive stimulation, and minimally invasive implantation techniques are improving therapeutic outcomes. Growing investments in neuroscience research and expanding access to advanced neurological care, particularly in emerging Asian markets, are further accelerating growth in this segment.

By Technology: Implantable Neurostimulation Devices led, while Wearable Neurostimulation Devices is the fastest-growing segment.

Implantable Neurostimulation Devices lead the market because they offer continuous, precise, and long-term therapeutic stimulation for chronic neurological and pain-related conditions. Their ability to deliver targeted neuromodulation with programmable settings makes them highly effective for complex disorders requiring sustained treatment. Strong clinical evidence, reimbursement support in developed regions, and widespread physician familiarity contribute to dominance. Additionally, innovations such as closed-loop systems, miniaturized implants, and longer battery life have improved patient compliance and outcomes, reinforcing the preference for implantable technologies across major healthcare institutions.

Wearable Neurostimulation Devices represent the fastest-growing technology segment due to rising demand for non-invasive, patient-friendly, and home-based treatment options. These devices are increasingly used for pain management, depression, migraine, and rehabilitation therapies. Their portability, ease of use, and integration with mobile health platforms enhance patient adherence and monitoring. Growing preference for outpatient care, reduced procedural risks, and increasing availability of FDA-cleared wearable solutions are accelerating adoption. Rapid technological advancements and expanding consumer awareness are particularly driving growth in Asia and other emerging healthcare markets.

By Application: Chronic Pain Management led, while Depression is the fastest-growing segment.

Chronic Pain Management dominates the application segment as neurostimulation has become a critical alternative to long-term opioid therapy. Rising prevalence of chronic back pain, neuropathic pain, and post-surgical pain conditions has significantly increased demand. Neurostimulation offers sustained relief, improved quality of life, and reduced dependence on pharmaceuticals. Strong clinical evidence, physician preference, and growing adoption of spinal cord and peripheral nerve stimulators reinforce leadership. Favorable reimbursement policies in North America and Europe further support continued dominance of this application segment.

Depression is the fastest-growing application segment due to increasing recognition of neurostimulation as an effective therapy for treatment-resistant cases. Rising global mental health burden, growing awareness, and expanding clinical evidence supporting vagus nerve and deep brain stimulation are driving adoption. Advances in neuromodulation targeting emotional and cognitive circuits have improved outcomes. Additionally, reduced stigma, greater acceptance of device-based mental health therapies, and increasing investment in psychiatric neuromodulation research especially in Asia are accelerating growth within this application segment.

By End User: Hospitals led, while Ambulatory Surgical Centers is the fastest-growing segment.

Hospitals dominate the end-user segment as they are the primary centers for complex neurostimulation procedures requiring advanced infrastructure, skilled neurosurgeons, and multidisciplinary care teams. They handle high patient volumes for implantation, post-operative management, and long-term follow-up. Availability of advanced imaging, surgical navigation systems, and intensive care facilities supports widespread adoption. Strong reimbursement coverage and established clinical pathways further reinforce hospitals as the leading end-user for neurostimulation devices across both developed and developing healthcare systems.

Ambulatory Surgical Centers are the fastest-growing end-user segment due to the shift toward minimally invasive procedures and cost-effective outpatient care. Advances in neurostimulation implantation techniques have reduced procedure time and recovery duration, making ASCs a viable option. Patients benefit from shorter hospital stays, lower costs, and faster recovery. Increasing investments in specialized outpatient surgical facilities and growing acceptance of same-day neurostimulation procedures are driving rapid adoption, particularly in Asia and other regions focused on healthcare efficiency and accessibility.

Regional Insights

North America Neurostimulation Devices Market Insights:

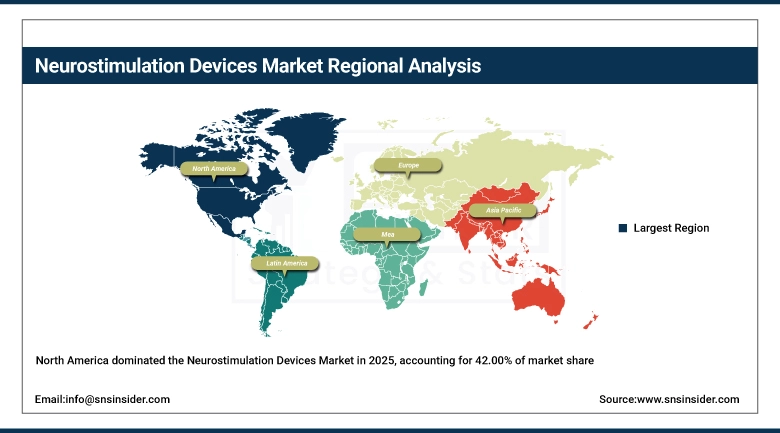

North America dominated the Neurostimulation Devices Market with a 42.00% share in 2025 due to advanced healthcare infrastructure, high prevalence of chronic pain and neurological disorders, and strong adoption of innovative neurostimulation technologies. Supportive reimbursement policies, presence of leading device manufacturers, and growing awareness among patients and physicians further reinforced the region’s market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Neurostimulation Devices Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 14.04% from 2026–2035, driven by increasing incidence of neurological disorders, rising healthcare expenditure, and expanding access to advanced medical technologies. Rapid adoption of minimally invasive procedures, growing awareness of neurostimulation benefits, and government initiatives to enhance healthcare infrastructure are accelerating market growth across the region.

Europe Neurostimulation Devices Market Insights

Europe held a significant share in the Neurostimulation Devices Market in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive therapies, and growing prevalence of chronic pain and neurological disorders. Strong reimbursement systems, technological innovation by leading device manufacturers, and increasing patient awareness further reinforced Europe’s market position.

Middle East & Africa and Latin America Neurostimulation Devices Market Insights

The Middle East & Africa and Latin America together showed steady growth in the Neurostimulation Devices Market in 2025, driven by improving healthcare infrastructure, rising prevalence of neurological disorders, and increasing adoption of advanced neurostimulation therapies. Government initiatives, growing investments in medical technology, and expanding awareness among healthcare providers and patients contributed to the regions’ emerging market presence.

Competitive Landscape:

Medtronic plc

Medtronic plc is a global leader in medical technology, offering a broad range of neurostimulation devices for pain management, movement disorders, and neurological conditions. Its portfolio includes spinal cord stimulators, deep brain stimulators, and peripheral nerve stimulators. Medtronic focuses on innovation, patient safety, and advanced clinical research, delivering devices that improve quality of life. With a strong global presence and extensive healthcare partnerships, Medtronic continues to expand access to neurostimulation therapies across both developed and emerging markets worldwide.

-

May 2024, Medtronic received FDA approval for the Intellis Plus Spinal Cord Stimulation (SCS) System, featuring AdaptiveStim AI that automatically adjusts therapy based on body position and activity.

Boston Scientific Corporation

Boston Scientific Corporation is a leading medical device company specializing in neuromodulation and neurostimulation solutions. Its offerings include spinal cord stimulators, peripheral nerve stimulators, and deep brain stimulators designed to manage chronic pain and neurological disorders. The company emphasizes cutting-edge technology, minimally invasive procedures, and patient-centered innovation. Boston Scientific collaborates with healthcare providers globally to ensure effective treatment outcomes, while investing in research and clinical trials to continuously advance neurostimulation therapies and expand treatment accessibility worldwide.

-

October 2023, Boston Scientific launched the WaveWriter Alpha SCS System with Tempore Sensing, the industry’s first real-time neural sensing and stimulation platform for personalized pain relief.

Abbott Laboratories

Abbott Laboratories is a diversified healthcare company developing advanced neurostimulation devices for pain management and neurological conditions. Its neuromodulation portfolio includes spinal cord stimulators, vagus nerve stimulators, and other implantable systems that enhance patient comfort and mobility. Abbott focuses on innovation, safety, and clinical efficacy, conducting rigorous trials and research to optimize therapy outcomes. With a strong international footprint, the company aims to improve quality of life for patients worldwide, offering scalable, patient-friendly neurostimulation solutions across multiple therapeutic areas.

-

January 2025, Abbott expanded access to its Proclaim Dorsal Root Ganglion (DRG) Neurostimulation System, receiving CE Mark and FDA approval for broadened use in chronic lower limb pain, including Complex Regional Pain Syndrome (CRPS) and post-amputation pain.

Neurostimulation Devices Market Key Players

-

Medtronic plc

-

Boston Scientific Corporation

-

Abbott Laboratories

-

LivaNova PLC

-

Nevro Corp.

-

NeuroPace, Inc.

-

Aleva Neurotherapeutics SA

-

Synapse Biomedical Inc.

-

Neuronetics, Inc.

-

NeuroSigma, Inc.

-

Biocontrol Medical

-

ElectroCore, Inc.

-

SPR Therapeutics

-

Soterix Medical Inc.

-

Sapiens Neuro

-

BrainsWay Ltd.

-

Saluda Medical Pty Ltd.

-

Nalu Medical, Inc.

-

Sceneray Corporation

-

Renishaw Plc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.95 Billion |

| Market Size by 2035 | USD 20.64 Billion |

| CAGR | CAGR of 11.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type (Spinal Cord Stimulators, Deep Brain Stimulators, Vagus Nerve Stimulators, Sacral Nerve Stimulators, Gastric Electrical Stimulators) • By Technology (Implantable Neurostimulation Devices, External Neurostimulation Devices, Wearable Neurostimulation Devices) • By Application (Chronic Pain Management, Parkinson’s Disease, Epilepsy, Depression, Urinary & Fecal Incontinence) • By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, LivaNova PLC, Nevro Corp., NeuroPace, Inc., Aleva Neurotherapeutics SA, Synapse Biomedical Inc., Neuronetics, Inc., NeuroSigma, Inc., Biocontrol Medical, ElectroCore, Inc., SPR Therapeutics, Soterix Medical Inc., Sapiens Neuro, BrainsWay Ltd., Saluda Medical Pty Ltd., Nalu Medical, Inc., Sceneray Corporation, Renishaw Plc. |

Frequently Asked Questions

North America dominated the Neurostimulation Devices Market in 2025 with a 42.00% share, due to advanced healthcare infrastructure and high adoption of neurostimulation therapies.

Spinal Cord Stimulators by device type, Implantable Devices by technology, Chronic Pain Management by application, and Hospitals by end user dominated the market.

Rising prevalence of chronic pain, Parkinson’s disease, epilepsy, and other neurological disorders, along with advanced implantable and non-invasive technologies, is fueling global market expansion.

The global Neurostimulation Devices Market is valued at USD 6.95 billion in 2025, driven by chronic pain, neurological disorders, and increasing adoption of advanced neuromodulation therapies.

The Neurostimulation Devices Market is expected to grow at a CAGR of 11.50% from 2026 to 2033 due to rising neurological disorders and technological adoption.

Get in Touch