Blood Plasma Derivatives Market Report Scope & Overview:

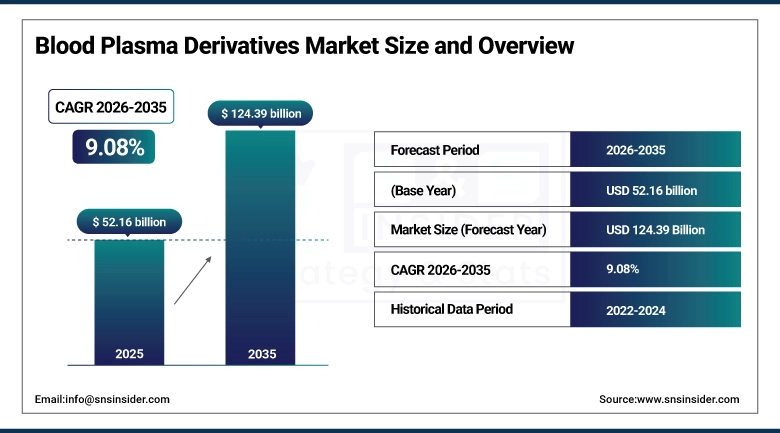

The Blood Plasma Derivatives Market Size is valued at USD 52.16 Billion in 2025 and is projected to reach USD 124.39 Billion by 2035, growing at a CAGR of 9.08% during the forecast period 2026–2035.

The Blood Plasma Derivatives Market analysis report offers an exhaustive coverage of the business along with artful contents to help industry players with reliable information. Increasing per capita healthcare expenditure, robust product pipeline and favorable reimbursement policy are the key factors that would trigger immense growth in commercial plasma market in the upcoming years.

Blood plasma derivatives demand reached 145 million liters in 2025, driven by rising immunoglobulin usage and growing plasma collection.

Blood Plasma Derivatives Market Size and Forecast:

-

Market Size in 2025: USD 52.16 Billion

-

Market Size by 2035: USD 124.39 Billion

-

CAGR: 9.08% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Blood Plasma Derivatives Market - Request Free Sample Report

Blood Plasma Derivatives Market Trends:

-

Growing interest in the use of immunoglobulins and albumin as treatments are shaping therapeutic strategies using plasma in healthcare ecosystems.

-

Supply capability is being enhanced with the further development of plasma collection networks and fractionation facilities.

-

Advancing trend of use of recombinant plasma products to increase safety and decrease risk of infection.

-

More broadly, biopharma company and research institute partnerships are driving innovation in plasma therapeutics.

-

Both government support and reimbursement policies are expanding access to plasma derived therapies.

-

Advances in cold chain logistics and automation are enhancing both quality and shelf life of blood derivatives.

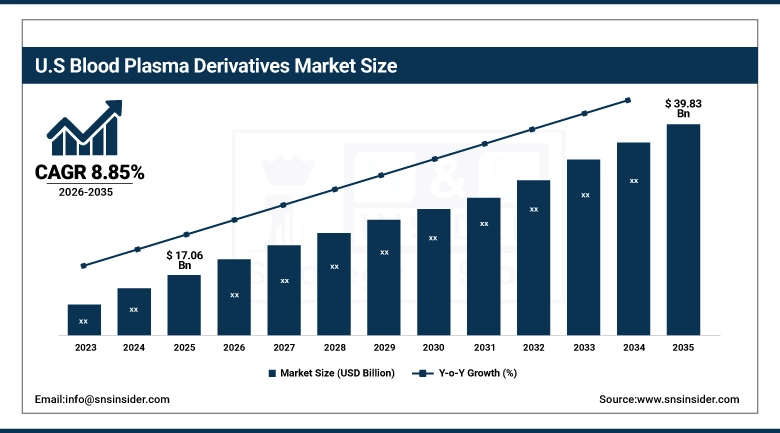

U.S. Blood Plasma Derivatives Market Insights:

The U.S. Blood Plasma Derivatives Market is projected to grow from USD 17.06 Billion in 2025 to USD 39.83 Billion by 2035, at a CAGR of 8.85%. The market is driven by the increasing adoption of plasma therapy, growing plasma collection infrastructure and strong demand for immunoglobulins in treatment immune and neurological diseases at large healthcare facilities.

Blood Plasma Derivatives Market Growth Drivers:

-

Growing prevalence of immune and neurological disorders driving higher demand for advanced plasma-derived therapeutic products.

Growing prevalence of immune and neurological disorders is a key driver of Blood Plasma Derivatives Market growth. Growing incidences of diseases, such as primary immunodeficiency, haemophilia and Guillain-Barré syndrome have resulted in greater consumption of plasma derived products. Innovations in diagnosis, care enhancement, and access to dedicated treatment centers are also driving faster product adoption, providing biopharmaceutical companies with opportunities to develop new therapeutic offerings that deliver value in patient care from a healthcare market perspective.

Blood plasma derivative sales grew 9.5% in 2025, driven by rising cases of immune disorders and increasing adoption of plasma-based therapies.

Blood Plasma Derivatives Market Restraints:

-

Limited plasma availability and high production costs are constraining the growth of the Blood Plasma Derivatives Market.

Limited plasma availability and high production costs remain key restraints for the Blood Plasma Derivatives Market. Dependence on donations of human plasma limits availability of raw materials, and also results in increased production costs due to complicated turn out processes and printmaking. Regulatory hurdles and high quality standards also delay product approval and market penetration. Taken together, these obstacles impede scale-up of production and inflate the cost of treatment and patient access in resource-poor settings such as developing countries.

Blood Plasma Derivatives Market Opportunities:

-

Rising investment in plasma collection infrastructure and recombinant technology presents opportunities for innovation and therapy expansion.

Rising investment in plasma collection infrastructure and recombinant technology presents a major opportunity for the Blood Plasma Derivatives Market. Rapid establishment of plasma donation facilities and high-end manufacturing technologies is benefiting supply of plasma and its processing speed. And finally, advances in recombinant alternatives improve product safety while mitigating infection risk and addressing supply limitations. Technology integration and scalability are key areas where companies can address the emerging needs and increase access in developing healthcare economies.

Recombinant plasma derivatives accounted for 22% of new product approvals in 2025, driven by rising investment in safer, scalable, and infection-free therapeutic solutions.

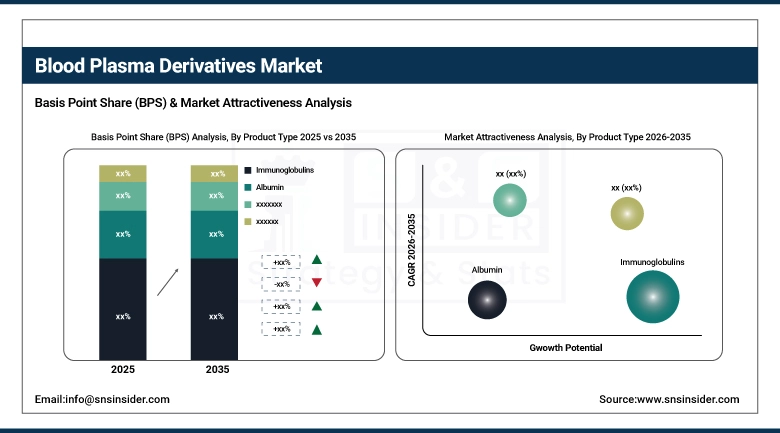

Blood Plasma Derivatives Market Segmentation Analysis:

-

By Product Type, Immunoglobulins held the largest market share of 41.28% in 2025, while Fibrinogen Concentrate is expected to grow at the fastest CAGR of 10.74% during 2026–2035.

-

By Source, Human Plasma dominated with a 67.85% share in 2025, while Recombinant is projected to expand at the fastest CAGR of 11.29% during the forecast period.

-

By Application, Immunology accounted for the highest market share of 38.62% in 2025, while Neurology is anticipated to record the fastest CAGR of 9.97% through 2026–2035.

-

By End User, Hospitals & Clinics held the largest share of 54.43% in 2025, while Research Institutes are expected to grow at the fastest CAGR of 8.86% during 2026–2035.

By Product Type, Immunoglobulins Dominate While Fibrinogen Concentrate Expands Rapidly:

Immunoglobulins segment dominated the market as they were widely being used to treat immune deficiencies, autoimmune diseases & infections. This segment’s lead is being reinforced by increasing realization in early adoption of immunotherapy and enhanced plasma fractionation capacity. Fibrinogen Concentrate is the fastest growing segment, medical indication is it can be used into trauma and surgical bleeding control. In 2025, more than 180 million vials of fibrinogen concentrate were supplied globally, marking strong clinical adoption.

By Source, Human Plasma Leads While Recombinant Advances Swiftly:

Human Plasma segment dominated the market as they have demonstrated safety and proven to be trustworthy in generating therapeutic proteins. An expanded network of plasma donation centres and better cold-chain have ensured supply reliability. Recombinant is the fastest growing segment by growth as it removes the risk of infection and reliance on human donors. Its production is also being accelerated by constant R&D and biotechnological developments. In 2025, around 320 recombinant plasma units were launched, reflecting rapid innovation.

By Application, Immunology Dominates While Neurology Emerges as the Fastest Growing Area:

Immunology segment dominated the market, supported by increasing incidence of immunodeficiency diseases and autoimmune disorders. The increasing access of intravenous immunoglobulins (IVIG) treatment and enhancement of diagnostic facilities add weight to this predominance. Neurology is the fastest growing segment and in neuropathy, plasma-derive day treatments have had increasing usage. Growing R&D in neuroimmunology further accelerates plasma therapy adoption. In 2025, 2.8 million neurological patients were treated with plasma-derived therapies, signaling strong therapeutic potential.

By End User, Hospitals & Clinics Dominate While Research Institutes Grow Significantly:

Hospitals & Clinics segment dominated the market, incorporating as the main centers for plasma therapy, with advanced diagnostic products and well-established patient care processes. Growing public funding of health date serves as a part of the success in this segment. Research Institutes are the fastest growing segment as clinical trials expand and academic joint ventures with biopharmaceutical corporations have multiplied. In 2025, over 950 research collaborations involving plasma derivatives were recorded, reflecting a surge in scientific exploration and innovation.

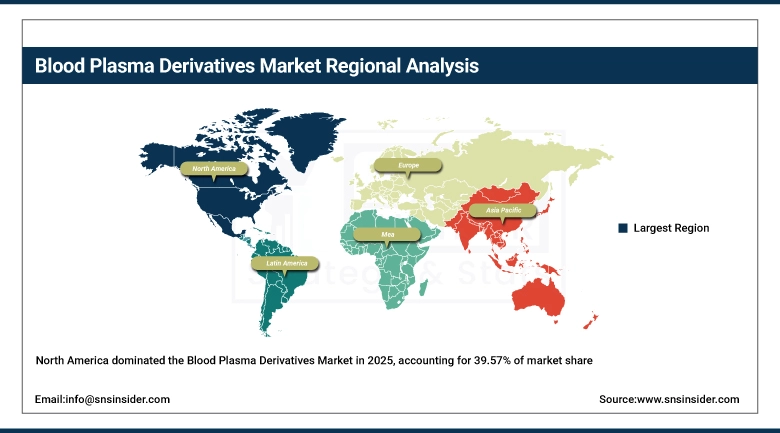

Blood Plasma Derivatives Market Regional Analysis:

North America Blood Plasma Derivatives Market Insights:

The North America dominated the Blood Plasma Derivatives Market with a 39.57% share, owing to investment in healthcare infrastructure and high plasma therapy utilization rate U.S and Canada. The market is continuously growing due to strengthening presence of major the biopharmaceutical companies, growing plasma collection networks and well laid reimbursement system. Rising incidence of immune and neurological diseases and constant R&D for plasma-based therapeutics are some others reasons that help North America maintain its lead status and continue to innovate in the landscape of Plasma derived products.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Blood Plasma Derivatives Market Insights:

The U.S. Blood Plasma Derivatives Market is dominated by developed healthcare infrastructure, high plasma donations, and the presence of major key players in biopharma industry. Increasing R&D funding, escalating application of immunoglobulins in treatment for chronic diseases, and advances in recombinant technology and plasma fractionation are driving demand growth for these drugs that offer improved safety, efficacy and access to treatment.

Asia-Pacific Blood Plasma Derivatives Market Insights:

The Asia-Pacific Blood Plasma Derivatives Market is the fastest-growing region, projected to expand at a CAGR of 10.89% during 2026–2035. Increased demand in China, Japan, India and South Korea for healthcare infrastructure and increased awareness toward plasma therapies (including IVIG) are the major factors that spur growth. APAC’s clinical and therapeutic potential flourishes backed by a fast-pacing investment on plasma collection centers, supportive government healthcare and local biopharmaceutical production capacity expansion.

China Blood Plasma Derivatives Market Insights:

China Blood Plasma Derivatives Market is driven by growing healthcare reforms, increasing adoption of plasma therapy, rising prevalence of immune diseases. The market trajectory of China is anticipated to rise due to high government investment in plasma collection centers, expansion of domestic biopharma production and increasing recombinant technology, making it a significant player in the Asia-Pacific landscape for plasma therapeutics.

Europe Blood Plasma Derivatives Market Insights:

Europe claims momentum in the Blood Plasma Derivatives Market due to their established healthcare system, treatment penetration and robust biopharmaceutical innovation throughout Germany, France, UK and Italy. Growing uses of Immunoglobulins and Coagulation Factors, robust R&D investment, and favorable regulatory context are fueling market growth. Europe’s established plasma collection networks and partnerships between public health authorities and private industry are continuing to build its position as a central hub for plasma therapeutics.

Germany Blood Plasma Derivatives Market Insights:

Germany is one of the significant markets in the Blood Plasma Derivatives sector due to high penetration levels and technological advancement in healthcare industry. Increasing use of immunoglobulin therapies, increasing number of plasma collection centers and constant R&D spending are boosting the market. Medical technology leadership and regulatory expertise in Germany solidify the country’s leadership position in Europe’s plasma therapeutics sector.

Latin America Blood Plasma Derivatives Market Insights:

The Latin America Blood Plasma Derivatives Industry continues to gain traction due to improved healthcare penetration, increasing awareness about plasma therapies and greater focus on the part of governments toward developing medical infrastructure. Growing plasma collection networks and biopharma production on a localised basis in Brazil, Mexico and Argentina and regional research partnerships are driving therapeutic access and market growth.

Middle East and Africa Blood Plasma Derivatives Market Insights:

The Middle East & Africa Blood Plasma Derivatives Market is increasing with the advancement in healthcare systems, increasing burden of chronic diseases and focus of government on advanced therapies. Rising spending on plasma collection, healthcare modernization and strategic collaborations with world leaders in biopharma industry are boosting the sector, with Saudi Arabia, UAE & South Africa leading the way.

Blood Plasma Derivatives Market Competitive Landscape:

CSL Limited, headquartered in Melbourne, Australia, is a biotechnology leader specializing in the development and manufacture of blood plasma-derived therapies and vaccines. The company accounts for a leading share in the Blood Plasma Derivatives Market with its broad offering of products such as immunoglobulins, albumin, and coagulation factors. Featuring leading-edge plasma collection facilities and research, CSL is committed to delivering high-quality, innovative and safe products. This, along with its extensive presence and ongoing reinvestment in medical innovation has led to the company's leadership position.

-

In April 2025, CSL unveiled its state-of-the-art plasma fractionation Facility F in Broadmeadows, Australia. Featuring full automation and robotics, the plant enhances plasma processing capacity to over 10 million litres annually, boosting CSL’s leadership in plasma-derived therapies and manufacturing excellence.

Takeda Pharmaceutical Company Limited, based in Tokyo, Japan, is one of the world’s largest biopharmaceutical firms with a strong heritage in plasma-derived therapies. Through the acquisition of Shire, Takeda has strengthened its position and capabilities in immunology and rare diseases. The company leads the market with highly innovative therapeutic solutions and patient focused innovation, including plasma collection, supported by massive BioLife network. Its attention to safety, and quality and expanding patient access has not only resulted in but never surpassed its corresponding market leading position.

-

In October 2025, Takeda launched HyHub and HyHub Duo devices in the U.S. for use with its plasma-derived immunoglobulin therapy HYQVIA. The devices simplify infusion preparation, reduce steps and ancillary supplies, and enhance patient mobility during treatment.

Grifols, S.A., headquartered in Barcelona, Spain, is a pioneer in plasma-derived medicines and diagnostic solutions. Levering off one of the world’s largest plasma collection network and a vertically integrated production capacity Grifols is among the major players in Blood Plasma Derivatives Market. Leadership is driven by the company’s innovative spirit, stringent quality measures and access to healthcare. Investments in R&D and sustainable sourcing of plasma continue to reinforce Grifols leadership in plasma therapies.

-

In October 2025, Grifols’ subsidiary Biotest AG launched Yimmugo, an innovative intravenous immunoglobulin therapy for primary immunodeficiencies in the U.S., marking a significant addition to its plasma-derived therapeutic portfolio.

Blood Plasma Derivatives Market Key Players:

-

CSL Limited

-

Takeda Pharmaceutical Company Limited

-

Grifols, S.A.

-

Baxter International Inc.

-

Octapharma AG

-

Kedrion S.p.A.

-

LFB Group

-

Biotest AG

-

China Biologic Products Holdings, Inc.

-

ADMA Biologics, Inc.

-

Green Cross Corporation

-

Fusion Health Care Pvt. Ltd.

-

SK Plasma Co., Ltd.

-

Bayer AG

-

Sanquin (Netherlands)

-

Hualan Biological Engineering Inc.

-

Intas Pharmaceuticals Ltd.

-

BDI Pharma

-

Shanghai RAAS Blood Products Co., Ltd.

-

Swedish Orphan Biovitrum AB

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 52.16 Billion |

| Market Size by 2035 | USD 124.39 Billion |

| CAGR | CAGR of 9.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Albumin, Immunoglobulins, Coagulation Factors, Protease Inhibitors, Fibrinogen Concentrate, Others) • By Source (Human Plasma, Recombinant) • By Application (Immunology, Hematology, Critical Care, Neurology, Others) • By End User (Hospitals & Clinics, Diagnostic Centers, Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CSL Limited, Takeda Pharmaceutical Company Limited, Grifols S.A., Baxter International Inc., Octapharma AG, Kedrion S.p.A., LFB Group, Biotest AG, China Biologic Products Holdings Inc., ADMA Biologics Inc., Green Cross Corporation, Fusion Health Care Pvt. Ltd., SK Plasma Co. Ltd., Bayer AG, Sanquin, Hualan Biological Engineering Inc., Intas Pharmaceuticals Ltd., BDI Pharma, Shanghai RAAS Blood Products Co. Ltd., Swedish Orphan Biovitrum AB |

Frequently Asked Questions

The blood plasma derivatives market is valued at USD 52.16 billion in 2025 and is expected to grow significantly over the forecast period.

The market is projected to reach USD 124.39 billion by 2035, reflecting strong long-term growth potential.

The market is anticipated to grow at a compound annual growth rate (CAGR) of 9.08% during 2026–2035.

Blood plasma derivatives are medicinal products derived from human plasma, including immunoglobulins, albumin, clotting factors, and protease inhibitors used to treat various diseases.

Key growth drivers include rising prevalence of chronic and rare diseases, increasing demand for immunoglobulins, and advancements in plasma fractionation technologies.

Get in Touch