Cartilage Degeneration Market Report Scope & Overview:

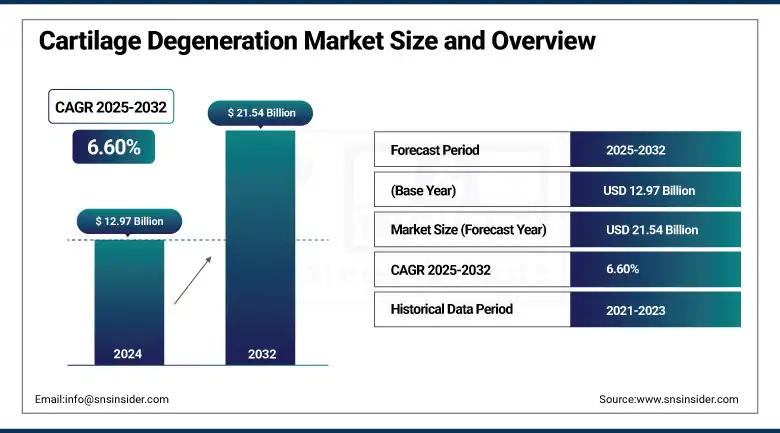

The Cartilage Degeneration Market size was valued at USD 12.97 billion in 2024 and is expected to reach USD 21.54 billion by 2032, growing at a CAGR of 6.60% over the forecast period of 2025-2032.

The global cartilage degeneration market is experiencing significant growth due to the increasing incidence of osteoarthritis, sports injuries, and a growing aging population. Also, some of the exciting advances in regenerative medicine, including autologous chondrocyte implantation and tissue engineering, are promoting treatment. The market is also being driven by increased demand for minimally invasive procedures and better reimbursement policies. Furthermore, increasing awareness regarding early intervention along with the availability of various biologic therapies are some factors propelling the market growth in hospitals and specialty care clinics globally.

To Get more information On Cartilage Degeneration Market - Request Free Sample Report

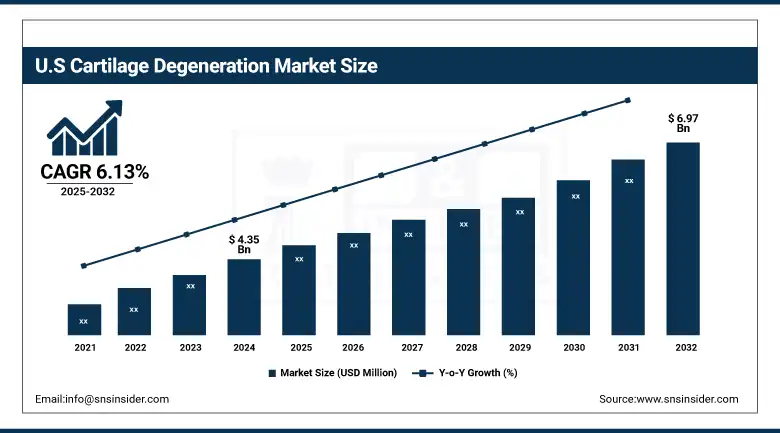

The U.S. cartilage degeneration market size was valued at USD 4.35 billion in 2024 and is expected to reach USD 6.97 billion by 2032, growing at a CAGR of 6.13% over the forecast period of 2025-2032.

The U.S. dominated the North American cartilage degeneration market in 2024, owing to its sophisticated healthcare infrastructure, increasing prevalence of osteoarthritis and associated risk factors, and the growing uptake of regenerative therapies. The U.S. represented the highest share in the regional market, highlighting its impact on the cartilage degeneration market trends.

Cartilage Degeneration Market Dynamics:

Drivers:

-

Rising Prevalence of Osteoarthritis and Sports Injuries is Driving the Market Growth

Osteoarthritis is a degenerative joint disease characterized by a progressive loss of cartilage and is one of the most common arthritic disorders globally, particularly in an ageing population. As it results in pain, stiffness, and limited movement, patients have become keen in doctoring for effective remedies. As participation in sports and physical activities has increased, the rate of cartilage injuries has increased. Although special cartilage repair procedures are required for these injuries, this creates a demand for products and technologies that will restore cartilage function and improve patient outcomes.

In 2021, the global prevalence of osteoarthritis (OA) was approximately 607 million, with knee OA being the most common subtype, with a reported prevalence of 365 million people.

-

Increasing Development of Regenerative Medicine and Biologic Therapies is Determining the Growth of the Market

Regenerative medicine strategies, including the use of autologous chondrocyte implantation (ACI), stem cells, and bioengineered scaffolds, have contributed to changes in cartilage repair. Unlike conservative measures that only address the symptoms, these modern therapies have the potential to regenerate damaged cartilage. These novel therapies enhance the natural regenerative processes of the body to facilitate the success of cartilage restoration procedures, further promoting cartilage degeneration market growth by increasing healthcare professionals' and patients' acceptance of the therapy.

A new approach to cartilage tissue generation carries promise for cartilage repair, according to two studies from MIT and the National University of Singapore, which found that introducing ascorbic acid during mesenchymal stromal cell (MSC) expansion improved their chondrogenic potential.

Restraints:

-

Complex Regulatory Approvals are Limiting the Growth of the Market

Cartilage degeneration treatments, particularly those using novel therapies such as cell-based implants, tissue engineering, stem cell therapies, and gene editing technologies, are subject to rigorous regulatory mechanisms because of their complexity and biological nature. Hence, regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) label these products biologics or Advanced Therapy Medicinal Products (ATMPs), which demand complete preclinical and clinical evidence for safety, efficacy, and long-term durability.

It requires several stages of clinical trials, which take years to complete and are expensive. On top of this, increasingly stringent regulations, especially for new types of solutions such as 3D-printed scaffolds or tailored cell therapies, complicate matters even more. As a result, these challenges can lead to delayed product launches, increased R&D costs, and disinterest from smaller companies or startups in entering the market, which may further slow innovation and the commercial availability of beneficial cartilage repair technologies.

Cartilage Degeneration Market Segmentation Analysis:

By Procedure Type

The microfracture segment dominated the cartilage degeneration market with a 54.30% market share by procedure type in 2024, due to its wide adoption, low cost, and minimally invasive nature. This is a classical surgical approach used as a first-line treatment to initiate cartilage regeneration using small subchondral bone fissures to induce new cartilaginous tissue. Microfracture provides a relatively simple, shorter hospitalization time and good clinical results in early-stage cartilage defects, which leads orthopedic surgeons to favor it as their first-line treatment for knee joint degeneration.

The osteochondral allograft transplantation segment is anticipated to exhibit the fastest growth in the duration of the forecast period. Improvements in the preservation of graft technology and a wide acceptance of donor tissue and transplant success rates in the clinic have all enabled this growth in tissue engineering for large or complex cartilage lesions. With increasing awareness of long-term results and the success of this procedure, particularly in the active, younger population that would benefit from enduring solutions, allograft transplantation will be more greatly sought.

By Application

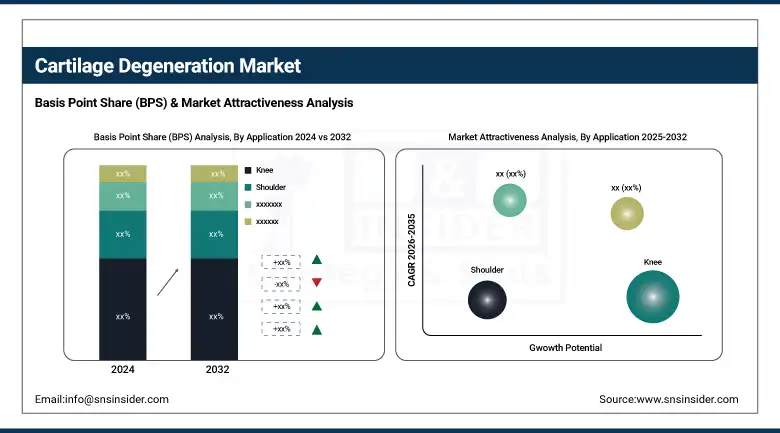

The Knee segment dominated the cartilage degeneration market in 2024 with a 72.20% market share, owing to the high prevalence of knee-related cartilage injuries and Knee osteoarthritis. Knee joints are vulnerable to degenerative change owing to constant weight-bearing and repetitive activity, particularly in sportsmen and amongst the older demographic. In addition to these advances, the knee has become the focus of cartilage repair efforts, arguably due to the relative novelty of diagnostic tools, early intervention techniques, and the widespread availability of surgical options, such as microfracture, autologous chondrocyte implantation (ACI), and osteochondral grafting.

Due to the increasing prevalence of femoroacetabular impingement (FAI), hip labral tears, and other degenerative conditions, the Hip segment is expected to grow at the fastest rate during the forecast period. Demand is being driven by increased uptake of early diagnosis and a growing patient population of younger and increasingly active patients who are opting for less invasive hip preservation surgeries. This is also a result of better imaging technology available, surgical intervention helps to manage hip cartilage damage more effectively than ever in the fast-growing segment.

By End-User

The hospitals segment dominated the cartilage degeneration market share by end-user in 2024 with a 68.5% market share, owing to the well-built infrastructure, availability of advanced surgical equipment, and presence of trained orthopedic surgeons. Severe cartilage injury and degenerative joint disease are commonly encountered clinical problems, presenting most often initially in the hospital for diagnosis, surgical treatment, and postoperative care. Moreover, wide hospital capabilities for carrying out hauling out complicated methods, including autologous chondrocyte implantation and osteochondral transplants, have helped the segment maintain its leading position within the cartilage degeneration market analysis.

The specialty clinics segment is anticipated to grow at the fastest CAGR over the forecast period, as the demand for targeted and outpatient-based orthopedic care is expected to rise further. These facilities combine personalized treatment and shorter waiting times with affordability, attracting an increasing number of health-conscious patients. In addition, specialty clinics are now able to perform an increasing array of cartilage repair procedures largely due to technological improvements and minimally invasive procedures, drawing patients who want a quick recovery and want to avoid the hospital.

Regional Analysis:

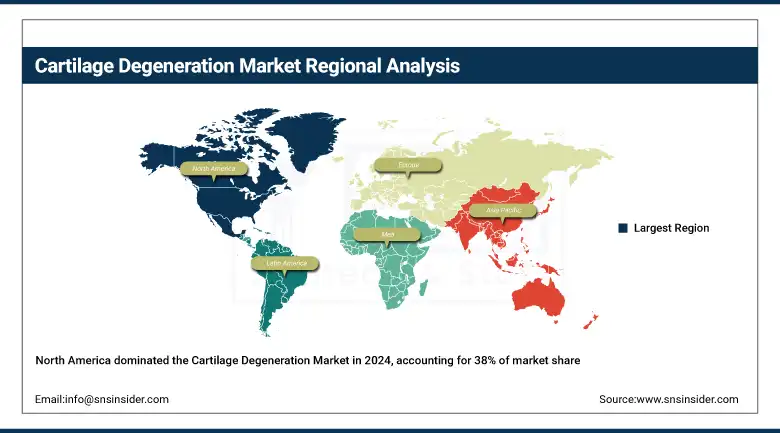

North America dominated the cartilage degeneration market with around 38% market share in 2024, due to the presence of well-established healthcare infrastructure, rising awareness of joint disorders, and availability of advanced treatment options in the region. Given high patient demand in the territory linked to athletes, along with the expected increase in demand from the ageing population for osteoarthritis and associated cartilage injuries, this region represents substantial potential for the Group. In addition, a significant number of prominent companies, favorable reimbursement treatment, and ongoing investments in regenerative medicine R&D have combined to drive additional growth for the market. The U.S. in particular emerges with a markedly high utilization of emerging treatment options, such as autologous chondrocyte implantation and osteochondral grafting.

Get Customized Report as per Your Business Requirement - Enquiry Now

The cartilage degeneration market in Asia Pacific is projected to grow at the fastest rate during the forecast period, with a 7.42% CAGR, owing to a large elderly population, increasing prevalence of disorders related to joints, and an increase in awareness regarding early diagnosis and treatment. The ongoing economic growth in the other countries, including China, India, and South Korea has led to the improvement of healthcare access and the increase in health expenditure in these countries, thus enabling advanced orthopedic procedures to be made more available. Moreover, rising government initiatives to improve healthcare infrastructure, proliferation of medical tourism, and increasing investments of foreign medical device companies are driving market growth in the region. Additionally, the growth of the market in the region is driven by the increasing adoption of minimally invasive procedures.

Europe is expected to remain a key contributor to the cartilage degeneration market, owing to the advanced healthcare infrastructure and rise in joint disorder prevalence, and adoption of innovative treatment modalities in the region. which in part is attributed to well-established medical system and high health care expenditures, specifically in the U.K., Germany, and France. The growth of the market is fueled by the early detection approach in the region, and additionally, the availability of advanced therapies for treatment, such as autologous chondrocyte implantation, along with stem cell therapies.

In addition, increased incidence of degenerative joint diseases, particularly osteoarthritis, due to an aging population in certain regions, such as Europe, is anticipated to propel the growth of the market over the years. The government's initiatives to enhance the quality of healthcare services, coupled with the presence of key market players, are likely to drive the growth of the market as well. Europe is anticipated to retain its substantial position in the global cartilage degeneration market due to continual R&D activities and the initiation of minimally invasive procedures.

The cartilage degeneration market in Latin America is expected to witness moderate growth owing to the awareness regarding joint health and the increasing prevalence of orthopedic conditions, such as osteoarthritis and sports-related injuries, in the region. Health care systems in Latin America and other countries are maturing and seeking to provide more complex orthopedic treatment pathways, particularly cartilage repair strategies. At the same time, increasing age, changes in lifestyle, and motility contribute to the pool of patients in need of treatment for cartilage degeneration.

The Middle East & Africa (MEA) market is in a progressing phase owing to the increasing prevalence of obesity, the availability of sports activities availability of orthopedic treatment in metropolitan areas. However, any barriers to the market will give way to improvements in institutional healthcare systems and the growth of private medical services, helping to drive moderate market growth.

Cartilage Degeneration Market Key Players:

The cartilage degeneration companies are Zimmer Biomet Holdings, Smith & Nephew, Stryker, DePuy Synthes, Vericel, Anika Therapeutics, Arthrex, Histogenics, Orthocell, Medtronic, and other players.

Recent Developments in the Cartilage Degeneration Market:

-

August 2024 – Researchers at Northwestern University have created a new bioactive material that can regenerate high-quality cartilage in the knee joints of large-animal models. Even though it has a rubbery, gel-like appearance, the material contains a refined network of molecular components that work together to mimic the natural environment of cartilage inside the human body.

-

February 2024 – Smith+Nephew, a global leader in medical technology, introduced its new CARTIHEAL AGILI-C Cartilage Repair Implant and REGENETEN Bioinductive Implant at the AAOS Annual Meeting. These technologies highlight the company's leadership in biologically driven sports medicine technology. Both implants are supported by strong clinical evidence and are strongly improving soft tissue repair results over conventional methods.

Cartilage Degeneration Market Report Scope:

Report Attributes Details Market Size in 2024 USD 12.97 Billion Market Size by 2032 USD 21.54 Billion CAGR CAGR of 6.60% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Procedure Type (Microfracture, Osteochondral Allograft Transplantation, Osteochondral Autograft Transplantation, Autologous Chondrocyte Implantation (ACI), Others)

• By Application (Knee, Hip, Shoulder, Others)

• By End-user (Hospitals, Specialty Clinics, Others)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles Zimmer Biomet Holdings, Smith & Nephew, Stryker, DePuy Synthes, Vericel, Anika Therapeutics, Arthrex, Histogenics, Orthocell, Medtronic, and other players.

Frequently Asked Questions

North America dominated the Cartilage Degeneration Market in 2024.

The “Knee” segment dominated the Cartilage Degeneration Market.

The Rising prevalence of osteoarthritis and sports injuries is driving the market growth.

The Cartilage Degeneration Market was USD 12.97 billion in 2024 and is expected to reach USD 21.54 billion by 2032.

The Cartilage Degeneration Market is expected to grow at a CAGR of 6.60% from 2025 to 2032.

Get in Touch