Thin Film Battery Market Report Scope & Overview:

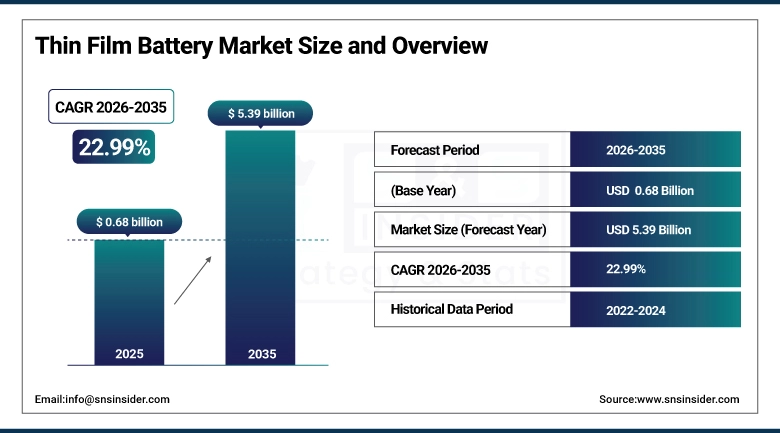

The Thin Film Battery Market was valued at USD 0.68 billion in 2025 and is expected to reach USD 5.39 billion by 2035, growing at a CAGR of 22.99% from 2026-2035.

The Thin Film Battery Market has moved well past the early-stage curiosity phase and is now a genuine high-growth segment of the global energy storage industry. What is drawing so much attention is the combination of ultra-thin form factors, solid-state electrolytes, and the ability to deposit battery layers directly onto flexible substrates qualities that simply cannot be matched by conventional battery architectures. Industries are rethinking how power gets embedded into products: instead of designing around a battery, manufacturers are designing batteries into the product itself.

The U.S. Department of Energy allocated more than USD 3 billion to over 25 battery manufacturing projects across 14 states starting September 2024 under the Bipartisan Infrastructure Law. While much of that funding targets EV and grid storage, it is directly upgrading the domestic materials science and battery fabrication ecosystem that thin film battery producers rely on particularly in critical mineral processing, electrochemical deposition techniques, and battery recycling infrastructure that benefits the entire sector.

Thin Film Battery Market Size and Forecast

-

Market Size in 2025: USD 0.68 Billion

-

Market Size by 2035: USD 5.39 Billion

-

CAGR: 22.99% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Thin Film Battery Market - Request Free Sample Report

Thin Film Battery Market Trends

-

Solid-state electrolyte development is eliminating liquid leakage risks and enabling batteries thin enough to be printed directly onto circuit boards and flexible substrates.

-

Wearable health monitoring devices continuous glucose monitors, cardiac patches, neural interfaces are demanding ever-smaller, longer-lasting power cells that only thin film technology can deliver at the required dimensions.

-

Smart packaging for pharmaceuticals and cold-chain logistics is emerging as a fast-growing use case, with thin film batteries powering NFC tags and freshness sensors embedded in labels.

-

Roll-to-roll manufacturing is beginning to scale, which should meaningfully bring down per-unit costs over the forecast horizon and open up price-sensitive IoT applications.

-

Military and aerospace programs are qualifying thin film cells for applications where weight, radiation hardness, and leak-proof construction are non-negotiable requirements.

-

Integration with energy harvesting systems piezoelectric, thermoelectric, photovoltaic is creating self-sustaining micro-devices that charge thin film batteries from ambient energy sources.

-

The push toward fully implantable neuromodulation and drug-delivery devices is accelerating regulatory pathways for biocompatible thin film chemistries.

U.S. Thin Film Battery Market Size Outlook:

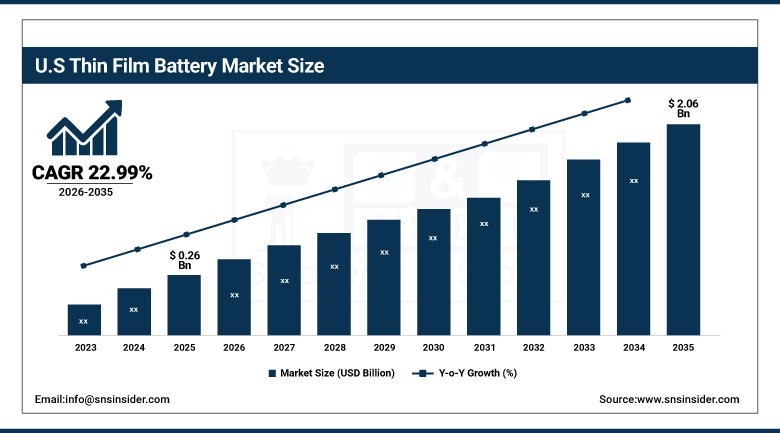

The U.S. Thin Film Battery Market was valued at USD 0.26 billion in 2025 and is expected to reach USD 2.06 billion by 2035, growing at a CAGR of 22.99% from 2026-2035. The U.S. holds a genuinely commanding position in this market not just because of demand, but because the country houses a disproportionate share of the research institutions, semiconductor fabs, and medical device developers that are actually pushing the technology forward.

The U.S. Food and Drug Administration's 510(k) pathway has seen a notable uptick in submissions for active implantable devices powered by thin film cells reflecting clinical developers' growing confidence in the technology's biocompatibility and longevity. The FDA's Center for Devices and Radiological Health has also issued updated guidance on battery-powered implant testing protocols, which is actually helping manufacturers by clarifying the evidence required for approval and reducing regulatory uncertainty that had previously slowed investment decisions.

Thin Film Battery Market Segment Analysis

-

By Battery Type, Rechargeable segment dominated the Thin Film Battery Market in 2025; Disposable segment fastest growing (CAGR ~23.61%).

-

By Battery Voltage, Below 1.5V segment dominated the Thin Film Battery Market with ~45% share in 2025; Above 3V segment fastest growing (CAGR ~23.54%).

-

By Application, Wearable Technology segment dominated the Thin Film Battery Market in 2025; Medical Devices segment fastest growing (CAGR).

By Application, Wearable Technology segment dominates the Thin Film Battery Market, Medical Devices segment expected to grow fastest

Wearable technology maintained its position as the largest application segment in the Thin Film Battery Market in 2025. Smartwatches, fitness bands, augmented reality glasses, hearing aids, and next-generation smart garments all demand power sources that fit within extremely tight physical envelopes without adding meaningful weight. Thin film batteries are often the only technology that can satisfy a product specification requiring a battery thinner than a credit card that still delivers days of continuous operation.

Medical Devices stands out as the fastest-growing application segment and is widely expected to hold that distinction throughout the 2026-2035 forecast window. The pull factors are compelling: implantable cardiac monitors, leadless pacemakers, drug delivery micropumps, continuous analyte sensors, and neuromodulation devices all represent markets where a battery failure is clinically serious, not merely inconvenient. Thin film solid-state batteries address this need exceptionally well they carry no liquid electrolyte to leak, maintain capacity over many years, and can be fabricated in custom shapes that conform to irregular implant geometries.

By Battery Type, Rechargeable segment dominates the Thin Film Battery Market, Disposable segment expected to grow fastest

Rechargeable thin film batteries held the larger share of the market in 2025 and that position looks durable well into the forecast period. The reason is straightforward: in consumer electronics and wearable devices, users expect to charge their devices rather than replace internal components, and manufacturers designing these products need a power source that can handle hundreds or thousands of charge-discharge cycles without degrading.

The Disposable segment, while smaller, is actually the faster-moving one, with a projected CAGR of approximately 23.61% running through 2035. The logic here is different: for single-use medical diagnostics, intelligent drug packaging, and one-time environmental sensors, a disposable cell is preferable precisely because there is no expectation or infrastructure for recharging. A blood glucose test strip with an embedded thin film battery, or a smart blister pack that logs medication adherence, only needs to work for a defined period often days or weeks and is then discarded along with the device.

By Battery Voltage, below 1.5V segment dominates the Thin Film Battery Market, above 3V segment expected to grow fastest

The below 1.5V segment carried approximately 45% of market revenue in 2025 and remains the workhorse of the thin film battery category. At these voltage levels, thin film cells power the broadest range of low-energy applications RFID tags, NFC labels, biosensors, hearing aids, and a wide variety of wearable health monitors that only need modest current draws over extended periods. The design characteristics of sub-1.5V thin film batteries align naturally with complementary low-power electronics: ARM Cortex-M0 microcontrollers, Bluetooth Low Energy transceivers, and low-power sensor readout ICs are all optimized to operate at these voltages, which keeps the overall system design compact and battery-friendly.

Above 3V thin film batteries are the smallest segment today but carry the fastest growth projection at roughly 23.54% CAGR through 2035. Higher voltage cells open the door to applications that cannot be served at lower voltages: active medical implants requiring more powerful stimulation currents, military-grade sensors operating in harsh environments without battery access, and advanced IoT nodes running edge AI inference locally rather than transmitting raw data.

Thin Film Battery Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

South Korea |

35% |

|

Middle East & Africa |

Israel |

30% |

|

Latin America |

Brazil |

48% |

North America Thin Film Battery Market Insights

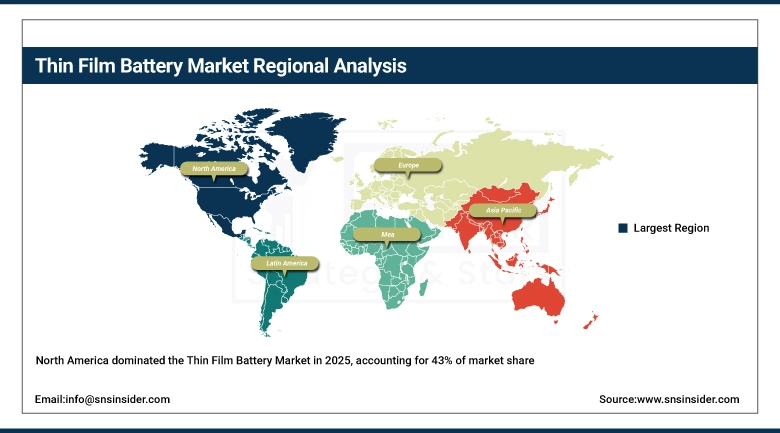

North America held the leading regional position in the Thin Film Battery Market in 2025 with approximately 43% revenue share. That position rests on a real foundation: the U.S. has more active thin film battery research programs, more implantable medical device companies, and more vertically integrated IoT hardware developers than any other region. The medical device cluster in Boston and Minneapolis, the consumer electronics supply chain influence flowing through California, and the defense electronics programs in the southeast all create sustained, sophisticated demand for high-performance thin film cells. Federal R&D investment through DARPA, NIH, and the DOE's Advanced Research Projects Agency-Energy (ARPA-E) has consistently funded the foundational materials science work that eventually becomes commercial thin film battery chemistry.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. Department of Energy's ARPA-E program has specifically funded projects targeting solid-state thin film battery architectures for grid-edge energy management and implantable medical applications, with several grantee companies having since progressed to commercial pilot production. ARPA-E's Batteries for Electrical Energy Storage in Transportation (BEST) and IONICS programs created significant intellectual property that continues to influence thin film cell design, particularly around high-conductivity solid electrolyte materials that are now entering commercial product lines.

Asia Pacific Thin Film Battery Market Insights

Asia Pacific is forecasted to grow at the fastest regional CAGR through 2035, building on the region's extraordinary depth in consumer electronics manufacturing, its rapidly growing medical device sector, and government-led investment in semiconductor and advanced materials capability. South Korea home to Samsung SDI and LG Chem, both of which have active thin film battery programs carries the largest single-country share within the region. Japan's well-established precision manufacturing industry and its leadership in industrial IoT applications provide a second important demand center. China's push into domestic battery technology development, backed by significant state investment, is steadily expanding the country's thin film battery production capability, and India's growing electronics manufacturing sector is beginning to emerge as a demand market as well.

South Korea's Ministry of Science and ICT has specifically allocated funding under the K-Battery initiative for next-generation solid-state and thin film battery technologies, identifying them as strategic materials for the country's future competitiveness in consumer electronics and electric mobility. The initiative has supported university-industry collaborative research programs focused on LiPON electrolyte optimization and high-throughput sputtering deposition techniques work that is directly feeding into commercial thin film battery product development at Korean conglomerates.

Europe Thin Film Battery Market Insights

Europe held approximately 22% of the global Thin Film Battery Market revenue in 2025, with strength concentrated in Germany, France, Sweden, and the Netherlands. Europe's thin film battery demand is driven by a distinctive combination of industrial IoT applications — Industry 4.0 sensor networks, smart factory asset tracking, and predictive maintenance nodes and a strong medical device manufacturing base in Germany, Switzerland, and the Netherlands. The EU's ambitious electronics recycling and product sustainability regulations are also pushing manufacturers toward rechargeable thin film configurations over primary batteries in regulated categories. Companies like Soleras Advanced Coatings in the Netherlands have built specialized thin film deposition capabilities that serve both research institutions and commercial battery manufacturers across the region.

The European Commission's Batteries Regulation (EU 2023/1542), which came into force in 2023 and is being phased in through 2027, imposes new performance, durability, and recycled content requirements for batteries placed in the EU market. For thin film batteries used in medical devices and industrial electronics categories specifically addressed in the regulation manufacturers must now demonstrate minimum cycle life performance and provide end-of-life collection data. This regulatory framework is prompting European medical device manufacturers to qualify next-generation thin film cells that exceed the minimum thresholds, effectively raising the technology bar and rewarding innovation in the segment.

Middle East & Africa and Latin America Thin Film Battery Market Insights

The Middle East & Africa and Latin America regions together represent a smaller but steadily developing portion of the global Thin Film Battery Market. In MEA, the primary drivers are defense and security electronics in Israel and the Gulf states, along with growing investment in smart city infrastructure across Saudi Arabia and the UAE that incorporates IoT sensor networks requiring compact, maintenance-free power. Israel's deep defense electronics industry has long been a user of specialized thin film battery configurations for wearable soldier systems and drone electronics. In Latin America, Brazil leads regional adoption through its medical device import and distribution channels, and the country's growing electronics manufacturing incentive programs are beginning to attract more investment in advanced components, including energy storage.

Saudi Arabia's Vision 2030 smart city programs including the NEOM project and the wider Smart Cities National Program have incorporated IoT infrastructure specifications that implicitly require compact, high-reliability power sources compatible with outdoor environmental sensors operating across temperature extremes. The Saudi Authority for Industrial Cities and Technology Zones (MODON) have created industrial zone incentives specifically targeting advanced electronics and energy storage manufacturers, which may attract thin film battery production capability to the region over the medium term.

Thin Film Battery Market Growth Drivers:

-

Explosive demand for miniaturized, flexible power sources across wearable health technology, implantable medical devices, and IoT-connected systems creating structural growth in the thin film battery sector

The underlying pull for thin film batteries is not coming from one industry it is coming from several simultaneously, which is what makes the market's growth trajectory so resilient. Wearable health monitoring has moved from fitness enthusiasts to clinical-grade continuous monitoring, and the devices driving that shift continuous glucose monitors, cardiac loop recorders, remote patient monitoring patches all need power that can be embedded into a flexible, body-conforming form factor without adding uncomfortable bulk. Simultaneously, the IoT buildout is creating literally billions of sensor nodes that need power for years at a time in locations where battery replacement is impractical, and thin film cells' exceptional shelf life and self-discharge characteristics make them the logical choice for those applications. Medical device development is converging on fully active implants that can stimulate, sense, and wirelessly communicate functions that demand reliable, biocompatible, long-lived power, which is precisely what solid-state thin film technology provides.

The U.S. National Institutes of Health (NIH) reports that active implantable device approvals and clinical trials have increased significantly over the past five years, particularly for neuromodulation, cardiac monitoring, and drug delivery applications. The NIH's National Institute of Biomedical Imaging and Bioengineering (NIBIB) has funded multiple research programs specifically targeting miniaturized power systems for next-generation implantables, identifying solid-state thin film batteries as a priority technology area given their unique combination of biocompatibility, form-factor flexibility, and demonstrated longevity in implanted environments.

Thin Film Battery Market Restraints:

-

Manufacturing complexity and high per-unit production costs relative to conventional batteries limiting rapid volume scaling and holding back penetration into cost-sensitive application categories

There is a real tension in the thin film battery market between the technology's technical elegance and the economic realities of commercializing it at scale. Physical vapor deposition and sputtering processes the primary manufacturing methods for high-performance thin film cells are slow relative to the wet chemistry processes used for conventional lithium-ion batteries. Equipment costs are high, throughput per machine is limited, and yield management in multi-layer thin film deposition is genuinely difficult. The result is a per-unit cost structure that remains well above conventional batteries for equivalent stored energy, which effectively prices thin film cells out of most mainstream consumer electronics applications where cost is the primary specification.

Thin Film Battery Market Opportunities:

-

Convergence of solid-state chemistry advances, roll-to-roll manufacturing maturation, and expanding active implantable device markets creating a wide window of commercial opportunity for thin film battery innovators through 2035

The opportunity picture for thin film batteries over the next decade is genuinely attractive for companies that can navigate the manufacturing challenge. Solid-state electrolyte chemistry is improving at a pace that should push energy density meaningfully higher without compromising the safety and stability that make thin film cells distinctive — and higher energy density directly expands the range of applications that are technically feasible. The active medical implant market is growing at rates that justify premium pricing, and regulatory pathways are becoming clearer as agencies like the FDA accumulate more clinical data on implanted thin film device performance. Smart packaging, which is still early-stage, could become a very large volume market as pharmaceutical traceability regulations tighten and food safety requirements evolve a single global regulation mandating active tamper evidence on prescription drugs, for instance, would create demand for hundreds of millions of embedded thin film cells annually. Companies that establish manufacturing scale and regulatory qualifications now will be positioned to capture that demand as it materializes.

Recent Developments:

-

2025: Samsung SDI announced the successful qualification of a new solid-state thin film battery cell designed specifically for next-generation smartwatch applications, featuring a 15% improvement in volumetric energy density over the previous generation and passing 1,000 charge-cycle testing without measurable capacity fade a result the company indicated would support product design lifespans of over four years of daily use.

-

2025: Front Edge Technology received a new U.S. Department of Defense contract for the development of radiation-hardened thin film lithium batteries intended for satellite and high-altitude unmanned vehicle applications, with the contract specifically targeting solid-state architectures capable of operating across a temperature range from -40°C to +85°C without performance degradation.

-

2024: STMicroelectronics expanded its EH4295 thin film solid-state battery product family with two new form factors targeting asset tracking tags and smart pharmaceutical packaging, citing growing pharmaceutical industry interest in active serialization and cold chain monitoring as the primary commercial driver for the expansion.

Thin Film Battery Companies are:

-

STMicroelectronics N.V.

-

Front Edge Technology, Inc.

-

Cymbet Corporation

-

Excellatron Solid State, LLC

-

BrightVolt, Inc.

-

TDK Corporation

-

Panasonic Energy Co., Ltd.

-

Murata Manufacturing Co., Ltd.

-

LG Chem Ltd.

-

Infinite Power Solutions (MFLEX)

-

Enfucell Oy

-

Blue Spark Technologies

-

Imprint Energy, Inc.

-

Polymerion GmbH

-

Solid Power, Inc.

-

Prieto Battery Inc.

-

Kurt J. Lesker Company Ltd.

-

Soleras Advanced Coatings B.V.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.68 Billion |

| Market Size by 2035 | USD 5.39 Billion |

| CAGR | CAGR of 22.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Voltage (Below 1.5V, 1.5 V to 3V, Above 3V), • By Battery Type (Disposable, Rechargeable), • By Application (Consumer Electronics, Medical Devices, Wearable Technology, Smart Cards, RFID, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cymbet Corporation, STMicroelectronics, Excellatron Solid State LLC, Blue Spark Technologies, BrightVolt, Enfucell Oy, Imprint Energy, Ilika plc, ProLogium Technology Co., Ltd., Front Edge Technology Inc., Jenax Inc., NEC Corporation, Panasonic Corporation, Samsung SDI Co., Ltd., LG Energy Solution, Solid Power Inc., QuantumScape Corporation, Murata Manufacturing Co., Ltd., Seiko Instruments Inc., Toshiba Corporation. |

Frequently Asked Questions

Ans: North America dominated the Thin Film Battery Market in 2025.

Ans: The Wearable Technology segment dominated the Thin Film Battery Market in 2025.

Ans: Explosive demand for miniaturized, flexible power sources across wearable health technology, implantable medical devices, and IoT-connected systems is the primary growth driver of the Thin Film Battery Market.

Ans: The Thin Film Battery Market was valued at USD 0.68 billion in 2025.

Ans: The Thin Film Battery Market is expected to grow at a CAGR of 22.99% from 2026 to 2035.

Get in Touch