Nucleic Acid Testing Market Report Scope & Overview:

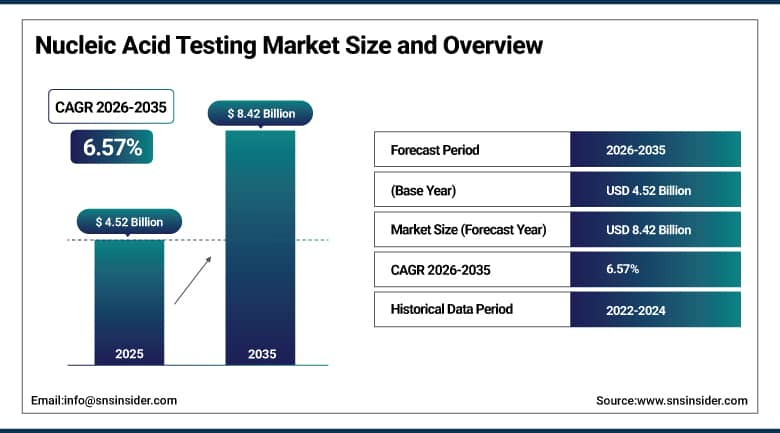

The Nucleic Acid Testing Market was valued at USD 4.52 billion in 2025 and is expected to reach USD 8.42 billion by 2035, growing at a CAGR of 6.57% during the forecast period of 2026-2035.

The nucleic acid testing market is experiencing robust growth on account of increasing cases of infectious diseases, growing adoption of precision medicine, expanding oncology diagnostics, and rising demand for rapid molecular testing techniques among other factors. Healthcare facilities are opting to incorporate molecular diagnostic tests based on nucleic acids due to the high levels of accuracy, sensitivity, and specificity associated with detecting biomarkers/pathogens at early stages. Advances in automation, multiplexing capacity, integration of next-generation sequencing techniques, and point-of-care technologies will continue propelling market growth in the coming years. Expanding blood screening programs, growing demand for companion diagnostics, and rising investments in personalized care also continue driving market growth.

In March 2025, Roche Diagnostics launched a new set of automated nucleic acid testing solutions to expand their molecular diagnostics suite to enhance infectious disease screening capacity. The launch of this product was a significant indicator of the increasing importance of developing molecular testing platforms in the industry.

Market Size and Forecast

-

Market Size 2026E: USD 4.75 Billion

-

Market Size 2035: USD 8.42 Billion

-

CAGR (2026 - 2035): 6.57%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Nucleic Acid Testing Market - Request Free Sample Report

Nucleic Acid Testing Market Trends

-

Rising adoption of multiplex testing platforms is improving diagnostic efficiency and multi-target detection.

-

Increasing laboratory automation is accelerating advanced nucleic acid testing deployment.

-

Rapid AI integration is enhancing diagnostic accuracy and faster result interpretation.

-

Growing demand for point-of-care molecular testing is expanding decentralized diagnostics.

-

Rising investments in precision medicine and oncology diagnostics are driving market growth.

-

Increasing adoption of next-generation sequencing is expanding testing applications.

-

Expanding use of portable molecular platforms is accelerating rapid diagnostic innovation.

The US Nucleic Acid Testing Market Size Outlook

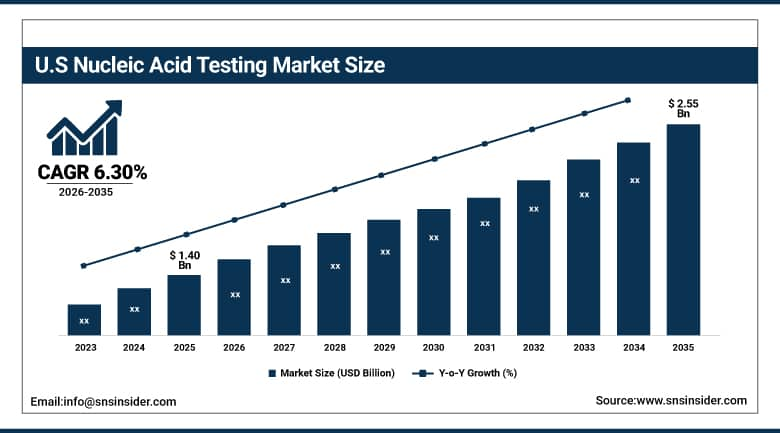

The U.S. nucleic acid testing market was valued at USD 1.40 billion in 2025 and is expected to reach around USD 2.55 billion by 2035, growing at a CAGR of 6.30% from 2026–2035.

The United States is one of the dominant countries in the global nucleic acid testing market due to the country’s supremacy as one of the leading molecular diagnostics ecosystems around the world, characterized by sophisticated healthcare infrastructure, high capacity for genomic research and presence of key players such as Roche Diagnostics, Thermo Fisher Scientific Inc., Abbott Laboratories, Danaher Corporation, and QIAGEN N.V. The United States has emerged as one of the dominant adopters of molecular tests in areas such as infectious diseases, oncology tests, blood testing, analysis of genetic diseases, and precision medicines. Continued high expenditure in healthcare, favorable reimbursement system, and adoption of advanced laboratory facilities have fueled the widespread implementation of nucleic acid testing solutions in the region.

For instance, in 2025, many molecular diagnostics firms increased their investments in automation technology and rapid multiplex tests to enhance their offerings in terms of infectious diseases and oncology testing. In addition, players within the industry increased their strategic alliances in relation to AI-powered molecular diagnostics and decentralized testing.

Segment Analysis

-

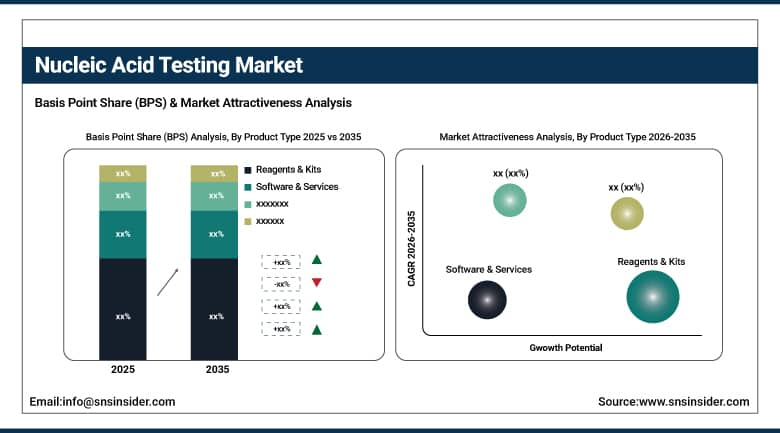

By Product Type, reagents & kits dominated the nucleic acid testing market with 46.69% share in 2025; software & services is the fastest-growing segment with the highest CAGR.

-

By Technology, polymerase chain reaction (PCR) & real-time PCR dominated the nucleic acid testing market with 42.54% share in 2025; sequencing-based testing is the fastest-growing segment with the highest CAGR.

-

By Application, infectious disease diagnostics dominated the nucleic acid testing market with 39.44% share in 2025; oncology testing is the fastest-growing segment with the highest CAGR.

-

By End User, hospitals & diagnostic Laboratories dominated the Nucleic Acid Testing Market with 43.59% share in 2025; pharmaceutical & biotechnology companies is the fastest-growing segment with the highest CAGR.

-

By Sample Type, blood samples dominated the nucleic acid testing market with 37.45% share in 2025; tissue samples is the fastest-growing segment with the highest CAGR.

By Product Type, reagents & kits dominates the nucleic acid testing market, while software & services is the fastest-growing segment.

Reagents & Kits segment emerged as a market leader with the dominant market share of 46.69% in 2025 due to consistent demands from usage, high volume of tests conducted, and increased demand for diagnostic consumables. The ongoing growth in infectious disease diagnostics and molecular diagnostics also adds to the market’s strength.

Software & Services segment is projected to register the fastest CAGR during the forecast period of 2026–2035.Due to increased laboratory digitization, workflow automation using AI, and increasing use of analytics software for analysis of molecular test results. Increasing demand for automated laboratory management systems is helping immensely in the growth of the segment.

By Technology, polymerase chain reaction (PCR) & real-time PCR dominates the nucleic acid testing market, while sequencing-based testing is the fastest-growing segment.

Polymerase Chain Reaction (PCR) & Real-Time PCR segment dominated the nucleic acid testing market with the highest revenue share of about 42.54% in 2025. This is due to the fact that it is highly sensitive, can produce results quickly, is clinically useful, and has been widely adopted for infectious disease detection, blood tests, and genetic analysis purposes. Excellent laboratory systems around the world have helped the technique of PCR remain extensively used.

Sequencing-Based Testing segment is estimated to register the highest CAGR during the forecast period of 2026–2035. As a result of increased adoption of precision medicine, oncology diagnostics, and use of genomics in clinical decision-making. Continued innovations and reductions in sequencing cost are leading to market expansion around the world.

By Application, infectious disease diagnostics dominates the nucleic acid testing market, while oncology testing is the fastest-growing segment.

Infectious Disease Diagnostics segment dominated the nucleic acid testing market with the highest revenue share of about 39.44% in 2025 because of the rising number of viral and bacterial infections globally, growing demands for rapid molecular testing technologies, and increased screening programs for public health care. Large test loads and requirements for early detection make the continued adoption of such solutions necessary.

Oncology Testing segment is expected to witness the highest CAGR during 2026–2035. Due to the increasing adoption of biomarker analysis, companion diagnostics, and precision medicine. Growing adoption of molecular profiling and personalized medicine is expected to drive segment growth.

By End User, hospitals & diagnostic laboratories dominate the nucleic acid testing market, while pharmaceutical & biotechnology companies is the fastest-growing segment.

Hospitals & Diagnostic Laboratories segment dominated the nucleic acid testing market with the highest revenue share of 43.59% in 2025. Due to the high number of tests conducted on patients, well-developed laboratories, and increased use of molecular diagnostic technologies. High demands for quick diagnosis remain a key factor supporting segment dominance.

Pharmaceutical & Biotechnology Companies segment is projected to experience the fastest CAGR during the forecast period of 2026–2035. Because of increased investment in drug development, biomarker discovery, genomics studies, and companion diagnostics initiatives. Increased use of molecular tests in therapy development is leading to rapid growth of the market.

By Sample Type, blood samples dominates the nucleic acid testing market, while tissue samples is the fastest-growing segment.

Blood Samples segment held the dominant revenue share of around 37.45% in 2025 due to its wide application in the diagnosis of infectious diseases, blood screening tests, oncology tests, and genotyping processes. Easy accessibility of blood, standard methods for collection, and wide usage have resulted in the increased acceptance of blood based nucleic acid testing techniques.

Tissue Samples segment is anticipated to grow at the fastest CAGR from 2026 to 2035. Because of increased use of biomarker analysis and molecular diagnostics, the market is expected to grow. The growing need for personalized medicine approaches as well as the increasing use of genomics in treating cancer is fueling the market growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

80.54% |

|

Europe |

Germany |

26.45% |

|

Asia Pacific |

China |

41.29% |

|

Middle East & Africa |

UAE |

21.56% |

|

Latin America |

Brazil |

36.79% |

North America Nucleic Acid Testing Market Insights

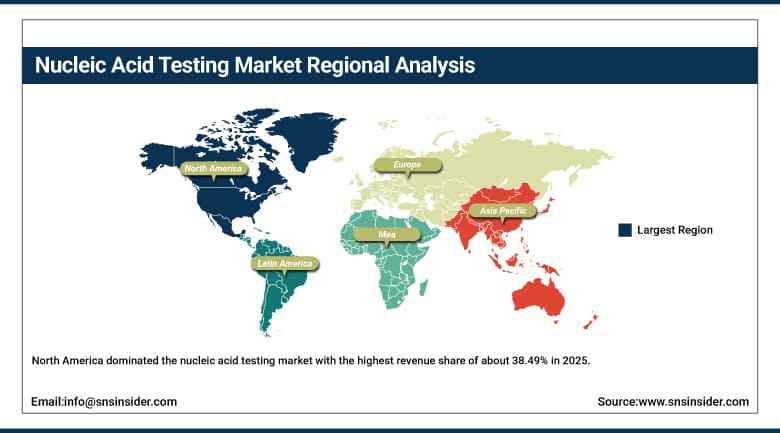

North America dominated the nucleic acid testing market with the highest revenue share of about 38.49% in 2025 owing to robust molecular diagnostics infrastructure, high healthcare spending, and wide acceptance of precision medicine technologies within the U.S. and Canada markets. High demand for tests used in diagnosing infectious diseases, cancer, blood screening, and genetic disorders has increased the use of cutting-edge nucleic acid testing equipment within hospitals, diagnostic centers, and other clinical laboratories. North America is also advantaged by the presence of leading molecular diagnostics manufacturers, favorable reimbursement policies, and growing automation of laboratory processes, which continues to bolster its market leadership.

Supporting this dominance, in 2025, multiple U.S.-based diagnostics companies accelerated investments in high-throughput molecular laboratory automation systems capable of processing large sample volumes with faster turnaround times. Furthermore, several healthcare organizations expanded implementation of AI-assisted molecular interpretation platforms to optimize assay analysis and improve workflow efficiency across large diagnostic networks.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Nucleic Acid Testing Market Insights

Europe is recognized as one of the most significant markets for nucleic acid testing because of the growing expenditure in diagnostic precision, genomics projects, and healthcare system modernizations. Countries like Germany, UK, France, and Italy continue to play major roles in the growth of this market due to their contribution to the expansion of cancer detection programs, surveillance in case of infectious diseases, and molecular diagnostic methods. Growing focus on individualized treatment of patients and early diagnosis of diseases continues to drive the demands in Europe. Several diagnostic partnerships within Europe have been working toward investments in genomic sequencing and biomarker discovery since 2025.

Asia Pacific Nucleic Acid Testing Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 24.45% during 2026–2035 as a result of fast development in healthcare facilities, increased cases of infectious diseases, and investment in molecular diagnostics in China, India, Japan, and Southeast Asian nations. Increased genomic research activities, health expenditures, and laboratory facilities have led to an increase in demand for nucleic acid test kits in the region. Development in the field of oncology diagnosis and precision medicine is also helping in creating opportunities for the market. To support growth in the market, some healthcare companies in Asia developed their molecular laboratories in the region.

Middle East & Africa and Latin America Nucleic Acid Testing Market Insights

Middle East & Africa (MEA) and Latin America regions are witnessing steady growth in the nucleic acid testing market owing to improvement in healthcare infrastructure, increased awareness about the early detection of diseases, and increased investments in molecular diagnostics technologies. In the MEA region, countries such as the UAE, Saudi Arabia, and South Africa are promoting its uptake with the help of healthcare modernization efforts and laboratory expansions, whereas Brazil and Mexico remain key contributors to growth in the Latin American region through the expansion of diagnostic access and disease surveillance. Facilitating this trend, healthcare facilities in the UAE and Saudi Arabia made significant investment in molecular laboratories and genomic healthcare projects.

Market Dynamics:

Growth Drivers: Rising demand for rapid molecular diagnostics and precision medicine adoption is accelerating expansion of nucleic acid testing technologies globally

The rising cases of infection-related illnesses, cancers, and genetic diseases have led to an increasing need for rapid and highly-sensitive diagnostics. The use of nucleic acid tests has become popular among healthcare professionals since these techniques are more effective than the older techniques in terms of detecting pathogens, offering accurate results, and diagnosing infections at an early stage. An increase in personalized medicine, including companion diagnostics, is another factor that has boosted the adoption of molecular diagnostics. Laboratory automation, multiplex testing technologies, and next-generation sequencing technologies are some of the innovations driving clinical applications of nucleic acid tests.

Restraints: High equipment costs and infrastructure requirements are limiting broader adoption of advanced nucleic acid testing platforms

The high upfront costs of molecular diagnostics devices, automation systems, and laboratory infrastructure remain among the biggest obstacles for the mass adoption of the technology in the marketplace. More sophisticated methods of nucleic acid testing typically involve specific equipment, trained technicians, quality control measures, and lab conditions, making the processes more complicated and expensive. Health care institutions in emerging markets often struggle with the problem of restrictions to payment and lack of molecular diagnostics equipment. Moreover, the issue of higher test expenses, inadequate lab space, and integration troubles may hinder further penetration of innovative technologies.

Opportunities: Expansion of decentralized diagnostics and AI-enabled molecular platforms is creating new opportunities across global healthcare markets

The development of innovative technologies in portable molecular devices, cartridges, and AI-enabled molecular diagnosis platforms creates considerable potential for expansion in the marketplace. The rising need for molecular diagnostic devices that provide fast results at the point of care, outside laboratories, is expanding their usage in the areas of emergency treatment, remote medicine, and infectious disease testing. The use of AI in molecular analysis systems increases efficiency in diagnostics. Investments in genomic medicine projects, laboratory decentralization projects, and overall healthcare infrastructure improvements in developing countries present additional opportunities for manufacturers of nucleic acid testing technologies.

Recent Developments

-

2026: Thermo Fisher Scientific Inc. expanded its molecular diagnostics capabilities through enhanced automated nucleic acid testing workflows and high-throughput laboratory integration platforms aimed at supporting large-scale infectious disease and genomic testing demand across North America and Europe.

-

2026: Roche Diagnostics strengthened its molecular testing ecosystem by advancing next-generation multiplex assay development and integrated digital laboratory solutions designed to improve testing efficiency and reduce turnaround time in clinical settings.

-

2025: QIAGEN N.V. expanded its syndromic and molecular diagnostics portfolio with advanced sample preparation and nucleic acid assay technologies to support decentralized testing and precision medicine applications globally.

-

2025: Danaher Corporation (Cepheid) accelerated deployment of rapid molecular testing systems and cartridge-based diagnostic solutions focused on expanding near-patient infectious disease detection capabilities and improving accessibility across healthcare environments.

Nucleic Acid Testing Market Key Players:

-

Roche Diagnostics

-

Hologic Inc.

-

QIAGEN N.V.

-

Danaher Corporation (Cepheid/Beckman Coulter)

-

Thermo Fisher Scientific Inc.

-

Bio-Rad Laboratories Inc.

-

Siemens Healthineers AG

-

bioMérieux S.A.

-

Agilent Technologies Inc.

-

Becton, Dickinson and Company (BD)

-

PerkinElmer Inc. (Revvity)

-

Illumina Inc.

-

Grifols S.A.

-

Meridian Bioscience Inc.

-

OraSure Technologies Inc.

-

GenMark Diagnostics Inc.

-

BGI Genomics Co., Ltd.

-

Exact Sciences Corporation

Nucleic Acid Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.52 Billion |

| Market Size by 2035 | USD 8.42 Billion |

| CAGR | CAGR of 6.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Polymerase Chain Reaction (PCR) & Real-Time PCR, Isothermal Amplification Technologies, Sequencing-Based Testing, Hybridization-Based Assays, Digital Molecular Diagnostics, Others) • By Product Type (Instruments, Reagents & Kits, Consumables, Software & Services) • By Application (Infectious Disease Diagnostics, Blood Screening, Oncology Testing, Genetic Disease Testing, Others) • By End User (Hospitals & Diagnostic Laboratories, Research & Academic Institutes, Blood Banks, Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Others) • By Sample Type (Blood Samples, Urine Samples, Saliva Samples, Tissue Samples, Swab Samples, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Roche Diagnostics, Hologic Inc., QIAGEN N.V., Abbott Laboratories, Danaher Corporation (Cepheid/Beckman Coulter), Thermo Fisher Scientific Inc., Bio-Rad Laboratories Inc., Siemens Healthineers AG, bioMérieux S.A., Agilent Technologies Inc., Becton, Dickinson and Company (BD), PerkinElmer Inc. (Revvity), Illumina Inc., Grifols S.A., Meridian Bioscience Inc., OraSure Technologies Inc., Seegene Inc., GenMark Diagnostics Inc., BGI Genomics Co., Ltd., Exact Sciences Corporation. |

Frequently Asked Questions

North America dominated the nucleic acid testing market in 2025.

The polymerase chain reaction (PCR) & real-time PCR segment dominated the nucleic acid testing market in 2025.

Rising prevalence of infectious diseases, increasing adoption of precision medicine, expanding oncology diagnostics, and growing demand for rapid molecular testing technologies are driving demand for advanced nucleic acid testing solutions globally.

The nucleic acid testing market was valued at USD 4.52 billion in 2025.

The nucleic acid testing market is expected to grow at a CAGR of 6.57% from 2026 to 2035.

Get in Touch