Aerospace And Defense Connectors Market Report Scope & Overview:

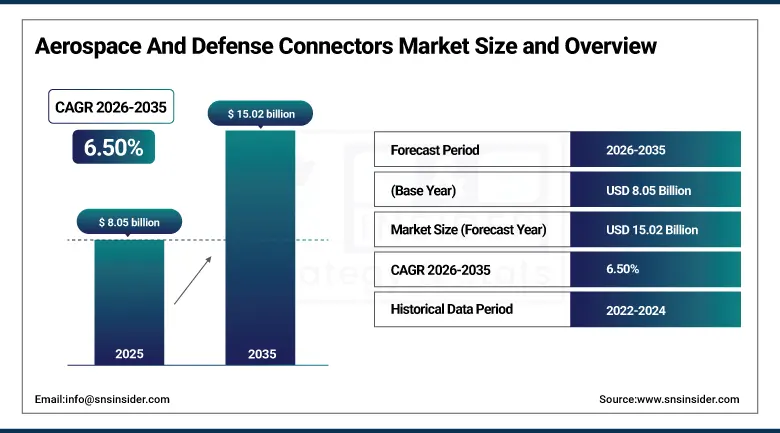

The Aerospace And Defense Connectors Market was valued at USD 8.05 billion in 2025 and is expected to reach USD 15.02 billion by 2035, growing at a CAGR of 6.50% from 2026-2035.

The Aerospace and Defense Connectors market is witnessing tremendous growth owing to the increase in demand for reliable, tough connectors which reduce system failure and help in performing missions reliably in harsh conditions. Innovations in fiber optic, hybrid, and high-speed data connector technology are enhancing the capabilities in military aircraft, civil aircraft, space, unmanned aerial vehicle/drones, naval, and defense platforms. Increasing defense modernization plans, commercial air fleet expansion, satellite launches, and unmanned system advancements are creating continuous demand.

Furthermore, the U.S. Department of Defense announced in late 2025 a new USD 9.5 billion defense modernization plan aimed at improving aircraft communication and avionics systems, thus increasing the demand for state-of-the-art aerospace connectors. Additionally, in January 2025, NASA embarked on its preparation phase for the Artemis IV mission, and thus, advanced fiber optic and hybrid connectors would be required for its space vehicles.

Aerospace And Defense Connectors Market Size and Forecast

-

Market Size in 2025: USD 8.05 Billion

-

Market Size by 2035: USD 15.02 Billion

-

CAGR: 6.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Aerospace And Defense Connectors Market - Request Free Sample Report

Aerospace And Defense Connectors Market Trends

-

Fiber optics are increasingly being used as connectors for fast data transfer in airplanes, satellites, and defense-related equipment.

-

Hybrid connectors are becoming popular because of their ability to integrate signal and power features into one package.

-

Connectors are experiencing increased demand due to their use in smaller aircraft and space vehicles.

-

Most connectors have to be ruggedized in order to survive harsh conditions like temperature and vibration.

-

Evolving modernization programs in the US, Europe, and Asia are stimulating the need for better connectors.

-

Growth in commercial aviation is driving demand for connectors in the next generation aircraft fleet.

-

Increased numbers of unmanned aerial vehicles will create new opportunities for connectors.

-

The emerging supply chain technologies using AM will help cut down production time and cost.

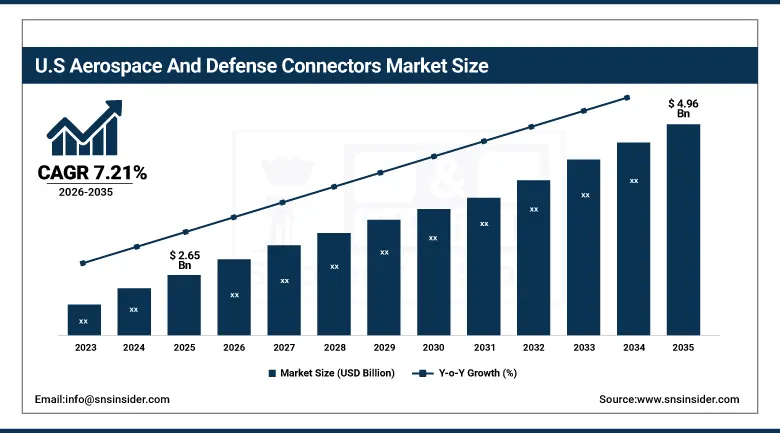

U.S. Aerospace And Defense Connectors Market was valued at USD 2.65 billion in 2025 and is expected to reach USD 4.96 billion by 2035, growing at a CAGR of 7.21% from 2026-2035.

The U.S. Aerospace and Defense Connectors Market is the largest globally, supported by a well-developed aerospace and defense industry infrastructure, substantial government investments, and presence of top technology companies like Amphenol, TE Connectivity, ITT Inc., Eaton, and Glenair. Positive initiatives by the DoD in the realm of modernization programs and expansion plans by NASA for space programs further boost the need for next-generation connectors used in aircraft, commercial airplanes, satellites, spacecrafts, and unmanned aerial vehicles (UAVs).

In line with this scenario, the U.S. Department of Defense (DoD) signed multi-billion-dollar contracts during 2024–2025 to upgrade avionics, radars, and communication equipment, which would fuel the need for advanced aerospace connectors. In December 2025, NASA expedited the planning phase of its Artemis IV program, necessitating the use of fiber-optic and hybrid connectors in spacecrafts.

Aerospace And Defense Connectors Market Segment Highlights

-

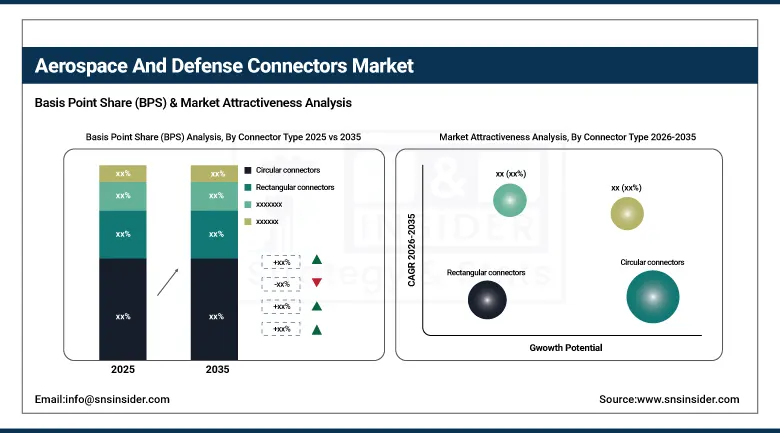

By Connector Type, Circular connectors dominated the Aerospace And Defense Connectors Market with 44.71% share in 2025; Fiber optic connectors fastest growing (CAGR).

-

By Application, Military aircraft dominated the Aerospace And Defense Connectors Market with 30.85% share in 2025; Space systems fastest growing (CAGR).

-

By Technology, High-speed data connectors dominated the Aerospace And Defense Connectors Market with 31.11% share in 2025; Hybrid connectors fastest growing (CAGR).

-

By End-Use Platform, Fixed-wing aircraft dominated the Aerospace And Defense Connectors Market with 34.56% share in 2025; Satellite & spacecraft systems fastest growing (CAGR).

Aerospace And Defense Connectors Market Segment Analysis

By Connector Type, Circular connectors segment dominates the Aerospace And Defense Connectors Market, Fiber optic connectors segment expected to grow fastest

Circular connectors emerged as the leading segment in the Aerospace & Defense Connectors Market, holding about 44.71% of total market share in 2025. This is mainly due to their widespread adoption in aerospace and defense sectors with harsh environmental conditions. They are commonly used in military aircraft, commercial avionics, spacecraft, and naval vessels, providing robust sealing capabilities, EMI shielding, and rugged performance.

The Fiber Optic Connectors segment is forecasted to grow at the highest CAGR between 2026 and 2035 in the Aerospace & Defense Connectors Market. The increasing requirement for high-speed data transmission, advanced avionics systems, and defense electronics has compelled the industry to shift towards fiber optics technology. The growing utilization of advanced radar systems, electronic warfare systems, satellite communication systems, and unmanned aerial vehicle (UAV)-based intelligence systems is driving the growth of this segment.

By Application, Military Aircraft segment dominates the Aerospace And Defense Connectors Market, Space Systems segment expected to grow fastest

The Military Aircraft category led the Aerospace & Defense Connectors Market in 2025, contributing about 30.85% to the market's overall revenue. The growth in the category can be attributed to widespread efforts towards the modernization of defense systems worldwide, growing investments in advanced fighter aircraft, and growing advancements in avionics, radar systems, electronic warfare systems, and communications systems.

The Space Systems category is predicted to witness the highest CAGR from 2026 to 2035. The growth will be driven by rapid advancements in satellite constellations, deep space expeditions, commercial space activities, and governmental space initiatives. The growing need for faster data transfer capabilities, low-weight interconnects, and radiation-resistant connectors will boost adoption.

By Technology, High-speed Data Connectors segment dominates the Aerospace And Defense Connectors Market, Hybrid Connectors segment expected to grow fastest

The High-speed Data Connectors category held the leading position in the Aerospace & Defense Connectors Market in 2025, accounting for about 31.11% of market share in terms of revenue. The major reason for its dominance was the increasing requirement for immediate processing of data in avionics, radar, mission computers, and defense communication systems.

During the forecast period from 2026 to 2035, the Hybrid Connectors category would exhibit the highest CAGR due to an increase in demand for multi-functional integration (signal, power, and data transfer). Hybrid connectors are ideal for advanced aircraft and defense platforms as they help decrease system weight, make wiring less complicated, and are efficient.

By End User, Fixed-Wing Aircraft segment dominates the Aerospace And Defense Connectors Market, Satellite & Spacecraft Systems segment expected to grow fastest

The Fixed-Wing Aircraft sector led the Aerospace & Defense Connectors Market in 2025, contributing around 34.56% toward the market’s overall revenues. Such dominance can be attributed to high-volume production of commercial aircrafts and military combat aircraft, alongside technological advancements in avionics, control systems, and in-flight networking infrastructure.

Between 2026 and 2035, the Satellite & Spacecraft Systems segment will exhibit the highest CAGR in terms of growth. These growth prospects are attributed to the growing popularity of commercial space exploration missions, internet through satellites, earth observation operations, and military surveillance missions. Rising use of compact, durable, and fast connectors in space technology applications is boosting growth prospects for space-grade connectors.

Aerospace And Defense Connectors Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40.47% |

|

Europe |

Germany |

25.56% |

|

Asia Pacific |

China |

24.76% |

|

Middle East & Africa |

UAE |

4.10% |

|

Latin America |

Brazil |

5.11% |

North America Aerospace And Defense Connectors Market Insights

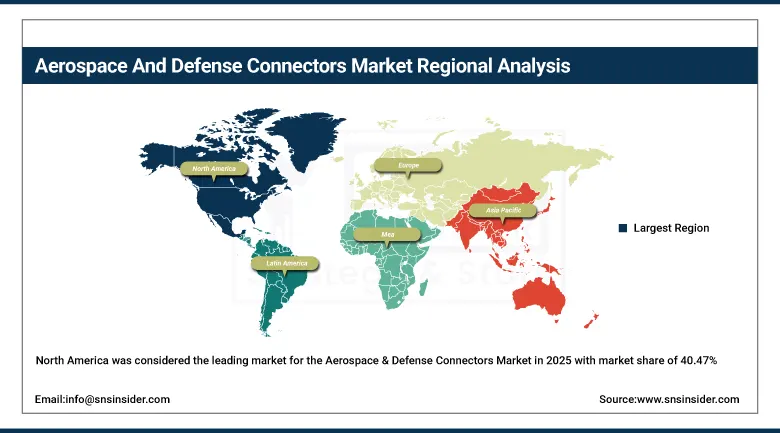

North America was considered the leading market for the Aerospace & Defense Connectors Market in 2025 with market share of 40.47%, due to its mature aerospace industry base and defense acquisition programs, along with the operations of leading OEMs and connector manufacturers. The United States is the key driver for regional growth due to widespread use in defense aviation, satellites, and advanced avionics applications. This market leadership is bolstered by ongoing efforts to update defense infrastructure, rapid developments in digital cockpits and mission systems, as well as active commercial aerospace manufacturing.

Additionally, further reinforcing this market dominance, the strength of North America as a region in terms of aerospace and defense connectors is based on robust government-sponsored defense modernization programs, next-generation fighter aircraft, and space and satellite projects. Acquisition agencies and defense ministries in North America continue to focus heavily on advanced avionics equipment, secure communications devices, and electronic warfare equipment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Aerospace And Defense Connectors Market Insights

The Asia Pacific region is expected to experience the highest CAGR from 2026 to 2035 with 7.76% CAGR, owing to fast growth in the aerospace manufacturing industry, modernization trends in defense systems, and increased expenditure on satellites and space exploration activities. There is a high demand for sophisticated aerospace & defense connectors in the region because of rising aircraft deliveries, indigenously developed defense systems, and accelerated deployment of UAVs and future avionics technology. Key countries like China, Japan, India, South Korea, and Australia are becoming potential hubs for growth, owing to the expansion in aerospace chains and localizing defense manufacturing operations.

In order to facilitate the above developments, China is developing its aerospace and defense sector through national strategic initiatives centered around advanced avionics, communication satellites, and locally produced aircraft systems, thereby leading to high adoption of superior connectors in both military and space segments.

Europe Aerospace And Defense Connectors Market Insights

Europe is among the top two revenue generators in the Global Aerospace & Defense Connectors Market due to its robust aerospace manufacturing industry, advanced defense procurement programs, and extensive use of modern aviation technologies. The region boasts leading manufacturers of aircraft and systems, along with a thriving environment for avionics, satellites, and advanced connector technology. Nations such as Germany, UK, France, and Italy are significant centers for aerospace research and development (R&D), defense electronics, and the creation of advanced aircraft, thus ensuring sustained demand for reliable connector systems.

To support this statement, it is important to note that the European Union is constantly working towards innovation in aerospace and defense industries through massive funding programs dedicated to developing advanced aviation, space technologies, and secure communication systems. Under European defense cooperation initiatives, there is accelerated growth in the production of modern military systems, unmanned aerial vehicles, and satellite systems.

Middle East & Africa and Latin America Aerospace And Defense Connectors Market Insights

The MEA and Latin American regions are showing steady incremental gains in the Aerospace & Defense Connectors Market, with rising trends in defense modernization, investments in aerospace infrastructure, and the development of local manufacturing capacity. In the MEA region, the UAE, Saudi Arabia, and South Africa have been the leading adopters of the technology, driven by large-scale defense purchases, the development of their air forces, and investments in satellite communications and unmanned aerial vehicles (UAVs). The Vision 2030 program in Saudi Arabia and the UAE’s national aerospace policies have propelled the deployment of innovative aircraft and cutting-edge defense systems, all of which will require reliable connector systems.

The growth drivers in Latin America include Brazil and Mexico. The former has made significant advances in its aerospace industry owing to robust aircraft manufacturing capacity and the deployment of advanced avionics and communication systems for civil and military applications.

Aerospace And Defense Connectors Market Growth Drivers:

-

Rising demand for high-reliability, lightweight, and high-speed interconnect solutions across advanced aerospace, defense, and space systems driving global adoption of aerospace & defense connectors

The transition of aerospace and defense system architecture from traditional mechanical and analog systems to extremely digitalized, electrified, and networked systems represent the key structural force impacting the Aerospace & Defense Connectors Market. Contemporary aviation equipment and military systems demand connectors that provide for high-speed data communication, power and data sharing, and reliable operations in harsh conditions such as vibrations, temperature changes, electromagnetic radiation, and radiations.

According to IATA, global aviation traffic and fleet modernization are continuously growing, promoting the adoption of advanced avionics and predictive maintenance systems in commercial aircraft.

Aerospace And Defense Connectors Market Restraints:

-

High development, qualification, and certification costs for aerospace-grade connectors limiting adoption among smaller suppliers and increasing overall system integration costs across the aerospace & defense value chain

There is one very important structural barrier that exists in the Aerospace & Defense Connectors industry, and that is the very high cost of capital and compliance when it comes to designing, testing, and certifying connectors for aerospace and defense uses. The connectors that are developed for aircrafts, spacecrafts, missiles, and naval vessels must meet the requirements set forth by MIL-SPEC and DO-160 and many more stringent aerospace specifications that involve testing for vibration, thermal shock, EMI susceptibility, corrosion, and overall reliability in harsh environments.

Aerospace And Defense Connectors Market Opportunities:

-

Rapid expansion of next-generation aerospace platforms, space exploration programs, and electrified defense systems creating strong growth opportunities for advanced connector technologies

There have been numerous openings in the Aerospace & Defense Connectors Market as a result of changes occurring in aerospace architecture to digital, electrified, and autonomous designs. The increasing use of next-generation aircraft, modern military fighter jets, UASs, and satellite networks have created a high demand for effective connectors that are able to transmit high-speed data efficiently. The shift to More Electric Aircraft (MEA) and avionics architecture is adding more urgency towards developing hybrid, optical, and high-density connectors.

Recent Developments:

-

2026: Amphenol Corporation enhanced its aerospace and defense interconnect solutions range by introducing the next-generation high-speed and fiber optic connector systems for applications in satellite constellations, sophisticated avionics and unmanned air vehicles. The company announced an increase in use of its ruggedized circular connectors and hybrid interconnect systems by the military in various aircraft upgrade and next-generation spacecraft programs.

-

2025: TE Connectivity continued enhancing its portfolio of aerospace connectors with advanced solutions for high-speed data, RF and hybrid connections, suitable for use in electrified aircraft systems and high-end defense electronics. The company reinforced its presence in aerospace and defense markets with expanding usage of its solutions in next-generation avionics cockpit and electronic warfare systems and space communications infrastructure.

-

2026: ITT Inc. added new ruggedized interconnects to their Cannon connector family of products that were specifically designed for use in demanding aerospace and defense environments. These included applications such as military planes, ships, and satellites. It is mentioned by the company that there is an increase in the number of high reliability connectors from the company used in next-generation defense avionics, missiles, and satellites owing to the increasing need for reliable and high performing signal and power distribution capabilities.

-

2025: Glenair Inc. enhanced its offering for aerospace and defense connectors by making improvements in the areas of micro-miniature, high-density, and EMI-shielded connectors. The company reported an increase in use of these connectors in UAV systems, space-grade applications, and military electronics systems.

Aerospace And Defense Connectors Market Key Players

Some of the Aerospace And Defense Connectors Market Companies

-

Amphenol Corporation

-

TE Connectivity

-

ITT Inc.

-

Glenair Inc.

-

Eaton Corporation

-

Smiths Group Plc

-

Fischer Connectors SA

-

Winchester Interconnect

-

Conesys Inc.

-

Omnetics Connector Corporation

-

Milnec Interconnect Systems

-

Weald Electronics Ltd

-

Turck Inc.

-

Ray Service a.s.

-

Rojone Pty Ltd

-

Allied Electronics Corporation (India)

-

Souriau-Sunbank (Esterline/Amphenol)

-

Molex (Koch Industries)

-

Radiall SA

-

Carlisle Interconnect Technologies

Aerospace And Defense Connectors Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.05 Billion |

| Market Size by 2035 | USD 15.02 Billion |

| CAGR | CAGR of 6.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Connector Type (Circular Connectors, Rectangular Connectors, Fiber Optic Connectors, RF & Coaxial Connectors, Others), • By Application (Military Aircraft, Commercial Aircraft, Space Systems, UAVs/Drones, Naval & Ground Defense Systems, Others), • By Technology (High-Speed Data Connectors, Power Connectors, Signal Connectors, Hybrid Connectors, Others), • By End-Use Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Missiles & Weapon Systems, Satellite & Spacecraft Systems, Unmanned Aerial Systems (UAS), Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amphenol Corporation, TE Connectivity, ITT Inc., Glenair Inc., Eaton Corporation, Smiths Group Plc, Fischer Connectors SA, Winchester Interconnect, Conesys Inc., Omnetics Connector Corporation, Milnec Interconnect Systems, Weald Electronics Ltd, Turck Inc., Ray Service a.s., Rojone Pty Ltd, Allied Electronics Corporation (India), Souriau-Sunbank (Esterline/Amphenol), Molex (Koch Industries), Radiall SA, Carlisle Interconnect Technologies. |

Frequently Asked Questions

North America dominated the Aerospace And Defense Connectors Market in 2025.

The High-speed data connectors segment dominated the Aerospace And Defense Connectors Market in 2025.

The major growth factor driving the Market is the rising demand for rugged, high‑reliability connectors, defense modernization programs, commercial aircraft fleets, space exploration and satellite launches and UAVs/drones.

The Aerospace And Defense Connectors Market was valued at USD 8.05 billion in 2025.

The Aerospace And Defense Connectors Market is expected to grow at a CAGR of 6.50% from 2026 to 2035.

Get in Touch