Satellite Bus Market Report Scope & Overview:

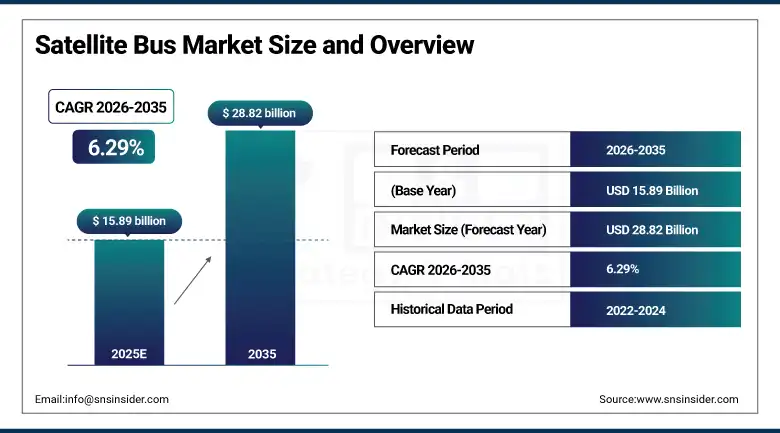

The Satellite Bus Market size is valued at USD 15.89 Billion in 2025 and is projected to reach USD 28.82 Billion by 2035, growing at a CAGR of 6.29% during the forecast period 2026–2035.

Insights on the Satellite Bus Market report provide a detailed study of platform architectures, modular spacecraft integration, and next-generation satellite subsystem innovations enabling communication, earth observation, navigation, and defense missions. The growth of the market is driven by factors such as rising deployment of LEO mega-constellations, increasing demand for high-speed global connectivity, rapid miniaturization of satellites, advancements in electric propulsion and AI-enabled onboard systems, and growing investments in commercial space infrastructure.

The deployment of satellite bus platforms has surpassed 12,500 active satellite systems across LEO, MEO, and GEO orbits in 2025.

Market Size and Forecast:

-

Market Size in 2025: USD 15.89 Billion

-

Market Size by 2035: USD 28.82 Billion

-

CAGR: 6.29% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Satellite Bus Market - Request Free Sample Report

Satellite Bus Market Trends:

-

Rising deployment of LEO mega-constellations and satellite internet programs is accelerating demand for modular and scalable satellite bus platforms.

-

Increasing shift toward small satellites (Nano, Micro, Mini) is driving high-volume, cost-efficient satellite bus manufacturing.

-

Rapid integration of AI-enabled onboard autonomy and software-defined satellite buses is improving mission flexibility and operational efficiency.

-

Growing adoption of electric propulsion and advanced power systems (EPS) is enhancing satellite lifespan and reducing launch mass requirements.

-

Expanding commercialization of space and rising participation of private players is accelerating satellite bus production and deployment cycles.

-

Increasing focus on standardized and reusable satellite bus architectures is improving manufacturing scalability and reducing development costs.

U.S. Satellite Bus Market Insights:

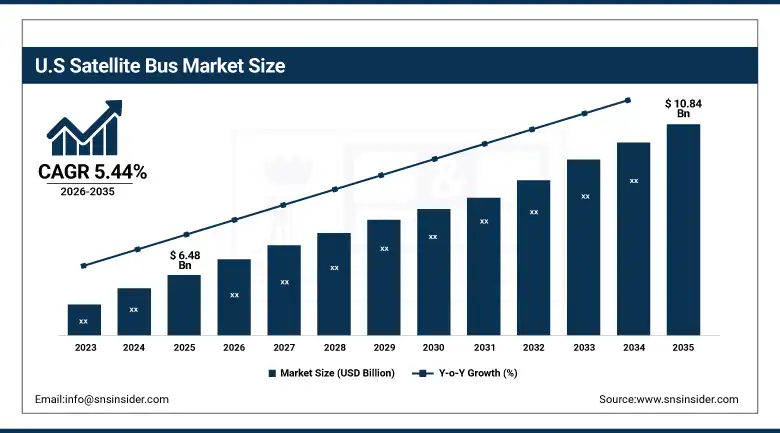

The U.S. Satellite Bus Market is projected to grow from USD 6.48 Billion in 2025 to USD 10.84 Billion by 2035, at a CAGR of 5.44%. The factors that will drive this growth are higher investment in the defense and commercial satellite industries, further proliferation of LEO mega-constellations, adoption of software-defined satellites (SDSs), presence of major aerospace and space technologies players, and incorporation of more advanced propulsion, power, and AI-driven onboard electronics for communications, earth observations, and navigation satellites.

Satellite Bus Market Growth Drivers:

-

Increasing deployment of LEO satellite constellations and global broadband programs is driving strong demand for advanced satellite bus platforms across commercial and defense applications.

One of the important drivers likely to fuel the Satellite Bus Market growth includes the rapid development of space-based communication services, including global Internet networks, Earth Observation Services, and Navigation Enhancement Services. The growing demand for highly scalable and cost-effective spacecraft solutions is propelling the adoption of satellite buses due to their standard nature. Modernization trends including the use of electric propulsion, artificial intelligence for enhanced autonomy, highly efficient power generation systems, and software-defined satellites have revolutionized the efficiency of satellite buses.

More than 62% of satellites deployed in 2025 will feature standardized or modular satellite bus platforms, primarily due to the deployment of LEO constellations and commercial space ventures.

Satellite Bus Market Restraints:

-

High development cost and complex integration of advanced satellite bus platforms are restraining rapid adoption across emerging space programs and small operators.

The high costs associated with developing and implementing the next generation of satellites featuring such advancements as electric propulsion, artificial intelligence for increased levels of autonomy, highly capable power generation capabilities, and modular designs is one of the key issues preventing the market from expanding. The need to utilize aerospace-grade parts, the time-intensive nature of development and extensive testing process add considerable expenses to projects. The reliance on expensive launches and precision manufacturing adds another layer of difficulty in the space business environment.

Satellite Bus Market Opportunities:

-

Expansion of commercial space ecosystems and private satellite mega-constellations is creating significant growth opportunities for advanced satellite bus platforms.

With the fast growth of commercial space businesses such as global broadband networks, earth observation firms, and space logistics ventures, there is a significant market potential for the Satellite Bus Market. The increasing demand for quick deployment, reusability of spacecraft chassis, and scalable satellite constellations is promoting manufacturers to design highly flexible and software-defined satellite bus platforms. With the commercialization of low Earth orbit infrastructure, the manufacture of satellite platforms in bulk is becoming increasingly economical.

By 2025, more than 60 percent of new satellite platforms' demands will be fulfilled by commercial and privately owned satellite constellations' satellite buses.

Satellite Bus Market Segmentation Analysis:

• By Satellite Type, Small Satellites (Nano, Micro, Mini) held the largest market share of 52.36% in 2025, while also expected to grow steadily at a CAGR of 6.78% during 2026–2035.

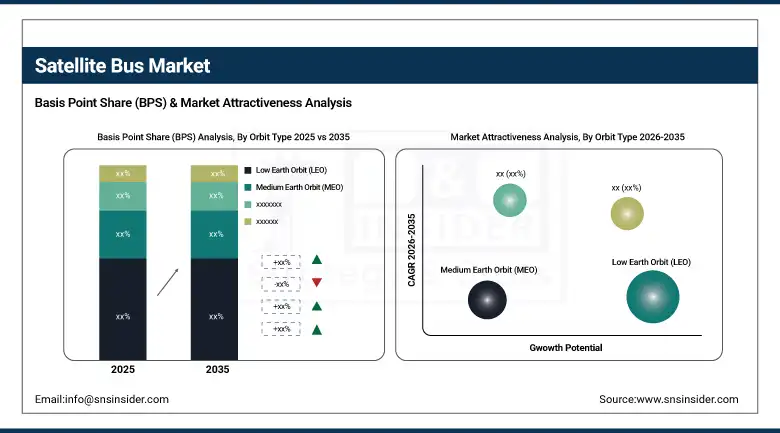

• By Orbit Type, Low Earth Orbit (LEO) held the largest market share of 54.45% in 2025, while Medium Earth Orbit (MEO) is expected to grow at the fastest CAGR of 7.72% during 2026–2035.

• By Application, Communication Satellites dominated with a 44.85% market share in 2025, while Earth Observation & Remote Sensing is expected to grow at the fastest CAGR of 7.59% during 2026–2035.

• By Subsystem, Power Systems (EPS) accounted for 24.58% market share in 2025, while Flight Software & Avionics is projected to grow at the fastest CAGR of 9.34% during 2026–2035.

• By End User, Commercial Operators dominated with a 52.14% market share in 2025, while Government Space Agencies are expected to grow steadily at a CAGR of 7.51% during 2026–2035.

By Satellite Type, Small Satellites Dominate and Also Grow Rapidly:

The Small Satellites (Nano, Micro, Mini) segment had a dominating presence in the market due to the development of LEO mega-constellation systems, demand for economical space structures, and inclination towards modular and standard satellite buses. The dominance of the segment is also driven by the increased need for quick manufacturing processes, reduced launch costs, and scalable approaches to space and military space missions.

The Small Satellites (Nano, Micro, Mini) segment was the fastest-growing segment because of the ongoing miniaturization of satellite payload systems, increasing involvement of private space organizations, and escalating demand for satellite deployment initiatives.

By Orbit Type, Low Earth Orbit (LEO) Dominates while Medium Earth Orbit (MEO) Grows Rapidly:

The Low Earth Orbit (LEO) segment was dominating the market because of the high use of satellite internet constellations, earth observation constellations, and low latency communication systems. The dominant position of the LEO segment is greatly explained by the commercialization of space-related projects, along with growing demand for connectivity solutions via satellite bus platforms.

Medium Earth Orbit (MEO) is the fastest-growing segment due to its increasing use in the field of navigation and communications systems and satellite bus hybrid systems. With increasing funding going into next generation navigation and positioning projects, there is greater adoption of the MEO satellites across different applications.

By Application, Communication Satellites Dominate while Earth Observation & Remote Sensing Grow Rapidly:

The Communication Satellites segment held the largest market share because of increasing demand for broadband connectivity and data transmission services in addition to growth in satellite internet networks worldwide. The market dominance of this segment is further fueled through persistent deployment of communication constellations in space.

Earth Observation & Remote Sensing is the fastest-growing segment on account of the growing demand for remote sensing systems in applications related to weather monitoring, disaster management, precision farming, and military intelligence. Increasing importance is being attached to satellites designed for earth observation due to their imaging capacity.

By Subsystem, Power Systems (EPS) Dominate While Flight Software & Avionics Grow Rapidly:

Power Systems (EPS) segment dominated the market of revenue due to its importance in maintaining reliable electricity generation, efficient electricity distribution, and satellite performance stability irrespective of the mission undertaken. The growing installation of high-power communication payloads and the electric propulsion system makes the requirement for effective power management architecture essential.

The Flight Software & Avionics segment has been observed to be the fastest-growing segment, owing to the growing need for satellite autonomy and software-controlled spacecraft performance.

By End User, Commercial Operators Dominate While Government Space Agencies Grow Rapidly:

Commercial Operators segment dominated the market due to the substantial growth in private space companies, satellite internet firms, and Earth observation services providers. The growing commercialization of space operations and demand for satellite constellations are some of the significant aspects contributing to the domination of this segment in the satellite bus market.

Government Space Agencies are among the fastest-growing segments, due to the high investments in space agencies, communication networks, and science missions. Growing space sovereignty, modernization of defense forces, and international collaborations are driving the adoption of satellite bus solutions in government-led projects.

Satellite Bus Market Regional Analysis:

North America Satellite Bus Market Insights:

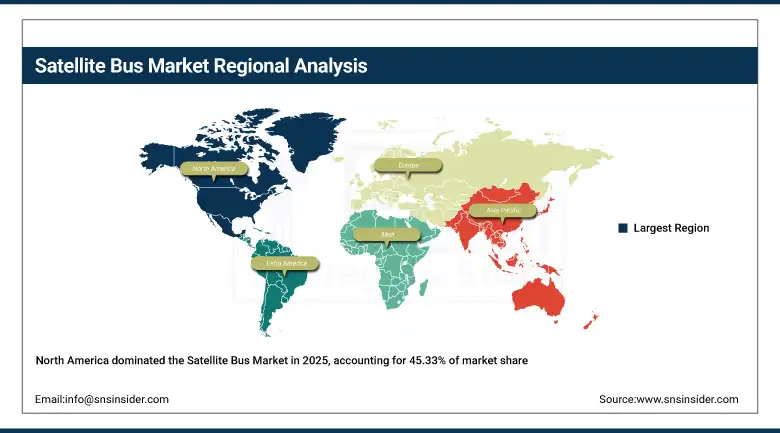

The North America Satellite Bus Market is dominant, holding a 45.33% share in 2025, Backed by the significant presence of aerospace and space technology companies, advanced manufacturing capabilities, and wide-scale adoption of commercial and defense satellite missions. The region has been able to capitalize on consistent investments into its space sector infrastructure, covering satellite internet systems, earth observation missions, and national security space endeavors. In addition to that, the integration of new-age modular satellite buses, electric propulsion, and artificial intelligence-based technologies further enhances the capabilities of the region in government and commercial space markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Satellite Bus Market Insights:

The U.S. Satellite Bus Market is driven by high levels of investments in space exploration missions, involvement of private space organizations, and early adaptation of innovative satellite bus systems. The country remains highly advanced in the deployment of mega-constellation satellite bus systems and satellite manufacturing infrastructure. There is an increasing trend of development of software-definable satellite bus systems, and reusable spacecraft in the market.

Asia-Pacific Satellite Bus Market Insights:

The Asia-Pacific Satellite Bus Market is the fastest-growing region, projected to expand at a CAGR of 7.29% during 2026–2035. It is fueled by growing space missions, increased satellite launches, and rising funding for satellite-based communications and earth observation systems. Nations like China, India, Japan, and South Korea are investing heavily in improving their capabilities in satellite manufacturing and developing domestic satellite bus platforms. Rising demand for satellite-based connectivity services, monitoring natural disasters, and navigations are fueling the growth of the regional market. Private enterprises are also increasingly taking part in space missions, adding further impetus to the growth of the market.

China Satellite Bus Market Insights:

The China Satellite Bus Market is fueled by the growing number of space missions, increased government investment in satellite manufacturing capabilities, and emphasis on becoming technologically self-sufficient. China is developing large satellite networks for applications related to communications, navigation, and earth observation. Advances in technologies like electric propulsion, autonomous systems, and advanced satellite bus architecture are making missions more efficient.

Europe Satellite Bus Market Insights:

The Europe Satellite Bus market is characterized by an extensive level of collaboration between the leading space agencies and established aerospace players as well as between various regional space programs backed by the European Space Agency. Currently, many countries such as France, Germany, and Italy have invested significantly in sophisticated satellite bus systems for earth observation, communication, and scientific missions. There are a number of factors driving the Europe Satellite Bus market which includes the region's extensive engineering expertise aimed at designing reliable space crafts and conducting sustainable space operations and missions.

Germany Satellite Bus Market Insights:

Germany plays a significant role in shaping the Europe Satellite Bus Market considering the extensive capabilities that the country has in terms of space engineering as well as aerospace manufacturing. The country has been making significant strides in designing highly precise satellite bus systems for various earth observation, environmental monitoring, and communication purposes. Various investments in engineering institutions and research programs have been instrumental in shaping the country's engineering prowess in designing modular satellite systems.

Latin America Satellite Bus Market Insights:

The Latin America Satellite Bus Market is witnessing steady growth due to increasing demand for satellite-based communication and Earth observation and monitoring systems. Countries like Brazil, Mexico, and Argentina are gradually indulging in space projects either on a national level or even through collaboration with other countries. Systems that assist in disaster management, agricultural monitoring, and providing connectivity to remote locations have made the installation of satellite bus systems more necessary. Space coalitions and technological advancements are helping countries establish efficient satellite bus systems.

Middle East & Africa Satellite Bus Market Insights:

The Middle East & Africa Satellite Bus Market is flourishing owing to growing investments in national space programs and the growing focus on space communication and surveillance technologies. Nations like UAE, Saudi Arabia, and South Africa are progressively investing in satellite technology through strategic alliances and space missions. The growing focus on earth observation, smart city construction, and security systems is promoting the demand for sophisticated satellite bus systems. Collaboration with foreign aerospace firms and indigenous space technology development are contributing to long-term regional success and technological evolution.

Satellite Bus Market Competitive Landscape:

The Airbus SE is an industry-leading aerospace and space systems manufacturer known for being a significant competitor in the satellite bus industry owing to its state-of-the-art spacecraft designs employed in communications, earth observation, and navigation operations. It has achieved a competitive advantage from its modular satellite bus architecture design, highly reliable avionics, and integration of electric propulsion. Its efforts toward developing space systems, such as software defined satellites and low earth orbit satellite constellation platforms, have improved its competitiveness in satellite production.

-

In February 2025, Airbus SE advanced its next-generation satellite bus programs by enhancing modular platform capabilities and expanding standardized spacecraft production for LEO and GEO missions, reinforcing its position in large-scale commercial satellite deployments.

The Lockheed Martin Corporation is one of the leading players in the industry due to its robust offerings of space systems, defense satellites, and satellite bus integration technologies. The company uses its expertise in secure communications, deep space exploration, and robust satellite design to develop efficient and reliable satellite buses. Lockheed Martin Corporation's consistent emphasis on space defense systems, autonomous operation of satellites, and resilience makes the organization stand out in government and defense applications. Strategic partnerships with space organizations further enhance its significance in satellite bus manufacturing.

-

In March 2025, Lockheed Martin advanced its satellite bus capabilities through upgrades in next-generation space systems and modular spacecraft platforms designed for resilient communication and defense missions across multiple orbital environments.

Northrop Grumman Corporation has been a major innovator within the satellite bus industry, owing to its expertise in developing advanced spacecraft buses, space logistics vehicles, and satellites. This organization has a significant focus on providing extremely reliable satellite bus systems for use in national security, intelligence, and commercial space applications. Northrop Grumman’s continued dedication to developing autonomous space systems, electric propulsion technology, and mission flexibility makes it a leader in space infrastructure for the future.

-

In April 2025, Northrop Grumman enhanced its satellite bus portfolio through advancements in autonomous space platforms and modular spacecraft systems, strengthening its capabilities in defense-oriented and deep-space missions.

Satellite Bus Market Key Players:

Some of the Satellite Bus Market Companies are:

-

Airbus SE

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

The Boeing Company

-

Thales Alenia Space (Thales Group)

-

Honeywell International Inc.

-

Sierra Space Corporation

-

Israel Aerospace Industries (IAI)

-

Ball Aerospace

-

L3Harris Technologies

-

Maxar Technologies

-

OHB SE

-

Mitsubishi Electric Corporation

-

Indian Space Research Organisation (ISRO)

-

Rocket Lab USA

-

Terran Orbital Corporation

-

Surrey Satellite Technology Ltd (SSTL)

-

Kratos Defense & Security Solutions

-

Blue Canyon Technologies (RTX)

-

GomSpace A/S

Satellite Bus Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.89 Billion |

| Market Size by 2035 | USD 28.82 Billion |

| CAGR | CAGR of 6.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Connectivity Services, Content Services, Software & Middleware, Others) • By Connectivity Type (Satellite-Based Connectivity, Air-to-Ground (ATG) Connectivity, Hybrid Connectivity, Others) • By Aircraft Type (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Jets, Business Jets, Others) • By Offering (IFE Hardware, Internet Connectivity, Streaming & Content Services, Live TV Services, E-commerce / Onboard Retailing, Others) • By Fit Type (Line Fit, Retrofit, Others) • By End User (Commercial Airlines, Business Aviation, Government / Defense Aircraft, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, The Boeing Company, Thales Alenia Space (Thales Group), Honeywell International Inc., Sierra Space Corporation, Israel Aerospace Industries (IAI), Ball Aerospace, L3Harris Technologies, Maxar Technologies, OHB SE, Mitsubishi Electric Corporation, ISRO (Indian Space Research Organisation), Rocket Lab USA, Terran Orbital Corporation, Surrey Satellite Technology Ltd (SSTL), Kratos Defense & Security Solutions, Blue Canyon Technologies (RTX), GomSpace A/S |

Frequently Asked Questions

Small Satellites (Nano, Micro, Mini) dominated with a 52.36% share in 2025, while Small Satellites (Nano, Micro, Mini) are also projected to grow at the fastest CAGR of 6.78% during 2026–2035.

North America dominated with a 45.33% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 7.29% during 2026–2035.

Growth is driven by rising deployment of LEO mega-constellations, increasing demand for global broadband connectivity, and growing adoption of modular and software-defined satellite bus platforms.

The market is valued at USD 15.89 Billion in 2025 and is projected to reach USD 29.82 Billion by 2035.

The Satellite Bus Market is projected to grow at a CAGR of 6.29% during 2026–2035.

Get in Touch