Stainless Steel Market Report Scope & Overview:

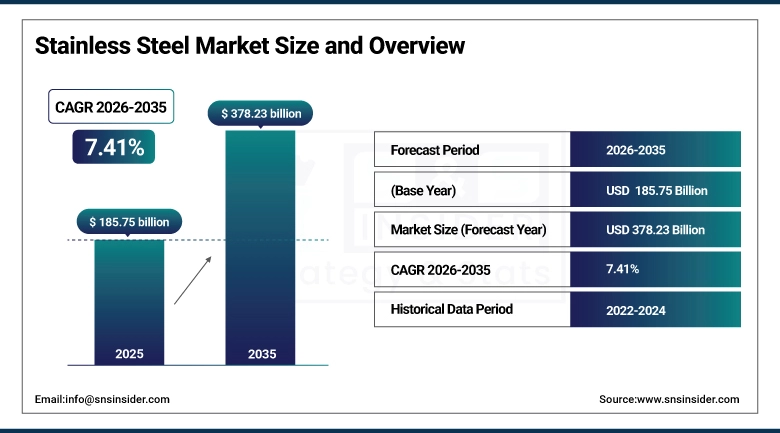

The Stainless Steel Market size is valued at USD 185.75 Billion in 2025 and is projected to reach USD 378.23 Billion by 2035, growing at a CAGR of 7.41% during the forecast period 2026–2035.

The Stainless Steel Market analysis report offers a comprehensive study of market dynamics, innovations, and industry applications. Growing infrastructure construction, surging demand from the automotive & transportation industries, increased use in consumer goods & appliances, and rising machinery & energy projects are propelling market expansion between 2026 and 2035.

Stainless steel production exceeded 60 million metric tons in 2025, fueled by rapid urbanization, technological advancements in specialty grades, and strong demand across Asia-Pacific, particularly in China and India.

Market Size and Forecast:

-

Market Size in 2025: USD 185.75 Billion

-

Market Size by 2035: USD 378.23 Billion

-

CAGR: 7.41% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Stainless Steel Market - Request Free Sample Report

Stainless Steel Market Trends:

-

HVDC transmission lines are expanding rapidly worldwide, especially in Asia and Europe.

-

Installed HVDC capacity continues to rise, with submarine and underground lines gaining share alongside overhead lines.

-

The average cost per kilometer of HVDC installation is gradually declining due to technology improvements.

-

Voltage Source Converter (VSC) technology is gaining market share over Line-Commutated Converter (LCC) systems.

-

Converter station efficiency has improved steadily over the last decade.

-

HVDC components such as valves, transformers, and control systems have long lifespans, often exceeding 30 years.

-

Capital expenditure is increasingly directed toward advanced converter stations and control systems.

-

Governments are allocating significant funding and subsidies to HVDC infrastructure projects.

-

Regulatory approval timelines for HVDC projects remain a critical factor influencing deployment speed.

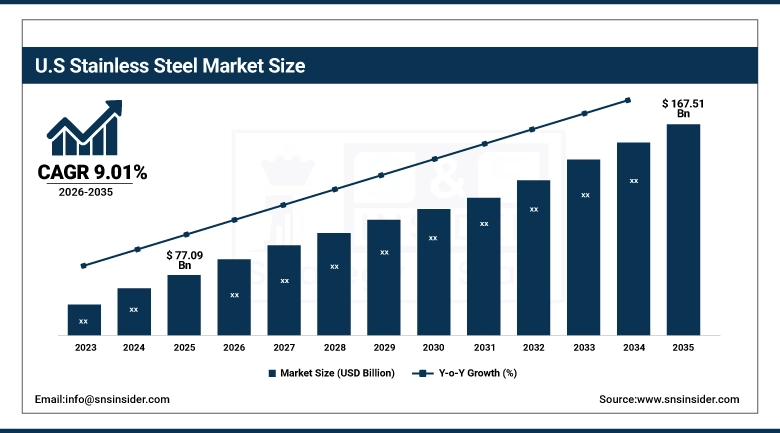

U.S. Stainless Steel Market Insights:

The U.S. Stainless Steel Market is projected to grow from USD 77.09 Billion in 2025 to USD 167.51 Billion by 2035, at a CAGR of 9.01%. The growth of the industry is supported by the fast pace of urbanization and infrastructure development, increased demands in automobiles and transport sectors, widespread use of stainless steel in household items, and increased spending on industrial equipment and power generation facilities.

Stainless Steel Market Growth Drivers:

-

Rising demand from construction, automotive, and industrial infrastructure driving Stainless Steel Market growth.

Urbanization trends, growing infrastructural developments, and increased manufacturing operations are some of the factors driving the growth of the stainless steel market. Many industries including the construction sector, the automotive sector, oil & gas industry, food industry, and medical industry are using more stainless steel owing to its properties of corrosion resistance, strength, durability, and recyclability. Increased consumption of stainless steel in areas like bridges, railway tracks, construction materials, cooking utensils, surgical tools, and electric vehicles is fueling the market growth even further.

Over 61% of construction, automotive, and industrial manufacturing companies in 2025 utilized stainless steel components to improve durability, corrosion resistance, and structural strength across critical applications.

Stainless Steel Market Restraints:

-

Volatility in raw material prices and supply chain disruptions restraining Stainless Steel Market growth.

Price volatility in relation to crucial raw materials like nickel, chromium, and iron ore, coupled with uncertainties in the international supply chain, is posing many problems within the stainless steel industry. For the manufacturers as well as the various end-user industries using stainless steel within the construction, automotive, and manufacturing industries, it is leading to higher costs and volatile pricing. Dependency on scarce raw materials and trade limitations have compounded this problem.

Over 34% of stainless steel producers and end-use industries in 2025 were affected by raw material price volatility and supply chain disruptions, leading to cost pressure and delayed project execution across key application sectors

Stainless Steel Market Opportunities:

-

Rising demand for sustainable infrastructure and recyclable materials presents significant opportunities for the Stainless Steel Market.

Increased usage of green building techniques and initiatives related to the circular economy would generate favorable prospects for the stainless steel market. There would be greater usage of stainless steel by construction companies, automobile companies, and makers of industrial equipment because stainless steel is highly recyclable, durable, and requires minimal maintenance. Stainless steel companies that manufacture innovative stainless steel products with enhanced high strength and durability features can gain from this trend.

Over 50% of infrastructure developers, automotive OEMs, and industrial manufacturers in 2025 adopted stainless steel solutions driven by sustainability goals and lifecycle efficiency requirements.

Stainless Steel Market Segmentation Analysis:

-

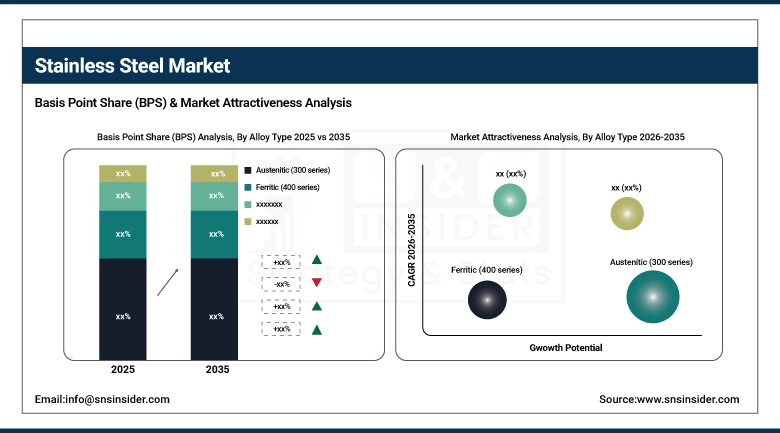

By Alloy Type, Austenitic (300 series) held the largest market share of 64.58% in 2025, while Duplex / Super Duplex are expected to grow at the fastest CAGR of 9.43% during 2026–2035.

-

By Product Form, Flat products dominated with 55.67% market share in 2025, whereas Pipes & tubes are projected to record the fastest CAGR of 8.61% through 2026–2035.

-

By Application, Construction dominated with a 29.68% share in 2025, while Industrial machinery is anticipated to expand at the fastest CAGR of 8.15% through 2026–2035.

-

By Surface / Processing, Hot rolled held the largest share of 39.49% in 2025, while Polished / mirror finish is expected to grow at the fastest CAGR of 8.86% during the forecast period.

By Alloy Type, Austenitic (300 series) dominates while Duplex/Super Duplex emerges as the fastest-growing segment:

The Austenitic (300 series) segment dominates the stainless steel market owing to its high resistance to corrosion, remarkable ductility, and extensive use in sectors such as construction, automobiles, food industry, and medical sector. High welding capability and adaptability of Austenitic (300 series) make them more desirable for various industrial applications.

Duplex and Super Duplex stainless steels constitute the fastest growing segment, mainly because of rising demand from oil & gas, marine, chemical processing, and offshore industries. The segment is witnessing faster growth owing to their exceptional mechanical properties, enhanced resistance to corrosion, and economical production even under extreme conditions.

By Product Form, Flat Products dominate while Pipes & Tubes emerge as the fastest-growing segment:

Flat Products have the dominating share of stainless steel markets owing to their wide application in various sectors such as construction, car manufacturing, kitchen equipment manufacturing, industrial fabrication, and others due to their high strength, malleability, and cost-effectiveness. They are the most favored products in large-scale industries due to easy processing, availability in many grades, and capability of mass production.

The Pipes and Tubes category is witnessing rapid growth on account of the rising requirement from end-user industries such as oil and gas, water and wastewater treatment plants, chemical manufacturing, and infrastructural projects due to their properties of corrosion resistance, durability, and capability to handle high pressures.

By Application, Construction leads while Industrial machinery grows rapidly:

The Construction industry forms the dominance of the stainless steel market due to the extensive use of stainless steel in structural frameworks, facades, reinforcements, and buildings, aided by quick urbanization and infrastructural development. The rising number of investments being made towards smart city developments and infrastructure development drives up demand.

Industrial machinery is the fastest growing category on account of growing automation, expanding production lines, and requirements for corrosion-resistant parts that can withstand tough conditions. This is being further driven by the adoption of Industry 4.0 technologies and production centers.

By Surface / Processing, Hot Rolled dominates while Polished / mirror finish grows fastest:

The Hot Rolled stainless steel segment is dominant because of the good structural strength, economic benefits, and wide-ranging applicability in construction and heavy industries. The hot rolled variety is widely used for big structural applications, ship building, and manufacturing equipment because of easy availability and capability of withstanding stress.

The Polished and Mirror finished variety is expected to be the fastest growing, owing to the increasing requirement for its application in architecture, luxurious interior decoration, kitchen equipment and car body designing among other sectors where both aesthetics and corrosion resistance take precedence.

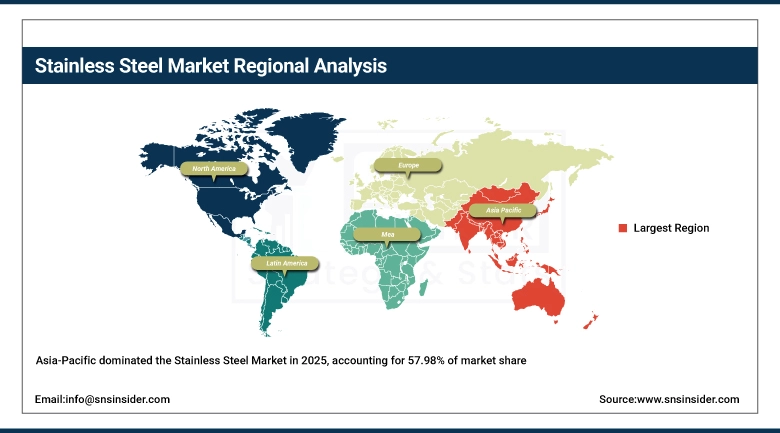

Stainless Steel Market Regional Analysis:

Asia-Pacific Stainless Steel Market Insights:

Asia-Pacific commands the highest market share at 57.98%, along with being the leading market for stainless steel with CAGR at 7.81%, anticipated to grow further in forecast period of 2026-2035. The growth in the Asia-Pacific region is attributed to high urbanization rates, infrastructural growth, and demands from the automotive, construction, and consumer goods industries. The key countries driving the growth in the Asia-Pacific region include China and India, backed by industrial developments led by the government and demands from the middle class.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Stainless Steel Market Insights:

China is at the forefront in terms of production and consumption of stainless steel, attributed to extensive infrastructure development, automobiles, and machinery requirements. The country is favored due to high levels of government support, technological capabilities, and increasing domestic demand. There is growing demand for specialized stainless steel types, such as duplex and precipitation hardened steel.

North America Stainless Steel Market Insights:

North America’s stainless steel market is expected to have a steady growth rate between 2026 and 2035. In North America, the U.S. is the highest consumer, owing to applications in the construction, industrial machinery, and medical device industries. Market development can be attributed to sustainable practices, recycling, and new stainless steel grades in the aerospace and defense sectors. Though mature when compared to Asia Pacific, continuous advancements in specialty finishing and high-performance alloy grades are anticipated to fuel market growth.

United States Stainless Steel Market Insights:

U.S. stainless steel market is influenced by demands from the construction, automotive, aerospace, and healthcare industries. Investment in renewable energy and manufacturing infrastructure has led to an increase in the consumption of specialty alloys. Issues such as recycling and sustainable production have brought about changes in supply chains, while domestic manufacturers aim at producing high-value products to compete with foreign goods. The growth rate of the market is relatively slow compared to that of Asia-Pacific, though.

Europe Stainless Steel Market Insights:

The European market for stainless steel is forecasted to grow steadily, with Germany, Italy, and Finland leading the way. Growth drivers include the construction industry, automobile manufacturing, and renewable energy industry, with a high focus on sustainable development and circular economy principles. Major players include Outokumpu, Aperam, and Acerinox, who concentrate on high-grade stainless steels with specific finishes. The region is growing at a lower pace compared to the Asia-Pacific region.

Germany Stainless Steel Market Insights:

Germany is the largest consumer of stainless steel in Europe because of its automotive industry and machinery and construction sectors. The industry focuses on producing quality and well-engineered products. The demand for cold-rolled stainless steel products and special finish types is increasing due to sustainability rules and recycling programs influencing production approaches. Renewable energy projects in the country contribute to increased product demand. Advanced manufacturing capabilities guarantee sustained growth in the sector.

Latin America Stainless Steel Market Insights:

Latin America's market for stainless steel products is expected to experience moderate growth between 2026 and 2035, with major contributors being Brazil and Mexico. The demand for stainless steel will be driven by the construction sector, manufacturing machinery sector, and consumer goods industry. The growth in infrastructure construction projects as well as an increase in the middle-class consumer base have resulted in such growth. The region's stainless steel consumption is dominated by imports but has shown steady local production growth.

Middle East & Africa Stainless Steel Market Insights:

The Middle East & Africa stainless steel market is forecasted to expand at its best pace. Factors such as major construction developments, increasing demand from the oil and gas sector, and energy infrastructure development are contributing to the growth. Consumption is highest in the UAE and Saudi Arabia, whereas South Africa is also showing promise due to the presence of Columbus Stainless. Investments in renewables and diversification of industries are fueling the demand for high-grade stainless steels.

Stainless Steel Market Competitive Landscape:

Tsingshan Holding Group, established in 1988 and based out of Wenzhou, China, is the leading stainless steel producer globally and a member of the Fortune Global 500 companies list. The company operates in a wide array of stainless steel and nickel products, featuring an integrated production process and a well-established supply chain across the globe. Tsingshan is renowned for its innovative technology, low-cost manufacturing, and ventures into renewable energy resources and international operations.

-

In February 2025, Tsingshan launched a new energy industry base through Ruipu Energy, investing nearly RMB 10 billion. The company also expanded operations in Argentina through strategic cooperation agreements, strengthening its global footprint.

China Baowu Steel Group, established in 2016 through the merger of Baosteel Group and Wuhan Iron & Steel Corporation, is one of the world’s largest steel manufacturers headquartered in Shanghai. The company produces advanced steel products for automotive, construction, energy, infrastructure, and industrial applications while focusing on digitalization, green manufacturing, and global expansion initiatives.

-

In June 2025, Baowu introduced over 90 new national steel standards, including innovations in wear-resistant and high-strength steels for construction machinery and mining equipment. It also gained global recognition for developing a proprietary testing method for secondary embrittlement in high-strength steel applications.

POSCO Holdings, established in 1968, is a leading South Korean steel manufacturer headquartered in Pohang. The company produces hot-rolled, cold-rolled, stainless, and specialty steel products serving automotive, shipbuilding, construction, and energy industries. POSCO is recognized globally for advanced steelmaking technologies, sustainability initiatives, and investments in battery materials, hydrogen-based steel production, and renewable energy projects.

-

In January 2026, POSCO advanced its “green steel” initiatives in India, focusing on carbon reduction technologies and partnerships with local industries. Globally, POSCO is transitioning to carbon-reduced manufacturing processes and expanding renewable energy integration through its HyREX technology platform.

Stainless Steel Market Key Players:

-

Tsingshan Holding Group

-

China Baowu Steel Group

-

POSCO

-

Acerinox

-

Outokumpu

-

Jindal Stainless

-

Nippon Steel Corporation

-

Yieh United Steel Corp (YUSCO)

-

Aperam

-

Allegheny Technologies Incorporated (ATI)

-

Viraj Profiles

-

Baosteel Stainless Steel

-

ArcelorMittal Stainless Europe

-

Sandvik Materials Technology

-

Thyssenkrupp Stainless

-

Daido Steel

-

Shandong Taishan Steel Group

-

Guangxi Chengde Group

-

Columbus Stainless (South Africa)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 185.75 Billion |

| Market Size by 2035 | USD 378.23 Billion |

| CAGR | CAGR of 7.41% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Alloy Type (Austenitic (300 series), Ferritic (400 series), Martensitic, Duplex / Super Duplex, Precipitation Hardening, Others), • By Product Form (Flat Products, Long Products, Pipes & Tubes, Forgings & Castings, Others), • By Application (Consumer Goods, Construction, Automotive & Transportation, Industrial Machinery, Energy & Chemicals, Others), • By Surface / Processing (Hot Rolled, Cold Rolled, Polished / Mirror Finish, Coated / Specialty Finishes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tsingshan Holding Group, China Baowu Steel Group, POSCO, Acerinox, Outokumpu, Jindal Stainless, Nippon Steel Corporation, Yieh United Steel Corp (YUSCO), Aperam, Allegheny Technologies Incorporated (ATI), Viraj Profiles, Baosteel Stainless Steel, ArcelorMittal Stainless Europe, Sandvik Materials Technology, Thyssenkrupp Stainless, Daido Steel, Shandong Taishan Steel Group, Guangxi Chengde Group, Columbus Stainless (South Africa), North American Stainless (NAS). |

Frequently Asked Questions

Asia-Pacific dominated with a 57.98% share in 2025, while it also the fastest-growing region, expected to expand at a CAGR of 7.81% during 2026–2035.

Austenitic (300 series) dominated with a 64.58% share in 2025, while Duplex / Super Duplex are projected to grow at the fastest CAGR of 9.43% during 2026–2035.

Growth is driven by infrastructure development, rising demand from automotive and transportation sectors, increasing use in consumer goods and appliances, expansion of industrial machinery and equipment.

The market is valued at USD 185.75 Billion in 2025 and is projected to reach USD 378.23 Billion by 2035.

The Stainless Steel Market is projected to grow at a CAGR of 7.41% during 2026–2035.

Get in Touch