Occupancy Sensor Market Report Scope & Overview:

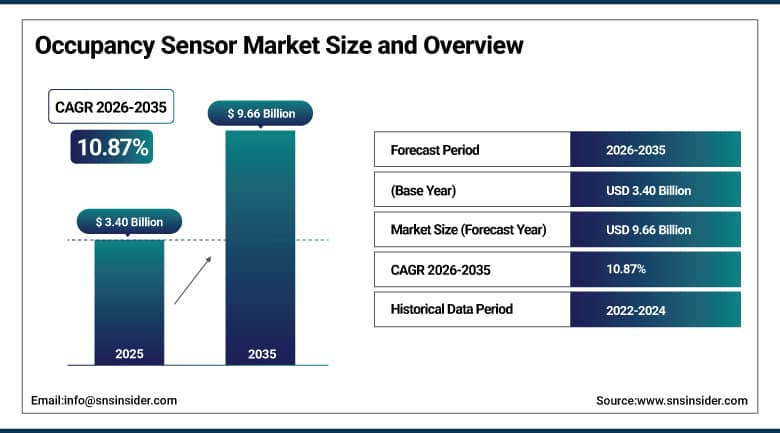

Occupancy Sensor Market was valued at USD 3.40 billion in 2025 and is expected to reach USD 9.66 billion by 2035, growing at a CAGR of 10.87% from 2026-2035.

Occupancy Sensor Market is expected to be propelled by the growing use of intelligent building automation technology and high demand for efficient lighting and HVAC controls. Increased usage of IoT technology in residential, commercial, and industrial infrastructures will also contribute towards growth in demand. Rising emphasis on sustainability and green buildings, along with cost savings on energy utilization, will drive market demand. Urbanization and smart cities initiatives are also playing an important role in promoting the widespread adoption of occupancy sensing technology.

The U.S. Department of Energy's 2023 Building Energy Data Book documents that commercial buildings account for approximately 18% of total U.S. energy consumption, with lighting and HVAC systems accounting for over 70% of building energy use the sectors that occupancy sensors most directly impact.

The American Council for an Energy-Efficient Economy estimates that full commercial building automation including occupancy sensing could reduce U.S. building energy consumption by 29% relative to 2023 levels.

Occupancy Sensor Market Size and Forecast

-

Market Size in 2025: USD 3.40 Billion

-

Market Size by 2035: USD 9.66 Billion

-

CAGR: 10.87% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Occupancy Sensor Market - Request Free Sample Report

Occupancy Sensor Market Trends

-

Rising demand for energy-efficient building automation systems is driving the occupancy sensor market.

-

Growing adoption across residential, commercial, and industrial buildings is boosting market growth.

-

Expansion of smart homes, smart offices, and smart city infrastructure is fueling sensor deployment.

-

Increasing focus on automated lighting, HVAC control, and space utilization optimization is shaping adoption trends.

-

Advancements in infrared, ultrasonic, and microwave sensing technologies are enhancing accuracy and reliability.

-

Rising emphasis on sustainability, energy conservation, and operational cost reduction is supporting market expansion.

-

Collaborations between sensor manufacturers, building management system providers, and construction firms are accelerating innovation and global adoption.

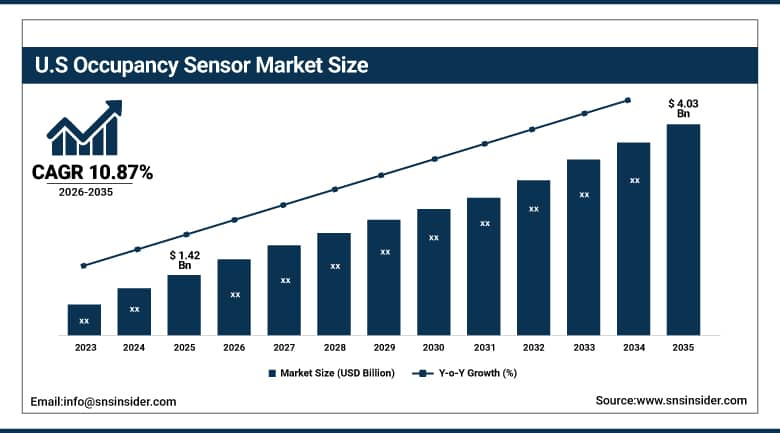

U.S. Occupancy Sensor Market was valued at USD 1.42 billion in 2025 and is expected to reach USD 4.03 billion by 2035, growing at a CAGR of 10.87% from 2026-2035.

The United States occupancy sensor market is expanding owing to high adoption rate of smart building automation technologies and escalating demand for energy-efficient lighting and HVAC control. The increasing emphasis on sustainability, green buildings, and intelligent commercial infrastructures is adding momentum to the growth of this market in the country.

The General Services Administration's Federal Building Program mandate requiring occupancy sensor installation in all new and renovated federal buildings creates a recurring government procurement stream for occupancy sensing technology.

ASHRAE 90.1 Energy Standard for Buildings Except Low-Rise Residential Buildings mandates occupancy sensors in a broad range of commercial space types, making code compliance a baseline occupancy sensor demand driver in U.S. construction.

Occupancy Sensor Market Segment Analysis

-

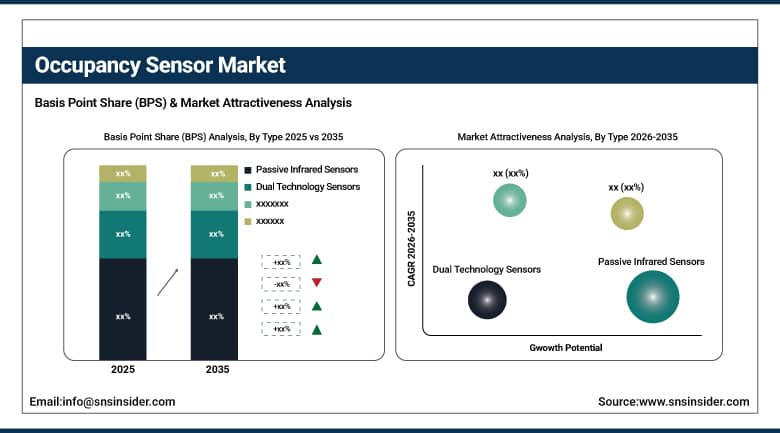

By Type, Passive Infrared Sensors segment dominated the Occupancy Sensor Market in 2025 with ~52% share; Dual Technology Sensors segment is fastest growing (CAGR).

-

By Connectivity, Wired segment dominated the Occupancy Sensor Market in 2025 with ~58% share; Wireless segment is fastest growing (CAGR).

-

By Application, Lighting Control segment dominated the Occupancy Sensor Market in 2025 with ~44% share; Energy Management segment is fastest growing (CAGR).

-

By End Use, Commercial segment dominated the Occupancy Sensor Market in 2025 with ~46% share; Residential segment is fastest growing (CAGR).

By Type, Passive Infrared Sensors segment dominates the Market, Dual Technology Sensors segment expected to grow fastest

Passive infrared sensors dominate the Occupancy Sensor Market owing to their economic feasibility, robust reliability, and easy operation through change in heat and movement levels. They find application in automatic lighting controls and security applications in buildings. Besides their economic benefits, they also consume little power and are quite easy to install and maintain. Their strong compatibility with building automation and management systems is another important factor behind their increased adoption in infrastructure projects and energy-saving buildings.

The dual technology sensors are witnessing high growth rates due to their use of various techniques such as infrared and ultrasonic. Dual technology sensors are suitable for places where precise and reliable detection of occupancy is needed. The dual technique ensures high accuracy, flexibility to adapt to changing lighting conditions and movements in the environment. There is rising demand for smart buildings that require efficient building automation and energy management solutions.

By Connectivity, Wired segment dominates the Market, Wireless segment expected to grow fastest

Wired connectivity leads in the market owing to the constant nature of its functioning, stability, and reliability. It has a constant power source, which ensures efficient performance. The application of the technology has been observed in larger commercial buildings and factories. The wired connection provides a secure environment for signals to pass through without any disturbance. The longevity of its use and minimal chances of interruptions make it the best choice for such purposes as building automation and energy conservation.

Wireless occupancy sensors are growing rapidly owing to their easy installation process, adaptability, and minimal infrastructural demands. These wireless occupancy sensors do away with the requirement of wiring, thus making them highly appropriate for use in retrofitted constructions along with smart infrastructures. Further innovations in technologies like IoT integration and efficient power consumption are improving the capabilities of wireless occupancy sensors.

By Application, Lighting Control segment dominates the Market, Energy Management segment expected to grow fastest.

Lighting control dominates the Occupancy Sensor Market because of their contribution to the field of energy savings and automation of lighting management systems. Such sensors allow lights to function only when there are people present within the particular space, which ensures minimal energy wastage. The sensors are commonly used in office buildings, schools, and commercial structures. Increasing awareness about green building concepts is boosting their adoption rate.

Energy Management is expected to be the fastest growing application, driven by the growing focus on the optimized usage of energy, which has been observed across all organizations today. Occupancy sensors can help in the optimization of energy usage, especially in terms of space occupancy. With the increasing adoption of smart grid technology and Internet of Things (IoT), the segment is expected to show rapid growth.

By End Use, Commercial segment dominates the Market, Residential segment expected to grow fastest.

Commercial segment holds major shares in the market owing to the presence of a wide number of occupancy sensors installed in offices, retail stores, hospitals, and schools. The requirement of efficient lighting controls, space management, and reduced energy consumption makes this technology a favorable choice for such places. Increased focus on automation of buildings and compliance with energy efficiency regulations contribute towards the growth in the market for the same. Installation of occupancy-based sensor control systems is being undertaken in large scale infrastructure development activities and sustainability programs initiated by businesses.

Residential segment is expected to register fastest growth due to the increased use of smart home technology and energy efficiency concerns. Individuals have been installing occupancy sensors in their homes for controlling lighting systems, security systems, and other HVAC equipment in order to make life easier and minimize electricity bills. Increasing popularity of smart homes along with cost effective sensors drives the adoption.

Occupancy Sensor Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

48% |

North America Occupancy Sensor Market Insights

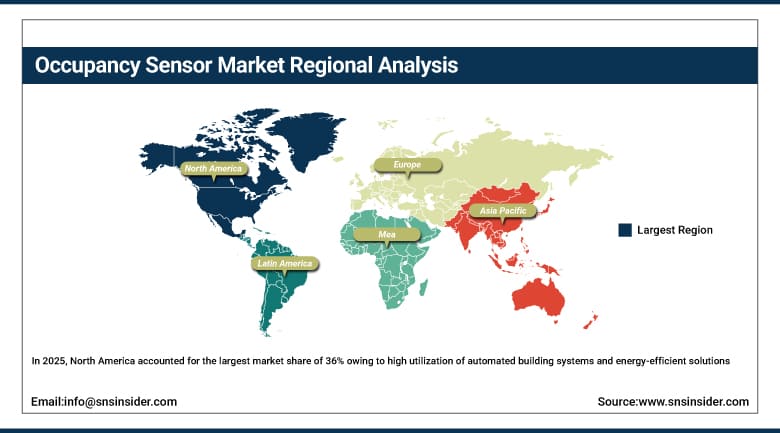

In 2025, North America accounted for the largest market share of 36% owing to high utilization of automated building systems and energy-efficient solutions. The presence of smart infrastructure powered by IoT in commercial buildings, healthcare settings, and residential applications is driving market growth. Regulations related to energy efficiency and sustainability also contribute to the growth of this market. The presence of technology giants along with the rapid adoption of wireless sensors and AI-driven sensors is also a key factor supporting the dominance of this region in the global market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Occupancy Sensor Market Insights

The Asia Pacific market for Occupancy Sensors is expected to witness highest regional growth due to high rates of urbanization, building constructions, and deployment of Internet of Things (IoT)-enabled home automation systems. High investments made in infrastructure, automation technology, and energy saving solutions are fueling increased demand. High consciousness levels about energy-saving and smart cities programs by governments are contributing to market growth. Increased use of wireless sensors and affordability of smart devices are boosting adoption rates.

China's Ministry of Housing and Urban-Rural Development reports that over 2 billion square meters of green-certified building area has been certified under the Green Building Star Standard since 2006, with occupancy sensing a standard inclusion in 3-star certified buildings that represent the top tier of Chinese commercial construction quality.

Europe Occupancy Sensor Market Insights

The Europe Occupancy Sensor Market is experiencing consistent growth due to its focus on energy-efficient regulations, building automation, and sustainability efforts. The installation of automated systems in office buildings, healthcare facilities, and educational organizations has been aiding in driving the demand for occupancy sensors. Europe is known to have strict environmental policies that encourage lower energy usage and fewer greenhouse gas emissions. The growing implementation of Internet of Things (IoT)-based systems, wireless sensors, and smart lighting systems is expected to increase the adoption of occupancy sensors.

Middle East & Africa and Latin America Occupancy Sensor Market Insights

Occupancy Sensor Market in Middle East & Africa and Latin America has been growing steadily owing to increased construction activities and expansion in commercial infrastructure, apart from rising incorporation of smart technology. The need for energy efficiency and economy of operations in utilities is adding impetus to the use of occupancy sensors in lighting and heating applications. Initiatives towards developing smart cities along with urban development projects are further contributing to the demand in the region. The lack of awareness and financial limitations in some areas are hindering market penetration.

Occupancy Sensor Market Growth Drivers:

-

Increasing Adoption of IoT Enabled Smart Homes and Intelligent Infrastructure Development Across Urbanized Regions Worldwide Today Driving Market Expansion

Increasing urbanization and rising usage of smart home technology have created high demands for occupancy sensors in the global market. Occupancy sensors find extensive use in the residential sector for automated lighting systems, security installations, and optimizing energy consumption. Increasing use of IoT-enabled devices and connected networks makes it easier to integrate occupancy sensing capability with smart assistants and home automation solutions. In the commercial sector, improvements in intelligent infrastructure have contributed towards increased efficiency by providing automated energy management and optimizing space usage. Digital transformation initiatives in cities have fueled market growth worldwide.

Occupancy Sensor Market Restraints:

-

Limited Awareness and Technical Expertise in Developing Regions Hindering Efficient Deployment and Utilization of Advanced Occupancy Sensing Technologies

Inability to understand the value-added features of occupancy sensors and their ability to save energy is limiting market expansion in many emerging markets. End users are still depending on traditional lighting systems and control techniques owing to lack of awareness about modern technology such as automated systems. Lack of skilled personnel to ensure proper installation and optimize the systems is an additional limitation faced by many end users. Inability to comprehend the integration of occupancy sensors with Internet-of-Things technologies and building management systems makes it difficult for end users to utilize advanced features of these systems.

Occupancy Sensor Market Opportunities:

-

Expanding Smart City Development and Government Led Energy Efficiency Programs Creating Strong Growth Opportunities for Occupancy Sensor Technologies Globally

The increase in the investments in the development of smart cities and initiatives taken by the governments to improve energy efficiency are creating several opportunities in favor of the installation of occupancy sensors. The initiative taken by the governments worldwide for promoting smart infrastructure development is intended to conserve energy and ensure urban sustainability. The use of occupancy sensors is made in the lighting applications, traffic management applications, and energy conservation applications in buildings run by the government organizations. Smart grid technology and smart city management solutions are playing an important role in fueling the demand.

Recent Developments:

-

2026: Honeywell International launched its Metrologic Series 4 AI-powered occupancy sensor with integrated radar and PIR dual-sensing, on-device machine learning that distinguishes between temporary passage and sustained occupancy, and direct BACnet/IP integration that enables plug-and-play connectivity with over 95% of commercial building management systems - reporting 99.2% occupancy detection accuracy and less than 0.1% false trigger rate in 1,000-room commercial deployment validation.

-

2025: Signify (Philips Lighting) launched its Interact Office occupancy intelligence platform with dense sensor deployment reaching per-desk resolution, real-time occupancy heatmaps accessible through browser-based dashboards, and Microsoft 365 calendar integration that correlates sensor-detected occupancy with meeting bookings to identify systematic space booking versus actual attendance gaps - enabling corporate real estate teams to identify specific meeting room types that generate the highest no-show rates.

-

2025: Johnson Controls released its NSW8000 Series Wireless Network Sensor combining occupancy detection, temperature, humidity, CO2, and volatile organic compound sensing in a single IoT device with 5-year battery life - enabling retrofit deployments in existing buildings without any wiring work while providing the multi-parameter environmental data that WELL Building Standard certification requires alongside occupancy sensing.

Occupancy Sensor Market Key Players

Some of the Occupancy Sensor Market Companies

-

Signify

-

Honeywell International

-

Schneider Electric

-

Johnson Controls

-

Acuity Brands

-

Legrand

-

Leviton Manufacturing

-

Lutron Electronics

-

Siemens

-

Eaton Corporation

-

GE Current

-

Hubbell Incorporated

-

Panasonic Corporation

-

Bosch

-

Texas Instruments

-

Omron Corporation

-

Delta Electronics

-

Crestron Electronics

-

OPTEX

-

Enerlites

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.40 Billion |

| Market Size by 2035 | USD 9.66 Billion |

| CAGR | CAGR of 10.87% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Passive Infrared Sensors, Ultrasonic Sensors, Dual Technology Sensors, Photoelectric Sensors) • By Connectivity (Wired, Wireless) • By Application (Lighting Control, HVAC Control, Security Systems, Energy Management) • By End Use (Residential, Commercial, Industrial, Institutional) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Signify, Honeywell International, Schneider Electric, Johnson Controls, Acuity Brands, Legrand, Leviton Manufacturing, Lutron Electronics, Siemens, Eaton Corporation, GE Current, Hubbell Incorporated, Panasonic Corporation, Bosch, Texas Instruments, Omron Corporation, Delta Electronics, Crestron Electronics, OPTEX, Enerlites |

Frequently Asked Questions

Ans: North America dominated in 2025; Asia Pacific is the fastest growing regional market.

Ans: Lighting Control dominated; Energy Management is growing at the fastest CAGR.

Ans: Passive Infrared Sensors dominated in 2025; Dual Technology Sensors is the fastest growing segment.

Ans: The Occupancy Sensor Market was valued at USD 3.40 billion in 2025.

Ans: The Occupancy Sensor Market is expected to grow at a CAGR of 10.87% from 2026 to 2035.

Get in Touch