Aircraft Gearbox Market Report Scope & Overview:

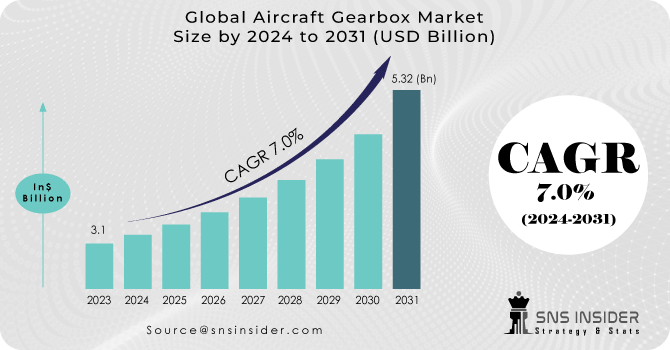

The Aircraft Gearbox Market Size was valued at USD 3.1 billion in 2023 and is expected to reach USD 5.32 billion by 2031 with a growing CAGR of 7.0% over the forecast period 2024-2031.

The gearbox is a transfer system used to change rotation speed. Many jet engines are equipped with accessory drive gearboxes that drive the required AC generators, electric pumps, oil pumps, and other accessories. If the engine has more than one compressor part, the gearbox is powered by single compressor drive shafts. The gearbox uses a lowering gear to reduce the shaft speed between the two engines. In turbofan, the fan-turned turbojet engine, part of the fan is much slower than half of the turbine. Therefore, the gearbox works to connect the shafts and reduce engine speed.

To get more information on KEYWORD Market - Request Free Sample Report

MARKET DYNAMICS

KEY DRIVERS

-

lightweight gearboxes

-

Pure Power Geared Turbofan motors

-

Strict government regulations.

RESTRAINTS

-

Using turboprop engines at high altitudes

-

Surveillance & intelligence gathering

-

High altitudes causes

OPPORTUNITIES

-

Increased R&D.

-

Two rows of propellers.

-

Fuel savings.

CHALLENGES

-

High cost

-

Major challenges

-

Significant investment in R&D.

THE IMPACT OF COVID-19

Aircraft gearbox companies are facing temporary operational problems due to supply problems and a shortage of entry points due to the COVID-19 outbreak.

COVID-19 has forced governments to suspend all integration and production activities, including the aviation industry.

The total closure of several countries due to COVID-19 has had a direct impact on security agencies delaying the purchase of aircraft gearboxes from aircraft carrier suppliers.

The COVID-19 epidemic puts a lot of pressure on aircraft gear companies by increasing the cost of airplane equipment.

The aviation industry has seen a sharp decline in flight hours as a large number of international and domestic flights are canceled globally to prevent the spread of COVID-19.

IMPACT OF UKRAINE AND RUSSIA CRISIS:

Russia's invasion of Ukraine and air traffic controls pose significant challenges to international airlines as hundreds of airlines flying in Russia's airspace now have to choose alternatives, leading to increased operating costs due to increased fuel burning. The sector is facing a crisis as ATF prices also rise due to rising green prices.

Airlines are considering the impact as the international aviation map could be reprinted due to the Russian invasion of Ukraine. Ukraine has been banned from flights since February 24 after Russia stepped up its military development in the country. Following the Moscow invasion of Ukraine, the European Union, Canada closed its airline on Russian flights. The US has also banned Russian flights from American airspace

KEY MARKET SEGMENTATION

By Application

-

Engine

-

Airframe

By Type

-

Accessory

-

Reduction

-

Tail Rotor

-

Auxiliary Power Unit

-

Others

By Component

-

Gear

-

Housing

-

Others

By platform

-

Civil

-

military

By End User

-

OEM

-

Aftermarket

-

By Platform

-

Civil

-

Military

Need any customization research on KEYWORD Market - Enquiry Now

REGIONAL ANALYSIS

The Aircraft gearbox market has been established in North America, Europe, Asia Pacific, and the rest of North America dominated the aircraft gearboxes market by 2023. speed, which dramatically increased demand for aircraft gears: The presence of key players, then GF Aerospace and Rexnord Corporations have been instrumental in boosting the growth of the North American aircraft gearbox market. The market in Europe is expected to grow slowly due to the presence of prominent CEM airlines such as Airbus SAS and Rolls Royce with technologies to enhance the market growth in the region. The market in the Asia Pacific region is expected to register the highest CAGR in the forecast period. Countries such as China and Japan are likely to continue to play a significant role in the region, while India, due to its rapid growth in the commercial aviation industry, is emerging as a fast-growing market. The Middle East has potential buyers such as Emirates, Qatar, Eshed and many other emerging airlines that are major players in making the global aviation gear market grow during the forecast period.

REGIONAL COVERAGE

North America

-

USA

-

Canada

-

Mexico

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

Asia-Pacific

-

Japan

-

South Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

KEY PLAYERS

The Major Players are Liebherr, Safran, Triumph Group, Northstar Aerospace, CEF Industries, LLC, AERO GEARBOX INTERNATIONAL, AERO GEAR, SKF, GE Aviation, United Technologies, Avion Corporation & Other Players

Safran-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 3.1 Billion |

| Market Size by 2031 | US$ 5.32 Billion |

| CAGR | CAGR of 7% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Application (Engine, Airframe) • by Type (Reduction, Accessory, Actuation, Tail Rotor, APU) • by End User (OEM, Aftermarket) • by Platform (Civil, Military) • by Component (Gears, Housing, Bearing) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Liebherr, Safran, Triumph Group, Northstar Aerospace, CEF Industries, LLC, AERO GEARBOX INTERNATIONAL, AERO GEAR, SKF, GE Aviation, United Technologies, Avion Corporation |

| Key Drivers | • lightweight gearboxes • Pure Power Geared Turbofan motors |

| RESTRAINTS | • Using turboprop engines at high altitudes • Surveillance & intelligence gathering |

Frequently Asked Questions

Yes, you will get an free sample of this report for that you have to make an contact with our team.

Aircraft Gearbox Market Size was valued at USD 3.1 billion in 2023, and expected to reach USD 5.32 billion by 2031, and grow at a CAGR of 7.0% over the forecast period 2024-2031.

The gear component segment is dominant the Aircraft Gearbox Market.

Investing more on geared turbofan engines and R&D in open-rotor engine configuration has been increased.

North America, Europe, Asia-Pacific, The Middle East & Africa, Latin America are major five region cover in this report.

Get in Touch