Vitreous Tamponade Market Report Scope & Overview:

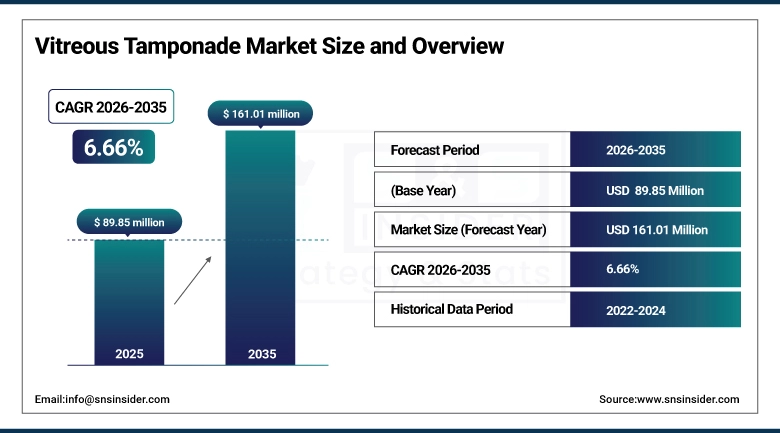

The Vitreous Tamponade Market was valued at USD 89.85 Million in 2025 and is expected to reach USD 161.01 Million by 2035, growing at a CAGR of 6.66% from 2026-2035.

The Vitreous Tamponade (MIS) Market is witnessing strong growth due to an increasing patient inclination towards surgeries that cause minimal trauma, shorter hospitalizations, and quicker recovery times. Innovations in technology such as robot-assisted surgeries, HD imaging, AI-powered surgery systems, and laparoscopic instruments have made significant progress within orthopaedic, gynaecological, urological, cardiac, and neurological practices.

Supporting this trend, the U.S. Centers for Disease Control and Prevention (CDC) reported 919,032 cardiovascular-related deaths in 2023 with someone dying every 34 seconds and the American Cancer Society projected approximately 2,041,910 new cancer cases in the U.S. alone in 2025.

In addition, the U.S. Food and Drug Administration (FDA) has been actively expanding regulatory pathways for advanced MIS technologies. In February 2024, FDA authorized Virtual Incision's MIRA Surgical System through the De Novo pathway, becoming the first miniaturized robotic-assisted surgery device cleared for colectomy procedures in adult patients exemplifying the agency's commitment to enabling next-generation minimally invasive solutions.

Vitreous Tamponade Market Size and Forecast

-

Market Size in 2025: USD 89.85 Million

-

Market Size by 2035: USD 169.01 Million

-

CAGR: 6.66% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Vitreous Tamponade Market - Request Free Sample Report

Vitreous Tamponade Market Trends

-

Increasing adoption of minimally invasive vitrectomy procedures (MIVS) is driving higher utilization of advanced vitreous tamponade agents across retinal surgeries.

-

Rising prevalence of diabetic retinopathy, retinal detachment, and macular disorders is significantly expanding the patient pool requiring tamponade-assisted interventions.

-

Growing shift toward short-acting gas tamponades (SF6, C3F8) is improving post-operative recovery times and reducing the need for secondary removal procedures.

-

Advancements in heavy silicone oils and semi-fluorinated compounds are enhancing retinal stabilization in complex and recurrent detachment cases.

-

Increasing preference for outpatient and ambulatory surgical settings (ASCs) is accelerating demand for efficient, fast-recovery tamponade solutions.

-

Integration of advanced vitrectomy systems and high-resolution visualization technologies is improving surgical precision and tamponade effectiveness.

-

Rising focus on biocompatibility and reduced complication rates (e.g., lower IOP, cataract risk) is driving innovation in next-generation tamponade materials.

-

Expanding research in drug-eluting and multifunctional tamponade agents is enabling combined therapeutic and structural retinal support solutions.

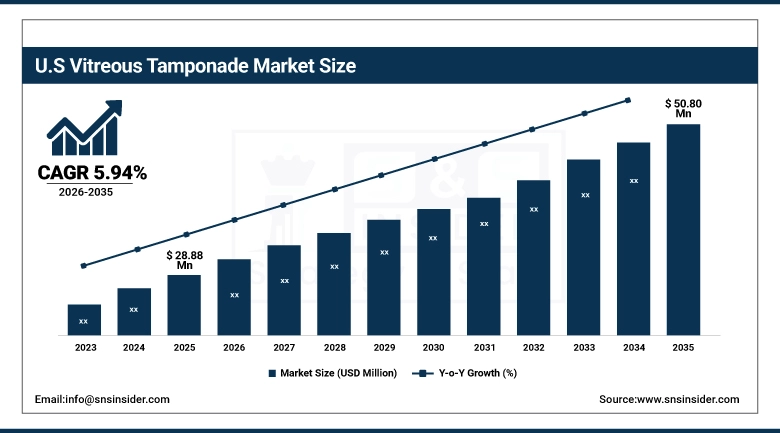

U.S. Vitreous Tamponade Market was valued at USD 28.88 million in 2025 and is expected to reach USD 50.80 million by 2035, growing at a CAGR of 5.94 from 2026–2035.

The United States Vitreous Tamponade Market is the largest globally and is driven by high levels of investment in ophthalmic surgery equipment, favorable reimbursement policies, and market leaders like Alcon, Bausch & Lomb, and Johnson & Johnson Vision. The increasing adoption of minimal invasiveness in vitrectomy procedures is boosting its growth.

Leading players such as Alcon and Bausch + Lomb are advancing next-generation silicone oils and gas tamponades with improved biocompatibility and longer retinal support duration.

Additionally, ongoing clinical studies on heavy silicone oils and combination tamponade therapies are enhancing surgical outcomes and reducing complication rates in complex retinal cases.

Vitreous Tamponade Market Segment Highlights

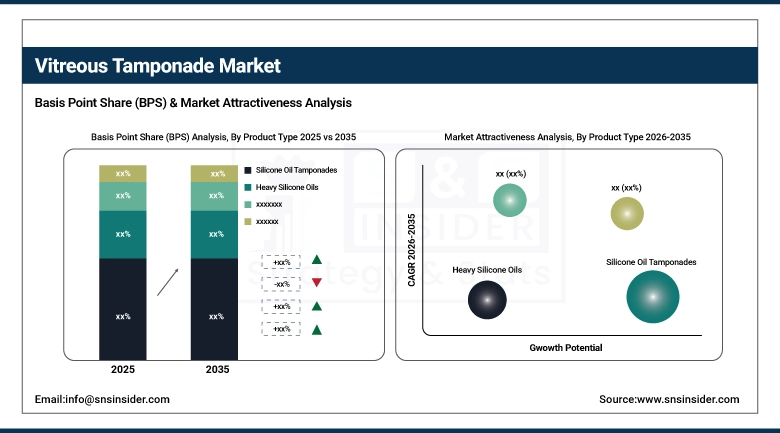

• By Product Type, Silicone Oil Tamponades dominated the Vitreous Tamponade Market with 52.36% share in 2025; Gas Tamponades (SF6, C3F8, Air) fastest growing Cagr

• By Application, Retinal Detachment dominated the Vitreous Tamponade Market with 48.45% share in 2025; Diabetic Retinopathy fastest growing CAGR

• By End User, Hospitals dominated the Vitreous Tamponade Market with 54.85% share in 2025; Ambulatory Surgical Centers (ASCs) fastest growing CAGR

• By Distribution Channel, Direct Sales dominated the Vitreous Tamponade Market with 50.24% share in 2025; Online Sales fastest growing CAGR

Vitreous Tamponade Market Segment Analysis

By Product Type, Silicone Oil Tamponades segment dominates the Vitreous Tamponade Market, Gas Tamponades segment expected to grow fastest

In 2025, the Silicone Oil Tamponades segment maintained its dominant position in the Vitreous Tamponade Market, accounting for 52.36% of total revenue. This segment includes standard silicone oils and long-term tamponade agents widely used in complex retinal detachment surgeries, proliferative vitreoretinopathy (PVR), and cases requiring extended intraocular support.

From 2026 to 2035, the Gas Tamponades segment encompassing SF6, C3F8, and air-based tamponades is projected to record the highest CAGR. The increasing preference for short-acting tamponade agents that naturally absorb within the eye is significantly improving patient convenience by eliminating the need for secondary removal procedures.

By Application, Retinal Detachment segment dominates the Vitreous Tamponade Market, Diabetic Retinopathy segment expected to grow fastest

The Retinal Detachment segment held the largest application share of 48.45% in the Vitreous Tamponade Market in 2025, driven by the high incidence of rhegmatogenous retinal detachment and the critical role of tamponade agents in achieving successful retinal reattachment. Vitreoretinal surgeries for detachment cases routinely require tamponade support to maintain retinal positioning during healing, making this segment the primary revenue contributor.

The Diabetic Retinopathy segment is expected to register the highest CAGR during the 2026–2035 forecast period. The growing number of cases of diabetes around the world, especially in developing countries, will result in an increase in the number of people who suffer from complications in their eyes caused by diabetes.

By End User, Hospitals segment dominates the Vitreous Tamponade Market, Ambulatory Surgical Centers segment expected to grow fastest

The Hospitals segment maintained the highest end-user share of 54.85% in the Vitreous Tamponade Market in 2025. Hospital settings provide the major platform for conducting complicated vitreoretinal surgery that necessitates advanced surgery facilities along with advanced vitrectomy units. The presence of experienced retinal surgeons, advanced imaging facilities, and capability to handle complicated cases ensures the dominance of hospitals.

The Ambulatory Surgical Centers (ASCs) segment is projected to achieve the highest growth rate during 2026–2035.

By Distribution Channel, Direct Sales segment dominates the Vitreous Tamponade Market, Online Sales segment expected to grow fastest

The Direct Sales segment maintained the highest share of approximately 50.24% in the Vitreous Tamponade Market in 2025. Direct distribution channels continue to be the most suitable method for hospitals and eye clinics, considering that vitreoretinal surgeries need a reliable source of high-quality products, compliance with regulatory requirements, and prompt availability of tamponades. Notable suppliers like Alcon, Bausch + Lomb, and Johnson & Johnson Vision utilize their direct distribution channels extensively to foster good working relationships with surgeons and medical facilities.

The Online Sales segment is projected to achieve the highest growth rate during 2026–2035.

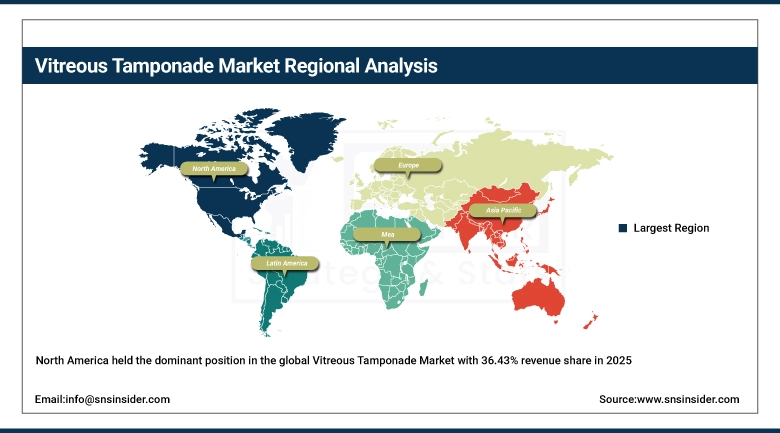

Vitreous Tamponade Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

36.43% |

|

Europe |

Germany |

29.14% |

|

Asia Pacific |

China |

25.75% |

|

Middle East & Africa |

UAE |

4.04% |

|

Latin America |

Brazil |

4.64% |

North America Vitreous Tamponade Market Insights

North America held the dominant position in the global Vitreous Tamponade Market with 36.43% revenue share in 2025, fueled by modern ophthalmic surgery capabilities, a higher number of vitreoretinal specialists, and higher usage of minimally invasive vitrectomy surgeries. The leading region in this category is the United States, owing to its intra-regional market share, which is facilitated by high procedure numbers for retinal detachment and diabetic retinopathy and the presence of specialized eye care centers.

Supporting this dominance, the Centers for Medicare & Medicaid Services (CMS) continues to provide favorable reimbursement coverage for outpatient ophthalmic procedures, including vitrectomy surgeries, encouraging adoption across ambulatory surgical centers and hospitals.

According to the American Academy of Ophthalmology (AAO), the U.S. performs hundreds of thousands of vitrectomy procedures annually, reflecting strong demand for tamponade agents in retinal repair.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Vitreous Tamponade Market Insights

The Asia Pacific region is anticipated to register the highest CAGR of 7.62% over the forecast period of 2026–2035, driven by rapidly expanding healthcare infrastructure, a large diabetic population, and increasing access to ophthalmic care. China, India, Japan, and South Korea represent key growth markets, with China accounting for regional revenue due to its large patient base and growing number of retinal surgery centers.

The region’s growth is strongly supported by rising awareness of preventable blindness and increasing government initiatives focused on early diagnosis and treatment of retinal disorders.

Supporting this trend, China’s National Health Commission (NHC) has prioritized ophthalmic disease management under national healthcare programs, while India’s National Programme for Control of Blindness and Visual Impairment (NPCBVI) continues to expand retinal care services across public hospitals. Increasing investments in private eye care chains and the rapid expansion of ambulatory ophthalmic centers are further accelerating demand for vitreous tamponade products across Asia Pacific.

Europe Vitreous Tamponade Market Insights

Europe accounted for of global revenue share in 2025, positioning it as the second-largest market. Growth is supported by well-established ophthalmology infrastructure, high adoption of advanced vitreoretinal surgical techniques, and strong regulatory oversight ensuring product safety and efficacy. Countries such as Germany, the United Kingdom, France, and Italy lead regional adoption due to the presence of specialized retinal centers and experienced surgical professionals.

Supporting this position, the European Commission continues to fund ophthalmology-related research under its healthcare innovation programs, including advancements in retinal disease treatment and surgical technologies.

Additionally, the implementation of the EU Medical Device Regulation (MDR 2017/745) has strengthened quality standards for ophthalmic products, including silicone oils and tamponade agents, enhancing clinical confidence and adoption. Increasing focus on aging population care and rising incidence of retinal diseases are further sustaining market growth across Europe.

Middle East & Africa and Latin America Vitreous Tamponade Market Insights

The MEA region and Latin America market are showing continuous growth within the market of vitreous tamponade, owing to improved healthcare infrastructures, growing awareness about retinal conditions, and increasing scope of eye clinics. Within the MEA region, key nations like Saudi Arabia, UAE, and South Africa have been at the forefront of adopting this technology due to ongoing healthcare transformation programs and investments in advanced facilities for surgery.

Supporting this development, Saudi Arabia’s Vision 2030 healthcare transformation program emphasizes expansion of specialized care services, including ophthalmology and retinal surgery capabilities.

In Latin America, Brazil and Mexico are key markets, with growth supported by expanding access to eye care services and rising prevalence of diabetes-related eye conditions. Regulatory bodies such as ANVISA (Brazil) are streamlining approval pathways for ophthalmic products, enabling faster adoption of advanced tamponade agents.

Vitreous Tamponade Market Growth Drivers:

-

Rising global burden of retinal disorders and diabetes-driven eye diseases driving demand for vitreoretinal surgeries and tamponade agents

The rise in the number of cases of retinal diseases like retinal detachment, diabetic retinopathy, macular holes, and vitreous hemorrhage is one of the key drivers behind the growth of the market for Vitreous Tamponades. With increased awareness about eye health among patients and improved access to ophthalmic treatments, early surgery is becoming the preferred choice in order to avoid permanent damage to vision. The use of vitreous tamponades during surgery is crucial for the stabilization of the retina.

Supporting this trend, the American Academy of Ophthalmology reports a continuous rise in vitreoretinal procedures globally, particularly for retinal detachment and diabetic eye diseases, with vitrectomy becoming a standard of care across major ophthalmic centers.

The World Health Organization estimates that over 2.2 Million people globally suffer from vision impairment or blindness, with a significant proportion linked to preventable or treatable retinal conditions, highlighting the expanding need for surgical interventions utilizing tamponade agents.

Vitreous Tamponade Market Restraints:

-

Post-operative complications and need for secondary procedures associated with vitreous tamponade agents creating clinical and patient management challenges

The drawbacks and complications associated with the use of vitreous tamponades pose a major constraint to the growth prospects within the industry, especially during complicated retinal surgeries where there is a need for continued intraocular presence. Silicone oil tamponades, which are known to work efficiently towards stabilizing retinas for a prolonged period, also need a follow-up surgery for their removal. Moreover, issues including high IOP, cataract development, silicone oil emulsification, and inflammation can also become an issue.

Vitreous Tamponade Market Opportunities:

-

Advancement of next-generation biocompatible and multifunctional vitreous tamponade agents creating new growth pathways for improved surgical outcomes and broader clinical applications

The upcoming stage of development of the Vitreous Tamponade Market is associated with the introduction of highly developed materials for tamponades that can overcome existing clinical barriers and enhance their potential. Advances in heavy silicone oil, semi-fluorinated substances, and innovative tamponades based on polymers contribute to more efficient retinal immobilization in complicated detachment cases, minimizing adverse effects like emulsification and increased intraocular pressure. In addition, studies in drug-delivery tamponades facilitate a new dimension in the combination of mechanical retinal stabilization with drug release, providing effective anti-inflammatory, anti-VEGF, and anti-proliferative treatment.

Recent Developments:

-

2026: Alcon Inc. advanced its vitreoretinal portfolio with continued global rollout of next-generation vitreous tamponade solutions and small-gauge vitrectomy systems, supporting improved retinal stabilization and expanding adoption across ambulatory surgical centers and high-volume eye hospitals.

-

2026: Bausch + Lomb Corporation strengthened its retinal surgery segment through ongoing clinical evaluations of advanced silicone oil formulations with enhanced biocompatibility, targeting reduced emulsification rates and improved long-term surgical outcomes in complex retinal detachment cases.

-

2025: Johnson & Johnson Vision expanded its ophthalmic surgery ecosystem with enhancements in vitrectomy platforms and integrated surgical workflows, indirectly supporting increased utilization of vitreous tamponade agents in minimally invasive retinal procedures.

-

2025: Carl Zeiss Meditec AG reported continued adoption of its advanced visualization and intraoperative imaging systems, improving surgical precision in vitreoretinal procedures and enabling more effective use of gas and silicone-based tamponades in complex cases.

Vitreous Tamponade Market Key Players

Some of the Vitreous Tamponade Market Companies

-

Alcon Inc.

-

Bausch + Lomb Corporation

-

Carl Zeiss Meditec AG

-

Dutch Ophthalmic Research Center (DORC)

-

Fluoron GmbH

-

Johnson & Johnson Vision

-

Beaver-Visitec International (BVI)

-

Santen Pharmaceutical Co. Ltd.

-

Aurolab

-

MedOne Surgical Inc.

-

AL.CHI.MI.A. S.r.l.

-

Vitreq B.V.

-

HOYA Corporation

-

Wacker Chemie AG

-

Dow Inc.

-

SilMag S.p.A.

-

PfW Silicone Oil Manufacturing GmbH

-

OCULUS Optikgeräte GmbH

-

CROMA-PHARMA GmbH

-

Insight Instruments Inc.

Vitreous Tamponade Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 89.85 Million |

| Market Size by 2035 | USD 169.01 Million |

| CAGR | CAGR of 6.66 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Gas Tamponades (SF6, C3F8, Air), Silicone Oil Tamponades, Heavy Silicone Oils, Semi-fluorinated Alkanes, Others) • By Application (Retinal Detachment, Macular Hole, Diabetic Retinopathy, Vitreous Hemorrhage, Others) • By End User (Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers (ASCs,Others) • By Distribution Channel (Direct Sales, Medical Distributors, Online Sales, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alcon Inc., Bausch + Lomb Corporation, Carl Zeiss Meditec AG, Dutch Ophthalmic Research Center (DORC), Fluoron GmbH, Johnson & Johnson Vision, Beaver-Visitec International (BVI), Santen Pharmaceutical Co. Ltd., Aurolab, MedOne Surgical Inc., AL.CHI.MI.A. S.r.l., Vitreq B.V., HOYA Corporation, Wacker Chemie AG, Dow Inc., SilMag S.p.A., PfW Silicone Oil Manufacturing GmbH, OCULUS Optikgeräte GmbH, CROMA-PHARMA GmbH, Insight Instruments Inc. |

Get in Touch