Vetronics Market Report Scope & Overview:

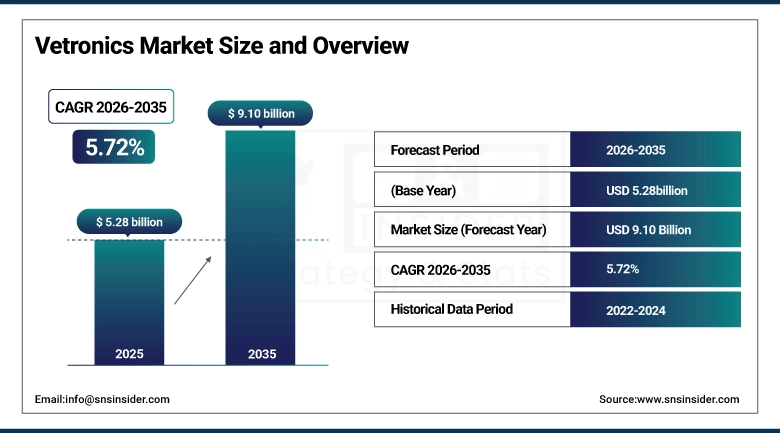

The Vetronics Market size is valued at USD 5.28 Billion in 2025 and is projected to reach USD 9.10 Billion by 2035, growing at a CAGR of 5.72% during the forecast period 2026–2035.

Overview & Analysis of the Vetronics Market is provided in the Vetronics Market analysis report, which focuses on the dynamics of the market, innovations in system integration, and platform modernization in defense vehicles. The growing trends in defense modernization initiatives, digital battlefield technologies, AI systems, and armored/unmanned ground vehicles are propelling high growth for the market from 2026 to 2035.

Deployments of Vetronics are increasing at a significant rate among various defense fleets, driven by the increased demand for advanced armored vehicles.

Market Size and Forecast:

-

Market Size in 2025: USD 5.28 Billion

-

Market Size by 2035: USD 9.10 Billion

-

CAGR: 5.72% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vetronics Market - Request Free Sample Report

Vetronics Market Trends:

-

Rising defense modernization programs are driving increased adoption of advanced Vetronics across armored vehicles and combat platforms.

-

Growing integration of AI-enabled, digital, and network-centric architectures is enhancing battlefield connectivity, automation, and decision-making capabilities.

-

Increasing deployment of unmanned ground vehicles (UGVs) and semi-autonomous platforms is boosting demand for advanced vetronics integration.

-

Expansion of situational awareness, sensor fusion, and real-time data processing technologies is improving operational effectiveness and mission readiness.

-

Development of modular, open-architecture Vetronics is enabling interoperability, upgradeability, and reduced lifecycle costs for defense forces.

-

Increasing investments in secure communication systems, cybersecurity, and electronic warfare resilience are strengthening vetronics system reliability in modern combat environments.

U.S. Vetronics Market Insights:

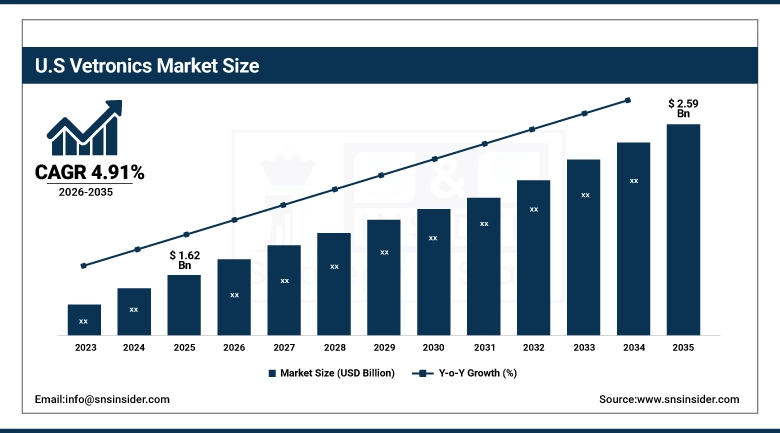

The Vetronics Market in the U.S. is projected to grow from USD 1.62 Billion in 2025 to USD 2.59 Billion by 2035, at a CAGR of 4.91%. The increasing modernization initiatives, the purchase of high-end armored combat vehicles, and the growing acceptance of AI-based and network-centric Vetronics solutions are among the key factors driving this market's growth.

Vetronics Market Growth Drivers:

-

Rising defense modernization programs and increasing adoption of advanced Vetronics across armored and combat vehicles are driving market growth.

With increasing investments in cutting-edge military platforms such as main battle tanks (MBTs), infantry fighting vehicles (IFVs), and unmanned ground vehicles (UGVs), the need for advanced vetronic systems will continue to rise. The military and original equipment manufacturers (OEMs) have been shifting focus toward advanced technologies that incorporate AI, digital, and networked solutions to improve their ability to command, control, communicate, navigate, and monitor situational awareness. Moreover, due to increasing focus on digitization on the battleground, collaboration among defense contractors, system integrators, and technology providers will further speed up deployments.

Over 60% of modern armored and combat vehicle programs in 2025 incorporated advanced Vetronics to enhance situational awareness, communication, and mission effectiveness.

Vetronics Market Restraints:

-

High procurement and integration costs of advanced Vetronics along with budget constraints in defense spending are restraining widespread adoption.

High expenses related to designing, integration, and maintenance of high-end Vetronics equipment continue to be an important restriction for the Vetronics market. Current solutions that use artificial intelligence-based systems, fused sensors, secure communications, and network-based systems involve huge initial investments, thus restricting their implementation in budget-conscious defense initiatives and defense forces with limited funding. Besides, the process of installing them into current armored and combat vehicles is not simple either, and requires additional costs and time.

Vetronics Market Opportunities:

-

Growing adoption of AI-enabled, network-centric, and software-defined Vetronics presents significant market expansion opportunities.

Increasing levels of convergence among AI analytics, sensor fusion, and modular open architecture-based platforms can prove very beneficial for the Vetronics Market. The incorporation of next-generation vetronics by defense forces, OEMs, and integrators is gaining prominence to achieve greater connectivity and faster decision-making capabilities on the battlefield. Innovations related to digital communication systems, cybersecurity architecture, and unmanned ground vehicles (UGVs) are driving developments within the market. There has been increased collaboration among defense companies, technology vendors, and research firms, which has resulted in innovations within the field of vetronics.

Over 45% of newly procured and upgraded defense vehicles in 2025 incorporated AI-enabled or digitally networked vetronics solutions to improve operational efficiency, situational awareness, and mission coordination.

Vetronics Market Segmentation Analysis:

-

By System / Component Type, Command & Control Systems held the largest market share of 28.25% in 2025, while Communication Systems are expected to grow at the fastest CAGR of 7.48% during 2026–2035.

-

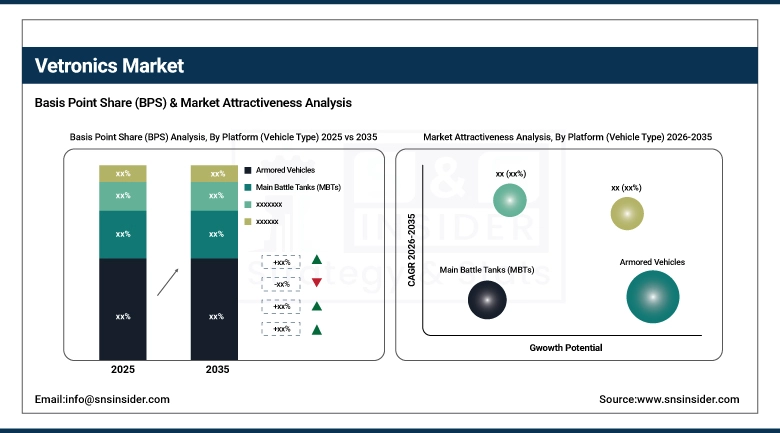

By Platform (Vehicle Type), Armored Vehicles held the largest market share of 24.25% in 2025, while Light Protected Vehicles are expected to grow at the fastest CAGR of 7.36% during 2026–2035.

-

By Technology, Digital Vetronics held the largest market share of 30.25% in 2025, while AI-enabled Vetronics are expected to grow at the fastest CAGR of 8.50% during 2026–2035.

-

By Application, Combat Operations held the largest market share of 28.12% in 2025, while Surveillance & Reconnaissance is expected to grow at the fastest CAGR of 6.50% during 2026–2035.

-

By End User, Defense Forces (Army, Marines, etc.) held the largest market share of 55.23% in 2025, while Defense Contractors / Integrators are expected to grow at the fastest CAGR of 5.54% during 2026–2035.

By System / Component Type, Command & Control Systems Dominate While Communication Systems Grow Rapidly:

Command & Control Systems segment dominated the market due to their critical role in mission coordination, battlefield decision-making, and integration of multiple subsystems across armored and combat vehicles. This segment is widely relied upon by defense forces and OEMs for real-time operational control and situational coordination.

Communication Systems are the fastest-growing segment, driven by increasing demand for secure data exchange, network-centric warfare capabilities, and interoperable communication across platforms. Adoption is expanding in modernized defense vehicles and unmanned ground platforms, highlighting rapid integration of advanced communication architectures.

By Platform (Vehicle Type), Armored Vehicles Dominate While Light Protected Vehicles Grow Rapidly:

Armored Vehicles segment dominated the market due to widespread deployment across defense fleets and their integral role in combat operations and troop protection. Consistent procurement and upgrade programs across major defense markets continue to support this dominance.

Light Protected Vehicles are the fastest-growing segment, driven by rising demand for mobility, rapid deployment, and protection in asymmetric warfare scenarios. Increasing use in patrol, reconnaissance, and border security operations is accelerating adoption of lighter and more versatile platforms.

By Technology, Digital Vetronics Dominate While AI-enabled Vetronics Grow Rapidly:

Digital Vetronics segment dominated the market due to their widespread adoption in modern defense vehicles, enabling integrated command, control, communication, and navigation capabilities. In 2025, deployments reached 30.25 units, reflecting strong transition from analog to digital architectures across defense platforms.

AI-enabled Vetronics are the fastest-growing segment, driven by increasing incorporation of artificial intelligence, sensor fusion, and autonomous decision-support systems. Adoption is accelerating across advanced military platforms, enhancing situational awareness, predictive maintenance, and real-time battlefield analytics, leading to rapid integration in next-generation defense vehicles.

By Application, Combat Operations Dominate While Surveillance & Reconnaissance Grow Rapidly:

Combat Operations segment dominated the market due to the extensive use of Vetronics in armored and combat vehicles for mission execution, fire control, coordination, and battlefield communication. This reflects strong reliance on integrated systems to support real-time command, control, and operational effectiveness across defense platforms.

Surveillance & Reconnaissance are the fastest-growing segment, driven by increasing demand for real-time intelligence, monitoring, and target identification across modern battlefields. Adoption is supported by the growing use of sensor integration, unmanned systems, and advanced data processing capabilities, enabling enhanced situational awareness and mission planning.

By End User, Defense Forces Dominate While Defense Contractors / Integrators Grow Rapidly:

Defense Forces (Army, Marines, etc.) segment dominated the market as the primary users of vetronics systems, accounting for large-scale deployment across armored vehicles, infantry platforms, and specialized combat units. This reflects strong procurement programs, fleet modernization initiatives, and reliance on integrated electronic systems for operational superiority.

Defense Contractors / Integrators are the fastest-growing segment, driven by increasing outsourcing of system integration, platform modernization programs, and collaborations with OEMs and technology providers. Their expanding role in assembling, integrating, and upgrading vetronics architectures for next-generation defense vehicles is accelerating market growth.

Vetronics Market Regional Analysis:

North America Vetronics Market Insights:

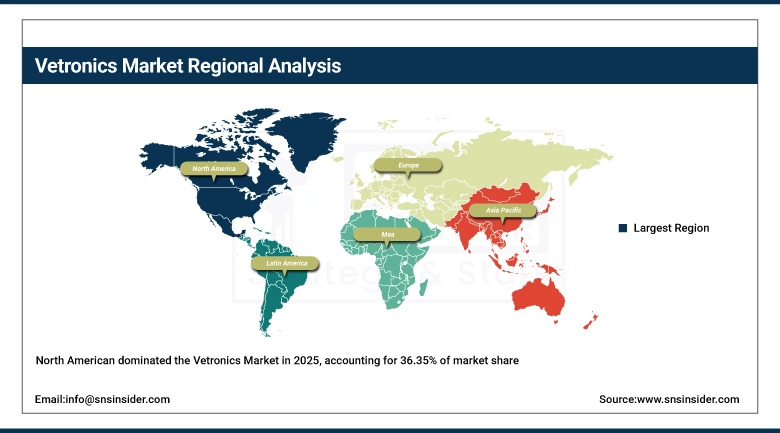

The North America Vetronics Market is dominant, holding a 36.35% share in 2025, supported by advanced defense infrastructure, strong military spending, and early adoption of integrated electronic systems across armored and combat vehicles. The region benefits from continuous modernization programs, high investment in next-generation battlefield technologies, and strong presence of leading defense contractors. Increasing deployment of advanced communication systems, sensor fusion, and electronic control units across defense platforms enhances operational efficiency. The presence of established procurement frameworks, R&D capabilities, and collaborations between defense agencies and technology providers further reinforces North America’s leadership in the Vetronics market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Vetronics Market Insights:

The market for Vetronics in the United States is being spurred by huge projects for modernization, a high defense budget, and the presence of highly developed electronic systems aboard military equipment on land. Digitizing the battlefield and enabling real-time information exchanges are critical aspects that contribute to vetronics integration into armored vehicles and tactical groups. Regular upgrading of combat fleets, the trend toward network-centric warfare, and cooperation between defense authorities and systems integrators are some of the key driving forces behind rapid growth and development in the local market.

Asia-Pacific Vetronics Market Insights:

The Asia-Pacific Vetronics Market is the fastest-growing region, projected to expand at a CAGR of 7.30% during 2026–2035. It is supported by rising defense expenditures, territorial security concerns, and increasing investments in armored vehicle modernization programs across countries such as China, India, Japan, and South Korea. Growing focus on indigenous defense manufacturing, expansion of military fleets, and adoption of advanced electronic systems for surveillance, navigation, and communication are driving demand. Rapid technological advancements, coupled with government initiatives to strengthen defense capabilities and enhance battlefield awareness, are accelerating the integration of Vetronics across new and upgraded platforms in the region.

China Vetronics Market Insights:

The China Vetronics Market is fueled by defense modernization, efficient manufacturing capabilities, and increasing deployment of electronic devices in armor and military applications. Increasing investments in research and development, and emphasis on self-reliance in defense technology, is facilitating the adoption of vetronics systems. Expansion of mechanized armed forces, emphasis on digital battlefield solutions, and upgrading of communications, control, and sensors technologies will help position China as a significant player in the Asia-Pacific region.

Europe Vetronics Market Insights:

The Europe Vetronics Market is fueled by strong defense modernization trends, emphasis on armored fleet upgrade projects, and sophisticated technology infrastructure across Germany, France, and the UK. The region enjoys efficient manufacturing ecosystem, cross-border partnerships, and sustained investment in digital battlefield technologies. Rising adoption of electronic control units, communications, and sensor-driven technologies across military assets enhances the operational efficiency of defense systems. Moreover, governmental initiatives, emphasis on interoperability of allied defense forces, and sustained research and development activity in defense electronics helps consolidate Europe's presence in the Vetronics market.

Germany Vetronics Market Insights:

Germany represents a significant market in Europe owing to efficient defense manufacturing capability and robust engineering expertise. Rising defense modernization activities include the adoption of advanced onboard electronics and integration of next generation communication, and control technologies. Partnerships between indigenous and international defense contractors and upgrading of existing platforms with vetronics solutions are making Germany prominent in regional Vetronics market.

Latin America Vetronics Market Insights:

The Latin America Vetronics Market is expected to grow steadily due to increasing defense expenditure in the region and modernization of existing military fleets. Increasing emphasis on border protection, surveillance capability, and tactical mobility drives the adoption of electronic devices and integrated systems in the defense vehicles in the region. However, constrained financial budget hinders the adoption of advanced solutions in the market. Partnerships between global defense providers and incremental fleet modernization is expected to drive the Latin American market for vetronics systems.

Middle East and Africa Vetronics Market Insights:

The Middle East & Africa Vetronics Market is witnessing growth due to rising defense spending, geopolitical factors, and increasing procurement of advanced armored vehicles. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are investing in modernizing their military capabilities with integrated electronic systems for improved battlefield performance. Expansion of defense infrastructure, collaborations with international defense manufacturers, and growing focus on surveillance, communication, and command systems are driving adoption.

Vetronics Market Competitive Landscape:

Lockheed Martin Corporation is a leading U.S. aerospace and defense company with a strong presence in the Vetronics market through its advanced mission systems, integrated vehicle electronics, and battlefield digitization solutions. The company focuses on developing next-generation command, control, communication, computing, intelligence, surveillance, and reconnaissance (C4ISR) capabilities integrated into armored and tactical vehicles. Its extensive R&D investments, strong government contracts, and collaborations with defense agencies enable continuous innovation in modular vetronics architectures, enhancing situational awareness, interoperability, and mission effectiveness across modern combat platforms

-

In March 2025, Lockheed Martin advanced its integrated mission systems initiatives by enhancing open-architecture vetronics solutions designed to improve real-time data sharing, sensor fusion, and battlefield connectivity across multi-domain operations.

RTX Corporation is a major U.S. defense and aerospace company with a strong role in the Vetronics market through its advanced electronics, sensors, and communication technologies. The company specializes in integrating electronic warfare systems, secure communication modules, and sensor-based solutions into military vehicles, enabling enhanced operational awareness and mission coordination. Its focus on digital engineering, modular system integration, and advanced battlefield connectivity supports the development of scalable vetronics architectures. Strategic partnerships with defense organizations and continuous innovation in defense electronics strengthen RTX’s position in next-generation armored vehicle systems and modern warfare technologies.

-

In June 2025, RTX expanded its next-generation battlefield electronics portfolio by advancing integrated communication and sensing systems designed to improve interoperability, targeting accuracy, and real-time decision-making in armored platforms.

Northrop Grumman Corporation is a leading U.S. defense technology company with significant contributions to the Vetronics market through its expertise in autonomous systems, electronic systems, and advanced mission solutions. The company focuses on integrating onboard computing, sensor fusion, and control systems into military vehicles to enhance situational awareness and operational efficiency. Its strong emphasis on autonomy, AI-enabled systems, and digital battlefield technologies supports the evolution of smart vetronics architectures. With robust R&D capabilities, long-standing defense contracts, and collaboration with military agencies, Northrop Grumman continues to play a critical role in advancing integrated electronic systems for modern defense platforms.

-

In September 2025, Northrop Grumman progressed its intelligent defense systems initiatives by enhancing autonomous vetronics capabilities, enabling improved sensor integration, data processing, and mission support across next-generation combat vehicles.

Vetronics Market Key Players:

Some of the Vetronics Market Companies are:

-

Lockheed Martin

-

RTX Corporation (Raytheon Technologies)

-

Northrop Grumman

-

General Dynamics

-

BAE Systems

-

Thales Group

-

Leonardo S.p.A.

-

Rheinmetall

-

Elbit Systems

-

Saab AB

-

L3Harris Technologies

-

Honeywell

-

Leonardo DRS

-

Kongsberg Gruppen

-

Oshkosh Corporation

-

Curtiss-Wright Corporation

-

Moog Inc.

-

Collins Aerospace

-

Hensoldt

-

Indra Sistemas

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.28 Billion |

| Market Size by 2035 | USD 9.10 Billion |

| CAGR | CAGR of 5.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By System / Component Type (Command & Control Systems, Communication Systems, Navigation & Positioning Systems, Power Management Systems, Display & Interface Systems, Others) • By Platform (Vehicle Type) (Armored Vehicles, Main Battle Tanks (MBTs), Infantry Fighting Vehicles (IFVs), Light Protected Vehicles, Unmanned Ground Vehicles (UGVs), Combat Support Vehicles, Others) • By Technology (AI-enabled Vetronics Systems, Digital Vetronics Systems, Analog Vetronics Systems, Hybrid Vetronics Architectures, Network-centric Systems, Open / Modular Architecture Systems, Others) • By Application (Combat Operations, Surveillance & Reconnaissance, Command & Control, Navigation & Targeting, Situational Awareness, Others) • By End User (Defense Forces (Army, Marines, etc.), Homeland Security Agencies, OEMs (Original Equipment Manufacturers), Defense Contractors / Integrators, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin, Raytheon Technologies, Northrop Grumman, General Dynamics, BAE Systems, Thales Group, Leonardo S.p.A., Rheinmetall, Elbit Systems, Saab AB, L3Harris Technologies, Honeywell, Leonardo DRS, Kongsberg Gruppen, Oshkosh Corporation, Curtiss-Wright Corporation, Moog Inc., Collins Aerospace, Hensoldt, Indra Sistemas |

Frequently Asked Questions

North America dominated with a 36.35% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 7.30% during 2026–2035.

Combat Operations systems dominated with a 28.12% share in 2025, while Surveillance & Reconnaissance systems are projected to grow at the fastest CAGR of 6.50% during 2026–2035

Growth is driven by increasing defense modernization programs, rising demand for integrated battlefield electronics, and sensor systems, expansion of armored vehicle fleets, and the need for enhanced situational awareness and real-time data processing.

The market is valued at USD 5.28 Billion in 2025 and is projected to reach USD 9.10 Billion by 2035.

The Vetronics Market is projected to grow at a CAGR of 5.72% during 2026–2035.

Get in Touch