Reusable Launch Vehicles Market Report Scope & Overview:

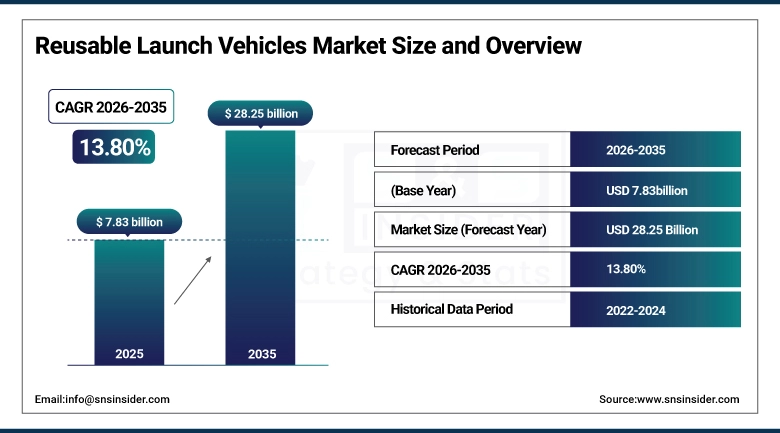

The Reusable Launch Vehicles Market size is valued at USD 7.83 Billion in 2025 and is projected to reach USD 28.25 Billion by 2035, growing at a CAGR of 13.80% during the forecast period 2026–2035.

This Reusable Launch Vehicles Market analysis report gives an insight into market dynamics, innovation, and application areas. The increased number of satellite launches, exploration of space by various organizations, commercial space activities, and space tourism will boost market growth from 2026 to 2035.

The operations with reusable launch vehicles have been carried out to exceed 350 flights by 2025 and these include Space X Falcon 9 and Starship, owing to cheaper launch costs and fast turnaround ability on average.

Market Size and Forecast:

-

Market Size in 2025: USD 7.83 Billion

-

Market Size by 2035: USD 28.25 Billion

-

CAGR: 13.80% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Reusable Launch Vehicles Market - Request Free Sample Report

Reusable Launch Vehicles Market Trends:

-

Growth in satellite launches is contributing to the steady adoption of reusable rockets.

-

Space missions to the moon and Mars are leading to increased investments in heavy and super-heavy RLVs.

-

Exponential growth of businesses is contributing to the dominance of private organizations over government bodies.

-

Space tourism is gaining popularity and proving to be one of the most profitable uses of reusable rockets.

-

Developments in methane engines are helping set standards in terms of reusability and cost-effectiveness.

-

Liquid rocket engines form the base of existing reusable launch vehicles.

-

Public-private collaborations are growing, providing substantial funding and innovations.

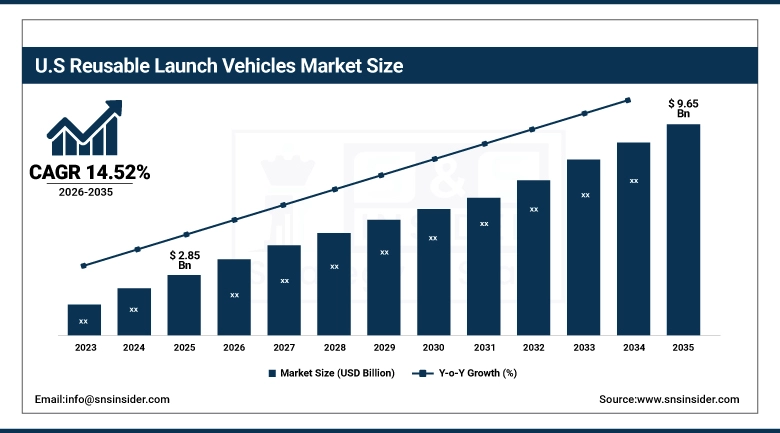

U.S. Reusable Launch Vehicles Market Insights:

The U.S. Reusable Launch Vehicles Market is projected to grow from USD 2.85 Billion in 2025 to USD 9.65 Billion by 2035, at a CAGR of 14.52%. Growth is driven by rising demand for satellite launches, increasing space exploration missions, strong adoption of reusable propulsion technologies, and investments in innovative vehicle designs and launch infrastructure across government agencies, commercial enterprises, and research institutions.

Reusable Launch Vehicles Market Growth Drivers:

-

Rising demand for satellite launches and expanding space exploration programs are key drivers of Reusable Launch Vehicles Market growth.

Government organizations, businesses, and laboratories are increasingly incorporating state-of-the-art reusable technologies in the form of heavy and super-heavy launch systems. Technological advancements in the area of propulsion systems, including methane engines, liquid and hybrid propellants, and other factors such as faster turnaround, higher safety and reliability, will lead to even more rapid adoption of these systems.

By 2025, over 60% of all satellites will have been launched on reusable launch vehicles, which would account for cost reductions of as much as 70%.

Reusable Launch Vehicles Market Restraints:

-

High development costs, complex regulatory frameworks, and technological challenges present significant restraints for the Reusable Launch Vehicles Market.

Challenges that may be faced when scaling up the use of reusable rockets include costs associated with research and development, safety, and inadequate infrastructure. Rocket manufacturers who are struggling with refurbishing rockets, durability of materials, and reliability of propulsion may face challenges in adopting reusable rockets as anticipated. Other factors including international regulations regarding launches, environmental effects, and geopolitics may hinder the growth of the market.

As at 2025, less than 40% of launches utilized reusable rockets, owing to the high initial investments needed and lack of advanced launch sites.

Reusable Launch Vehicles Market Opportunities:

-

Growing development of advanced reusable propulsion systems and next-generation launch vehicle designs presents significant opportunities for the Reusable Launch Vehicles Market.

There is an increasing usage of heavy and ultra-heavy reusable launch vehicles for the purpose of launching satellites and exploring outer space by agencies of public spaces, private aerospace companies, and academic/scientific organizations. There are a lot of opportunities available for those companies that use advanced, safer, and cheaper technologies such as methane-powered engines, faster turnaround, and modular designs of aircrafts. Improvements in technology regarding liquid fuel and hybrids, reliability, reusability rate, and more mission flexibility are the reasons.

By 2025, around 55% of all launches took place utilizing reusable spacecraft thanks to savings that can be up to 70%.

Reusable Launch Vehicles Market Segmentation Analysis:

-

By Vehicle Type, Small Reusable Launch Vehicles held the largest market share of 28.97% in 2025, while Super Heavy Reusable Launch Vehicles are expected to grow at the fastest CAGR of 15.58% during 2026–2035.

-

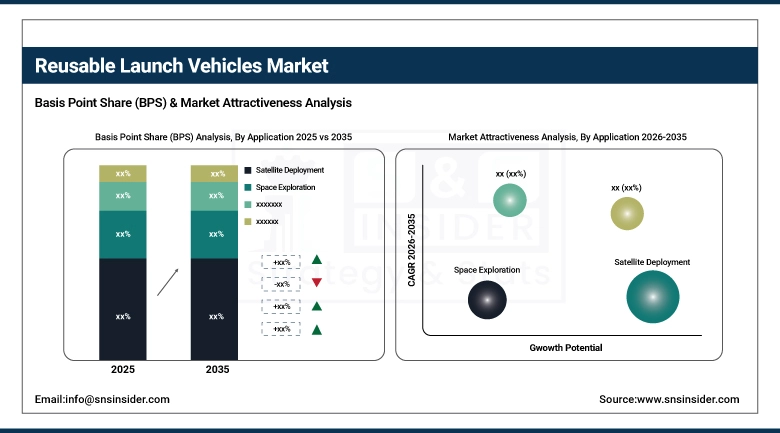

By Application, Satellite Deployment dominated with 41.23% market share in 2025, whereas Space Tourism are projected to record the fastest CAGR of 15.33% through 2026–2035.

-

By End User, Commercial Enterprises held the largest share of 41.23% in 2025, while they are also expected to grow at the fastest CAGR of 14.59% during the forecast period.

-

By Propulsion Technology, Liquid Propellant Engines accounted for the highest market share of 42.86% in 2025, while Methane-based Engines are expected to grow at the fastest CAGR of 15.01% during the forecast period.

By Vehicle Type, Small Reusable Launch Vehicles Dominate While Super Heavy Reusable Launch Vehicles Grow Rapidly:

Small Reusable Launch Vehicles segment dominates the market due to their proven efficiency in deploying small satellite constellations and strong adoption by commercial operators. Their ability to provide cost-effective access to orbit has made them the preferred choice for communication, Earth observation, and navigation missions.

Super Heavy Reusable Launch Vehicles are the fastest-growing segment, driven by rising demand for deep-space exploration, lunar cargo delivery, and Mars mission initiatives. Their large payload capacity and advanced reusability cycles are positioning them as critical assets for future interplanetary programs.

By Application, Satellite Deployment Leads While Space Tourism Expands Quickly:

Satellite Deployment remains the dominant application in market, supported by the surge in satellite constellations for broadband, navigation, and Earth monitoring. The reliability and frequency of reusable launches have made them indispensable for commercial and government satellite programs.

Space Tourism is the fastest-expanding application, fueled by growing interest from private travelers and companies offering suborbital and orbital experiences. Advancements in vehicle safety and reusability are enabling broader accessibility and accelerating adoption in this emerging sector.

By End User, Commercial Enterprises Drive Growth While It Gain Momentum:

Commercial Enterprises dominate the market, led by private aerospace companies pioneering reusable technologies and offering competitive launch services. Their agility, innovation, and cost efficiency have shifted market leadership away from traditional government programs.

Commercial Enterprises are also emerging as a fastest growing segment, leveraging reusable vehicles for scientific experiments, microgravity research, and collaborative missions. Their increasing participation highlights the expanding role of academia and innovation hubs in space exploration.

By Propulsion Technology, Liquid Engines Lead While Methane-based Engines Advance Rapidly:

Liquid Propellant Engines are dominant the mainstay of reusable launch systems, as these engines boast high levels of dependability, efficiency, and flexibility in their applicability to different types of vehicles. Currently, liquid propellant engines are still dominating due to existing facilities and proven effectiveness.

Methane Engines are considered the most fastest developing type of propulsion system today, thanks to their high reusability rate, environmental friendliness, and compatibility with future heavy and superheavy launch systems.

Reusable Launch Vehicles Market Regional Analysis:

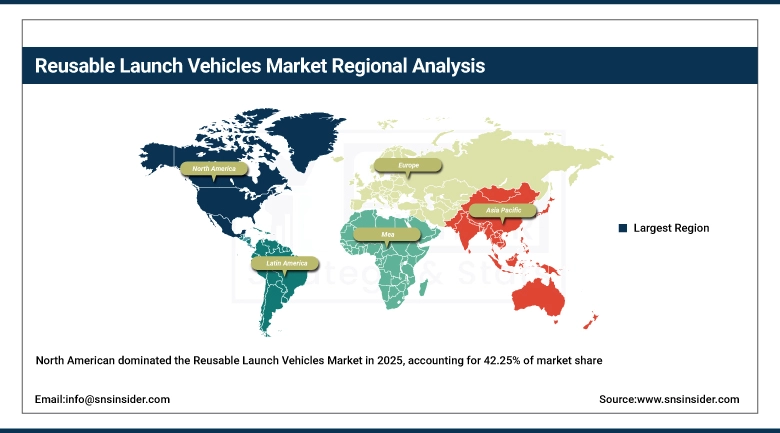

North America Reusable Launch Vehicles Market Insights:

North America holds the top position in the RLV market with a market share of 42.25%. The reason behind its supremacy is the existence of robust government policies, innovative private aerospace industries, and the presence of existing launching facilities in the United States and Canada. The frequent launches of satellites and defense cargo along with commercial activities are the primary reasons that boost its popularity. Innovations in heavy and super-heavy launchers along with fast turnaround time add to the strength of the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Reusable Launch Vehicles Market Insights:

The U.S. is the clear leader of the North American market for RLVs due to the companies SpaceX, Blue Origin, and United Launch Alliance. Satellite constellations, military launches, and the development of the industry of space tourism contribute significantly to market growth. Investments into methane-powered engines and super heavy lift vehicles make the U.S. one of the leading countries in terms of deep space explorations.

Asia-Pacific Reusable Launch Vehicles Market Insights:

The Asia Pacific region is the fastest growing segment of the RLV market, with a compound annual growth rate of 15.58%, due to the presence of major economies such as China, India, and Japan. Increased satellite launch projects, defense sector expansion, and plans for ambitious missions to the moon and Mars are contributing factors to adoption. There is also increased government support and activity in private sector R&D, making Asia Pacific region a fierce competitor of North America.

China Reusable Launch Vehicles Market Insights:

China is quickly becoming a strong player in the RLV space thanks to its CASC and CASIC programs. Government investment, launches of military payloads, and lunar exploration activities fuel this rapid progress. Methane engine technology and developments in heavy-duty and reusable vehicles showcase China’s dedication to low-cost operations. Expansion of its commercial companies and satellite launches make China a major player in the APAC region’s RLV ecosystem.

Europe Reusable Launch Vehicles Market Insights:

The European RLV industry is characterized by the presence of major players such as Arianespace, ArianeGroup, and the European Space Agency. There is significant concentration on the launch of satellites, research collaboration, and environmentally friendly propellant systems. Reinvestment in reusable heavy-lift systems and cross-state cooperation enhance the competitive edge of Europe in this industry. Despite being less adopted than North America and the Asia-Pacific region, Europe is steadily growing in the industry.

Germany Reusable Launch Vehicles Market Insights:

Germany acts as an important stakeholder for Europe’s RLV program. There are excellent possibilities of success due to its strong engineering background in the field of aerospace and research-oriented innovations. Projects developed by ESA and other national programs contribute to the progress in areas such as sustainable propulsion systems and vehicles. The focus on sustainability, satellites, and military use contributes greatly to the success of the program.

Latin America Reusable Launch Vehicles Market Insights:

The Latin American RLV market is in the process of development due to growing interest in deploying satellites and developing regional space programs. Brazil and Mexico are playing the most significant roles in these developments, receiving help from aerospace companies from around the world. However, lack of funds and infrastructure pose obstacles that need to be overcome, as the role of Latin America is expected to grow in the field.

Middle East & Africa Reusable Launch Vehicles Market Insights:

Middle East & Africa region is slowly but steadily moving toward RLVs due to increased investment in satellite communications and defense. The United Arab Emirates leads in the race with advanced space exploration plans that include mission to Mars. Partnership with international aerospace firms and development of launch facilities is encouraging use of RLVs. Though still in infancy stage, the region shows high potential for future market growth considering emerging interest in space tourism and innovations.

Reusable Launch Vehicles Market Competitive Landscape:

SpaceX

SpaceX is one of the key American aerospace corporations with significant control over the market segment of Reusable Launch Vehicles, delivering revolutionary products including Falcon 9 and Starship to deploy satellites, transfer cargos, and carry out deep space missions. The company’s range of reusable launch products along with massive research and development efforts are behind its dominance in the sphere of commercial spaceflights, whereas advancements which includes the use of methane fuel and fast cycle times contribute to SpaceX’s competitiveness.

-

In January 2026, SpaceX achieved over 350 successful re-flights of Falcon 9, underscoring its unmatched reliability and cost efficiency in orbital launches.

Blue Origin

Blue Origin is a leading aerospace company in the United States that currently has an increasing stake in the RLVs industry through products such as New Shepard, designed for space tourism, and New Glenn, aimed at delivering payloads into orbit. The diversity of Blue Origin's product line and significant private funding have ensured consistent growth, coupled with the development of innovative heavy reuse and advanced propulsion capabilities that increase its competitive advantage.

-

In April 2025, Blue Origin advanced development of New Glenn, targeting commercial satellite deployment and government payload launches with reusable heavy-lift capability.

United Launch Alliance (ULA)

The United Launch Alliance (ULA) is one of the top joint ventures operating in the U.S., formed by Boeing and Lockheed Martin and with significant operations in the Reusable Launch Vehicle market using their programs, including the Atlas and the upcoming Vulcan programs. The success that ULA has had in launching satellites for governmental agencies and its investment in advanced systems make it a frontrunner in providing reliable and secure access to space.

-

In December 2025, ULA progressed Vulcan Centaur development, integrating reusable components to enhance cost efficiency and maintain leadership in defense and national security launches.

Reusable Launch Vehicles Market Key Players:

Some of the Reusable Launch Vehicles Market Companies are:

-

SpaceX

-

Blue Origin

-

United Launch Alliance (ULA)

-

Northrop Grumman

-

Boeing

-

Lockheed Martin

-

Sierra Space

-

Rocket Lab

-

Arianespace

-

ArianeGroup

-

European Space Agency (ESA) partners

-

China Aerospace Science and Technology Corporation (CASC)

-

China Aerospace Science and Industry Corporation (CASIC)

-

Indian Space Research Organisation (ISRO)

-

Mitsubishi Heavy Industries (Japan)

-

JAXA (Japan Aerospace Exploration Agency)

-

Roscosmos (Russia)

-

Relativity Space

-

Firefly Aerospace

-

Virgin Galactic

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.83 Billion |

| Market Size by 2035 | USD 28.25 Billion |

| CAGR | CAGR of 13.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vehicle Type (Small Reusable Launch Vehicles, Medium Reusable Launch Vehicles, Heavy Reusable Launch Vehicles, Super Heavy Reusable Launch Vehicles, Others), • By Application (Satellite Deployment, Space Exploration, Cargo Delivery, Space Tourism, Others), • By End User (Government Agencies, Commercial Enterprises, Defense Organizations, Research Institutions, Others), • By Propulsion Technology (Liquid Propellant Engines, Hybrid Propulsion Systems, Methane-based Engines, Electric/Advanced Propulsion Concepts, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Blue Origin, United Launch Alliance (ULA), Northrop Grumman, Boeing, Lockheed Martin, Sierra Space, Rocket Lab, Arianespace, ArianeGroup, European Space Agency (ESA) partners, China Aerospace Science and Technology Corporation (CASC), China Aerospace Science and Industry Corporation (CASIC), Indian Space Research Organisation (ISRO), Mitsubishi Heavy Industries (Japan), JAXA (Japan Aerospace Exploration Agency), Roscosmos (Russia), Relativity Space, Firefly Aerospace, Virgin Galactic. |

Frequently Asked Questions

North America dominated with a 42.25% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 15.58% during 2026–2035.

Small Reusable Launch Vehicles dominated with a 28.97% share in 2025, while Super Heavy Reusable Launch Vehicles are projected to grow at the fastest CAGR of 15.58% during 2026–2035.

Growth is driven by increasing demand for satellite launches, rising space exploration missions, cost efficiency achieved through reusability, expanding commercial space enterprises, and emerging opportunities in space tourism.

The market is valued at USD 7.83 Billion in 2025 and is projected to reach USD 28.25 Billion by 2035.

The Reusable Launch Vehicles Market is projected to grow at a CAGR of 13.80% during 2026–2035.

Get in Touch