Programmable Ammunition Market Report Scope & Overview:

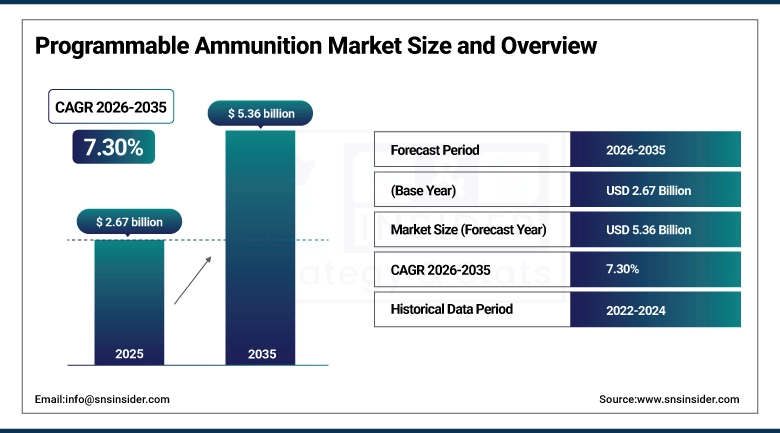

The Programmable Ammunition Market size is valued at USD 2.67 Billion in 2025 and is projected to reach USD 5.36 Billion by 2035, growing at a CAGR of 7.30% during the forecast period 2026–2035.

The Programmable Ammunition Market analysis report offers an in-depth analysis of Programmable Ammunition Market dynamics, technological developments, and military applications. The military modernization programs, increased need for precise guided ammunition, smart artillery shell usage, and military infrastructure developments are contributing to high growth in the Programmable Ammunition Market from 2026 to 2035.

The Programmable Ammunition usage was over 11.64 billion in 2025, driven by increased military procurements and the need for advanced military and homeland security operations.

Market Size and Forecast:

-

Market Size in 2025: USD 2.67 Billion

-

Market Size by 2035: USD 5.36 Billion

-

CAGR: 7.30% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Programmable Ammunition Market - Request Free Sample Report

Programmable Ammunition Market Trends:

-

Programmable artillery shells and guided rockets are increasingly being adopted due to modernization programs for defense forces around the world.

-

Integration of AI-based technologies for targeting and image recognition is becoming an innovation trend for next-generation ammunition systems.

-

Export restrictions and cybersecurity concerns are influencing procurement strategies, thereby slowing down adoption in some countries.

-

Demand for electronic warfare-resistant ammunition is increasing, with militaries seeking protection against signal jamming and hacking.

-

NATO countries are steadily modernizing their ammunition systems with programmable shells to improve interoperability and operational efficiency.

-

Increasing R&D costs are compelling defense companies to consider joint ventures and government-backed innovation programs.

-

Programmable ammunition systems are increasingly being integrated with digital fire control systems to improve accuracy and flexibility.

-

The balance between offensive and defensive capabilities is shifting toward more precision strikes to minimize collateral damage.

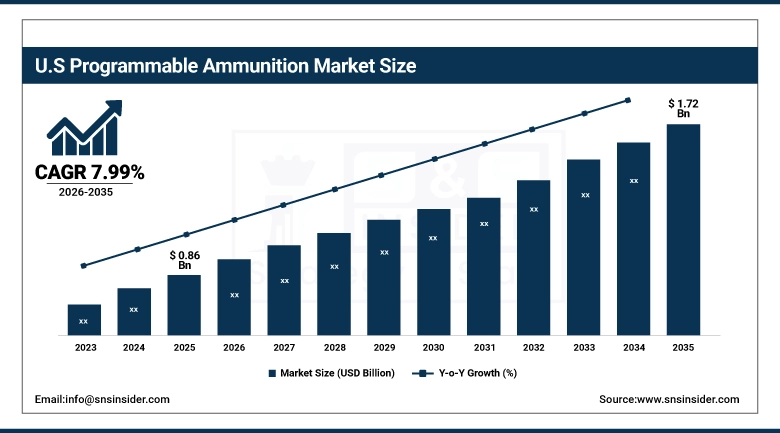

U.S. Programmable Ammunition Market Insights:

The U.S. Programmable Ammunition Market is expected to grow from USD 0.86 Billion in 2025 to USD 1.72 Billion in 2035 at a CAGR of 7.99%. Factors contributing to the growth of the Programmable Ammunition Market include increased defense modernization programs, rising demand for precision-guided ammunition, high adoption of advanced artillery shells, guided rockets, and innovative GPS, laser, and AI technologies used for targeting in different divisions of the armed forces.

Programmable Ammunition Market Growth Drivers:

-

Rising defense modernization programs and increasing demand for precision-guided munitions are driving adoption of advanced programmable ammunition.

Increasing military procurements and enhanced importance for precision strike weapons are major factors for Programmable Ammunition Market growth. Defense forces, homeland security agencies, and law enforcement teams are increasingly relying on advanced weapons, such as GPS-guided shells, laser-targeted rockets, and AI-assisted smart bullets, to improve combat efficiency and minimize collateral damage. Innovations in programming fuses, digital fire control systems, and electronic warfare resistance, combined with enhanced accuracy, flexibility, and operational safety, are significantly contributing to increased adoption, combat efficiency, and sustained Programmable Ammunition Market growth.

More than 58% of defense division teams, homeland security agencies, and tactical law enforcement teams adopted advanced programmable ammunition in 2025 to improve accuracy for increased mission success rates.

Programmable Ammunition Market Restraints:

-

High R&D costs and complex manufacturing requirements are restraining wider adoption of programmable ammunition.

The high investment costs involved in the programming of advanced fuse technology, AI technology for targeting, and electronic warfare technology are key factors restraining the growth of the market. Budgetary constraints for defense forces and homeland security organizations have led to the slow adoption of programmable ammunition compared to conventional ammunition. Export regulations, compliance, and cyber security risks have further contributed to the slow adoption of programmable ammunition. In addition, the complexity of different systems has posed interoperability issues, thereby restraining the growth of the programmable ammunition market.

More than 42% of the defense procurement programs were delayed or reduced in 2025 due to budgetary constraints on programmable ammunition acquisition programs.

Programmable Ammunition Market Opportunities:

-

Advancements in AI-enabled targeting and electronic warfare-resistant technologies are creating new opportunities for programmable ammunition.

The integration of Artificial Intelligence, Digital Fire Control, and Resilient Fuse Programming has created opportunities for the development of Next-Generation Ammunitions. Defense forces and homeland security organizations are increasingly considering programmable ammunition to boost precision, flexibility, and success in the face of evolving combat challenges. Increased investments in hybrid propulsion technology, long-range smart shells, and collaborative research and development initiatives by governments and defense contractors are creating opportunities. These technologies not only boost operational efficiency but also enhance long-term defense capabilities.

In 2025, more than 36% of new defense procurement contracts accounted for the inclusion of Artificial Intelligence or Electronic Warfare-Resistant Programmable Ammunition, indicating the high growth prospects in the industry.

Programmable Ammunition Market Segmentation Analysis:

-

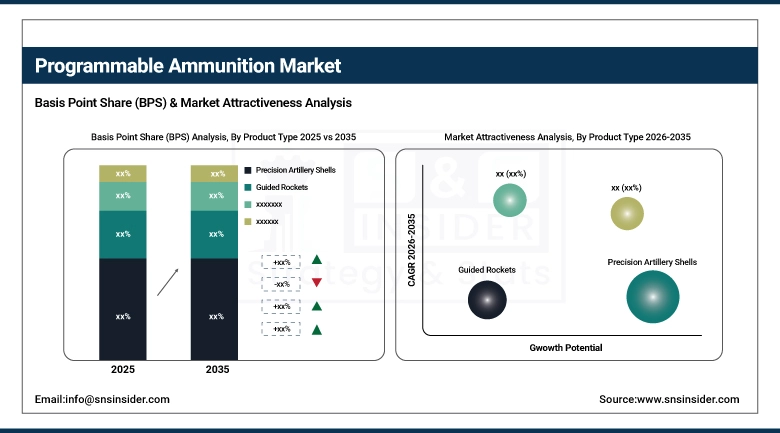

By Product Type, Precision Artillery Shells held the largest market share of 25.38% in 2025, while Smart Bullets are expected to grow at the fastest CAGR of 9.10% during 2026–2035.

-

By Application, Military dominated with 70.72% market share in 2025, whereas they are also projected to record the fastest CAGR of 8.67% through 2026–2035.

-

By Technology, Laser-Guided accounted for the highest market share of 31.23% in 2025, while Image Recognition are expected to grow at the fastest CAGR of 9.27% during the forecast period.

-

By Caliber, Large Caliber dominated with a 29.61% share in 2025, while Medium Caliber are anticipated to expand at the fastest CAGR of 7.31% through 2026–2035.

By Product Type, Precision Artillery Shells Dominate While Smart Bullets Grow Rapidly:

Precision Artillery Shells was the dominant segment in the market due to the effectiveness of the product in delivering accurate strikes. The feature of programmable detonation has further increased the acceptance of the product by the military divisions. The effectiveness of the product in reducing damage has further increased the acceptance of the product in the homeland security sector.

Smart Bullets has been the fastest-growing segment in the market due to the effectiveness of the product in delivering accurate strikes. The advancements in the product in terms of AI-enabled targeting systems have further increased the acceptance of the product in the military sector.

By Application, Military Dominates While Also Growing Rapidly:

The Military segment was the market leader in the programmable ammunition market due to the large requirement of programmable ammunition in precision strikes. The strong procurement programs, modernization initiatives, and the need for minimizing collateral damage have helped the Military segment remain at the top in the programmable ammunition market.

The Military segment is not only the leader in the programmable ammunition market; it is also the fastest-growing segment in the market. The Military segment is growing rapidly in the programmable ammunition market due to the increasing investments in smart artillery shells. This dual dominance both in current market share and future growth which underscores the military’s central role in shaping the programmable ammunition landscape.

By Technology, Laser-Guided Dominates While Image Recognition Grows Rapidly:

The Laser Guided technology segment had the dominant share due to the accuracy and reliability associated with the technology. Defense forces rely on the technology to carry out precision strikes. They also appreciate the flexibility and compatibility of the technology with other fire control systems.

The Image Recognition technology segment has the fastest growth rate. This is attributed to the technology’s capabilities in providing precision strikes in combat zones. There has been a notable increase in the adoption rate of the technology by the military and homeland security forces.

By Caliber, Large Caliber Dominates While Medium Caliber Grows Rapidly:

The Large Caliber segment held the dominant share in the market due to its extensive usage in heavy artillery, precision strikes, and the integration of high-end fire control systems. Defense forces rely on large caliber programmable shells owing to their high destructive power, flexibility in different combat conditions, and reliability in modern warfare.

The fastest growth rate is in Medium Caliber, which is being driven by increasing demand for flexible ammunition for infantry, armor, and tactical purposes. Advances in fuse programming, electronic warfare resistance, and increased durability are also contributing to the growth in this area, emphasizing the importance of medium caliber in conventional and non-conventional warfare.

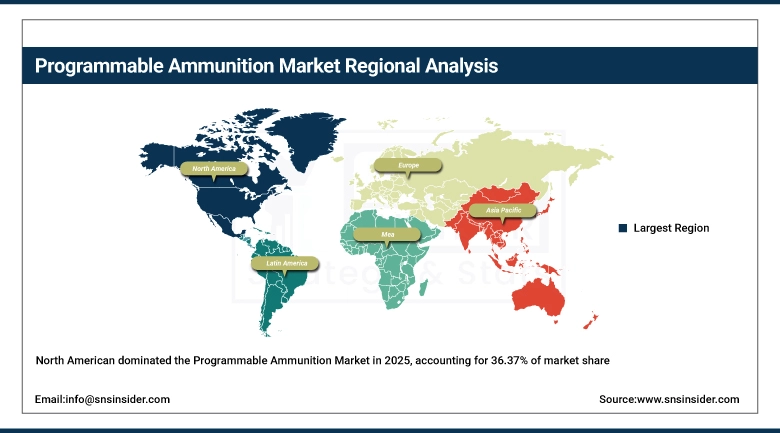

Programmable Ammunition Market Regional Analysis:

North America Programmable Ammunition Market Insights:

The North American market holds a dominant position with a market share of 36.37%, owing to robust defense spending, high-end research and development facilities, and high adoption rates for precision-guided weapons in both the U.S. and Canadian territories. Increasing investments in smart artillery shells, guided rockets, and AI-based targeting systems are driving market growth. Robust defense infrastructure, constant innovations in fuse programming and electronic warfare resistance capabilities, and robust government procurement programs have placed North America at the top in a highly developed market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Programmable Ammunition Market Insights:

The market in the U.S. is fueled by large-scale defense modernization programs, high demand for programmable ammunition, and the integration of advanced targeting technologies in the military divisions of the country. High adoption rates of GPS-guided shells, laser-guided rockets, and AI-enabled smart bullets confirm the market's focus in the country. Ongoing innovations, robust defense capabilities, and government-backed R&D initiatives solidify the position of the U.S. market as the largest in the North American region.

Asia-Pacific Programmable Ammunition Market Insights:

Asia-Pacific is the highest-growing segment with a CAGR of 9.91%, owing to the increasing defense spending in India, China, and South Korea. Significant emphasis is given to military modernization, smart rockets, and AI-based targeting systems. An increase in defense infrastructure and government-backed innovation initiatives point to the importance of the Asia-Pacific segment in the global market. Moreover, partnerships between local defense manufacturers and foreign defense contractors are boosting the local industry and sustainability of programmable ammunition markets.

China Programmable Ammunition Market Insights:

China plays a significant role in the growth of the programmable ammunition market in the Asia-Pacific region. This growth is attributed to the increase in national defense expenditures and the modernization of military technology. China has been investing a lot in the development and deployment of smart artillery shells and guided rockets. This has boosted the country’s position in the programmable ammunition market, making the Asia-Pacific region the fastest-growing market.

Europe Programmable Ammunition Market Insights:

The market in Europe is boosted by NATO modernization initiatives, increasing defense cooperation, and high adoption rates of programmable artillery shells in major markets such as Germany, France, and the UK. In addition, investments in interoperability, electronic warfare, and fire control integration drive growth in the region. The focus on precision-guided munitions for defensive and offensive purposes contributes to the stable growth in the region.

Germany Programmable Ammunition Market Insights:

Germany is at the forefront of the programmable ammunition industry in Europe, with support from NATO modernization programs and domestic defense initiatives. The country is focusing on precision-guided artillery shells with advanced programming of fuses to improve interoperability between allies. Germany is playing an instrumental role in ensuring the steady growth of the European market, thanks to its strong domestic defense manufacturing capabilities and collaborative R&D activities.

Latin America Programmable Ammunition Market Insights:

The programmable ammunition market in Latin America is in its development phase, with Brazil and Mexico being at the forefront. This is due to the increasing demand for smart ammunition in border control, counter-terrorism, and modernization processes. Although the Latin American countries are still struggling to purchase smart ammunition in large quantities due to budget constraints, they have started collaborating with defense contractors and organizations, thus developing the market.

Middle East and Africa Programmable Ammunition Market Insights:

The Middle East & Africa market is driven by regional conflicts, defense spending, and robust procurement plans in countries such as Saudi Arabia, UAE, and Israel. Programmable artillery shells and guided rockets are increasingly being used, focusing on accuracy for better mission success. Defense alliances and modernization plans are strengthening demand for defense solutions. Investments in electronic warfare-resistant technologies underscore the importance placed on resilience in the region.

Programmable Ammunition Market Competitive Landscape:

Raytheon Technologies is one of the largest defense companies in the U.S. and holds a commanding share in the programmable ammunition business, especially in terms of precision-guided munitions and advanced artillery shells. The company's products in this domain are known for accuracy, reliability, and compatibility with modern combat systems, thanks to its strong R&D and defense contracts. Raytheon's investments in AI technologies, GPS, and smart munitions give it an edge over its competitors in the marketplace.

-

In October 2025, Raytheon expanded its Excalibur precision artillery shell program, enhancing range and programmable detonation capabilities, while advancing laser-guided rocket systems for U.S. and allied forces.

Lockheed Martin is the leading defense contractor in the U.S., boasting a significant presence in the programmable ammunition sector. This includes guided rockets, missiles, and advanced artillery systems.This prominence stems from Lockheed Martin's history of substantial innovation within the aerospace and defense industries, particularly emphasizing battlefield interoperability and operational efficiency. Strategic initiatives undertaken by Lockheed Martin encompass the expansion of missile defense systems and the integration of programmable technology within multi-domain operations.

-

In May 2025, Lockheed advanced its GMLRS (Guided Multiple Launch Rocket System) with programmable warheads, while progressing AI-driven targeting solutions for next-generation missile systems.

BAE Systems holds a prominent position in Europe's programmable ammunition market. This UK-based company maintains a substantial presence within the European defense landscape. The company has substantial experience in the production of programmable ammunition in the form of artillery shells, armor vehicle ammunition, and naval systems. The company prioritizes the safety and accuracy of its products and has the backing of NATO modernization programs. BAE Systems has significantly improved its position in the market with its focus on smart artillery and electronic warfare-resistant ammunition.

-

In July 2025, BAE expanded its Bofors 155mm programmable artillery shells, enhancing precision strike capabilities and supporting NATO’s modernization initiatives across Europe.

Programmable Ammunition Market Key Players:

Some of the Programmable Ammunition Market Companies are:

-

Raytheon Technologies

-

Lockheed Martin

-

Northrop Grumman

-

General Dynamics

-

BAE Systems

-

Rheinmetall AG

-

Nammo AS

-

Saab AB

-

Thales Group

-

Leonardo S.p.A.

-

MBDA

-

Elbit Systems

-

FN Herstal

-

Kongsberg Gruppen

-

Hanwha Defense

-

Bharat Dynamics Limited

-

ASELSAN A.Ş.

-

Olin Corporation

-

Nexter Systems

-

Denel Dynamics

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.67 Billion |

| Market Size by 2035 | USD 5.36 Billion |

| CAGR | CAGR of 7.30% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Precision Artillery Shells, Guided Rockets, Smart Bullets, Self-Propelled Projectiles, Target-Seeking Missiles, Others), • By Application (Military, Homeland Security, Law Enforcement, Civilian, Others), • By Technology (Laser-Guided, GPS, Infrared, Radio Frequency, Image Recognition, Others), • By Caliber (Large Caliber, Medium Caliber, Small Caliber, Artillery, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Raytheon Technologies, Lockheed Martin, BAE Systems, Northrop Grumman, General Dynamics, Rheinmetall AG, Nammo AS, Saab AB, Thales Group, Leonardo S.p.A., MBDA, Elbit Systems, FN Herstal, Kongsberg Gruppen, Hanwha Defense, Bharat Dynamics Limited, ASELSAN A.Ş., Olin Corporation, Nexter Systems, Denel Dynamics. |

Frequently Asked Questions

Key technologies include GPS guidance, laser targeting, infrared sensors, radio frequency systems, and emerging AI-based image recognition. These innovations improve accuracy, adaptability, and resistance to electronic warfare.

Challenges include high R&D costs, strict export regulations, cybersecurity vulnerabilities, and budget constraints in developing regions. Ensuring reliability under battlefield conditions is also a critical hurdle.

Europe holds about 25.84% market share with a steady 6.59% CAGR, supported by NATO modernization programs and increased procurement in countries such as Germany, France, and the UK.

Asia-Pacific is the fastest-growing region, expected to expand at a 9.91% CAGR, driven by India, China, and South Korea’s defense modernization initiatives.

North America dominates with around 36.37% market share, led overwhelmingly by the United States due to its massive defense budget and advanced R&D programs.

Get in Touch