Optical Satellite Communication Market Report Scope & Overview:

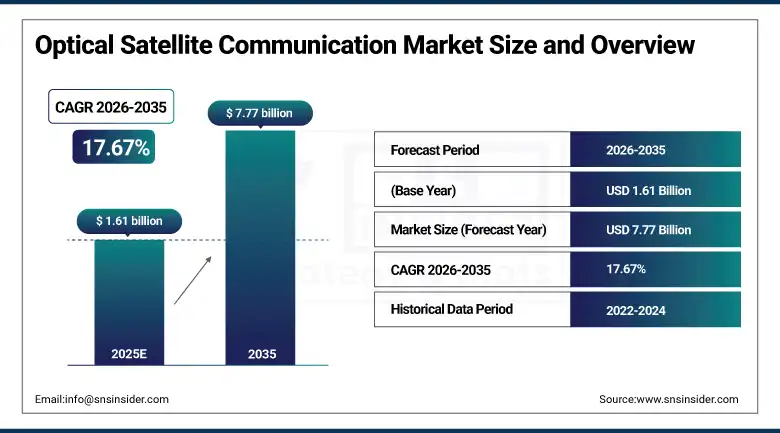

The Optical Satellite Communication Market was valued at approximately USD 1.61 billion in 2025 and is expected to reach around USD 7.77 billion by 2035, growing at a CAGR of 17.67% from 2026–2035.

Optical Satellite Communication Market is experiencing fast growth owing to the increasing demand for highly advanced, ultra-fast and highly secured space-based communication network solutions from various application areas. The increasing utilization of LEO mega constellations, the growing requirement for highly efficient Inter-Satellite Link (ISL), and high reliance on laser communication system are drastically transforming the structure of satellite communication market worldwide.

Supporting this trend, NASA has significantly advanced optical communication validation through missions such as the Laser Communications Relay Demonstration (LCRD) and the Integrated LCRD Low Earth Orbit User Modem and Amplifier Terminal (ILLUMA-T) launched to the International Space Station in 2023, demonstrating multi-Gbps optical data transmission capabilities from space to ground.

In parallel, the European Space Agency (ESA) has accelerated optical terminal development through projects such as the European Data Relay System (EDRS), which already enables laser-based inter-satellite links between LEO satellites and GEO relay satellites, significantly improving real-time Earth observation data transfer.

Optical Satellite Communication Market Size and Forecast

-

Market Size in 2025: USD 1.61 Billion

-

Market Size by 2035: USD 7.77 Billion

-

CAGR: 17.67% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Optical Satellite Communication Market - Request Free Sample Report

Optical Satellite Communication Market Trends

-

Rising deployment of laser-based inter-satellite links (ISLs) is significantly improving data throughput and enabling near real-time global satellite connectivity.

-

Increasing adoption of free-space optical (FSO) communication systems is enhancing secure, high-bandwidth space-to-space and space-to-ground transmission capabilities.

-

Rapid integration of AI-enabled beam steering, adaptive optics, and precision tracking systems is improving link stability and reducing signal degradation in dynamic orbital environments.

-

Growing focus on LEO mega-constellations equipped with optical payloads is accelerating demand for scalable, low-latency global broadband infrastructure.

-

Expanding investments in quantum-secure optical communication and encrypted laser links are strengthening defense-grade and cyber-resilient space communication networks.

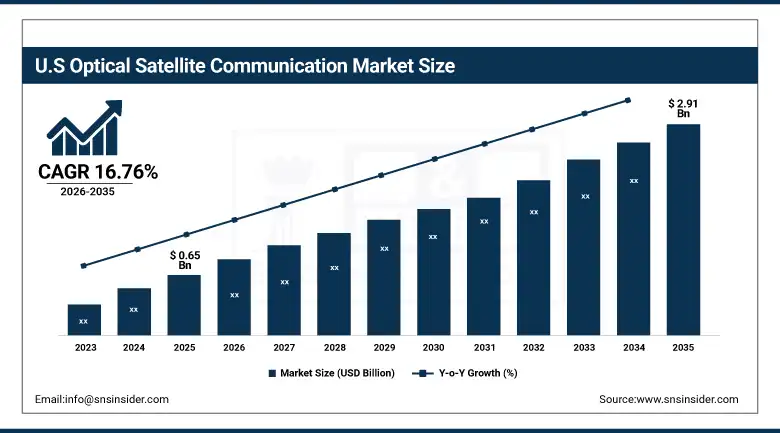

U.S. Optical Satellite Communication Market was valued at USD 0.65 billion in 2025 and is expected to reach USD 2.91 billion by 2035, growing at a CAGR of 16.76% from 2026-2035.

The US Optical Satellite Communication Market is the pioneer of innovations around the world with substantial involvement from key participants like SpaceX, Boeing, Northrop Grumman, L3Harris Technologies, and Viasat, along with high-level integration in the US defense sector and NASA’s satellite communication initiatives. Growing investment in laser communications technology by the Department of Defense and US Space Force to ensure security against jamming attacks is propelling the development of optical intersatellite communication solutions.

Supporting this trend, NASA’s successful demonstrations of multi-Gbps laser communication through the LCRD and ILLUMA-T missions (2023–2024) have validated high-speed optical data transfer from space to Earth, marking a major milestone for next-generation satellite communications.

In addition, the U.S. Space Force’s ongoing testing of optical crosslink-enabled LEO satellite architectures in 2024 highlights accelerating regulatory and operational adoption of laser-based space communication systems, reinforcing the U.S. as the global hub for optical satellite communication innovation.

Optical Satellite Communication Market Segment Highlights

-

By Component, Laser Communication Terminals dominated the Optical Satellite Communication Market with 34.36% share in 2025; Laser Communication Terminals is the fastest growing segment.

-

By Orbit Type, Low Earth Orbit (LEO) dominated the Optical Satellite Communication Market with 46.45% share in 2025; Geostationary Orbit (GEO) is the fastest growing segment CAGR.

-

By Application, Inter-Satellite Links (ISL)dominated the Optical Satellite Communication Market with 31.85% share in 2025; Broadband Internet / Data Relay is the fastest growing segment.

-

By End User, Commercial dominated the Optical Satellite Communication Market with 39.24% share in 2025; Space Agencies is the fastest growing segment.

-

By Data Rate, 1–10 Gbps dominated the Optical Satellite Communication Market with 41.24% share in 2025; Above 10 Gbps is the fastest growing segment.

Optical Satellite Communication Market Segment Analysis

By Component, Laser Communication Terminals segment dominates the Optical Satellite Communication Market, Laser Communication Terminals segment also expected to grow fastest.

The Laser Communication Terminals segment accounted for the largest market share of 34.36% in 2025, backed by its importance in supporting high-bandwidth, low-latency laser communications between satellites, as well as its widespread usage within LEO mega-constellation systems and advanced secure communication systems. The growing development of space-based broadband infrastructure along with the rising need for high-speed optical payloads will drive the dominance of the product line within the industry.

The same Laser Communication Terminals segment is projected to witness the fastest CAGR from 2026 to 2035, aided by the quick development of optical inter-satellite connections, increasing penetration into advanced satellite constellations, and constant innovations in laser communication technologies.

By Orbit Type, Low Earth Orbit (LEO) segment dominates the Optical Satellite Communication Market, Geostationary Orbit (GEO) segment expected to grow fastest.

LEO held the largest market share of 46.45% in 2025 due to the fast-paced launch of mega-constellation satellites that support broadband internet services, earth observation services, and live data relays. The relatively short distance between the Earth’s surface and LEO facilitates effective optical communications via laser links that have minimal latency, making LEO the optimal constellation type for both private satellite companies and defense reconnaissance systems.

GEO is expected to register the highest CAGR during the forecast period 2026-2035 owing to the increasing need for seamless global coverage and the use of GEO satellites as optical relay satellites.

By Application, Inter-Satellite Links (ISL) segment dominates the Optical Satellite Communication Market, Broadband Internet / Data Relay segment expected to grow fastest.

By Application, Inter-Satellite Links (ISL) segment dominates Broadband Internet / Data Relay segment to record highest CAGR. In terms of market share, the Inter-Satellite Links (ISL) segment held a market share of 31.85% in 2025, primarily due to its critical importance in facilitating satellite mesh networks at ultra-high speeds using lasers and removing reliance on ground stations.

The Broadband Internet / Data Relay segment is projected to witness the fastest CAGR from 2026 to 2035 fueled by rapidly growing worldwide demand for high-speed internet in outer space, rising digital access programs in remote and poorly connected areas, and the widespread launch of satellite internet constellations.

By End User, Commercial Satellite Operators segment dominates the Optical Satellite Communication Market, Space Agencies segment expected to grow fastest.

The Commercial Satellite Operators segment held the largest market share of 39.24% in 2025, owing to the quick adoption of large LEO mega constellations that offer services such as global broadband internet, earth observation, and inter-satellite optical mesh network. The growing involvement of private players in the space industry has led to a significant rise in the installation of laser communication terminals on satellites.

The Space Agencies segment is projected to achieve the highest growth rate during 2026–2035.

By Data Rate, 1–10 Gbps segment dominates the Optical Satellite Communication Market, above 10 Gbps segment expected to grow fastest.

The 1–10 Gbps market category captured the largest market share of 41.24% in 2025 due to its extensive use in present-generation low Earth orbit satellite constellations and intersatellite optical communication links. The range of data rates from 1-10 Gbps provides an ideal balance among factors such as efficiency, power requirements, and technological complexity, thus making it well suited for application in satellites used for observing Earth, as well as broadband relay and communication purposes.

The Above 10 Gbps segment is projected to achieve the highest growth rate during 2026–2035

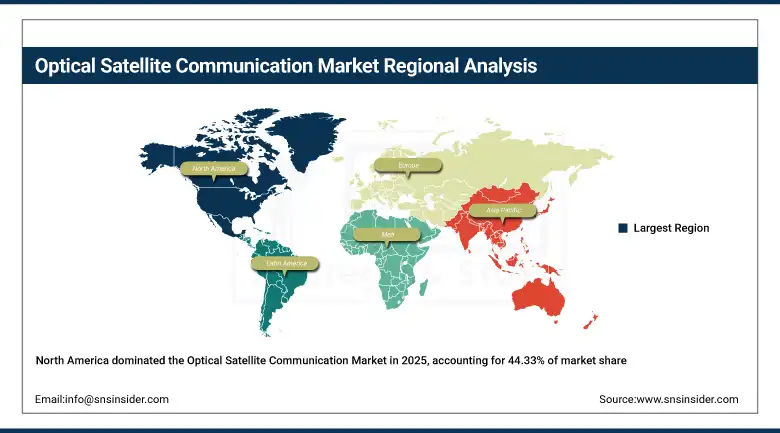

Optical Satellite Communication Market Regional Analysis

| Region | Major Country | Share within Region (%) |

| North America | United States | 44.33% |

| Europe | Germany | 25.14% |

| Asia Pacific | China | 21.75% |

| Middle East & Africa | UAE | 4.94% |

| Latin America | Brazil | 3.84% |

North America Optical Satellite Communication Market Insights

North America captured the major share of the Global Optical Satellite Communication Market in 2025, with the share of about 44.33%, owing to a significant presence of major aerospace and defense players, state-of-the-art space technology infrastructure, and heavy investments in the upcoming generation of satellite communication system. In North America, almost 85% market share is accounted for by the United States, owing to the fast emergence of LEO mega-constellation services, highly secured communication services for military applications, and the adoption of laser-based inter-satellite communication solutions.

Supporting this dominance, NASA’s Laser Communications Relay Demonstration (LCRD) and ILLUMA-T mission (2023–2024) successfully demonstrated multi-Gbps optical data transmission between space and Earth, validating operational readiness of laser communication systems for future satellite networks.

In addition, the U.S. Space Force has expanded testing of optical crosslink-enabled satellite architectures in 2024, focusing on resilient, jam-resistant communication systems for defense applications, significantly strengthening North America’s leadership in optical satellite communications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Optical Satellite Communication Market Insights

The Asia Pacific region is expected to have the highest CAGR of 19.40% between 2026 and 2035 owing to increased satellite communication systems development, increased government spending on space missions, and a growing need for high bandwidth communications in developing countries. The major players in the Asia Pacific region include China, India, Japan, and South Korea. China holds the dominant share of the revenue in the region, attributable to its large-scale satellite deployment efforts.

Supporting this growth, China’s State Administration of Science, Technology and Industry for National Defence (SASTIND) has prioritized optical satellite communication in its next-generation space infrastructure roadmap, promoting development of high-throughput laser communication payloads.

Additionally, India’s ISRO successfully demonstrated optical inter-satellite communication links in 2024, marking a key milestone in indigenous space laser communication capability development, while Japan continues to advance optical relay satellite programs through its national space agencies to support high-capacity Earth observation and communication missions.

Europe Optical Satellite Communication Market Insights

Europe was the second largest revenue contributor to the Optical Satellite Communication Market, occupying about 25.14% share in 2025 due to robust backing of government institutions toward innovation in space technology, highly developed satellite fabrication technology, and collective efforts at EU level in establishing secure communication network. Nations including Germany, France, UK, and Italy have been emerging as significant sources of activities associated with the production of optical terminals and integration of satellites.

Supporting this position, the European Space Agency (ESA) continues to expand its European Data Relay System (EDRS), which uses laser-based inter-satellite links to enable near real-time high-speed data transmission between LEO satellites and GEO relay stations.

In addition, the European Union’s Horizon Europe Space Programme (2021–2027) has significantly increased funding for advanced photonics, quantum-secure satellite communications, and next-generation optical payload technologies, reinforcing Europe’s strategic focus on secure, high-capacity space communication networks.

Middle East & Africa Optical Satellite Communication Market Insights

In the Middle East and Africa market, the Optical Satellite Communication market is experiencing continuous growth owing to increased investments made by companies into building space-based technology infrastructure, increased demand for secure defense satellite communications, and growing national satellite programs for achieving digital sovereignty and improving communications. The countries like UAE, Saudi Arabia, and Israel have become pioneers in adopting innovative space communication technology, which contributes considerably to regional revenues due to the implementation of highly effective satellite communication systems.

Supporting this momentum, the UAE’s Mohammed Bin Rashid Space Centre (MBRSC) has advanced optical communication experiments through Earth observation and deep-space mission support initiatives, while Saudi Arabia’s Vision 2030 space strategy is accelerating investment in satellite communication infrastructure and next-generation space technologies, including high-speed laser communication payloads.

Additionally, increasing defense modernization programs across the region are driving demand for secure, jam-resistant optical satellite communication systems for surveillance, intelligence, and border monitoring applications.

Optical Satellite Communication Market Growth Drivers:

-

Rising demand for high-speed, secure, and low-latency satellite connectivity, along with rapid expansion of LEO mega-constellations and space-based broadband networks, is driving strong adoption of optical satellite communication systems globally.

This transformation in the architecture of the space communications environment is a result of the inherent limitations of conventional RF technology, such as bandwidth constraints, limited spectrum availability, and increased latency during transmission. The employment of laser communication technologies for satellites in space, through the utilization of free-space optics, has become the most popular choice for developing future space communication networks that can handle massive volumes of data traffic, conduct live relaying of observations on Earth, and facilitate inter-satellite communications.

Supporting this growth, NASA’s Laser Communications Relay Demonstration (LCRD) and ILLUMA-T mission (2023–2024) successfully achieved multi-Gbps optical data transmission between space and Earth, validating operational feasibility of laser-based communication networks.

The U.S. Space Force has expanded testing of optical crosslink-enabled satellite architectures in 2024 to strengthen secure, jam-resistant military communication capabilities. These developments collectively underscore accelerating global validation and commercialization of optical satellite communication technologies.

Optical Satellite Communication Market Restraints:

-

High capital expenditure requirements for deployment of optical satellite communication systems, laser communication terminals, and precision optical payload integration, combined with complex testing and space qualification processes, are creating significant adoption barriers for new entrants and smaller satellite operators.

The design and incorporation of space-ready laser communication terminals call for specific photonic devices, precise beam-steering mechanisms, and radiation-tolerant electronics, which considerably contribute to increased satellite production expenses. Also, setting up optical inter-satellite communication constellations calls for modifications to pre-existing satellite designs, enhancement of terrestrial equipment, and support for hybrid RF-optical systems, leading to increased expenditure. Moreover, the necessity of testing, prolonged development periods, and reliability issues in deep space and military applications add to the cost implications.

Optical Satellite Communication Market Opportunities:

-

Accelerating deployment of laser-based inter-satellite networks, optical terminals, and high-capacity satellite constellations is creating strong growth opportunities in global space communication infrastructure.

The trend in this regard has been moving quickly towards establishing an optical-based backbone for space communication whereby satellites can communicate with each other using laser beams at very high speeds in near real-time communication with no need for ground stations in between. With the rise of optical communication technology in low earth orbit mega-constellations, there now exist opportunities to establish broadband networks, high-resolution earth observation data streams, and fast military communication channels.

Recent Developments:

-

2026: SpaceX expanded deployment of optical inter-satellite laser links across its next-generation LEO constellation, enhancing high-speed satellite mesh networking capabilities for global broadband coverage and improving network resilience through fully optical data routing between satellites.

-

2025: Mynaric AG advanced commercialization of its space-qualified laser communication terminals, securing additional contracts with satellite operators in Europe and North America for integration into LEO and Earth observation constellations, supporting scalable deployment of high-throughput optical communication networks.

-

2024: NASA successfully validated enhanced multi-Gbps optical communication performance through the continuation of its LCRD (Laser Communications Relay Demonstration) operations and early-phase ILLUMA-T mission integration, demonstrating reliable space-to-Earth laser data transmission under operational conditions and reinforcing readiness for next-generation optical satellite communication architectures.

-

2026: Airbus Defence and Space progressed deployment of advanced optical communication payloads under its next-generation satellite programs, focusing on integration of high-precision laser terminals for inter-satellite links in LEO and GEO missions, strengthening Europe’s capability in secure and high-capacity space-based data networks.

-

2025: Thales Alenia Space expanded development of optical relay and laser communication systems for the European Data Relay System (EDRS) evolution program, enhancing high-speed data transfer between Earth observation satellites and ground stations while improving real-time connectivity for defense and climate monitoring applications.

Optical Satellite Communication Market Key Players

Some of the Optical Satellite Communication Market Companies

-

SpaceX

-

Tesat-Spacecom GmbH & Co. KG

-

Mynaric AG

-

Ball Aerospace

-

CACI International Inc.

-

Honeywell International Inc.

-

Thales Alenia Space

-

Airbus Defence and Space

-

Northrop Grumman Corporation

-

RTX Corporation

-

BridgeComm, Inc.

-

General Atomics

-

L3Harris Technologies, Inc.

-

Viasat, Inc.

-

Skyloom Global Corp.

-

Kongsberg Defence & Aerospace

-

Kepler Communications

-

Astro Digital

-

ATLAS Space Operations

-

Telesat Corporation

Optical Satellite Communication Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.61 Billion |

| Market Size by 2035 | USD 7.77 Billion |

| CAGR | CAGR of 17.67% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Laser Communication Terminals, Optical Head / Telescope Systems, Modulators & Demodulators, Transmitters & Receivers, Network Management & Control Systems) • By Orbit Type (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO), Deep Space / Interplanetary Missions) • By Application (Inter-Satellite Links (ISL), Earth-to-Satellite / Satellite-to-Ground Communication, Deep Space Communication, Broadband Internet / Data Relay, Military & Secure Communication) • By End User (Commercial Satellite Operators, Government & Defense, Space Agencies, Research Institutions, Others) • By Data Rate (Below 1 Gbps, 1–10 Gbps, Above 10 Gbps) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Tesat-Spacecom GmbH & Co. KG, Mynaric AG, Ball Aerospace, CACI International Inc., Honeywell International Inc., Thales Alenia Space, Airbus Defence and Space, Northrop Grumman Corporation, RTX Corporation, BridgeComm, Inc., General Atomics, L3Harris Technologies, Inc., Viasat, Inc., Skyloom Global Corp., Kongsberg Defence & Aerospace, Kepler Communications, Astro Digital, ATLAS Space Operations, Telesat Corporation. |

Frequently Asked Questions

North America dominated the Optical Satellite Communication Market in 2025.

The Laser Communication Terminals segment dominated the Optical Satellite Communication Market in 2025.

Rapid demand for high-speed, low-latency, and secure space-based data transmission, driven by the expansion of LEO mega-constellations and increasing need for high-capacity inter-satellite laser communication networks, is the primary growth driver of the Optical Satellite Communication Market.

The Optical Satellite Communication Market was valued at USD 1.61 billion in 2025.

The Optical Satellite Communication Market is expected to grow at a CAGR of 17.67% from 2026 to 2035.

Get in Touch