Multi Camera System Market Report Scope & Overview:

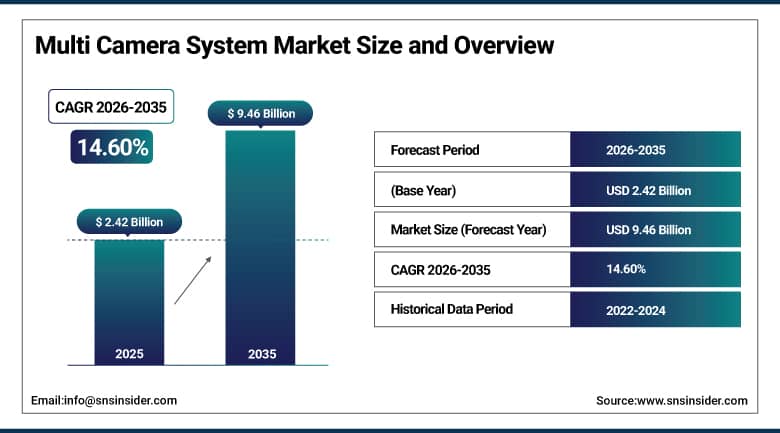

The Multi Camera System Market was valued at USD 2.42 Billion in 2025 and is expected to reach USD 9.46 Billion by 2035, growing at a CAGR of 14.60% from 2026 to 2035.

The fast-paced deployment of ADAS, along with increasing consumer preference towards improved safety features in automobiles and the accelerated development towards high-level automation in vehicles, have been contributing significantly to the rising adoption of multi-camera solutions. OEMs have started using multi-cameras in their automobiles to remove blind spots, provide assistance in parking as well as monitoring the driver in real-time, making multi-camera solutions a norm for automotive safety.

Magna International expanded its partnership with NVIDIA in 2026 to develop Drive Hyperion-compatible electronic control units integrating camera and sensor data for advanced autonomous driving systems, reflecting deepening collaboration between Tier 1 suppliers and semiconductor platform providers across the automotive perception technology landscape.

Market Size and Forecast:

-

Market Size in 2026E: USD 2.77 Billion

-

Market Size by 2035: USD 9.46 Billion

-

CAGR: 14.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Multi Camera System Market - Request Free Sample Report

Multi Camera System Market Trends:

-

Rising integration of camera-based driver monitoring systems is expanding beyond premium vehicles into mainstream passenger car segments.

-

Growing adoption of more than 4-camera architectures is enabling trailer, pillar, and interior views for Level 2+ autonomy features.

-

Advancements in edge AI chips are enabling on-vehicle compression and encryption of camera data before routing to cloud-based fleet analytics.

-

Software-enabled activation of dormant camera channels post-sale is creating new lifelong revenue opportunities for automakers and suppliers.

-

Expanding regulatory mandates around pedestrian safety and rear visibility are accelerating multi-camera adoption across mid-range vehicle segments.

U.S. Multi Camera System Market Outlook:

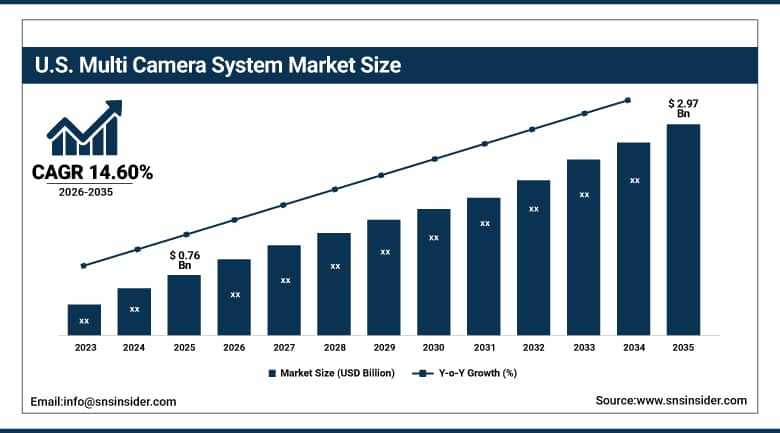

The U.S. Multi Camera System Market was valued at USD 0.76 Billion in 2025 and is projected to reach USD 2.97 Billion by 2035, growing at a CAGR of 14.60% during 2026-2035.

The continued focus of regulators on rear visibility and pedestrian safety, along with the huge consumer interest in safety-related technologies, keeps multi-camera systems in demand across the USA. American manufacturers and their counterparts from abroad keep collaborating with top-tier camera suppliers and semiconductor makers headquartered in the USA, which enables quick implementation of new generation perception solutions. The rising research and development investments of the world’s top automakers in self-driving technology is adding additional momentum to the trend.

Bosch signed a memorandum of understanding with Horizon Robotics in 2025 to jointly develop multipurpose cameras and mid-segment ADAS solutions, focusing on scalable, cost-efficient sensing platforms designed to broaden multi-camera system adoption across a wider range of vehicle price points in the United States and beyond.

Multi Camera System Market Segment Analysis:

-

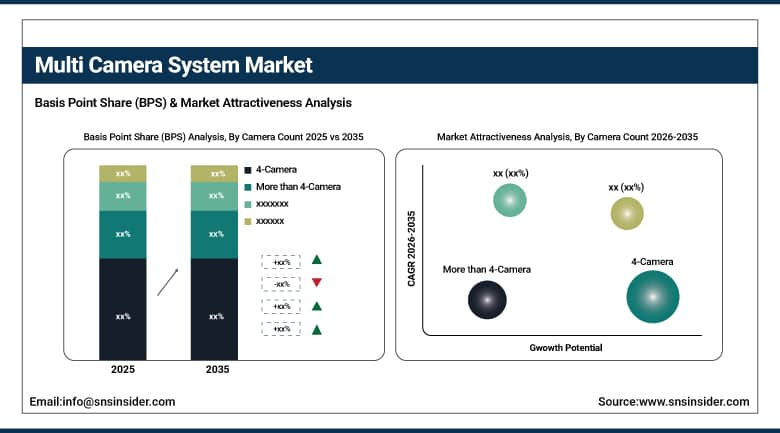

By Camera Count, 4-Camera led the Multi Camera System Market with a 65.27% share in 2025, while More than 4-Camera is the fastest-growing camera count segment with a CAGR of 19.20% from 2026-2035.

-

By Application, Surround-View/Park Assist led the Multi Camera System Market with a 46.80% share in 2025, while Driver Monitoring System is the fastest-growing application segment with a CAGR of 17.40% from 2026-2035.

-

By Vehicle Type, Passenger Vehicles led the Multi Camera System Market with a 73.90% share in 2025, while Commercial Vehicles is the fastest-growing vehicle type segment with a CAGR of 15.80% from 2026-2035.

-

By Sales Channel, OEM led the Multi Camera System Market with a 81.60% share in 2025, while Aftermarket is the fastest-growing sales channel segment with a CAGR of 13.90% from 2026-2035.

-

By Automation Level, Level 1/2 led the Multi Camera System Market with a 58.40% share in 2025, while Level 4 and Above is the fastest-growing automation level segment with a CAGR of 21.60% from 2026-2035.

By Camera Count, 4-Camera Dominated the Market While More Than 4-Camera Is the Fastest-Growing Segment

The 4-Camera category commanded the highest revenue market share of 65.27% in 2025 as the most cost-effective configuration for surround-view and parking assistance functions on the standard vehicle platform, which explains its dominance in the market as the right combination of safety performance and per-vehicle costs for these applications. The widespread regulatory requirement for rear-visibility in North America and Europe has made the 4-camera configuration as the bare minimum across the vast majority of the new vehicles being sold in these regions.

The 'More than 4-Camera' category is expected to grow at the highest CAGR of 19.20% from 2026-2035 on the back of growing adoption of cameras beyond just 4 on high-end, and now mid-level vehicles with the aim to enable Level 2+ autonomous driving functionalities. Software updates now enable automakers to activate additional dormant camera channels post-sale and improve their revenues without installing additional hardware in the future. The trend towards the 8-camera and possibly 12-camera configurations due to the growing need for full perimeter vision in urban delivery vans is likely to propel the growth in this category even further.

By Application, Surround-View/Park Assist Dominated the Market While Driver Monitoring System Is the Fastest-Growing Segment

The Surround-View/Park Assist segment was the top revenue generator in the Multi Camera System Market in 2025 with a market share of 46.80%. The success of the segment was fueled by its status as the first and most popular multi-camera system deployment for premium as well as mass-market vehicles. Surround-view systems use the input from various camera installations fitted to the vehicle to generate a live feed display in a bird's-eye view format, solving parking-related problems that are particularly resonant among consumers. The development of technology and decreasing prices are driving adoption of the segment in mid-market and entry-level cars.

The Driver Monitoring System segment is projected to show the highest CAGR of 17.40% during the 2026-2035 forecast period due to the increasing number of mandatory regulations requiring driver monitoring of attention in automotive industry leaders as well as the growing interest of car manufacturers in distracting and fatigued driving prevention measures. The usage of interior cameras combined with AI-based algorithms to analyze drivers' gaze and attention is increasingly bundled with other ADAS modules in order to ensure compliance with safety norms as well as insurance risks management policies.

By Vehicle Type, Passenger Vehicles Dominated the Market While Commercial Vehicles Is the Fastest-Growing Segment

Passenger Vehicles dominated the Multi Camera System Market in terms of revenue share at 73.90% in 2025 because of the huge volume of passenger vehicles manufactured globally and the increasing adoption of multi-camera safety technologies in both premium as well as mid-market segments of passenger vehicles. The need for consumer-friendly safety features, coupled with regulatory standards and third-party safety rating organizations, is driving automotive manufacturers to develop multi-camera technology as a standard feature rather than an add-on option.

Commercial Vehicles is projected to register the highest CAGR of 15.80% through the forecast period 2026-2035 on the back of increasing use of camera-based safety and telematics systems by fleet operators to lower their liability and insurance claims in case of accidents. Fleets of trucks and deliveries are using the multi-camera technology to avoid blind spots, monitor goods transported, and analyze the driving behavior of drivers. Growing deployment of delivery vehicles with the requirement of all-round visibility for automated deliveries is giving this segment an above average growth trajectory.

By Sales Channel, OEM Dominated the Market While Aftermarket Is the Fastest-Growing Segment

OEM segment accounted for the largest revenue share of 81.60% in the Multi Camera System Market in 2025, owing to the predominance of factory installed multi camera systems during original production of the vehicles over post-purchase integration. Increasing specification of multi-camera systems at the time of vehicle design to account for calibration, sensor fusion and other safety norms, is fueling preference towards OEM integration. Design collaboration between automobile manufacturers and Tier 1 suppliers remains an important factor reinforcing the dominance of the OEM channel in the Multi Camera System Market.

Aftermarket segment is projected to be the fastest-growing segment with a CAGR of 13.90% during the forecast period 2026-2035. Growing demand for upgrading safety technology in older cars through aftermarket multi camera systems among consumers and fleet operators, falling component prices and easy-to-install kits are driving growth in this segment. Awareness regarding benefits of camera-based safety solutions among operators of aging fleet of vehicles is another key factor that is boosting growth in this segment.

By Automation Level, Level 1/2 Dominated the Market While Level 4 and Above Is the Fastest-Growing Segment

The Level 1/2 segment led the Multi Camera System Market with a revenue share of 58.40% in 2025, reflecting the current predominance of driver-assistance rather than fully autonomous vehicle platforms across global new vehicle production. Most vehicles sold today rely on multi-camera systems to support driver-assistance functions such as lane departure warning, adaptive cruise control, and parking assistance rather than higher levels of vehicle autonomy. The segment's large installed base across mainstream vehicle production continues to anchor its position as the primary near-term demand driver for multi-camera system adoption worldwide.

The Level 4 and Above segment is expected to register the fastest CAGR of 21.60% during the forecast period 2026-2035, driven by accelerating investment from automotive and technology companies in developing and testing highly automated vehicle platforms. Regulatory support for autonomous vehicle trials, combined with the potential for meaningful safety and efficiency improvements in transportation, continues to attract substantial capital investment toward higher automation levels. Growing deployment of robotaxi and autonomous delivery fleets requiring extensive multi-camera perception coverage is further reinforcing this segment's rapid growth trajectory across the forecast period.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

88.40% |

|

Europe |

Germany |

26.30% |

|

Asia Pacific |

China |

43.70% |

|

Middle East & Africa |

UAE |

22.60% |

|

Latin America |

Brazil |

31.80% |

North America Multi Camera System Market Insights

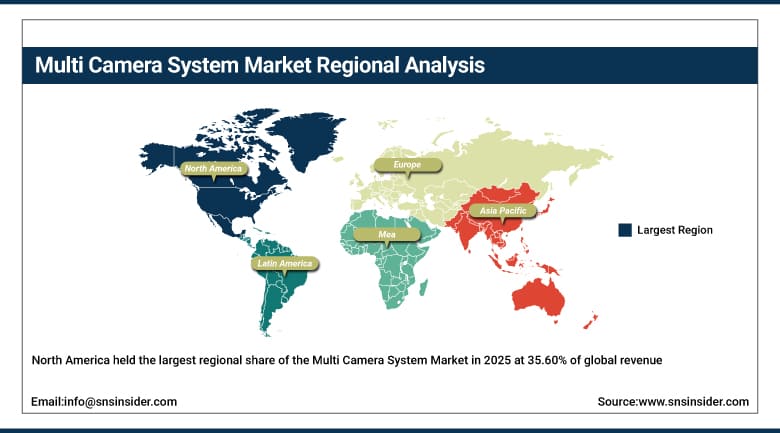

North America held the largest regional share of the Multi Camera System Market in 2025 at 35.60% of global revenue, anchored by strict rear-visibility and pedestrian safety regulations that have elevated multi-camera systems from luxury features to compliance essentials. The region's dense concentration of leading Tier 1 suppliers, semiconductor providers, and automotive technology developers continues to support rapid innovation and early adoption of next-generation perception technology. Strong consumer demand for advanced safety features, reinforced by independent vehicle safety rating programs, further sustains the region's leadership position across the broader market.

The United States accounted for approximately 88.40% of the North American market in 2025, reflecting its large vehicle production base, stringent federal safety regulation, and concentration of leading automotive technology and semiconductor companies. Canada is contributing to regional growth through steady vehicle production activity and growing consumer demand for advanced safety features aligned with U.S. regulatory standards and cross-border vehicle platform sharing.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Multi Camera System Market Insights

Europe was a significant contributor to the global Multi Camera System Market in 2025 due to the strict vehicle safety regulations of EU, high consumer demand for premium safety features, and the presence of major OEMs and Tier 1 providers of automotive industry based out of this region. The regulatory trend in favor of installing advanced driver assistance features in vehicles is driving demand for multi-camera systems in the region.

Germany dominated Europe multi camera system market with a regional market share of 26.30% in 2025 owing to the high production volume of premium vehicles in Germany and the presence of automotive suppliers in the country. France, UK, and Italy are among other contributors to growth in this market.

Asia Pacific Multi Camera System Market Insights

The Asia Pacific is expected to have the highest CAGR over the forecast period of 2026-2035 due to the rapid rise in vehicle production in China, India, and Southeast Asia coupled with increased domestic demand for safety features. Government-led vehicle safety programs and increased domestic manufacturing capabilities of semiconductors and camera modules are adding to the faster-than-the-rest growth potential of the region compared to other more developed regions such as North America and Europe.

China held around 43.70% of the Asia Pacific market share in 2025 owing to being the biggest manufacturer of vehicles globally and increasing adoption of advanced driver assistance systems domestically. Japan, South Korea, and India are also contributing significantly to the growth in the region, with Japan and South Korea maintaining their demand for the premium multi-camera systems while India derives benefits due to increasing vehicle production.

Middle East & Africa and Latin America Multi Camera System Market Insights

The Middle East & Africa and Latin America regions remain earlier-stage markets for multi-camera system adoption but are exhibiting steady growth as vehicle safety regulation expands and consumer demand for advanced features rises alongside growing disposable income. Middle Eastern nations in particular are seeing rising adoption of premium vehicles equipped with advanced multi-camera systems within their expanding luxury and commercial vehicle fleets.

The UAE led the Middle East & Africa market with a 22.60% regional share in 2025, supported by strong demand for premium vehicles and growing commercial fleet safety investment, while Saudi Arabia is separately expanding its vehicle safety regulatory framework. Brazil represented 31.80% of the Latin American market in 2025, driven by its large domestic vehicle production base and expanding safety regulation, with Mexico also contributing to regional growth through its export-oriented vehicle manufacturing sector.

Market Dynamics:

Growth Drivers: Rising ADAS Adoption and Autonomous Driving Investment Driving Market Growth

The Multi Camera System Market is being driven primarily by rapid integration of advanced driver assistance systems, expanding regulatory mandates around rear visibility and pedestrian safety, and accelerating automaker investment in autonomous driving research and development. Multi-camera systems have become a foundational technology for enhancing vehicle safety, enabling everything from lane departure warnings to surround-view parking assistance, and are increasingly viewed as essential rather than optional equipment across mainstream vehicle segments. Growing consumer awareness of camera-based safety benefits continues to reinforce automaker prioritization of multi-camera integration across new vehicle platforms globally.

Continued semiconductor cost declines and AI-driven image processing advancement are enabling higher-resolution, lower-cost camera modules capable of supporting increasingly sophisticated perception software across a widening range of vehicle price points. Growing deployment of robotaxi and autonomous delivery fleets requiring extensive multi-camera perception coverage is further expanding the addressable market beyond traditional passenger vehicles. Strategic partnerships between Tier 1 suppliers, semiconductor providers, and technology companies continue to accelerate the pace of innovation across the competitive landscape, sustaining rapid product development cycles.

Restraints: Calibration Complexity and Component Cost Volatility Limiting Market Expansion

In spite of the positive demand factors, the industry is constrained by a number of issues associated with the increasing challenges of multi-camera calibration and validation, and testing in real-world scenarios – a process which has become more costly for most manufacturers compared to the actual camera hardware cost itself. Maintaining sensor fusion accuracy in various lighting and environmental conditions poses a considerable challenge to engineers.

The cost variability of semiconductor components and periodic tariffs imposed on multi-camera module components have been a source of unpredictability in prices throughout the supply chain. The increasing fragmentation of regulations regarding autonomous vehicle testing and requirements for cameras in various countries also creates obstacles for global product development and certification for manufacturers operating in different regions.

Opportunities: Autonomous Driving Scaling and Software Monetization Creating New Growth Avenues

Substantial opportunity exists in the continued scaling of autonomous driving technology, where higher camera counts and more sophisticated sensor fusion architectures are essential prerequisites for achieving Level 4 and above automation. Suppliers that successfully develop cost-efficient, scalable multi-camera platforms stand to capture disproportionate share of this rapidly expanding application segment as automakers and technology companies accelerate autonomous vehicle deployment across both passenger and commercial fleet applications.

Growing adoption of software-enabled activation of dormant camera channels post-sale presents a further significant growth avenue, creating new lifelong revenue streams for automakers and suppliers beyond the initial vehicle sale. Expanding vehicle production and safety regulation across emerging markets in Asia Pacific and Latin America also represents meaningful untapped opportunity, as rising incomes and regulatory modernization create new demand for advanced multi-camera safety systems in previously underserved regional vehicle markets.

Recent Developments:

-

2026: Valeo inaugurated a new HD surround-view camera production line at its Sanand facility in Gujarat, India, strengthening localized manufacturing capabilities for next-generation automotive vision systems.

-

2026: Magna International expanded its partnership with NVIDIA to develop Drive Hyperion-compatible electronic control units integrating camera and sensor data for advanced autonomous driving systems.

-

2025: Bosch signed a memorandum of understanding with Horizon Robotics to jointly develop multipurpose cameras and mid-segment ADAS solutions for scalable, cost-efficient sensing platforms.

-

2026: Continental AG expanded its ProViu 360 surround-view camera platform with HD digital imaging, real-time bird's-eye visualization, and collision warning capabilities for commercial and off-highway vehicles.

Multi Camera System Market key players are:

-

Magna International Inc.

-

Robert Bosch GmbH

-

Continental AG

-

DENSO Corporation

-

Valeo SA

-

Aptiv PLC

-

ZF Friedrichshafen AG

-

LG Innotek Co., Ltd.

-

OmniVision Technologies, Inc.

-

Sony Semiconductor Solutions Corporation

-

onsemi

-

Ambarella, Inc.

-

NVIDIA Corporation

-

Panasonic Holdings Corporation

-

Hyundai Mobis Co., Ltd.

-

Gentex Corporation

Multi Camera System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.42 Billion |

| Market Size by 2035 | USD 9.46 Billion |

| CAGR | CAGR of 14.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Camera Count (4-Camera, More than 4-Camera) • by Application (Surround-View/Park Assist, ADAS, Driver Monitoring System, Blind Spot Detection) • by Vehicle Type (Passenger Vehicles, Commercial Vehicles) • by Sales Channel (OEM, Aftermarket) • by Automation Level (Level 1/2, Level 2+/3, Level 4 and Above) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Magna International Inc., Robert Bosch GmbH, Continental AG, DENSO Corporation, Valeo SA, Aptiv PLC, ZF Friedrichshafen AG, LG Innotek Co., Ltd., OmniVision Technologies, Inc., Sony Semiconductor Solutions Corporation, onsemi, Ambarella, Inc., NVIDIA Corporation, Panasonic Holdings Corporation, Hyundai Mobis Co., Ltd., Gentex Corporation |

Frequently Asked Questions

The Multi Camera System Market is expected to grow at a CAGR of 14.60% from 2026 to 2035.

The Multi Camera System Market was valued at USD 2.42 Billion in 2025.

The increasing demand for advanced driver assistance systems (ADAS), rising adoption of surveillance and security solutions, technological advancements in imaging and processing capabilities, and the growing need for enhanced situational awareness in various applications, including automotive, robotics, and smart cities.

The North America region dominated the Multi Camera System Market in 2025, accounting for approximately 35.60% market share.

The 4-Camera segment dominated the Multi Camera System Market in 2025, accounting for approximately 65.27% market share.

Get in Touch