Semiconductor Lead Frame Market Size

Get more information on Semiconductor Lead Frame Market - Request Free Sample Report

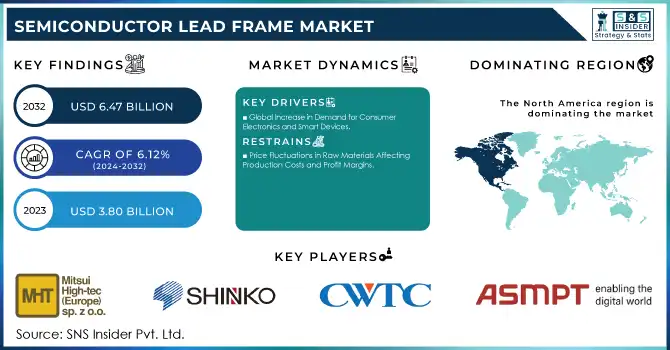

The Semiconductor Lead Frame Market Size was valued at USD 3.80 Billion in 2023 and is expected to reach USD 6.47 Billion by 2032 and grow at a CAGR of 6.12% over the forecast period 2024-2032.

The Semiconductor Lead Frame Market had experienced tremendous developments in the years 2023 and 2024, led by a wave of technological innovations and increasing requirements in various industries. Countries like Japan, China, the USA, France, Germany, and India were major contributors to the general trends of the Semiconductor Lead Frame Market. For example, government initiatives from China have considerably enhanced domestic production capacity and the USA's CHIPS Act has offered incentives for domestic manufacturing of semiconductors, leading to growth in the area of lead frame applications. For instance, in December 2024, the US Department of Commerce announced that it has completed a USD 6.165 billion subsidy for Micron Technology, an American chipmaker, to enhance local semiconductor manufacturing. Japan still leads in the use of high-precision semiconductor technology, driven by government-backed R&D programs. Germany and France have emphasized the improvement of their semiconductor industries with funding from the European Union, and India's "Make in India" program has also created a new window for local semiconductor manufacturing.

Technological developments in 2023 and 2024 have pushed the adoption of advanced lead frame designs, including multi-layered and miniaturized frames for compact devices. Further propelling the growth of the market were a number of launches within the same period, like leading-edge lead frames for 5G and IoT. Lead frames in power electronics find growth prospects amid increasing adoption of electric vehicles and renewable energy systems. In the future, rising applications of artificial intelligence, robotics, and smart home appliances will also offer good growth opportunities in high-performance semiconductors.

From the perspectives of governments and industries, this research reveals a rise in concern towards sustainability, and in turn, eco-friendly lead frame materials are witnessing higher demand across the world. Further, geopolitical influences and policies promoting semiconductor self-reliance have inspired investment in localized production capabilities around the world. With collaboration between governments and the private sector, combined with new packaging technologies entering the fray, the landscape is evolving. As the world accelerates its digital transformation, the semiconductor lead frame market is set to cater to the ever-growing needs of next-generation electronic applications.

Semiconductor Lead Frame Market Dynamics

KEY DRIVERS:

-

Global Increase in Demand for Consumer Electronics and Smart Devices

The consumer electronics segment holds a significant share in the Semiconductor Lead Frame Market. Already as of 2023, it reaches to more than 50% of households around the globe where these have at least one smart device. In India, subsidies launched by the government for domestic electronics manufacturing increase demand further to semiconductors while products like smartphones, wearables, or home automation systems rely massively on integrated circuits made available through advanced lead frames. Consequently, consumer electronics induce innovation and higher production, which supports the market.

-

Expansion of 5G Infrastructure and Telecommunications Networks around the Globe

With the launch of 5G around the globe in 2023, telecommunication networks have been upgraded significantly. Lead frames are crucial in enabling high-speed processors and antennas required for 5G. Research states that by the end of 2024, 65% of mobile subscribers in the Asia-Pacific region will use 5G. It fuels demand for lead frames optimized for high-frequency and low-latency applications, which supports robust market growth.

RESTRAIN:

-

Price Fluctuations in Raw Materials Affecting Production Costs and Profit Margins.

Copper is a primary constituent of lead frames, and the prices have gone through a fluctuation of over 20% in the last two years, due to supply chain disruptions and geopolitical tensions. Japan and the US governments report rising costs in their domestic manufacturing industries, leading to narrower margins for lead frame manufacturers.

The changes are directly impactful on the cost of producing and will serve as a hindrance for the manufacturers that intend to expand production. In addition, price instability of raw materials tends to delay innovation and new product introductions as the firms allocate their resources to combat rising costs. Stabilizing material supplies will need more powerful sourcing strategies and collaboration by governments.

Semiconductor Lead Frame Market Segmentation Analysis

by Industry Vertical

The Telecommunication segment dominated the Semiconductor Lead Frame Market in 2023 with 34% market share, driven by rapid deployment of 5G networks and advancements in communication infrastructure. This dominance has further been supported by the adoption of sophisticated lead frames for high-speed processing and low-latency communication equipment.

The Consumer Electronics segment is expected to witness the fastest growth at a CAGR of 7% during 2024-2032. The trend of adoption of smart devices and home automation systems is witnessing growth due to innovation in wearable technology, smart appliances, and connected home solutions. Support by governments in the regions of Asia-Pacific and North America for local electronics manufacturing adds to growth. As consumers demand greater convenience and connectivity, the need for high-end semiconductor components in consumer electronics is increasing.

by Application

Integrated circuits segment dominated 2023 with 73% market share, driven by their important application in consumer electronics, automotive systems, and telecommunications. Advances of ICs integrated within small devices and lead frames integrated within multi-layered designs contribute to the growth of the segment.

With integrated circuits projected to expand at the fastest CAGR of 6.24% over the given forecast period 2024-2032, because of rapid demand for AI-driven technology and IoT-enabled devices, there also lies a minor discrete device, necessary for applications in power management and signal processing.

Semiconductor Lead Frame Market Regional Outlook

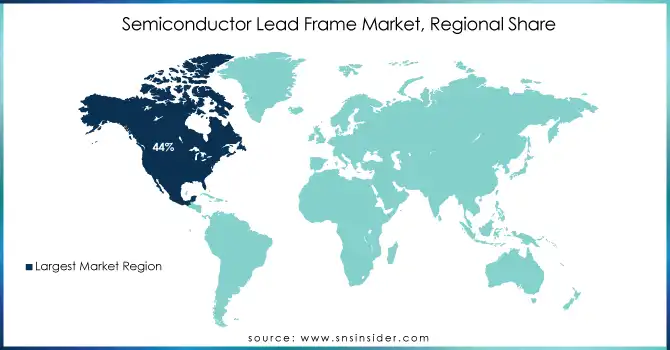

The North America region held the highest market share of 44% in 2023, driven by strong government support through the CHIPS Act and an already established semiconductor industry. In December 2024, German engineering firm has a preliminary agreement for as much as USD 225 million in direct funding from the CHIPS Act to support its USD 1.9 billion investment in a semiconductor manufacturing facility being built in Roseville. The region's focus on research and innovation, particularly in the USA, has cemented its leadership. Investments in state-of-the-art technologies, such as advanced semiconductor packaging and 3D stacking, have supported this market.

Asia-Pacific is likely to grow at the fastest CAGR of 6.80% in the forecast period 2024-2032. Growth drivers are China, Japan, and India; massive investments in semiconductor manufacturing along with the benefits of pro-government policies. China's efforts in becoming a global semiconductor hub and India's "Make in India" campaign mark the region's commitment to expanding its market presence. Precision semiconductor components in Japan and memory chip technology in South Korea are also major growth contributors for the region. This combination of strategic investments and technological breakthroughs positions Asia-Pacific as a critical player in shaping the future of the Semiconductor Lead Frame Market.

Need any customization research on Semiconductor Lead Frame Market - Enquiry Now

Key Players

Some of the major players in the Semiconductor Lead Frame Market are

-

Mitsui High-tec, Inc. (Lead Frames, Lead Frame Materials)

-

Shinko Electric Industries Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Chang Wah Technology Co., Ltd. (Lead Frames, Lead Frame Materials)

-

ASM Pacific Technology Ltd. (Lead Frames, Lead Frame Materials)

-

Enomoto Co., Ltd. (Lead Frames, Lead Frame Materials)

-

POSSEHL Electronics Deutschland GmbH (Lead Frames, Lead Frame Materials)

-

SDI Corporation (Lead Frames, Lead Frame Materials)

-

Fusheng Electronics Corporation (Lead Frames, Lead Frame Materials)

-

Ningbo Kangqiang Electronics Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Jentech Precision Industrial Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Dynacraft Industries Sdn. Bhd. (Lead Frames, Lead Frame Materials)

-

QPL Limited (Lead Frames, Lead Frame Materials)

-

Samsung Electro-Mechanics Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Sumitomo Metal Mining Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Shenzhen Sunlord Electronics Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Advanced Assembly Materials International Ltd. (Lead Frames, Lead Frame Materials)

-

HAESUNG DS Co., Ltd. (Lead Frames, Lead Frame Materials)

-

I-Chiun Precision Industry Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Jentech Precision Industrial Co., Ltd. (Lead Frames, Lead Frame Materials)

-

Ningbo Hualong Electronics Co., Ltd. (Lead Frames, Lead Frame Materials)

Major Suppliers (Components, Technologies)

-

Gotoh Manufacturing Co., Ltd. (Alloy Strips for Lead Frames)

-

Proterial Ltd. (Hitachi Metals Co., Ltd.) (Alloy Strips for Lead Frames)

-

Poongsan Corporation (Lead Frame Alloys)

-

DOWA Metaltech Co., Ltd. (Alloy Strips for Lead Frames)

-

Ningbo Hualong Electronics Co., Ltd. (Lead Frame Materials)

-

Changsha Saneway Electronic Materials Co., Ltd. (Heat Sinks for Semiconductor Packaging)

Recent Trends

-

December 2024: Haesung DS sets up more production lines to grow its lead frame business for auto IC substrates, Korean reports say.

-

August 2024: Chang Wah Technology (CWTC) subsidiary specializing in lead frame held a board meeting, approving an expansion plan for the Malaysian facility with a preliminary capital expenditure of USD 100 million.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.80 Billion |

| Market Size by 2032 | USD 6.47 Billion |

| CAGR | CAGR of 6.12% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Copper Lead Frames, Copper Alloy, Lead Frames, Iron-Nickel Lead Frames, Others) • By Packaging Type (Dual Inline Pin Package, Small Out-Line Package, Small Outline Transistor, Quad Flat Pack, Dual Flat No-Leads, Quad Flat No-Leads, Flip Chip, Others) • By Industry Vertical (Consumer Electronics, Automotive Electronics, Industrial Electronics, Telecommunication, Others) • By Type (Stamping Process Lead Frame, Etching Process Lead Frame) • By Application (Integrated Circuit, Discrete Device) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Mitsui High-tec, Inc., Shinko Electric Industries Co., Ltd., SDI Corporation, ASM Pacific Technology, Samsung Electro-Mechanics, Chang Wah Technology Co., Ltd., POSSEHL Electronics, Enomoto Co., Ltd., JIH LIN Technology Co., Ltd., LG Innotek, Hualong Electronics Co., Ltd., I-Chiun Precision Industry Co., Ltd., Jentech Precision Industrial Co., Ltd., QPL Limited, Dynacraft Industries Sdn. Bhd., Yonghong Technology Co., Ltd., WuXi Micro Just-Tech, Toppan Inc., Advanced Assembly Materials International Ltd., HAESUNG DS Co., Ltd. |

| Key Drivers | • Global Increase in Demand for Consumer Electronics and Smart Devices. • Expansion of 5G Infrastructure and Telecommunications Networks around the Globe. |

| Restraints | • Price Fluctuations in Raw Materials Affecting Production Costs and Profit Margins. |

Frequently Asked Questions

Ans: Mitsui High-tec, Inc., Shinko Electric Industries Co., Ltd., SDI Corporation, ASM Pacific Technology, Samsung Electro-Mechanics, Chang Wah Technology Co., Ltd., POSSEHL Electronics, Enomoto Co., Ltd., JIH LIN Technology Co., Ltd., LG Innotek, Hualong Electronics Co., Ltd., I-Chiun Precision Industry Co., Ltd., Jentech Precision Industrial Co., Ltd., QPL Limited, Dynacraft Industries Sdn. Bhd., Yonghong Technology Co., Ltd., WuXi Micro Just-Tech, Toppan Inc.

Ans: The Semiconductor Lead Frame Market is expected to grow at a CAGR of 6.12% during 2024-2032.

Ans: Semiconductor Lead Frame Market size was USD 3.80 Billion in 2023 and is expected to Reach USD 6.47 Billion by 2032.

Ans: The major growth factors of the Semiconductor Lead Frame Market is Global Increase in Demand for Consumer Electronics and Smart Devices.

Ans: North America dominated the Semiconductor Lead Frame Market in 2023.

Get in Touch