Viral Vector Production (Research-use) Market Report Scope & Overview:

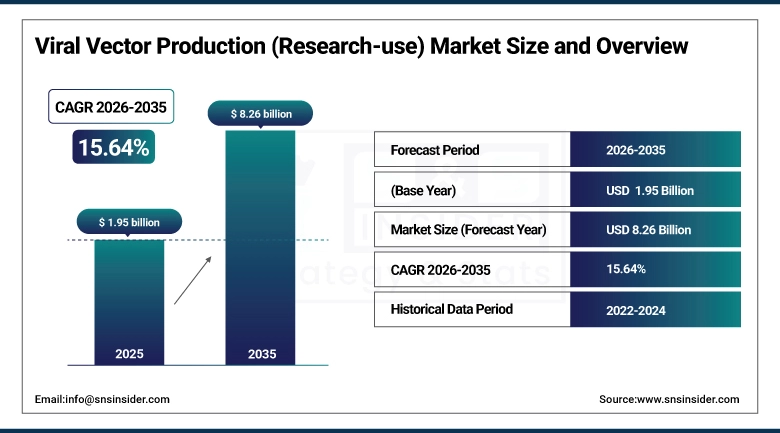

The Viral Vector Production (Research-use) Market was valued at USD 1.95 billion in 2025 and is expected to reach USD 8.26 billion by 2035, growing at a CAGR of 15.64% from 2026–2035.

The market for Viral Vector Production (Research-use) is experiencing substantial growth due to the accelerated development of gene therapy and cell therapy pipelines, escalating demand for viral vectors in pre-clinical and translational studies, and the burgeoning interest in advanced biologics development. The rising incidence of genetic, cancer, and rare disorders is leading to an increased requirement for effective gene delivery tools like AAV and lentiviral vectors. Innovations in scaling-up of upstream processes, high-efficiency transfection methods, suspension cell culture systems, and downstream automation techniques are revolutionizing viral vector manufacturing in research environments.

Supporting this trend, the Alliance for Regenerative Medicine has reported a continuous increase in gene and cell therapy clinical trials globally, with thousands of active programs highlighting the critical dependence on reliable viral vector production systems for research and early-stage development.

In parallel, regulatory and technological advancements are supporting market expansion. The U.S. Food and Drug Administration has been actively granting approvals and designations for gene therapy products, encouraging innovation and accelerating demand for high-quality research-grade viral vectors used in early development stages.

Viral Vector Production (Research-use) Market Size and Forecast

-

Market Size in 2025: USD 1.95 Billion

-

Market Size by 2035: USD 8.26 Billion

-

CAGR: 15.64% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Viral Vector Production (Research-use) Market - Request Free Sample Report

Viral Vector Production (Research-use) Market Trends

-

Rapid expansion of gene therapy and cell therapy pipelines is significantly increasing demand for high-quality viral vectors in preclinical and translational research.

-

Growing adoption of AAV and lentiviral vector platforms is improving gene delivery efficiency and enabling broader therapeutic applications across rare diseases and oncology.

-

Increasing shift toward outsourced viral vector production through CDMOs is enhancing scalability, reducing turnaround time, and optimizing research workflows.

-

Advancements in suspension cell culture systems and serum-free media technologies are improving production yield, consistency, and cost-efficiency.

-

Rising integration of automation and closed-system manufacturing platforms is minimizing contamination risks and improving reproducibility in research-grade vector production.

-

Expanding use of AI-driven process optimization and digital bioprocessing tools is accelerating vector development timelines and improving batch success rates.

-

Growing demand for high-titer, high-purity viral vectors is driving innovation in downstream purification technologies and chromatography systems.

-

Increasing investments from biotech firms, venture capital, and government funding programs are accelerating innovation and infrastructure development in viral vector production.

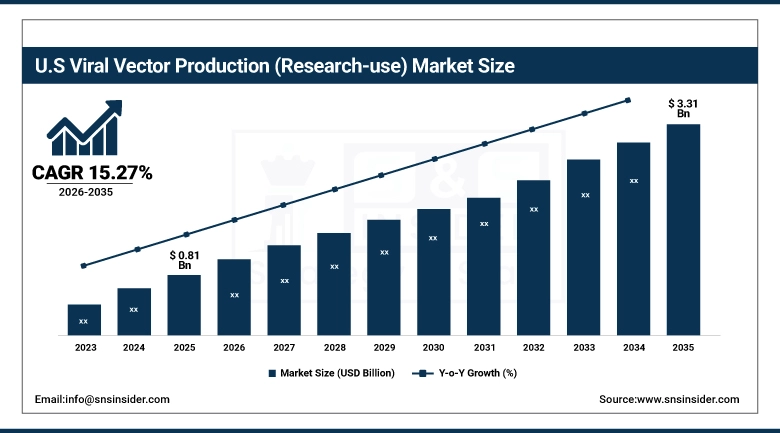

U.S. Viral Vector Production (Research-use) Market was valued at USD 0.81 billion in 2025 and is expected to reach around USD 3.31 billion by 2035, growing at a CAGR of 15.27% from 2026–2035.

The United States Viral Vector Production (Research-use) Market has been observed as the biggest in the world due to its advanced biotech ecosystem, significant presence of cell therapy and gene therapy companies, and substantial academic-industry collaboration efforts. High use of adeno-associated virus and lentivirus vector systems, rising dependence on contract development and manufacturing organizations for large-scale research vector production, and the latest advancements in the areas of upstream and downstream processing technologies are some key factors fueling market growth. Some of the prominent players are Thermo Fisher Scientific, Lonza, Merck KGaA, and Catalent.

Supporting this growth, the National Institutes of Health continues to fund a large number of gene therapy and advanced biologics research programs, reinforcing sustained demand for high-quality viral vectors in preclinical and translational studies.

In addition, regulatory progress by the U.S. Food and Drug Administration in approving and fast-tracking gene therapy products is accelerating innovation cycles and increasing the need for reliable research-grade vector production, strengthening the U.S. position as a global hub for advanced therapy development.

Viral Vector Production (Research-use) Market Segment Highlights

-

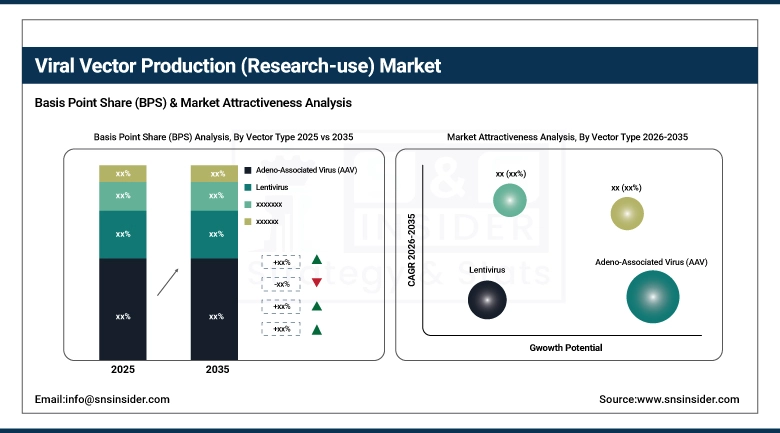

By Vector Type, Adeno-Associated Virus (AAV) dominated the Viral Vector Production (Research-use) Market with 38.36% share in 2025; Lentivirus is the fastest-growing segment.

-

By Workflow, Downstream Processing dominated the market with 49.45% share in 2025; Upstream Processing is the fastest-growing segment.

-

By Application, Gene Therapy Development dominated the market with 41.24% share in 2025; Cell Therapy Research is the fastest-growing segment.

-

By End User, Biotech & Pharma Companies dominated the market with 43.51% share in 2025; Contract Research Organizations (CROs) are the fastest-growing segment.

By Vector Type, Adeno-Associated Virus (AAV) segment dominates the Viral Vector Production (Research-use) Market, Lentivirus segment expected to grow fastest

In 2025, the Adeno-Associated Virus (AAV) segment maintained its dominant position in the Viral Vector Production (Research-use) Market, accounting for 38.36% of total revenue. Such leadership can be attributed to the high level of safety associated with this technology, along with its lower immunogenic properties and its excellent compatibility with in vivo gene delivery. Adeno-associated viral vectors have found widespread use in preclinical and translational research, owing to their efficacy in delivering long-term gene expression and the regulatory acceptability of gene therapies.

From 2026 to 2035, the Lentivirus segment is projected to record the highest CAGR of 16.37%. The rapid expansion of ex vivo gene-modified cell therapies, including CAR-T and stem cell-based therapies, is significantly accelerating demand for lentiviral vectors.

By Workflow, Downstream Processing segment dominates the Viral Vector Production (Research-use) Market, Upstream Processing segment expected to grow fastest

The Downstream Processing segment held the largest share of 49.45% in 2025, driven by the complexity of purification, concentration, and quality control steps required to achieve high-purity viral vectors. The need for removal of host cell proteins, DNA contaminants, and empty capsids has made downstream processes resource-intensive and technologically critical.

The Upstream Processing segment is expected to register the highest CAGR of 16.30% during the 2026–2035 forecast period. Increasing adoption of high-efficiency transfection methods, suspension cell culture systems, and bioreactor-based production platforms is improving scalability and yield.

By Application, Gene Therapy Development segment dominates the Viral Vector Production (Research-use) Market, Cell Therapy Research segment expected to grow fastest

The Gene Therapy Development segment held the largest share of 41.24% in 2025, Due to the growing interest in developing treatments based on gene therapy for rare diseases, oncology, and genetic disorders, there is an increase in the gene therapy pipeline. The importance of viral vectors, especially adeno-associated virus (AAV), in gene delivery is high in this segment, since they have become indispensable in this early-stage technology.

The Cell Therapy Research segment is expected to record the highest CAGR during the forecast period.

By End User, Biotech & Pharma Companies segment dominates the Viral Vector Production (Research-use) Market, Contract Research Organizations (CROs) segment expected to grow fastest

The Biotech & Pharma Companies segment maintained the highest end-user share of 43.51% in 2025. These advantages are facilitated by high investments in gene and cell therapy research and development, growing pipelines at the early stage, and the requirement for a stable viral vector manufacturing process to facilitate pre-clinical and clinical trials. The larger biotech companies are consistently building up their capacity internally and externally.

The Contract Research Organizations (CROs) segment is projected to achieve the highest growth rate, during 2026–2035.

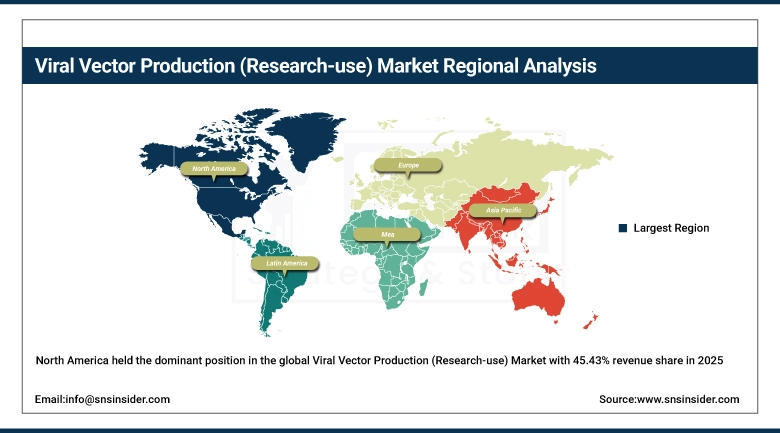

Viral Vector Production (Research-use) Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

45.43% |

|

Europe |

Germany |

26.14% |

|

Asia Pacific |

China |

20.75% |

|

Middle East & Africa |

UAE |

4.04% |

|

Latin America |

Brazil |

3.64% |

North America Viral Vector Production (Research-use) Market Insights

North America held the dominant position in the global Viral Vector Production (Research-use) Market with 45.43% revenue share in 2025, driven by its extremely sophisticated biotech cluster, intense localization of gene and cell therapy players, and high level of industry-academia cooperation. This area has early adoption of the AAV and Lentiviral vectors, well-established translational investments, as well as presence of top-notch CDMOs and bio-processing solution providers. USA represents % of regional market share, thanks to its large gene therapy pipeline, substantial venture investment and continuous expansion of viral vector manufacturing capacity.

Supporting this dominance, the National Institutes of Health continues to fund a significant number of gene therapy and rare disease research programs, reinforcing sustained demand for high-quality viral vectors in early-stage development.

Additionally, the U.S. Food and Drug Administration is actively advancing regulatory pathways for gene therapies, accelerating clinical translation and increasing the need for reliable research-grade vector production platforms.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Viral Vector Production (Research-use) Market Insights

The Asia Pacific region is projected to experience the highest CAGR of 16.93% from 2026-2035 due to the rapid expansion of the biotechnology sector, the rising tendency of outsourcing vector manufacturing services, and the favorable government policies for developing therapies through advanced techniques. China, India, Japan, South Korea, and Singapore are expected to drive the market growth, where China will make contributions toward revenue generation through the country's extensive investments in R&D and CDMO services for gene therapy.To support this market growth, the National Health Commission of China has made biotechnological innovation and gene therapy its priority in national healthcare strategies.

Supporting this growth, the National Health Commission of China has prioritized biotechnology innovation and gene therapy development under national healthcare strategies, accelerating research activities and infrastructure development.

Rapid expansion of domestic CDMO capacity in China and India, along with government-backed biotech hubs and gene therapy initiatives, is transforming the region into a global outsourcing and scalable production hub for viral vectors

Europe Viral Vector Production (Research-use) Market Insights

Europe held a significant share of the total revenue market in 2025 due to its solid networks of academic research, its mature biopharmaceutical sector, and its increasing interest in the development of advanced therapy medicinal products (ATMPs). Nations such as Germany, the United Kingdom, France, and Switzerland have been leading the adoption of these treatments because of their collaborative research efforts and their increasing capabilities in producing viral vectors.In support of this claim, the European Commission has increased its funding through programs

Supporting this position, the European Commission has expanded funding under programs such as EU4Health and Horizon Europe, promoting innovation in advanced therapies and supporting early-stage research infrastructure.

Additionally, increasing integration of automated bioprocessing technologies and expansion of specialized CDMOs are strengthening Europe’s role in viral vector development and research-scale production.

Latin America, Middle East & Africa (LAMEA) Viral Vector Production (Research-use) Market Insights

Both the Latin America and the Middle East and Africa markets have been registering consistent growth in the market for Viral Vector Production (for Research), due to better infrastructural developments in biotechnology, growing involvement in global clinical trials, and higher awareness levels regarding novel therapeutic treatments. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are proving to be significant contributors to the market, especially in association with international biotech companies.

Governments in the Middle East, particularly UAE and Saudi Arabia, are investing in precision medicine programs and biotech innovation hubs, enabling early-stage adoption of viral vector technologies and fostering regional research and clinical capabilities

In the Middle East, Saudi Arabia’s Ministry of Health under Vision 2030 is actively promoting biotechnology innovation and research infrastructure development, including support for advanced biologics and gene therapy research, contributing to increasing demand for viral vector production capabilities.

Viral Vector Production (Research-use) Market Growth Drivers:

-

Rapid expansion of gene therapy and cell therapy pipelines is driving exponential demand for high-quality viral vectors in research and early-stage development worldwide

The primary structural factor driving the market for the Viral Vector Production (Research-use) is the fast-growing pipeline of gene and cell therapies for rare diseases, cancers, and genetic conditions. The biopharmaceutical companies are now focusing on developing more advanced therapies where an effective means of delivering genes is needed, and AAV and lentiviral vectors are considered ideal candidates in this regard. With the growing development and testing of advanced therapies for treating diseases, the requirement for viral vectors is increasing rapidly. The applications of these viral vectors extend to complex areas such as CAR-T cells and in vivo gene editing.

Supporting this growth, the Alliance for Regenerative Medicine reports that there are over 2,000 active gene and cell therapy clinical trials globally, highlighting the massive and growing dependence on viral vectors for research and early-stage development.

Additionally, regulatory momentum from the U.S. Food and Drug Administration, including increasing approvals and fast-track designations for gene therapies, is accelerating innovation cycles and reinforcing demand for high-quality research-use viral vector production platforms.

Viral Vector Production (Research-use) Market Restraints:

-

High production costs and complex manufacturing workflows for viral vectors are creating significant scalability and accessibility barriers, particularly for small biotech firms and academic research institutions

The primary constraint in the Viral Vector Production (Research-use) Market is the complex and expensive process involved in the production of viral vectors. The production of high-quality viral vectors, such as AAV and lentivirus, demands a unique setup that includes clean rooms, bioreactors, purification equipment, among others, and qualified technical staff. This adds greatly to the costs, thus posing great difficulty for biotech firms and academic organizations to develop the capacity to produce these vectors themselves. Other constraints in upstream include inefficiency in transfection and in downstream purification and elimination of impurities.

Viral Vector Production (Research-use) Market Opportunities:

-

Emergence of next-generation vector engineering and scalable production platforms is creating new growth pathways for broader therapeutic applications and faster research translation

The next round of developments within the Viral Vector Production (Research-use) market will revolve around enhanced capabilities for vector design, as well as scalability and flexibility of production processes for more advanced gene and cell therapies. The development of techniques like capsid modification, tissue-specific delivery vectors, and high-carrying capacity viruses allows for expansion of targetable diseases as well as increased transduction efficacy and safety. On the other hand, the trend towards module, single-use bioprocessing systems and continuous manufacturing decreases the demands on infrastructure and speeds up vector manufacturing.

Recent Developments:

-

2026: Thermo Fisher Scientific expanded its viral vector development and manufacturing network with new research-use production capabilities and process optimization platforms, aimed at accelerating gene therapy pipelines and improving scalability for AAV and lentiviral vectors across early-stage research programs.

-

2026: Lonza Group advanced its modular viral vector manufacturing platforms by integrating automated, closed-system bioprocessing technologies to enhance yield consistency and reduce turnaround time for research-grade vector production.

-

2025: FUJIFILM Diosynth Biotechnologies expanded its viral vector production capacity in North America and Europe, strengthening support for preclinical and early clinical-stage gene therapy development, particularly in AAV-based applications.

-

2025: Catalent Inc. enhanced its gene therapy CDMO capabilities through facility upgrades and process innovations focused on improving viral vector yield, purity, and scalability, supporting increasing demand from biotech firms advancing cell and gene therapy pipelines.

Viral Vector Production (Research-use) Market Key Players

Some of the Viral Vector Production (Research-use) Market Companies

-

Lonza Group AG

-

Thermo Fisher Scientific Inc.

-

Merck KGaA

-

FUJIFILM Diosynth Biotechnologies

-

Catalent Inc.

-

Oxford Biomedica plc

-

Charles River Laboratories (Cognate BioServices / Cobra Biologics)

-

WuXi AppTec Co. Ltd.

-

AGC Biologics

-

Takara Bio Inc.

-

Genezen

-

YPOSKESI

-

Batavia Biosciences B.V.

-

VGXI Inc.

-

Vigene Biosciences Inc.

-

Waisman Biomanufacturing

-

Advanced BioScience Laboratories Inc.

-

SIRION Biotech GmbH

-

Miltenyi Biotec GmbH

-

Virovek Inc.

Viral Vector Production (Research-use) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.95 Billion |

| Market Size by 2035 | USD 8.26 Billion |

| CAGR | CAGR of 15.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vector Type (Adeno-Associated Virus (AAV), Lentivirus, Adenovirus, Retrovirus, Others) • By Workflow (Upstream Processing, Downstream Processing, Fill & Finish, Others) • By Application (Gene Therapy Development, Cell Therapy Research, Vaccine Development, Others) • By End-User (Academic & Research Institutes, Biotech & Pharma Companies, Contract Research Organizations (CROs), Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lonza Group AG, Thermo Fisher Scientific Inc., Merck KGaA, FUJIFILM Diosynth Biotechnologies, Catalent Inc., Oxford Biomedica plc, Charles River Laboratories (Cognate BioServices / Cobra Biologics), Wuxi AppTec Co. Ltd., AGC Biologics, Takara Bio Inc., Genezen, YPOSKESI, Batavia Biosciences B.V., VGXI Inc., Vigene Biosciences Inc., Waisman Biomanufacturing, Advanced BioScience Laboratories Inc., SIRION Biotech GmbH, Miltenyi Biotec GmbH, Virovek Inc. |

Frequently Asked Questions

North America dominated the Viral Vector Production (Research-use) Market in 2025.

The Adeno-Associated Virus (AAV) segment dominated the Viral Vector Production (Research-use) Market in 2025.

Rapid expansion of gene therapy and cell therapy pipelines is the primary growth driver of the Viral Vector Production (Research-use) Market.

The Viral Vector Production (Research-use) Market was valued at USD 1.95 billion in 2025.

The Viral Vector Production (Research-use) Market is expected to grow at a CAGR of 15.64% from 2026 to 2035.

Get in Touch