Radar Simulators Market Report Scope & Overview:

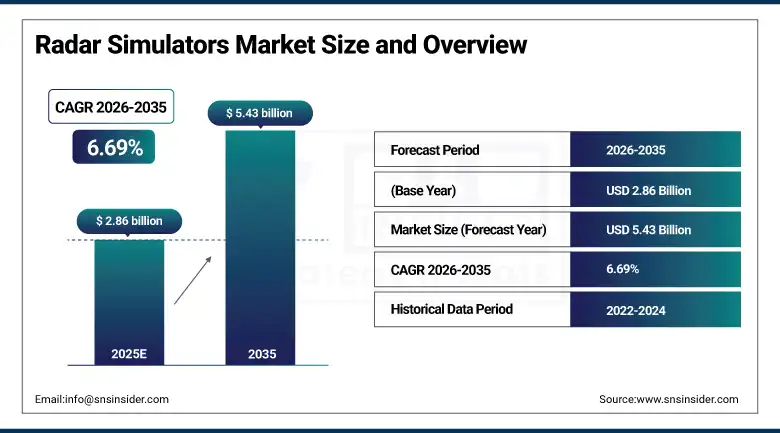

The Radar Simulators Market was valued at approximately USD 2.86 billion in 2025 and is expected to reach USD 5.43 billion by 2035, growing at a CAGR of 6.69% from 2026–2035.

The Radar Simulators Market is experiencing consistent growth due to higher levels of defense modernization initiatives worldwide, increased use of next-generation radar systems like AESA (Active Electronically Scanned Array) radars, and the escalating requirement for affordable yet highly accurate simulators for radar personnel training. Such simulators are essential for conducting realistic simulations of missions, threats identification, and testing systems without the costs and dangers of performing real-world tests with actual radar units. The increasing intricacies of contemporary warfare, which include electronic warfare (EW), multi-domain warfare, and UASs (Unmanned Aerial Systems), have led to heightened demands for next-gen simulation systems.

Department of Defense continues to expand its use of synthetic training environments under programs such as the Joint All-Domain Command and Control (JADC2) initiative, which integrates simulation and real-time data fusion for mission planning and training. Similarly, NATO member countries are increasingly adopting interoperable simulation systems to improve joint force readiness and cross-platform coordination.

In terms of recent developments, leading defense and simulation technology providers have been advancing high-fidelity radar simulation capabilities. In 2024–2025, companies such as RTX Corporation (Raytheon Technologies) and L3Harris Technologies have focused on enhancing electronic warfare and radar training simulators with AI-driven scenario generation and real-time threat modelling.

Radar Simulators Market Size and Forecast

-

Market Size in 2025: USD 2.86 Billion

-

Market Size by 2035: USD 5.43 Billion

-

CAGR: 6.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Radar Simulators Market - Request Free Sample Report

Radar Simulators Market Trends

-

Rising adoption of AI/ML-enabled radar simulation platforms and digital twin technologies is significantly enhancing training realism and adaptive threat scenario generation in defense environments.

-

Increasing integration of hybrid simulation systems combining real-time and synthetic radar environments is improving multi-domain mission rehearsal capabilities across air, land, sea, and space operations.

-

Rapid modernization of defense forces and growing use of AESA and phased-array radar systems are driving demand for advanced high-fidelity simulation and validation platforms.

-

Expanding deployment of cloud-based and networked simulation environments is enabling distributed training across multiple defense bases and allied military forces.

-

Rising emphasis on cost-effective virtual training replacing live radar exercises is accelerating adoption of simulation-based operator training programs globally.

-

Increasing use of electronic warfare (EW) simulation and jamming scenario modeling is enhancing preparedness for complex modern battlefield conditions.

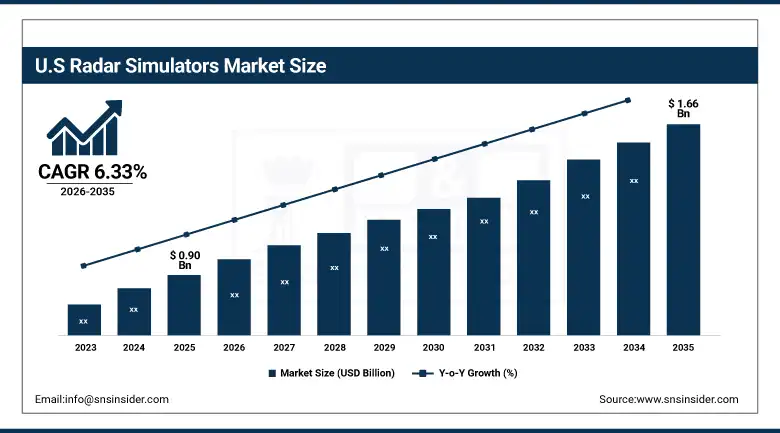

The U.S. Radar Simulators Market was valued at USD 0.90 billion in 2025 and is expected to reach USD 1.66 billion by 2035, growing at a CAGR of 6.33% from 2026–2035.

The United States Radar Simulators Market constitutes the largest national market share globally, owing to the advanced defense ecosystem along with presence of major defense contractors like RTX Corporation, L3Harris Technologies, Lockheed Martin, and Northrop Grumman in addition to constant investment in synthetic training solutions. The emphasis by the Department of Defense in the adoption of JADC2 and LVC training has been identified as a key growth factor in this market.

In addition, modernization programs across the U.S. Air Force and Navy are accelerating adoption of AESA radar simulation, electronic warfare (EW) training systems, and AI-enabled mission rehearsal platforms to enhance operational readiness and reduce reliance on expensive live exercises.

Recent developments include RTX and L3Harris advancing AI-powered radar and electronic warfare simulation systems in 2024–2025 to support next-generation training environments, alongside continued expansion of cloud-based synthetic training ecosystems under U.S. defense modernization initiatives, reinforcing the country’s position as the global hub for radar simulation innovation.

Radar Simulators Market Segment Highlights

-

By Application Defense & Military Training dominated the Radar Simulators Market with 55.36% share in 2025; Research & Development (R&D) Simulation fastest growing

-

By Platform Airborne Radar Simulators dominated the Radar Simulators Market with 48.24% share in 2025; Space-Based Radar Simulation Systems fastest growing

-

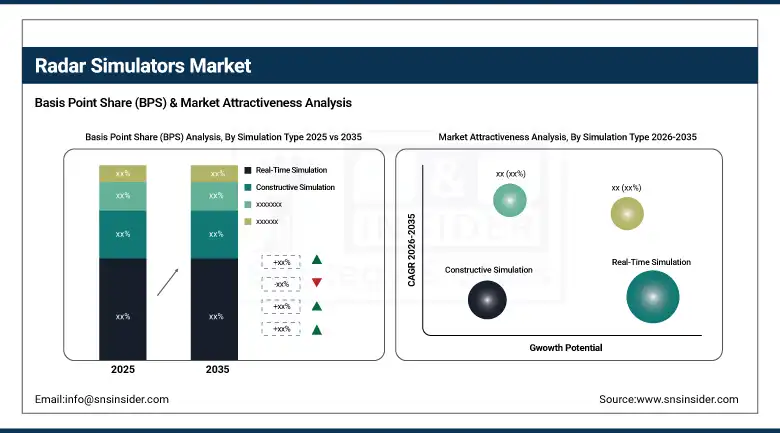

By Simulation Type Real-Time Simulation dominated the Radar Simulators Market with 30.85% share in 2025; Hybrid Simulation fastest growing

-

By End User Defense Forces (Army, Navy, Air Force) dominated the Radar Simulators Market with 60.24% share in 2025; Defense Contractors & Training Institutions fastest growing

-

By Technology Conventional Radar Simulation dominated the Radar Simulators Market with 35.57% share in 2025; AI/ML-Enabled Simulation Platforms fastest growing

By Application, Defense & Military Training segment dominates the Radar Simulators Market, Research & Development (R&D) Simulation segment expected to grow fastest

In 2025, the Defense & Military Training segment maintained its dominant position in the Radar Simulators Market, accounting for approximately 55.36% of total revenue. This leadership is driven by the critical need for continuous operator training, mission rehearsal, and combat readiness in increasingly complex multi-domain warfare environments.

The Research & Development (R&D) Simulation segment is projected to register the highest CAGR during the 2026–2035 forecast period. This growth is supported by increasing investment in next-generation radar technologies, including phased-array systems, AI-enabled threat modeling, and digital twin-based simulation environments.

By Platform, Airborne Radar Simulators segment dominates the Radar Simulators Market, Space-Based Radar Simulation Systems segment expected to grow fastest

In 2025, the Airborne Radar Simulators segment held the largest share of 48.24% of the Market for Radar Simulators, owing to wide usage in fighter planes, unmanned aerial vehicles (UAVs), surveillance systems, and pilot training simulators.

The market for Space-Based Radar Simulation Systems will see the highest CAGR from 2026 to 2035. This is because there has been a rise in investments in surveillance, SSA (Space Situational Awareness), and missile tracking using satellites. Growing expenditure on space defense by major economies and growing requirements for simulation of orbital radars as well as satellite communication jamming are fueling growth in this market segment.

By Simulation Type, Real-Time Simulation segment dominates the Radar Simulators Market, Hybrid Simulation segment expected to grow fastest

In 2025, the Real-Time Simulation segment accounted for the largest share of 30.85% of the Radar Simulators Market, motivated by its capacity to simulate live radar systems accurately for training purposes and mission execution planning. Real-time simulation finds application in defense setups in the making of tactical decisions, training personnel in detecting threats, and mission rehearsals in realistic battle scenarios.

Hybrid simulation will see the highest CAGR from 2026 to 2035. This will be attributed to the rising demand to fuse real-time data with simulations and thus create scalable training scenarios.

By End User, Defense Forces (Army, Navy, Air Force) segment dominates the Radar Simulators Market, Defense Contractors & Training Institutions segment expected to grow fastest

The Defense Forces (Army, Navy, Air Force) segment maintained the highest end-user share of 60.24% in the Radar Simulators Market in 2025. This domination is due to the widespread use of radar simulator systems in order to provide training to operators as well as mission rehearsals and combat readiness preparation programs in contemporary defense armies. Complexity in radar systems such as AESA radar systems, phased array radars, and EW enabled systems has made simulations indispensable.

The Defense Contractors & Training Institutions segment is projected to register the highest growth rate during the 2026–2035 forecast period.

By Technology, Conventional Radar Simulation segment dominates the Radar Simulators Market, AI/ML-Enabled Simulation Platforms segment expected to grow fastest

The Conventional Radar Simulation segment maintained the highest technology share of approximately 35.57% in the Radar Simulators Market till 2025. This is because of their extensive use in existing defense training systems, low-cost setup, and ongoing use in the current military system in the training of radar operators.

The AI/ML-Enabled Simulation Platforms segment is projected to register the highest CAGR during the 2026–2035 forecast period.

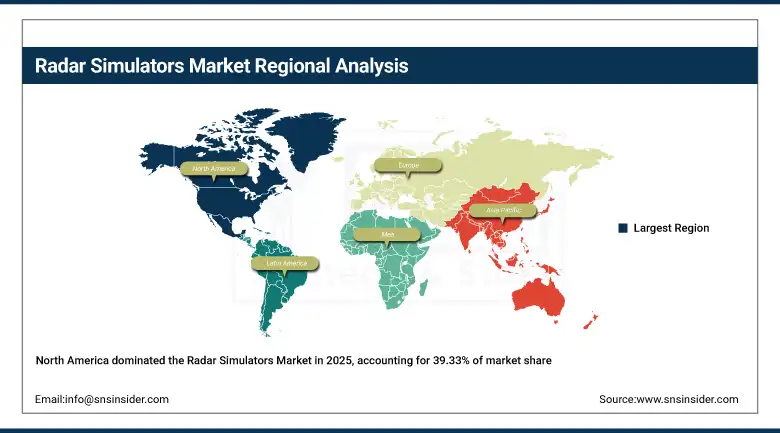

Radar Simulators Market Regional Analysis

| Region | Major Country | Share within Region (%) |

|---|---|---|

| North America | United States | 39.33% |

| Europe | Germany | 25.14% |

| Asia Pacific | China | 23.75% |

| Middle East & Africa | UAE | 7.04% |

| Latin America | Brazil | 4.74% |

North America Radar Simulators Market Insights

North America held the dominant position in the global Radar Simulators Market with 39.33% In terms of revenue share, North America is projected to account for a dominant share in 2025 due to its well-developed defense ecosystem, presence of major vendors providing simulation and radar technologies, and substantial investments in future military training facilities. In terms of regional performance, the United States dominates, accounting for about 85% of the regional market share driven by the implementation of synthetic training, AI simulation, and LVC systems within defense forces. The region has seen continuous upgrades in radars such as AESA and EW systems, increasing the need for simulations.

Get Customized Report as per Your Business Requirement - Enquiry Now

Supporting this dominance, the U.S. Department of Defense has expanded adoption of Joint All-Domain Command and Control (JADC2) initiatives, which integrate radar simulation, real-time data fusion, and multi-domain operational training to enhance battlefield readiness and interoperability across air, land, sea, space, and cyber domains.

In addition, defense contractors such as RTX Corporation, L3Harris Technologies, and Northrop Grumman have advanced AI-powered radar and electronic warfare simulation capabilities during 2024–2025, focusing on adaptive threat modeling, digital twin-based mission rehearsal, and cloud-enabled distributed training environments.

Asia Pacific Radar Simulators Market Insights

The Asia Pacific region is anticipated to register the highest CAGR of 7.49% over the forecast period 2026–2035, This growth will be fueled by initiatives in fast-paced modernization of defense forces, indigenous development capabilities in radars, and simulation technology for military training purposes. Some of the most important countries driving growth in the region are China, India, Japan, South Korea, and Australia. Out of all these countries, China alone accounts for about 55 percent of the regional market.

Supporting this expansion, China’s defense modernization strategy has prioritized development of indigenous simulation and electronic warfare training systems, integrating radar simulators into large-scale military training academies and research institutions. Similarly, India’s Ministry of Defence has expanded procurement of simulation-based training platforms under its “Make in India” initiative to strengthen domestic defense manufacturing and reduce reliance on foreign training systems.

In addition, Japan and South Korea are actively investing in AI-based radar simulation, space-domain awareness systems, and next-generation fighter jet training programs, with growing emphasis on networked and hybrid simulation environments

Europe Radar Simulators Market Insights

Europe is the second-biggest revenue generator in the Radar Simulators Market worldwide, contributing 26% (estimate) to the market in 2025, with its success being attributed to the region's sound collaboration strategies, superior military training facilities, and continued investment in radar technologies. Some of the key countries that have helped in driving the growth include Germany, UK, France, Italy, and Spain, among others.

Supporting this position, the European Defence Fund (EDF) has significantly increased funding for collaborative defense innovation projects, including electronic warfare simulation, radar system validation platforms, and AI-enabled mission training systems. These initiatives are aimed at improving interoperability and strengthening joint operational readiness among European defense forces.

In addition, leading European defense and technology companies such as Thales Group, Leonardo S.p.A., Saab AB, and Indra Sistemas have expanded development of cloud-based radar simulation systems, digital twin environments, and multi-domain training platforms during 2024–2025.

Middle East & Africa (MEA) Radar Simulators Market Insights

There is consistent growth in the Radar Simulators Market across the Middle East and Africa (MEA) region due to the increase in initiatives for modernizing the military, rising attention toward border security, and growing investments in military training infrastructures. Some of the key countries contributing to regional market growth include Saudi Arabia, the UAE, Israel, and South Africa, with GCC countries being the early adopters of the advanced generation radar simulation products.

Supporting this development, Saudi Arabia’s Vision 2030 defense transformation program continues to prioritize localization of defense technologies and expansion of military training academies, leading to increased deployment of radar simulation systems for air defense readiness and electronic warfare training. Similarly, the UAE’s Ministry of Defense has been actively investing in AI-enabled training systems and integrated simulation environments to enhance operational preparedness across multi-domain defense operations.

In addition, Israel remains a key innovation hub in the region, with strong development in electronic warfare simulation, radar testing systems, and AI-driven defense training technologies, supported by organizations such as Israel Aerospace Industries (IAI) and Elbit Systems

Latin America Radar Simulators Market Insights

Latin American Region sees slow yet steady growth in the market size of Radar Simulators because of the high rate of modernization in the defense sector, increased spending on air surveillance equipment, and the trend of simulation-based training of military forces. Major countries of this region that contribute to the growth include Brazil, Mexico, Argentina, and Chile, with Brazil contributing the most due to its advanced aerospace & defense sector.

Supporting this trend, Brazil’s Ministry of Defense has been expanding its SISDABRA (Brazilian Air Defense System) modernization program, which includes increased utilization of radar simulation technologies for air force training, airspace monitoring, and mission planning exercises.

In addition, Mexico’s Secretariat of National Defense (SEDENA) has increased investment in simulation-based training systems for radar operators and air surveillance units, focusing on improving border security and aerial monitoring capabilities.

Radar Simulators Market Growth Drivers:

-

Rising demand for realistic, cost-effective, and AI-enhanced defense training environments is accelerating global adoption of radar simulation systems across multi-domain military operations

The leading factor driving the Radar Simulators Market structure is the increasing trend towards moving away from live, expensive, and elaborate training exercises by defense agencies to high-end simulation exercises. With modern radar technology, especially AESA, phased array, and electronic warfare integration becoming exceedingly complex, there exists a need for high-end simulators in conducting training exercises, mission rehearsals, and simulations. There is an increasing reliance on simulators by defense bodies to ensure preparedness, cost reduction, and safe replication of real-life situations such as jamming, stealth identification, and target acquisition exercises.

Supporting this growth, the U.S. Department of Defense (DoD) has significantly expanded investment in Joint All-Domain Command and Control (JADC2) and Live-Virtual-Constructive (LVC) training environments, which integrate radar simulation systems with real-time operational data to enhance cross-domain mission readiness across air, land, sea, space, and cyber operations.

Radar Simulators Market Restraints:

-

High acquisition cost and complex integration requirements of advanced radar simulators and AI-enabled training systems are limiting large-scale deployment across cost-sensitive defense organizations and smaller military training institutions

The primary restraint impacting the Radar Simulators Market is the significant upfront capital investment and system integration complexity associated with advanced radar simulation platforms. Modern high-fidelity simulators—particularly those supporting AESA radar modelling, electronic warfare environments, AI-driven scenario generation, and multi-domain mission rehearsal—require sophisticated hardware infrastructure, high-performance computing systems, and specialized software ecosystems. These systems often involve long procurement cycles, customization for specific defense platforms, and continuous upgrades to remain compatible with evolving radar technologies.

Radar Simulators Market Opportunities:

-

Rapid advancement of AI-enabled autonomous simulation ecosystems and cloud-based distributed training networks is creating major expansion opportunities for scalable, next-generation radar training across global defense forces and allied military systems

The most significant opportunity in the Radar Simulators Market is the rapid evolution of AI-driven simulation ecosystems combined with cloud-native and distributed training architectures, enabling defense organizations to scale high-fidelity radar training without dependence on centralized, expensive physical simulation centers. These next-generation platforms allow real-time replication of complex radar environments, including electronic warfare interference, multi-target tracking, stealth detection scenarios, and dynamic battlefield conditions, while supporting simultaneous training across geographically dispersed military units.

Recent Developments:

-

2026: RTX Corporation (Raytheon Technologies) advanced its next-generation AI-enabled radar and electronic warfare simulation suite, expanding integration across U.S. Air Force and Navy synthetic training environments under the Joint All-Domain Command and Control (JADC2) framework. The upgrade focuses on improving adaptive threat modeling and real-time mission rehearsal for multi-domain operations.

-

2025: L3Harris Technologies expanded deployment of its Live, Virtual, Constructive (LVC) training and radar simulation platforms across NATO-aligned defense programs, supporting integrated air defense and electronic warfare training. The company also enhanced cloud-enabled simulation capabilities to enable distributed multi-site radar operator training.

-

2024: Northrop Grumman strengthened its digital radar simulation and electronic warfare training ecosystem by upgrading simulation modules used in advanced airborne early warning and space-domain awareness programs. The enhancement focused on improving high-fidelity radar environment replication for next-generation defense platforms.

-

2024: Thales Group introduced upgraded cloud-based radar simulation and synthetic training solutions integrated with AI-driven scenario generation, supporting European defense modernization programs and NATO interoperability training initiatives across air and naval defense systems.

Radar Simulators Market Key Players

Some of the Radar Simulators Market Companies

-

RTX Corporation (Raytheon Technologies)

-

L3Harris Technologies

-

BAE Systems plc

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

Thales Group

-

Saab AB

-

Leonardo S.p.A.

-

Indra Sistemas S.A.

-

Rohde & Schwarz GmbH & Co. KG

-

Mercury Systems Inc.

-

CAE Inc.

-

Collins Aerospace (RTX)

-

Elbit Systems Ltd.

-

Israel Aerospace Industries (IAI)

-

Leonardo DRS

-

Rheinmetall AG

-

Terma A/S

-

Keysight Technologies

-

Presagis (CAE Inc.)

Radar Simulators Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.86 Billion |

| Market Size by 2035 | USD 5.43 Billion |

| CAGR | CAGR of 6.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Application (Defense & Military Training, Radar System Testing & Validation, Air Traffic Control (ATC) Simulation, Maritime Navigation Training, Research & Development (R&D) Simulation) By Platform (Airborne Radar Simulators, Ground-Based Radar Simulators, Naval/Maritime Radar Simulators, Space-Based Radar Simulation System) By Simulation Type (Real-Time Simulation, Constructive Simulation, Virtual Simulation, Hybrid Simulation, Others) By End User (Defense Forces (Army, Navy, Air Force), Homeland Security Agencies, Aerospace & Aviation Companies, Defense Contractors & Training Institutions, Others) By Technology (Conventional Radar Simulation, AESA Radar Simulation Systems, Phased Array Simulation, AI/ML-Enabled Simulation Platforms) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | RTX Corporation (Raytheon Technologies), L3Harris Technologies, BAE Systems plc, Northrop Grumman Corporation, Lockheed Martin Corporation, Thales Group, Saab AB, Leonardo S.p.A., Indra Sistemas S.A., Rohde & Schwarz GmbH & Co. KG, Mercury Systems Inc., CAE Inc., Collins Aerospace (RTX), Elbit Systems Ltd., Israel Aerospace Industries (IAI), Leonardo DRS, Rheinmetall AG, Terma A/S, Keysight Technologies, Presagis (CAE Inc.) |

Frequently Asked Questions

Get in Touch