Graphene Electronics Market Report Scope & Overview:

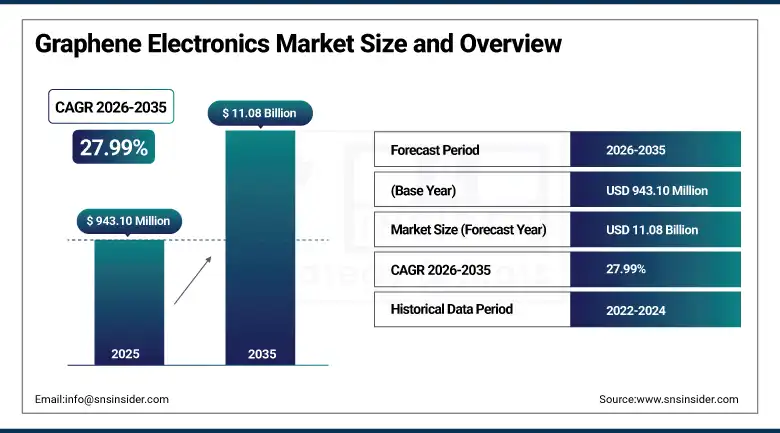

The Graphene Electronics Market was valued at USD 943.10 Million in 2025 and is expected to reach USD 11.08 Billion by 2035, growing at a CAGR of 27.99% from 2026–2035.

The global graphene electronics market is growing at an exceptional pace. The market expansion is largely attributed to graphene's exceptional material characteristics: high electrical conductivity, mechanical strength, thermal conductivity, optical transparency, and flexibility that collectively enable next-generation electronics demanding faster speeds, reduced energy consumption, and greater durability than conventional semiconductor materials. Rising demand for high-performance flexible electronics, energy storage devices, and advanced sensors across consumer electronics, automotive, healthcare, and telecommunications applications is sustaining above-average commercial investment in graphene electronics commercialisation.

In April 2024, Zeta Energy and Log9 Materials partnered to develop next-generation lithium-sulfur battery systems using graphene technology, aiming to enhance performance and sustainability for EVs and energy storage applications. The collaboration targets the EV battery market whose energy density improvement requirement creates commercial motivation for graphene-enhanced cathode and anode materials whose theoretical energy density substantially exceeds conventional lithium-ion chemistry limits.

Market Size and Forecast

-

Market Size in 2026E: USD 1,207.09 Million

-

Market Size by 2035: USD 11.08 Billion

-

CAGR: 27.99% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

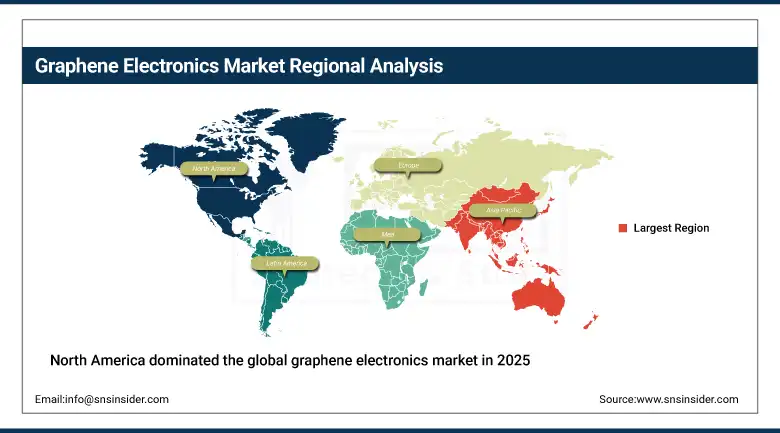

Largest Region: North America

To Get more information On Graphene Electronics Market - Request Free Sample Report

Graphene Electronics Market Trends

-

Graphene transistor commercialization is progressing toward large-scale production as researchers and technology companies demonstrate ultra-high-frequency performance.

-

Flexible and wearable electronics manufacturers are increasingly adopting graphene as a conductive electrode material.

-

Graphene-enhanced battery electrodes are improving energy density, charging speed, and battery lifespan.

-

Graphene biosensor development is expanding opportunities in medical diagnostics and healthcare monitoring.

-

Advances in chemical vapor deposition (CVD) and roll-to-roll manufacturing are reducing graphene production costs..

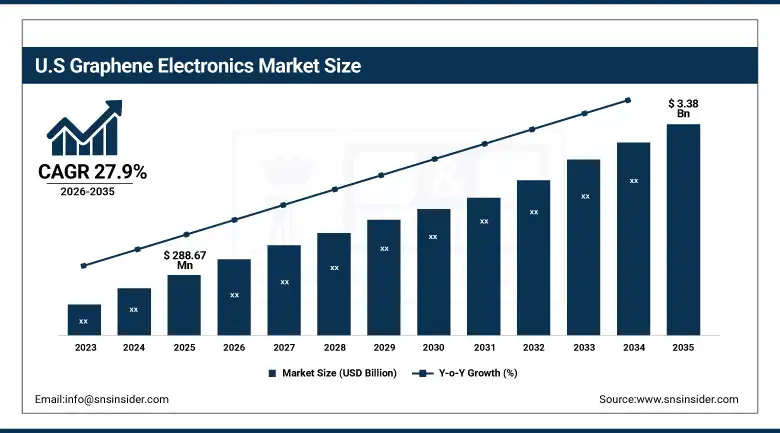

U.S. Graphene Electronics Market Outlook

The U.S. Graphene Electronics Market was valued at approximately USD 288.67 Million in 2025 and is expected to reach approximately USD 3.38 Billion by 2035, growing at a CAGR of approximately 27.9%.

The U.S. is the world's most commercially advanced graphene electronics market within North America's dominant revenue position. IBM Research, Samsung's U.S. R&D operations, Graphene Frontiers, and multiple university spinout companies define the domestic graphene electronics innovation ecosystem. DARPA and DOE research funding sustains pre-commercial graphene electronics development whose government-funded innovation pipeline feeds commercial application development..

In June 2023, Tecnalia developed a digital twin with sensors in partnership with Avanzare to reduce operator exposure to graphene particles during extraction, reflecting the safety and process optimisation investment that commercial graphene production scale-up requires. The development demonstrates the growing commercial maturity of graphene manufacturing processes whose occupational safety management is becoming an institutional procurement requirement for graphene materials used in regulated industrial applications.

Graphene Electronics Market Segment Analysis

-

By Product Type, the Graphene Coatings segment dominated the Graphene Electronics Market with approximately 35.80% share in 2025, while the Graphene Nanoplatelets segment is the fastest growing.

-

By Material Type, the Graphene Oxide segment dominated the Graphene Electronics Market with approximately 41.50% share in 2025, while the Reduced Graphene Oxide segment is the fastest growing.

-

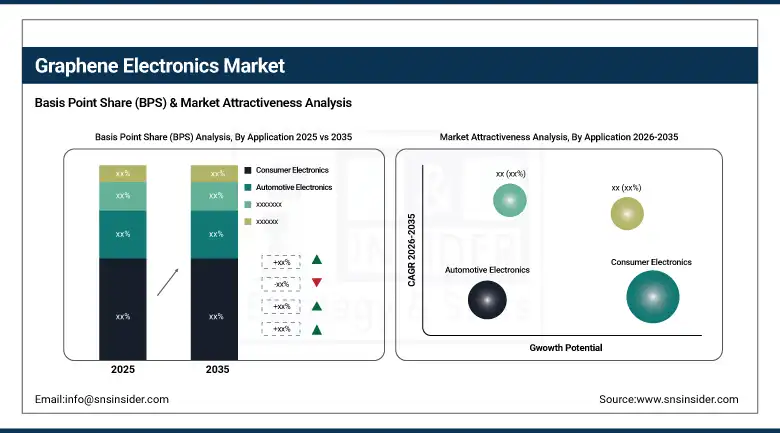

By Application, the Consumer Electronics segment dominated the Graphene Electronics Market with approximately 38.20% share in 2025, while the Energy Storage segment is the fastest growing.

-

By End User, the OEM segment dominated the Graphene Electronics Market with approximately 61.40% share in 2025, while the Research & Development segment is the fastest growing.

By Product Type, coatings dominate, graphene nanoplatelets grow fastest

Graphene coatings retained the dominant product type position with approximately 35.8% of the graphene electronics market in 2025. Their commercial primacy reflects the accessible technology pathway that graphene coating application provides for commercial adoption without requiring the precision deposition equipment and controlled contamination management that electronic-grade graphene transistor fabrication demands. Conductive graphene coatings for electromagnetic interference shielding, anti-static coatings for sensitive electronic enclosures, and thermal management graphene film coatings for heat dissipation in power electronics collectively represent commercially established graphene coating applications whose volume procurement sustains the product category's market leadership.

Graphene nanoplatelets are the fastest-growing product type because their adoption in lithium-ion battery anode materials, supercapacitor electrodes, and polymer composite reinforcement is creating above-average volume commercial procurement from battery manufacturers and composite material processors. GNPs' ability to improve the mechanical strength, electrical conductivity, and thermal conductivity of polymer matrices creates multi-functional performance enhancement whose commercial value justifies premium pricing relative to conventional carbon black and carbon fibre alternatives. The EV battery sector's electrode performance improvement requirement is the most commercially significant GNP application whose procurement compounds with global battery manufacturing capacity growth.

By Application, consumer electronics dominates, energy storage grows fastest

Consumer electronics retained the dominant application position in the graphene electronics market in 2025. Smartphones, tablets, laptops, and wearable devices create the most commercially accessible graphene electronics adoption pathway through heat spreading film, battery electrode, and conductive ink applications whose integration does not require redesign of existing device architectures. Each new flagship smartphone generation that incorporates graphene thermal management creates procurement whose volume scales with global smartphone production. The consumer electronics sector's commercial accessibility, combined with its sensitivity to performance differentiation that graphene's thermal and electrical properties create, sustains its dominant application position.

Energy storage is the fastest-growing application at approximately 32.5% CAGR because EV battery manufacturing's scale is creating the most commercially significant volume graphene electrode material procurement opportunity in the market's history. Each gigawatt-hour of new battery cell manufacturing capacity that incorporates graphene-enhanced silicon anode material or graphene conductive additive creates commercial procurement whose aggregate grows proportionally with the extraordinary pace of global battery factory construction. Grid energy storage's simultaneous expansion creates an additional non-EV energy storage procurement category whose graphene electrode material adoption compounds with the EV battery sector's procurement growth.

By Material Type, graphene oxide dominates, reduced graphene oxide grows fastest

Graphene oxide retained the dominant material type position in the graphene electronics market in 2025. GO's commercial primacy reflects the liquid phase exfoliation production process's lower capital cost and higher production scalability relative to CVD single-layer graphene whose vacuum deposition equipment and process control requirements create substantially higher production cost for equivalent material volume. GO's water dispersibility enables coating, filtration membrane, and composite material processing routes that solid graphene alternatives cannot access, creating commercial application breadth that sustains GO's aggregate market leadership despite its lower electrical conductivity relative to pristine graphene.

Reduced graphene oxide is the fastest-growing material type because its electrical conductivity, restored through thermal or chemical reduction of the graphene oxide, substantially exceeds GO's insulating character while maintaining the processing accessibility of solution-processed graphene that single-layer CVD graphene's dry transfer requirements cannot match. rGO electrode films for supercapacitors, rGO conductive ink for printed electronics, and rGO-based composite materials for EMI shielding collectively represent rGO's fastest-growing commercial application portfolio whose combined procurement growth outpaces GO's established but slower-growing coating and membrane applications.

By End User, OEMs dominate, R&D grows fastest

OEMs retained the dominant end user position in the graphene electronics market in 2025. Consumer electronics manufacturers, automotive OEMs, and industrial equipment producers that specify graphene materials in production create the most commercially significant volume procurement relationships that define graphene material producers' primary revenue stream. Samsung's graphene display electrode research, automotive OEMs' graphene composite body panel evaluation, and consumer electronics manufacturers' thermal management film specification collectively represent OEM procurement whose volume economics define the commercial viability of graphene production scale investment.

Research and development is the fastest-growing end user segment because the expanding institutional R&D investment in graphene electronics applications across pharmaceutical, semiconductor, energy, and defence sectors is creating growing procurement for research-grade graphene materials whose commercial specification requirements create above-average per-unit commercial value relative to commodity industrial graphene grades. Each new DARPA programme, EU Graphene Flagship project, and corporate graphene R&D programme creates structured procurement that compounds with the global innovation ecosystem's graphene research activity.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Graphene Electronics Market Insights

North America dominated the global graphene electronics market in 2025 due to strong R&D capabilities, significant government funding, and the presence of leading technology companies. The United States accounts for approximately 87.4% of North American revenues through IBM Research, Graphene Frontiers, and multiple university spinout companies whose combined innovation output defines the global graphene electronics technology frontier. DARPA, DOE, and NSF research funding creates the institutional investment environment that sustains pre-commercial graphene electronics development whose payoff timeline extends across the forecast period.

Canada contributes approximately 12.6% of North American revenues through its active graphene research university network, government clean technology investment, and the growing clean energy sector's graphene electrode material adoption whose combined procurement sustains consistent market engagement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Graphene Electronics Market Insights

Europe is a technically sophisticated graphene electronics market where the EU Graphene Flagship's EUR 1 billion research programme, established in 2013, has created the world's most comprehensive institutional graphene research ecosystem. Germany accounts for approximately 22.3% of European revenues through its chemical and materials industry's graphene composite development, the automotive sector's lightweight material research, and BASF and Evonik's advanced materials R&D investment.

The United Kingdom, Sweden, and Spain are significant secondary European markets where Graphenea's Spanish operations, the Cambridge Graphene Centre's research output, and Scandinavian cleantech investment create consistent graphene electronics procurement and innovation. Directa Plus's Graphene Plus technology platform, whose commercial applications in textiles, environmental remediation, and composites represent the most commercially advanced European graphene product portfolio, demonstrates the EU Graphene Flagship's translation into commercial applications.

Asia Pacific Graphene Electronics Market Insights

Asia Pacific is the fastest-growing regional graphene electronics market, driven by China's Made in China 2025 initiative's advanced materials investment, Japan's semiconductor material innovation, South Korea's Samsung and LG display technology development, and India's growing electronics manufacturing sector. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary manufacturing scale whose graphene coating and composite procurement creates the largest regional volume demand, combined with domestic graphene material producers whose competitive pricing is expanding market access.

Japan and South Korea represent technically sophisticated secondary markets whose semiconductor manufacturing, display technology, and battery production create commercial graphene electronics procurement at above-average per-unit specification. The June 2023 Directa Plus and Candiani collaboration introducing G+ enhanced graphene fabric demonstrates the commercial textile application development whose Asia Pacific manufacturing adoption creates additional procurement channels.

MEA & Latin America Graphene Electronics Market Insights

The Middle East and Africa and Latin America are growing graphene electronics markets where industrial development, clean energy investment, and university research programmes create structured demand. UAE leads MEA revenues at approximately 38.4% through its technology sector investment, the growing clean energy manufacturing sector, and research institute procurement from Masdar Institute and KAUST whose graphene research programmes create institutional demand.

Brazil leads Latin American revenues at approximately 44.2% through its university research network, growing electronics manufacturing sector, and the clean energy technology investment whose graphene electrode material procurement creates structured commercial demand from battery and supercapacitor developers.

Market Dynamics

Growth Drivers: Superior material properties enabling next-generation electronics and EV battery electrode adoption creating volume demand

Graphene's exceptional material properties, combining the highest known electrical conductivity of any material at room temperature, mechanical strength 200 times stronger than steel at one-atom thickness, and thermal conductivity superior to diamond, collectively create a material performance profile that enables electronic applications impossible with conventional materials. Each new graphene electronics product category that successfully commercialises one or more of these properties creates a new demand stream whose aggregate with other commercial applications compounds the market's exceptional CAGR.

EV battery electrode adoption represents the most commercially transformative near-term graphene volume demand opportunity. Each percentage point increase in EV market share creates proportional battery manufacturing procurement whose graphene electrode material content creates commercial demand that compounds with EV market penetration growth. Graphene's ability to improve lithium-ion battery energy density, fast charging capability, and cycle life creates product differentiation that EV manufacturers' competitive positioning motivates to specify in premium vehicle applications.

Restraints: High production cost of electronic-grade graphene and lack of standardisation in graphene quality specifications

Electronic-grade graphene production through chemical vapour deposition or mechanical exfoliation creates cost premiums over conventional electronic materials that limit adoption in cost-sensitive applications where silicon or carbon alternatives provide adequate performance. The current graphene production cost structure, where high-quality CVD graphene film can cost hundreds to thousands of dollars per square metre, restricts commercial adoption to applications whose performance premium justifies the input material cost differential.

The absence of standardised graphene quality specifications across the commercial market creates procurement risk for OEM engineers whose application requires consistent graphene layer count, defect density, and electrical properties that vary across producers and production methods. Each inconsistency in commercial graphene quality creates application failure risk whose reputational impact delays adoption in safety-critical applications where material performance reliability is non-negotiable.

Opportunities: Graphene semiconductor transistor commercialisation and flexible display electrode application

Graphene transistor commercialisation represents the most commercially transformative long-term opportunity whose realisation would define graphene electronics' role in the post-silicon semiconductor era. Each graphene transistor demonstration that exceeds silicon's theoretical switching speed limit in a production-compatible process creates investment momentum that sustains R&D funding for the engineering challenges whose resolution will define the graphene transistor commercialisation timeline.

Flexible display electrode application represents the most commercially accessible near-term volume opportunity for graphene as ITO replacement in next-generation rollable and foldable display technologies. Each new foldable smartphone or rollable display product that specifies graphene transparent conductive film over brittle ITO creates commercial procurement that demonstrates graphene's manufacturing integration capability in the highest-volume precision electronics production environment globally.

Recent Developments:

-

2024: Zeta Energy and Log9 Materials partnered in April 2024 to develop graphene-enhanced next-generation lithium-sulfur battery systems targeting improved performance and sustainability for EV and energy storage applications, demonstrating the commercial momentum of graphene electrode material adoption in advanced battery chemistry development.

-

2023: Directa Plus and Candiani introduced G+ enhanced graphene fabric in June 2023, combining Graphene Plus technology for antimicrobial and thermal properties with Candiani Denim's Kikotex Polymer, representing the commercial deployment of graphene in premium textile applications creating new non-electronics commercial graphene adoption channels.

-

2023: Tecnalia partnered with Avanzare in 2023 to develop digital twin monitoring systems for graphene particle exposure management during production, reflecting the commercial maturity of graphene manufacturing processes whose occupational safety management is becoming an institutional requirement for regulated industrial applications.

Graphene Electronics Market Key Players

-

IBM Research

-

Samsung Electronics

-

Graphene Frontiers LLC

-

Grafoid Inc.

-

Graphenea S.A.

-

Directa Plus plc

-

Applied Graphene Materials

-

XG Sciences Inc.

-

Haydale Graphene Industries

-

Skeleton Technologies

-

Vorbeck Materials Corp.

-

Global Graphene Group

-

NanoXplore Inc.

-

Talga Group

-

Log9 Materials

-

Zeta Energy Corp.

-

Graphene Batteries AS

-

Nanomedical Diagnostics

-

Emberion Oy

-

Cambridge Graphene Ltd.

Graphene Electronics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 943.10 Million |

| Market Size by 2035 | USD 11.08 Billion |

| CAGR | CAGR of 6.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Graphene Coatings, Graphene Transistors, Graphene Sensors, Graphene Capacitors, Graphene Flexible Electronics, Graphene Nanoplatelets, Others) • by Type/Material (Graphene Oxide, Reduced Graphene Oxide, Single-Layer Graphene, Multi-Layer Graphene, Graphene Nanoribbons) • by Application (Consumer Electronics, Automotive Electronics, Energy Storage, Healthcare & Medical Devices, Telecommunications, Wearable Electronics, Optoelectronics, Others) • by End User (OEMs, Research & Development, Electronics Manufacturing Services, Consumer End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM Research, Samsung Electronics, Graphene Frontiers LLC, Grafoid Inc., Graphenea S.A., Directa Plus plc, Applied Graphene Materials, XG Sciences Inc., Haydale Graphene Industries, Skeleton Technologies, Vorbeck Materials Corp., Global Graphene Group, NanoXplore Inc., Talga Group, Log9 Materials, Zeta Energy Corp., Graphene Batteries AS, Nanomedical Diagnostics, Emberion Oy, Cambridge Graphene Ltd. |

Frequently Asked Questions

The Graphene Electronics Market is expected to grow at a CAGR of 27.99% from 2026 to 2035.

The Graphene Electronics Market was valued at USD 943.10 Million in 2025.

Rising demand for high-performance electronics whose speed, flexibility, and energy efficiency requirements exceed conventional material capabilities.

Graphene Coatings dominated the Graphene Electronics Market with approximately 35.8% share in 2025, while Graphene Nanoplatelets is the fastest growing segment.

North America dominated the Graphene Electronics Market in 2025 due to strong R&D capabilities and significant government funding, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch